- Hardware & Software IT Services

- IoT Analytics Market

IoT Analytics Market Size, Share, and Growth Forecast 2026 - 2033

IoT Analytics Market by Component (Services, Systems, and Solutions), Deployment Mode (On-premises and Cloud-based), Industry Vertical (Government and Defense, Energy and Utilities, Healthcare, IT and Telecom, Transportation and Logistics, Manufacturing, and Others), and Regional Analysis, 2026 - 2033

IoT Analytics Market Size and Share Analysis

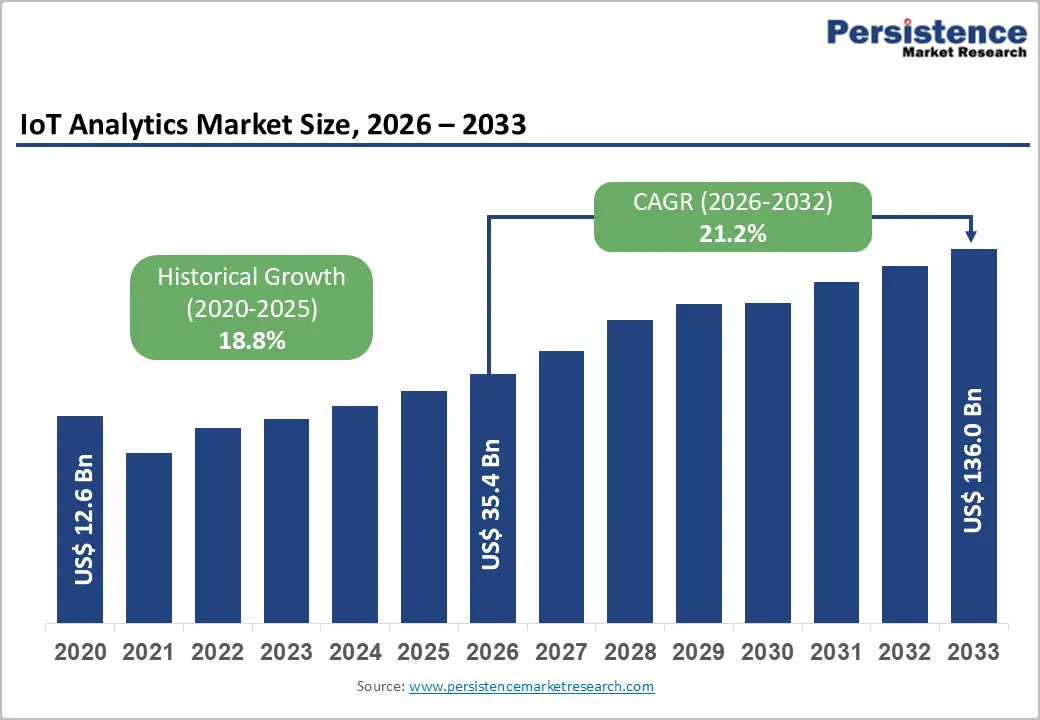

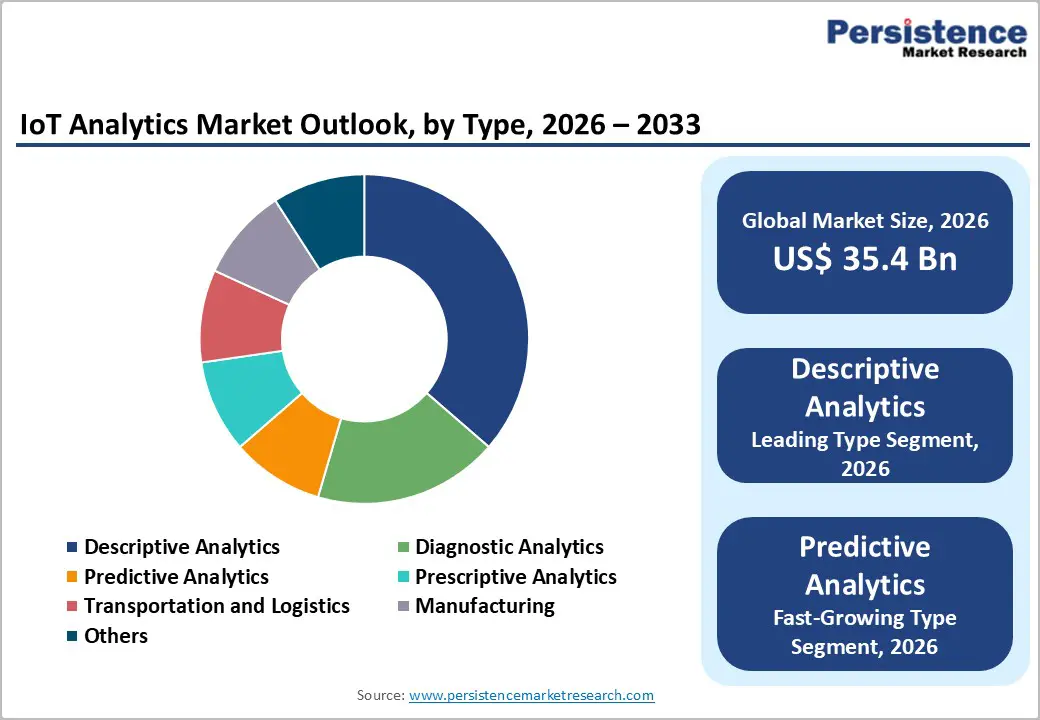

The global IoT Analytics market size was valued at US$ 35.4 billion in 2026 and is projected to reach US$ 136.0 billion by 2033, growing at a CAGR of 21.2% between 2026 and 2033.

The market expansion is primarily driven by the exponential growth in connected IoT devices, accelerated adoption of Industry 4.0 initiatives across manufacturing sectors, and the integration of artificial intelligence and machine learning technologies into analytics platforms. According to recent projections, the number of connected IoT devices worldwide is estimated to reach 45 billion by 2033, representing a compound annual growth rate of approximately 13.2% from 2026.

Key Market Highlights

- Leading Region: North America dominates the IoT Analytics market, with approximately 38.5% global market share, driven by mature digital infrastructure, substantial enterprise investment in Industry 4.0 implementations, advanced cloud adoption exceeding 94%, and Microsoft's leadership, capturing 45% of cloud AI case studies globally.

- Fastest Growing Region: Asia Pacific represents the fastest-growing regional market with a projected CAGR of 24.6%, fueled by rapid industrialization in China and Vietnam, India's 14% year-over-year IoT spending growth, government smart city investments, and combined $52.5 billion in AI infrastructure investments from Microsoft and Amazon.

- Dominant Component: Predictive Maintenance application dominates with approximately 45% market share, driven by the business-critical importance of equipment reliability, demonstrated ROI reducing downtime by 50% and maintenance costs by 25%, and widespread deployment across manufacturing, energy, and transportation industries.

- Growing Deployment Mode: Cloud-based deployment is the fastest-growing segment, expanding at a 21.8% CAGR, driven by superior scalability, financial efficiency through consumption-based pricing, rapid deployment timelines, and enterprise cloud adoption exceeding 94% among large organizations.

- Key Market Opportunity: Healthcare and Life Sciences sector expansion is the principal market opportunity, with a projected CAGR exceeding 20%, driven by regulatory compliance requirements, including the HIPAA Emergency Preparedness Rule, patient safety imperatives, telemedicine infrastructure deployment post-COVID, and adoption by leading institutions such as Johns Hopkins Medicine and Cleveland Clinic.

| Report Attribute | Details |

|---|---|

|

Global IoT Analytics Market Size (2026E) |

US$ 35.4 Bn |

|

Market Value Forecast (2033F) |

US$ 136.0 Bn |

|

Projected Growth CAGR (2026-2033) |

21.2% |

|

Historical Market Growth (2020-2025) |

18.8% |

Market Dynamics

Market Growth Drivers

Explosive Growth in Connected IoT Devices and Enterprise Adoption

The proliferation of connected IoT devices represents a fundamental driver of market expansion, as enterprises deploy sensor networks across operations to capture real-time data. According to IoT Analytics' State of IoT Spring 2025 report, there were 18.8 billion connected IoT devices by the end of 2024, with projections indicating growth to 40 billion devices by 2030. This massive expansion of connected infrastructure generates unprecedented volumes of data requiring sophisticated analytics platforms for meaningful interpretation.

Enterprise spending on IoT solutions grew 10% in 2024, with particularly robust growth in software and cloud-based solutions. Critically, 51% of enterprise IoT adopters plan to increase their IoT budgets in 2025, with approximately 22% of companies expecting 10% or greater budget increases compared to 2024 levels. This renewed investment momentum reflects confidence in the tangible return on investment from IoT analytics deployments, particularly in predictive maintenance and operational optimization applications.

Industry 4.0 Digital Transformation and Smart Manufacturing Initiatives

The rapid adoption of Industry 4.0 principles and smart manufacturing frameworks has created unprecedented demand for advanced analytics capabilities to support digitalized production environments. According to IoT Analytics research, 72% of manufacturers globally have implemented or are currently implementing Industry 4.0 and smart factory initiatives, up from 25% in 2019. Manufacturing organizations increasingly integrate connected sensors, automation systems, and artificial intelligence into operations to enhance productivity, quality control, and asset reliability.

Recent findings from the survey indicate that manufacturers are deploying cloud computing infrastructure, implementing industrial IoT solutions, and leveraging 5G connectivity. Additionally, 34% of manufacturers have deployed digital twins at scale, using virtual models to simulate and optimize manufacturing processes. These digital transformation initiatives fundamentally depend on robust analytics platforms to process multi-source data streams and deliver predictive insights for continuous improvement.

Market Restraints

Data Security, Privacy Regulations, and Cybersecurity Concerns

The integration of IoT systems with enterprise analytics platforms introduces significant cybersecurity vulnerabilities and regulatory compliance challenges that constrain market adoption. Organizations deploying IoT analytics solutions must navigate complex regulatory frameworks, including GDPR, CCPA, and industry-specific standards such as HIPAA for healthcare and NERC CIP for critical energy infrastructure. The distributed nature of IoT networks creates multiple potential attack vectors, with connected devices representing potential entry points for malicious actors.

Recent survey data indicates that cybersecurity concerns remain a significant barrier to IoT adoption, with organizations expressing apprehension regarding data interception, unauthorized access, and operational disruption from cyberattacks. Furthermore, implementing comprehensive security protocols, including encryption, multi-factor authentication, and continuous monitoring, increases deployment costs and implementation complexity. Organizations with limited security expertise struggle to design secure IoT architectures, creating demand for specialized consulting services but simultaneously slowing adoption among smaller enterprises.

Legacy System Integration Complexity and Workforce Skill Gaps

Many organizations operate with legacy systems, proprietary databases, and disconnected data repositories, which complicate integration with modern IoT analytics platforms. Implementing advanced analytics solutions requires significant data migration, system restructuring, and operational workflow modifications that demand specialized technical expertise. Organizations frequently report that data silos across departments and incompatible systems present substantial barriers to deploying unified IoT analytics solutions.

The market faces a pronounced shortage of qualified professionals with expertise in data engineering, machine learning model development, and analytics platform administration. The rapid evolution of IoT technologies and analytics methodologies exceeds the pace at which educational institutions can train specialized workforce talent. These skill gaps force organizations to invest substantially in external consulting services, talent acquisition, and staff training programs, increasing the total cost of ownership and extending deployment timelines.

Market Opportunities

Healthcare and Life Sciences Sector Rapid Expansion

The healthcare sector represents an exceptionally promising growth opportunity for IoT analytics providers, driven by regulatory requirements, patient safety imperatives, and operational efficiency demands. Healthcare organizations increasingly deploy connected medical devices, patient monitoring systems, and facility management sensors to collect real-time operational data. Advanced IoT analytics platforms enable predictive modeling for patient outcomes, equipment failure prediction, and resource optimization within healthcare systems. Research indicates that the healthcare vertical is projected to achieve a remarkable CAGR exceeding 20% through the forecast period, substantially outpacing broader market growth rates.

Regulatory mandates, including the HIPAA Emergency Preparedness Rule and accreditation requirements, drive healthcare organizations to implement comprehensive disaster recovery and business continuity systems dependent on advanced analytics. Additionally, the COVID-19 pandemic accelerated healthcare sector investment in telemedicine infrastructure, remote patient monitoring, and surge capacity management systems, all requiring sophisticated IoT data analytics. Hospital networks such as Johns Hopkins Medicine and Cleveland Clinic have deployed cloud-based disaster recovery systems incorporating real-time monitoring and predictive analytics to ensure uninterrupted patient care delivery.

Energy and Utilities Asset Management and Sustainable Infrastructure

The energy and utilities sector is experiencing transformative adoption of IoT analytics solutions for predictive asset management, grid optimization, and sustainability monitoring, creating substantial growth opportunities. Utility companies manage extensive infrastructure, including transformers, transmission lines, substations, and generation facilities, requiring continuous condition monitoring and maintenance optimization. Predictive asset analytics can reduce equipment maintenance costs by 10-40% while increasing asset uptime by 5-20%, delivering a measurable return on investment that justifies technology investments. According to industry analysis, the utility asset management market reached US$ 5.08 billion in 2024, with predictive maintenance solutions representing over 22% of the smart utility asset space.

Energy utilities increasingly deploy IoT sensors for real-time grid monitoring, demand forecasting, and distributed renewable energy management. Government sustainability initiatives and carbon-reduction mandates are accelerating utility investments in energy-optimization analytics. Smart meter infrastructure rollouts across developed markets generate massive volumes of consumption data suitable for advanced analytics applications. Critical infrastructure resilience requirements and aging infrastructure modernization programs create sustained demand for predictive analytics solutions enabling proactive maintenance scheduling.

Category-wise Insights

Type Analysis

The Descriptive Analytics segment captures approximately 33% of total market share, establishing itself as the foundational analytics type deployed across IoT implementations. Descriptive analytics serve as the essential layer for data visualization, historical performance monitoring, and operational reporting that converts raw sensor data streams into comprehensible dashboards and business intelligence outputs. Organizations universally require descriptive capabilities to establish a baseline understanding of system performance, identify historical patterns, and create performance benchmarks. The dominance of descriptive analytics reflects its ease of implementation, reliance on conventional data visualization techniques, and critical importance in organizational decision-making processes.

Organizations increasingly recognize the limitations of purely descriptive approaches and are upgrading toward more advanced analytics types. Predictive Analytics represents the fastest-growing segment, as enterprises transition from backward-looking analysis toward forward-looking failure prediction and scenario modeling. Prescriptive Analytics is anticipated to achieve the highest growth CAGR during the forecast period, driven by enterprises adopting artificial intelligence-driven decision automation, digital twin technologies, and autonomous optimization systems. Prescriptive analytics enables real-time system optimization by delivering specific recommendations for operational adjustments aligned with defined business objectives.

Component Analysis

The Solutions segment represents approximately 50% of component market share, encompassing integrated software platforms, data management systems, visualization dashboards, and analytics engines that process IoT data streams. Comprehensive solution offerings must integrate data ingestion capabilities, real-time processing engines, machine learning frameworks, and user interface systems to deliver end-to-end analytics functionality. Leading platforms such as Microsoft Azure IoT Hub, Amazon AWS IoT Analytics, and Google Cloud IoT provide enterprises with scalable cloud-native solutions supporting massive data volumes and distributed architectures.

The Services segment is expected to grow at the highest CAGR of approximately 23.4% during the forecast period, driven by enterprises requiring system integration, implementation support, managed analytics services, and ongoing consulting services. Professional services encompass solution design, platform customization, data architecture development, and staff training initiatives essential for successful deployments. Organizations, particularly smaller enterprises, lack internal expertise for deploying sophisticated IoT analytics platforms and depend on external service providers for system implementation and optimization.

Deployment Mode Analysis

The Cloud-based deployment mode represents the fastest-growing segment, expanding at a remarkable CAGR of 21.8% while capturing approximately 40% of the current market share and is projected to accelerate the growth trajectory. Cloud-based IoT analytics solutions offer superior scalability to accommodate fluctuating data volumes, financial efficiency through consumption-based pricing models, and rapid deployment timelines compared to on-premises infrastructure. Enterprise preference for cloud deployment continues to accelerate as organizations recognize advantages in disaster recovery capabilities, automatic software updates, and seamless integration with artificial intelligence and machine learning services.

Cloud adoption among enterprise organizations exceeds 94%, indicating widespread organizational comfort with cloud infrastructure for mission-critical applications. The On-premise deployment mode maintains approximately 57% of total market share, particularly prevalent among government agencies, financial institutions, and organizations operating in regulated industries requiring stringent data residency controls and offline operational continuity. Hybrid deployment approaches combining on-premises core systems with cloud-based analytics and collaboration tools are emerging as the enterprise preference, enabling organizations to balance control requirements with scalability advantages.

Application Analysis

The Predictive Maintenance application is the dominant use case, commanding approximately 45% of the total application market share, underscoring the business-critical importance of equipment reliability and operational continuity. Organizations deploying predictive maintenance analytics report significant benefits, including up to 50% reduction in unplanned equipment downtime and approximately 25% reduction in maintenance expenses compared to reactive and preventive maintenance strategies. IoT sensors installed throughout manufacturing facilities, energy infrastructure, and transportation networks continuously monitor equipment parameters, including vibration, temperature, acoustic signatures, and operational efficiency metrics.

Advanced machine learning algorithms analyze multi-parameter datasets to identify early indicators of equipment degradation and forecast potential failures weeks in advance, enabling maintenance teams to schedule interventions during planned downtime rather than responding to catastrophic breakdowns. The application of predictive maintenance extends across manufacturing production lines, power generation and distribution systems, aircraft engines, and healthcare medical equipment. Energy Management and Asset Management applications represent substantial secondary use cases, while Inventory Management and Remote Monitoring applications are expanding rapidly driven by supply chain optimization and real-time operational visibility requirements.

End Use Analysis

The Manufacturing vertical dominates with approximately 36% market share, driven by widespread adoption of Industry 4.0, competitive pressures to improve operational efficiency, and the fundamental dependence of production systems on equipment reliability. Manufacturers deploy IoT analytics to optimize production line efficiency, detect quality deviations in real time, predict equipment failures before unplanned outages, and enhance supply chain visibility. Advanced analytics enable manufacturers to implement predictive maintenance strategies by reducing costly production interruptions, to implement real-time quality control detecting manufacturing defects immediately rather than downstream, and to optimize resource utilization across distributed production facilities.

The Energy and Utilities vertical accounts for approximately 18% of market share, with rapid growth driven by regulatory sustainability mandates, aging infrastructure modernization requirements, and the expansion of renewable energy sources that require sophisticated grid optimization. The Healthcare and Life Sciences sector represent approximately 12% of market share with the highest projected growth rates as medical device manufacturers, hospital networks, and pharmaceutical companies increasingly deploy IoT analytics for patient monitoring, medical equipment maintenance, and facility optimization. The Transportation and Logistics, IT and Telecom, and Retail sectors represent additional vertical markets with distinct analytics requirements, driving diversified solution demand.

Regional Insights

North America IoT Analytics Trends

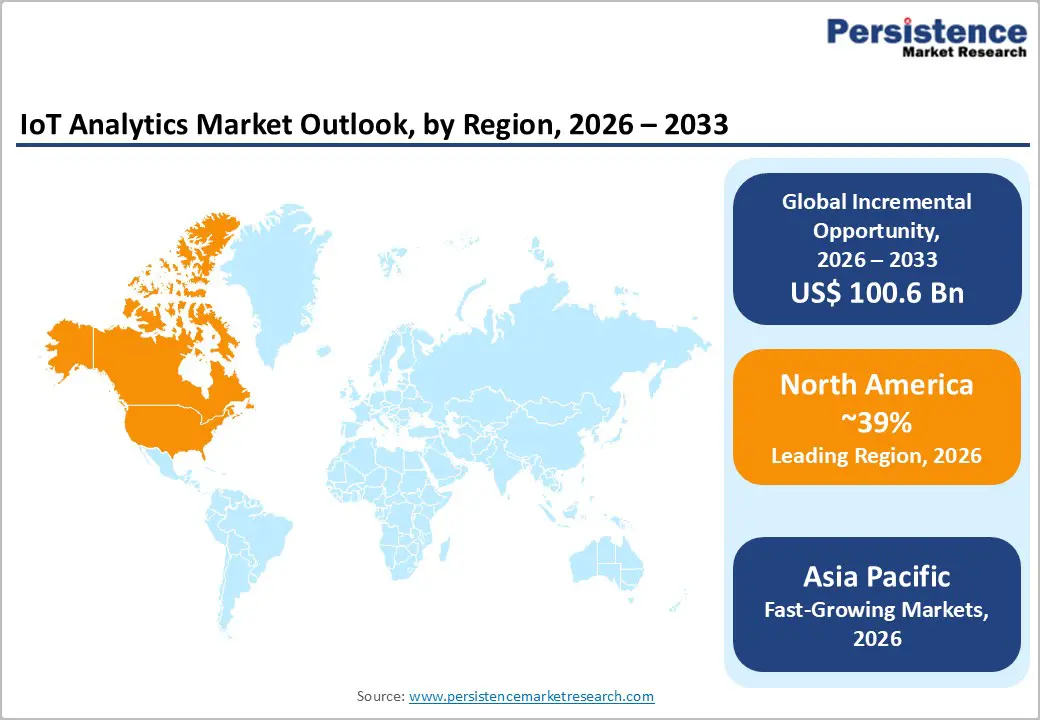

North America commands the largest regional market share at approximately 38.52%, with the United States representing the dominant market within the region. The region benefits from mature digital infrastructure, substantial enterprise investment in digital transformation initiatives, and a highly developed ecosystem of IoT analytics vendors and technology providers. North American enterprises are leading in adopting advanced analytics types, including prescriptive analytics and artificial intelligence-driven decision automation. Government initiatives promoting smart manufacturing and critical infrastructure modernization have accelerated the adoption of IoT analytics across federal agencies, state governments, and municipal authorities. The region's strong venture capital ecosystem and innovation-focused culture have fostered the emergence of specialized IoT analytics companies alongside traditional technology incumbents.

Enterprise cloud adoption in North America is particularly advanced, with over 94% of large organizations utilizing cloud-based infrastructure and 54% planning to migrate additional workloads to public clouds within 12 months. Cloud hyperscalers including Microsoft Azure, Amazon AWS, and Google Cloud are heavily investing in IoT analytics capabilities, with combined capital expenditure exceeding $250 billion in 2025 for data center and artificial intelligence infrastructure. Microsoft has captured 45% of new cloud AI case studies, including 62% of generative AI-focused projects, positioning the company as the market leader in AI-powered IoT analytics. North American manufacturing facilities are increasingly deploying integrated IoT analytics platforms that combine real-time monitoring, predictive maintenance, quality control automation, and supply chain optimization.

Europe IoT Analytics Trends

Europe represents a significant regional market characterized by stringent data privacy regulations, a strong industrial manufacturing base, and an increasing emphasis on sustainable operations and energy efficiency. European Union regulatory frameworks including the General Data Protection Regulation (GDPR) have significantly influenced how enterprises implement IoT analytics solutions, requiring robust data governance, consent management, and privacy-by-design approaches. Industrial manufacturing in countries including Germany, France, and Italy has driven substantial adoption of Industry 4.0 principles and IoT analytics platforms for production optimization. European enterprises are particularly focused on energy efficiency analytics and carbon footprint monitoring, driven by regulatory mandates and corporate sustainability commitments.

European organizations are increasingly adopting cloud-based IoT analytics solutions while maintaining GDPR compliance through careful data-residency planning and vendor selection. The region has experienced slower IoT enterprise spending growth compared to other regions, with IoT Analytics reporting European IoT adoption rates below global averages due to macroeconomic uncertainties and conservative corporate spending approaches. However, European digital transformation initiatives and government-backed smart city projects are expected to accelerate IoT analytics adoption through the forecast period. Leading European enterprises are implementing hybrid cloud deployments, balancing GDPR compliance requirements with scalability advantages.

Asia Pacific IoT Analytics Trends

Asia Pacific represents the fastest-growing regional market, expected to expand at a CAGR of approximately 24.6%, substantially exceeding global average growth rates. The region benefits from rapid industrialization, emergence of advanced manufacturing hubs, particularly in China and Vietnam, and aggressive government investment in smart city infrastructure and digital transformation initiatives. China has established itself as the world's largest manufacturing hub and is rapidly deploying Industry 4.0 technologies, including IoT analytics, to enhance productivity and global competitiveness. India is experiencing particularly rapid growth with 14% year-over-year IoT spending growth, driven by expanding manufacturing capabilities, increasing software development services, and government initiatives promoting digital infrastructure. Major technology companies, including Microsoft and Amazon, have announced combined investments exceeding $52.5 billion in India for AI infrastructure and digital transformation initiatives.

Asia Pacific markets are experiencing rapid expansion of cloud infrastructure supporting IoT analytics deployments, with cloud platforms such as Microsoft Azure, Amazon AWS, and Google Cloud expanding regional data center capabilities. The region benefits from substantial cost advantages in manufacturing and technology services, positioning Asia Pacific as a manufacturing hub for IoT devices and analytics platforms. 5G network rollout across the region is accelerating the adoption of real-time IoT analytics applications requiring high-bandwidth, low-latency connectivity. ASEAN countries, including Singapore, Malaysia, and Thailand, are investing in smart city infrastructure and manufacturing automation, driving IoT analytics adoption.

Competitive Landscape for the IoT Analytics Market

The IoT Analytics market exhibits moderate consolidation characterized by dominance of large cloud hyperscalers, specialized analytics platform vendors, and enterprise software providers with diverse competitive positioning. Microsoft Corporation has established market leadership in cloud AI applications including IoT analytics, capturing 45% of new cloud AI case studies and achieving $13 billion in annual AI revenue with 175% year-over-year growth. Amazon Web Services maintains a dominant position in traditional AI and IoT implementations through comprehensive service portfolios, including AWS IoT Analytics, SageMaker, and industrial IoT platforms. Google Cloud differentiates through advanced machine learning capabilities and integration of AI across product offerings.

Traditional enterprise software providers, including SAP, Oracle, and Salesforce, are embedding advanced analytics capabilities within enterprise applications. SAP announced plans to deliver 400 embedded AI use cases by 2025 and integrated its generative AI assistant Joule deeply within SAP S/4HANA. Oracle embedded over 50 new AI agents into Fusion Cloud Applications, enhancing supply chain, finance, and manufacturing workflows.

Key Market Developments

- In December 2025, SAP Advances AI Integration in Enterprise Systems: SAP embedded its generative-AI copilot, Joule, deeply into its SAP S/4HANA Cloud Public Edition, enabling natural-language navigation, contextual insights, and automated workflows across enterprise resource planning systems, advancing AI-powered analytics capabilities for organizations integrating IoT data.

- In December 2024, Microsoft and Amazon Announce Massive India Investments - Microsoft pledged $17.5 billion and Amazon committed $35 billion by 2030 to fortify India's AI ecosystem, cloud infrastructure, and digital transformation capabilities, positioning Asia Pacific as critical growth market for IoT analytics solutions.

- In November 2024, Enterprise Cloud Adoption Accelerates Beyond 94% - Research indicates that 94% of large enterprise organizations have deployed significant portions of workloads to cloud platforms, with 54% planning to migrate additional workloads to public clouds within 12 months, establishing cloud-based IoT analytics as the dominant deployment mode.

Companies Covered in IoT Analytics Market

- Accenture

- Aeris

- Amazon Web Services, Inc.

- Cisco Systems, Inc.

- Dell Inc.

- Hewlett Packard Enterprise Development LP

- Google (Alphabet Inc.)

- OpenText Web

- Microsoft

- Oracle

- PTC

- Salesforce, Inc.

- SAP SE

- SAS Institute Inc.

- Software AG

Frequently Asked Questions

The global IoT Analytics market is projected to reach US$ 136.0 billion by 2033, growing from US$ 35.4 billion in 2026 at a robust CAGR of 21.2%, driven by exponential growth in connected IoT devices, widespread Industry 4.0 adoption, and integration of artificial intelligence and machine learning technologies.

Primary demand drivers include the explosive growth in connected IoT devices projected to reach 40 billion by 2030, widespread adoption of Industry 4.0 with 72% of manufacturers implementing smart factory initiatives, substantial return on investment from predictive maintenance reducing downtime by 50% and maintenance costs by 25%, government-backed smart city projects and critical infrastructure modernization investments, and accelerating cloud adoption exceeding 94% among large enterprises.

The Predictive Maintenance application dominates with approximately 45% market share, as organizations prioritize equipment reliability and operational continuity, leveraging IoT sensors to forecast failures and schedule interventions during planned maintenance windows rather than responding to catastrophic breakdowns.

North America leads the global IoT Analytics market with approximately 38.2% market share, supported by mature digital infrastructure, advanced enterprise cloud adoption exceeding 94%, leadership of technology providers including Microsoft capturing 45% of cloud AI case studies, and substantial investment in Industry 4.0 and smart manufacturing initiatives.

Healthcare and Life Sciences sector expansion represents the principal market opportunity with projected growth exceeding 20% CAGR, driven by regulatory compliance requirements including HIPAA Emergency Preparedness Rule, patient safety imperatives, post-COVID telemedicine infrastructure deployment, and adoption by leading medical institutions deploying cloud-based disaster recovery systems.

Leading market players include Microsoft Corporation, which captured 45% of cloud AI case studies; Amazon Web Services, achieving 85% success in non-generative AI applications; Google Cloud integrating AI across 36% of case studies; SAP SE deploying 400 embedded AI use cases; Oracle Corporation embedding 50+ AI agents; and Salesforce, Inc. advancing Data 360 platform for unified analytics integration.