- Specialty & Fine Chemicals

- India Castor Oil & Derivatives Market

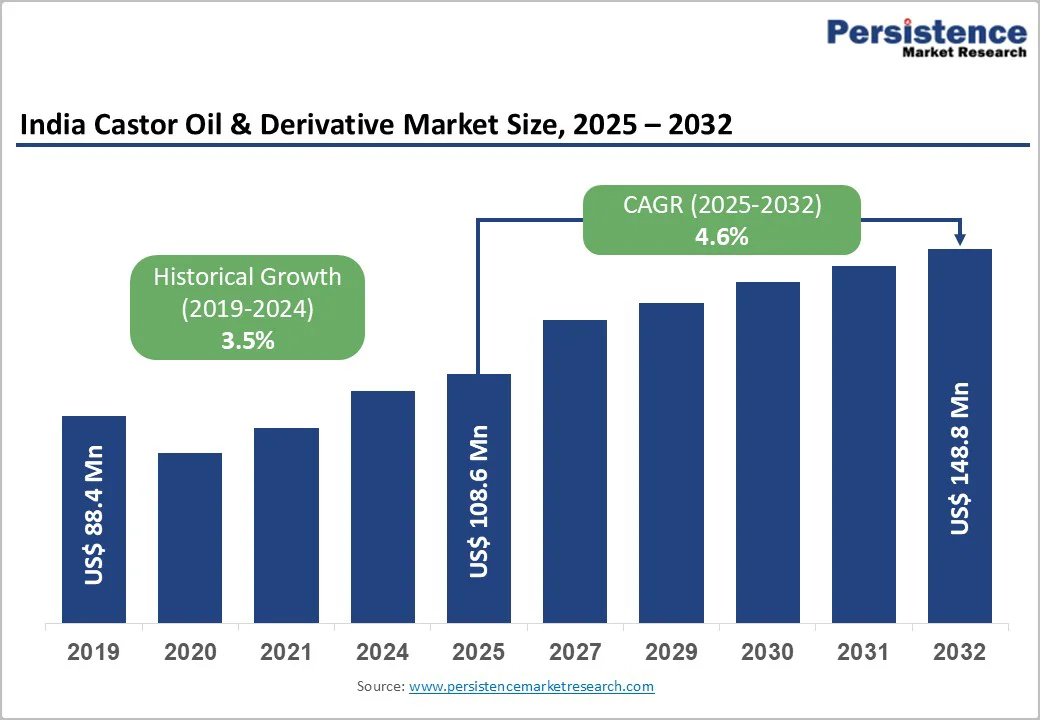

India Castor Oil & Derivatives Market Size, Trends, Share, and Growth Forecast 2025 - 2032

India Castor Oil & Derivatives Market by Generation of Derivatives (Castor Oil, Gen-2, Gen-3, Gen-4), Derivative Type (Ricinoleic Acid, 12-HAS, Heptanoic Acid, Undecylenic Acid, Sebacic Acid, Bio-Polyurethanes), End-user (Cosmetics & Personal Care, Pharmaceuticals, Textile & Footwear, Food & Beverages, and Other), and Regional Analysis for 2025 - 2032

India Castor Oil & Derivatives Market Size and Trend Analysis

The India castor oil & derivatives market size is valued at US$108.63 Mn in 2025 and is projected to reach US$148.82 Mn by 2032, growing at a CAGR of 4.6% between 2025 and 2032.

India's dominance in global castor oil production, accounting for over 85% of world castor seed output, positions the nation as a critical raw material supplier for advanced derivatives. The market expansion is driven by accelerating demand from the cosmetics and personal care industries, which increasingly prioritize natural and plant-derived ingredients aligned with clean-label trends.

Key Market Highlights:

- Regional Leader: Gujarat and surrounding West Indian regions dominate the India Castor Oil & Derivatives market, with approximately 52% regional share, driven by concentrated castor cultivation, which accounts for over 85% of national production.

- Fastest Growing Region: North Indian states represent the fastest-growing regional markets at approximately 5.8% annually, supported by rising consumer demand for personal care ingredients and government industrial incentives attracting new manufacturing capacity and derivative production facilities.

- Leading Segment: Ricinoleic Acid Derivatives command the largest derivative market segment at approximately 28% market value, driven by established applications in the personal care industry, such as deodorants, emulsifiers, skin conditioning agents, and cosmetic formulations.

- Fastest Growing Segment: Cosmetics & Personal Care applications represent approximately 38% of market value, driven by increasing adoption of castor oil derivatives in emulsifiers, emollients, and conditioning systems across skincare, haircare, and specialty beauty products.

- Growth Opportunities: Bio-polyamides (PA-11, PA-10, 10, PA-6, 10) and bio-polyurethanes represent the most substantial growth opportunities, driven by automotive industry adoption for sustainable lightweight components.

| Key Insights | Details |

|---|---|

| India Castor Oil & Derivatives Market Size (2025E) | US$ 108.63 Mn |

| Market Value Forecast (2032F) | US$ 148.82 Mn |

| Projected Growth CAGR (2025 - 2032) | 4.6% |

| Historical Market Growth (2019 - 2024) | 3.5% |

Market Dynamics

Strategic Supply Chain Partnerships Ensuring Raw Material Security

The India Castor Oil & Derivatives market is experiencing a significant trend in which manufacturers are establishing long-term supply contracts and strategic collaborations with castor oil suppliers to ensure uninterrupted raw material availability. This approach addresses the persistent vulnerability of castor supply chains to climatic disruptions, particularly in Gujarat, which accounts for approximately 85% of India's castor production.

Companies are negotiating fixed-price procurement agreements to hedge against the volatility that characterizes agricultural commodity markets. For example, strategic partnerships between global manufacturers and regional suppliers like Gokul Overseas, Royal Castor Products Ltd., and Jayant Agro-Organics Ltd. have enabled consistent access to premium-grade castor oil at predictable pricing, allowing downstream derivatives manufacturers to optimize production schedules and maintain competitive margins in international markets.

Rising Demand for Natural and Plant-Derived Cosmetic Ingredients

Cosmetics & Personal Care applications are driving substantial demand for castor oil derivatives, as consumers increasingly prefer natural, clean-label, and sustainable beauty formulations. Castor oil-derived compounds such as ricinoleate, undecylenate, and polyhydroxystearic acid are gaining prominence in emulsifying systems, emollients, and conditioning agents across skincare, haircare, and lip care products.

The global Cosmetic Ingredients Market is expanding rapidly, with Indian consumers increasingly seeking products formulated with plant-based derivatives, as demonstrated by industry reports indicating that 71% of Indian consumers prefer skincare products with organic and plant-derived ingredients.

Ingredient innovations like zinc ricinoleate for deodorants and polyglyceryl polyricinoleate (PGPR) for cosmetic emulsions are becoming industry standards. This shift toward bio-based alternatives in the beauty sector is opening substantial revenue opportunities for castor oil derivative producers targeting premium personal care segments and international beauty brands adopting sustainability mandates.

Restraints - Production Complexity and Limited Technical Expertise in Advanced Derivatives

The growth of advanced castor oil derivatives, especially Generation-4 products like polyamide-11 and bio-polyurethanes, is hindered by significant technological barriers. Their production involves complex multi-step synthesis, controlled environments, specialized catalysts, and strict quality control. The lack of technical expertise in India for advanced polymer chemistry limits manufacturers' ability to progress beyond basic derivatives to higher-value products.

Furthermore, maintaining consistent product purity across large-scale production batches demands continuous R&D investment and process optimization capabilities that many small and mid-sized enterprises lack. This technological bottleneck has resulted in Indian manufacturers concentrating on Generation-2 and Generation-3 derivatives, while international competitors in Europe and China dominate the advanced derivatives segment, limiting India's value capture in the global supply chain.

Regional Castor Production Concentration and Weather Volatility

India Castor Oil & Derivatives market faces significant supply constraints due to the geographical concentration of castor cultivation in Gujarat and Rajasthan, with Gujarat accounting for over 85% of production. This dependency exposes the market to climatic variations like unseasonal rainfall and droughts, affecting seed yield and oil extraction. Past disruptions, such as adverse weather in 2019 and delayed sowing in 2021, led to lower yields and higher raw material prices, creating uncertainty in the derivative supply chain.

Furthermore, castor cultivation remains economically uncompetitive compared to alternative oilseed crops like cotton and groundnut, which offer higher returns to farmers with less stringent agronomic requirements. Accordingly, land coverage under castor production remains stagnant or declines in certain years, creating intermittent supply shortages that directly impact the production planning and cost competitiveness of downstream castor oil derivatives manufacturers serving international markets.

Opportunity - Bio-based Polyamide Expansion Across Automotive and Industrial Applications

Castor oil-derived bio-polyamides, such as polyamide-11 (PA 11), polyamide-10,10, and polyamide-6,10, offer significant growth potential as the automotive industry shifts towards sustainable, lightweight materials. Manufacturers are replacing petroleum-based plastics with these castor-derived polyamides for applications such as fuel lines, cable insulation, pneumatic tubing, and underhood components, thanks to their superior heat resistance, chemical stability, and lower carbon footprints.

The specialty paints and coatings market is seeing increased interest in bio-based polymers for innovative coatings. In 2025, companies like Arkema are expanding polyamide-11 production, while Envalior is launching high-performance composites with castor-based bio-polyamides for aerospace and sports applications. The automotive sector's focus on carbon emission regulations and sustainability is driving demand for these advanced castor derivatives, essential for the transition to circular economy manufacturing.

Expansion of Bio-Polyurethane Applications in Furniture and Sustainable Packaging

Bio-polyurethanes from castor oil are quickly gaining popularity in furniture, construction, and sustainable packaging due to environmental regulations and demand for renewable materials. The global Bio-based Polyurethane Market is growing, with India’s market expanding at 8%. Advanced castor oil-derived polyols are replacing petroleum-based versions in flexible foams for cushioning and mattresses, while rigid foams are increasingly used in insulation and construction.

Government initiatives such as Make in India, Smart Cities Mission, and Housing for All programs are driving substantial construction and real estate development, creating concentrated demand for sustainable insulation materials and foam solutions. Companies are also developing castor-based polyurethane formulations for eco-friendly packaging applications that offer biodegradability and reduced environmental impact compared to conventional plastics.

Category-wise Analysis

Generation of Derivative Insights

Generation-2 derivatives dominate the Indian castor oil and derivatives market, accounting for approximately 43% of the market value. This dominance is driven by their established commercial applications and lower production complexity.

Generation-2 derivatives include sebacic acid, undecylenic acid, ricinoleic acid, and heptanoic acid compounds. They represent a foundational segment with widespread use in pharmaceutical, personal care, and industrial lubricant applications.

The established production pathways, regulatory approvals, and proven efficacy of these derivatives have made them a primary focus for Indian manufacturers. Additionally, the expansion of the cosmetic ingredients market in India and the increasing demand from personal care formulators for advanced emulsifiers and skin-conditioning agents are contributing to the growth of the Generation-2 segment.

Derivative Type Analysis

Ricinoleic Acid Derivatives command the largest market share, accounting for approximately 28% of the total derivative market value, driven by their multifunctional properties and extensive applications in deodorants, skin conditioning formulations, and therapeutic preparations.

Compounds like zinc ricinoleate, used in personal care products as odor-control agents, and polyglycerol polyricinoleate (PGPR), which functions as an emulsifier in cosmetics and food applications, demonstrate the category's commercial versatility.

The Bio-based polyurethane market is expanding, and the growing adoption of sebacic acid in bio-polyamide formulations are driving this segment's growth trajectory. The growing pharmaceutical sector and increased demand for natural antifungal agents in topical formulations are supporting the sustainable expansion of these derivative categories.

End-user Analysis

Cosmetics & Personal Care applications dominate the market, representing approximately 38% of market value. The justification for cosmetics' dominance reflects India's rapidly expanding beauty market, favorable demographics favoring personal care consumption, and global brand partnerships driving demand for natural ingredients.

Pharmaceuticals represent the second-largest end-user segment, with approximately 21% market share, and are concentrated in antifungal creams, anti-inflammatory formulations, and topical drug delivery systems. The expanding Indian pharmaceutical market, coupled with increasing adoption of natural active pharmaceutical ingredients, is supporting steady growth in this category.

Regional Insights

West India Castor Oil & Derivatives Market Leadership

West India, particularly Gujarat and surrounding regions, dominates the India Castor Oil & Derivatives market with approximately 52% regional market share, driven by the concentration of castor cultivation, processing infrastructure, and established supply chains. Gujarat's castor production of approximately 1,401.33 kilotonnes in the 2021-22 agriculture season represents over 85% of national output, establishing the region as the foundational raw material hub.

Beyond production, the state hosts major castor oil processing facilities and manufacturers like Gokul Overseas, Royal Castor Products Ltd., and Jayant Agro-Organics Ltd., creating integrated value chains from seed processing to derivative manufacturing.

The region's industrial ecosystem, characterized by well-developed ports, export infrastructure, and established trading centers in Rajkot, Ahmedabad, and Gondal, facilitates efficient distribution of finished products to international markets.

Emerging Growth Corridors in North Indian Regions

North and Central India, especially Rajasthan and emerging manufacturing hubs in Madhya Pradesh, are the fastest-growing regions at about 5.8% annually, fueled by the pharmaceutical industry, rising incomes, and government incentives.

Rajasthan's castor cultivation has grown significantly, supporting the manufacture of pharmaceuticals, antifungals, and industrial lubricants for the automotive and manufacturing sectors. Enhanced industrial initiatives and improved logistics are attracting chemical manufacturers seeking cost-effective production near emerging consumer markets.

Government support programs, including tax incentives and infrastructure development, are facilitating new capacity additions in derivative manufacturing across these regions. The Bio-based Polyurethane Market is expanding at an 8% growth rate in these regions, reflecting the accelerating adoption of sustainable materials in furniture manufacturing, construction, and consumer goods sectors.

Competitive Landscape

India Castor Oil & Derivatives market exhibits a consolidated competitive structure, with established manufacturers controlling significant market share while numerous small and laboratory-scale producers operate in the Generation-2 and Generation-3 segments.

Indian manufacturers, particularly Jayant Agro-Organics Ltd., Royal Castor Products Ltd., Gokul Overseas, and Ambuja Solvex Pvt Ltd., collectively maintain most of the market share, focused on Generation-2 and Generation-3 derivatives with established commercial applications and lower technological barriers to entry.

Market differentiation is driven by product purity, functional versatility, customization capabilities, and technical support services. Global manufacturers emphasize advanced chemistries targeting niche, high-value applications, while Indian companies compete on cost efficiency and supply chain proximity to raw materials.

Key Market Developments

- January 2025: Arkema SA increased investment in castor oil-derived polyamide-11 manufacturing to meet accelerating global demand from automotive fuel line applications and sustainable engineering polymer markets, reinforcing its leadership in bio-based polymer chemistry.

- October 2024: OQ Chemicals GmbH introduced OxBalance Neopentyl Glycol Diheptanoate, an ISCC PLUS-certified biomass-balanced cosmetic ingredient designed to support the cosmetics industry's transition toward sustainable, climate-conscious formulations utilizing renewable castor oil feedstock.

- September 2024: Envalior launched advanced bio-polyurethane formulations incorporating castor oil-derived polyols for sustainable insulation and construction materials, targeting the expanding infrastructure and smart cities sectors in India and the Asia Pacific regions.

Top Companies in India Castor Oil & Derivatives Market

- Arkema Inc. (France) is a leading global manufacturer of specialty chemicals and bio-based polymers, maintaining significant market presence in India's castor oil derivatives sector through investments in polyamide-11 production and sustainable polymer technologies.

- BASF SE (Germany) operates comprehensive specialty chemical operations in India with established competencies in sebacic acid derivatives, plasticizers, and bio-based polymers developed from castor oil feedstock.

- Jayant Agro-Organics Ltd. (India) is a domestic manufacturer and exporter of castor oil derivatives and specialty chemicals, commanding significant market share in Generation-2 and Generation-3 derivative segments through integrated production from castor seed processing through finished derivative manufacturing.

Companies Covered in India Castor Oil & Derivatives Market

- Arkema Inc.

- BASF SE

- Evonik Industries AG

- Gokul Overseas

- Ambuja Solvex Pvt Ltd

- Formosa Taffeta Co., Ltd.

- Jayant Agro-Organics Ltd.

- Radici Group

- Royal Castor Products Ltd.

- Envalior

- Aurorium

- Inolex Chemicals

- Modi Oil Mill

Frequently Asked Questions

India Castor Oil & Derivatives market is valued at US$ 108.63 Mn in 2025 and is projected to grow at a CAGR of 4.6% to reach US$ 148.82 Mn by 2032, driven by expanding cosmetics applications and bio-based polymer adoption.

The India Castor Oil & Derivatives market is driven by rising consumer demand for natural cosmetic ingredients, increasing pharmaceutical use of castor-based compounds for antifungal and anti-inflammatory purposes, corporate sustainability goals for lower carbon footprints, and the growing use of bio-based polyamides and polyurethanes in automotive and construction as manufacturers shift towards sustainable materials.

Ricinoleic Acid Derivatives dominate the India Castor Oil & Derivatives market segment, commanding approximately 28% market value driven by established applications in personal care industry.

West India, particularly Gujarat, dominates the India Castor Oil & Derivatives market with approximately 52% regional market share, driven by the concentration of castor seed cultivation representing over 85% of national production.

Bio-based polyamides (PA-11, PA-10,10, PA-6,10) and bio-polyurethanes derived from castor oil represent the most substantial market opportunities, driven by automotive industry adoption for sustainable fuel lines and lightweight components, and construction sector demand for eco-friendly insulation materials.

Leading market players include global manufacturers Arkema Inc., BASF SE, Evonik Industries AG, and Envalior operating in advanced polymer and specialty chemical segments, complemented by established Indian producers Jayant Agro-Organics Ltd., Royal Castor Products Ltd., Gokul Overseas, and Ambuja Solvex Pvt Ltd.