- Inks, Coatings, Adhesives & Sealants (ICAS)

- India Construction Equipment OEM Coating Market

India Construction Equipment OEM Coating Market Size, Share, and Growth Forecast 2026 - 2033

India Construction Equipment OEM Coating Market by Material Type (Acrylic, Alkyd, Polyurethane, Epoxy, Others), by Formulation (Water-borne Solutions, Solvent-borne Solutions, Others), by Technology (Electro-coating, Spraying, Others), by Application, by End Use, and Regional Analysis for 2026 - 2033

India Construction Equipment OEM Coating Market Size and Trend Analysis

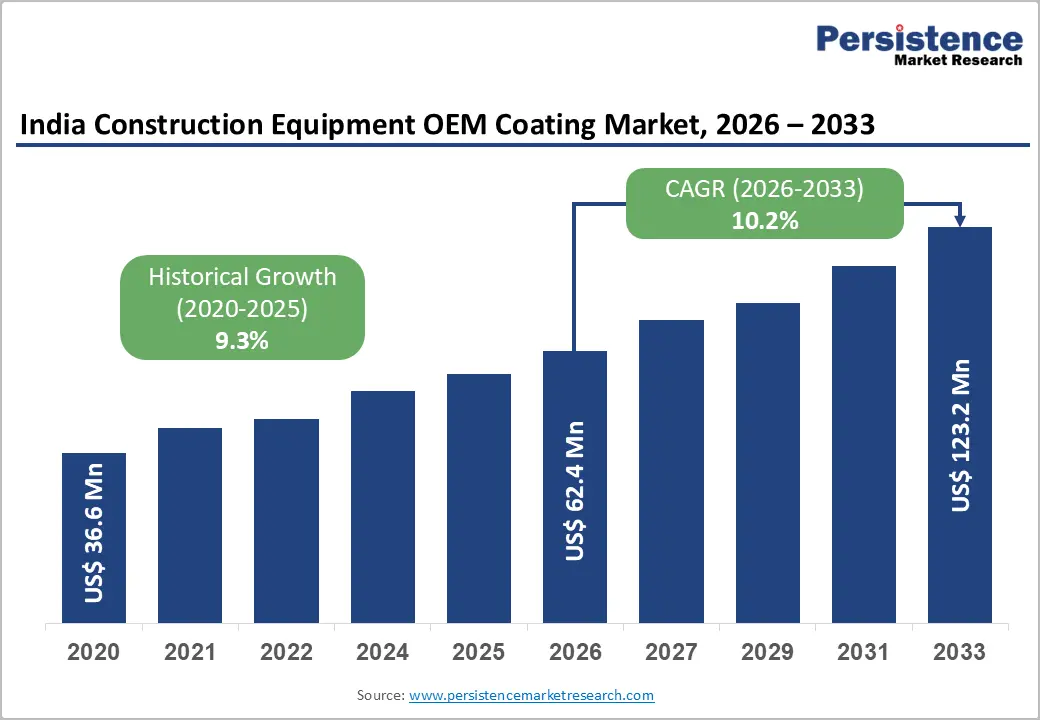

India Construction Equipment OEM Coating market size is supposed to be valued at US$ 62.4 Million in 2026 and is projected to reach US$ 123.2 Million by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

The Indian Construction Equipment OEM Coating market is experiencing one of the most sustained high-growth cycles in its commercial history, fundamentally propelled by the Government of India's unprecedented infrastructure investment program under the National Infrastructure Pipeline (NIP) allocating INR111 lakh crore (approximately US$ 1.4 trillion) across 7,400+ infrastructure projects spanning roads, railways, ports, airports, urban development, and housing through FY2025, generating structurally massive demand for construction equipment whose protective coating requirements sustain recurring OEM coating procurement at above-GDP growth rates.

Key Industry Highlights

- Leading Region: North India leads the India Construction Equipment OEM Coating market, anchored by JCB India's Faridabad manufacturing plant, NHAI's highest construction activity states of Uttar Pradesh and Haryana, DMIC and EDFC infrastructure programs, and Delhi NCR's metro rail expansion sustaining the highest construction equipment fleet deployment and OEM coating procurement volumes in India.

- Fastest Growing Region: South India is the fastest-growing regional market, driven by Tata Hitachi's Dharwad plant expansion, Tamil Nadu's globally competitive engineering manufacturing clusters, Kansai Paints' Hosur production, significant iron ore and granite mining in Karnataka and Andhra Pradesh, and Telangana's aggressive industrial infrastructure development generating above-average OEM coating demand growth.

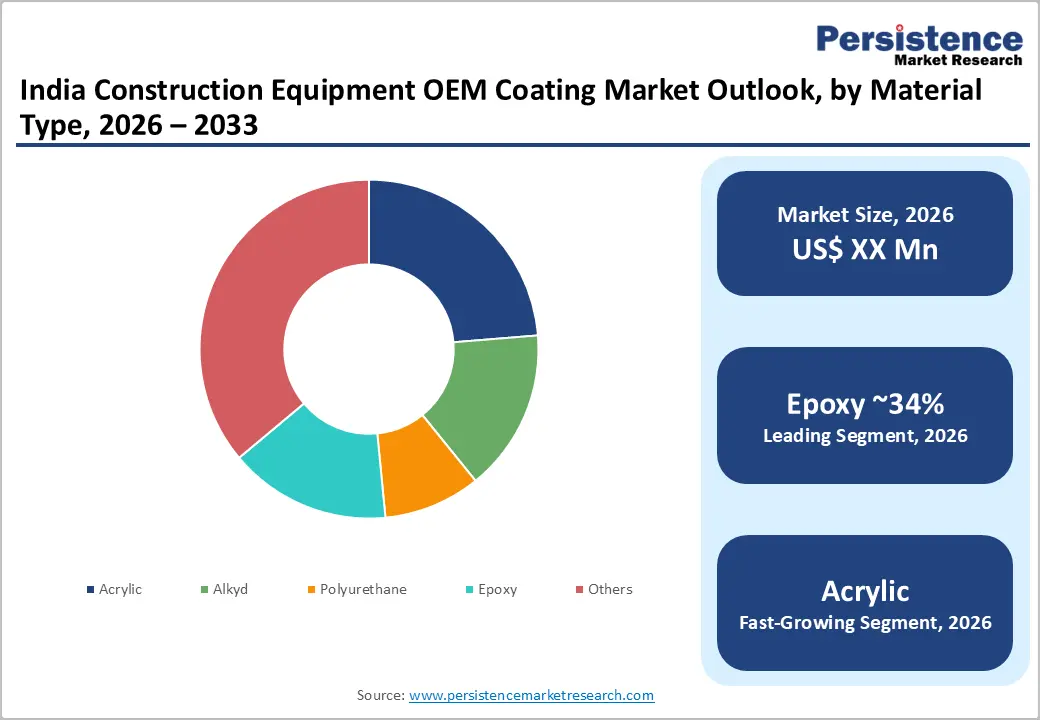

- Dominant Product Type: Epoxy dominates the Material Type segment with approximately 34% revenue share, anchored by its technically irreplaceable role as the universally specified primer system in Indian construction equipment OEM paint specifications, validated corrosion protection performance per IS 101 and ASTM B117 standards, and adoption by all major OEMs including JCB India, BEML, and Tata Hitachi as the mandatory base coat in their equipment coating systems.

- Fastest Growing: Water-borne Solutions is the fastest-growing Formulation segment, propelled by CPCB VOC compliance mandates, Asian Paints PPG's February 2025 water-borne OEM coating range launch, Green Public Procurement specifications for low-VOC coatings on government infrastructure projects, and major OEM paint shop upgrade investments targeting environmental certification aligned with Make in India sustainability commitments.

- Key Market Opportunity: Electro-coating technology and green OEM coating formulation transition represent the key market opportunity, with JCB India's INR200 crore automated e-coat plant investment in October 2024, PLI scheme construction equipment manufacturing expansion attracting multinational OEM paint shop upgrade investments, and CPCB water-borne compliance mandates creating structurally growing demand for technically certified e-coat and water-borne system capable OEM coating suppliers through the 2026–2033 forecast period.

| Key Insights | Details |

|---|---|

|

Construction Equipment OEM Coating Market Size (2026E) |

US$ 62.4 Million |

|

Market Value Forecast (2033F) |

US$ 123.2 Million |

|

Projected Growth CAGR (2026–2033) |

10.2% |

|

Historical Market Growth (2020–2025) |

9.3% |

Market Dynamics

Drivers - India's National Infrastructure Pipeline and PM Gati Shakti Driving Record Construction Equipment Demand and OEM Coating Procurement

The Government of India's National Infrastructure Pipeline (NIP), the world's largest national infrastructure investment program at INR111 lakh crore (approximately US$ 1.4 trillion), is the single most consequential demand driver for India's Construction Equipment OEM Coating market, as infrastructure construction scale directly determines construction equipment fleet size and consequently OEM coating procurement volumes across the Indian supply chain. The Union Budget 2024–25 allocated INR11.11 lakh crore for capital expenditure, representing 3.4% of GDP and the highest-ever Indian government capital expenditure budget allocation, directly funding road construction under the National Highways Authority of India (NHAI), railway expansion under Indian Railways, metro rail projects across 27 Indian cities, and port modernization under Sagarmala Programme that collectively generate multi-year construction equipment fleet demand sustaining OEM coating procurement growth.

ICEMA documented approximately 125,000 construction equipment units sold in FY2023–24, with hydraulic excavators, backhoe loaders, compactors, and motor graders representing the dominant equipment categories, each requiring multi-coat OEM protective coating systems incorporating primer, intermediate, and topcoat layers of anti-corrosion epoxy, polyurethane, or alkyd formulations applied during the manufacturing process. The Ministry of Road Transport and Highways (MoRTH) has set a target of constructing 25 km of national highways per day through FY2025, a construction pace demanding continuous high equipment utilization that drives both fleet replacement cycles and first-coat OEM procurement growth for domestic equipment manufacturers including Tata Hitachi, BEML, Mahindra Construction Equipment, and JCB India.

Mining Sector Expansion and PM Gati Shakti Mineral Logistics Program Sustaining Heavy-Duty OEM Coating Demand

India's rapidly expanding mining sector, stimulated by the Ministry of Mines' progressive mineral concession allocation reforms under the Mines and Minerals (Development and Regulation) Amendment Act, the National Mineral Policy 2019, and the Mineral Exploration and Consultation Agency (MECA)'s accelerated mineral block auction program, is generating structurally growing demand for the most technically demanding category of construction equipment OEM coatings: heavy-duty anti-corrosion, abrasion-resistant, and chemical-resistant coating systems applied to mining excavators, drilling equipment, haul trucks, and mineral processing plant equipment operating in highly aggressive chemical, thermal, and mechanical wear environments.

The Ministry of Mines' data documents that India's mineral production value reached INR2.4 lakh crore (approximately US$ 29 billion) in FY2022–23, reflecting the scale of active mining equipment fleet operations generating OEM coating procurement. The Coal India Limited (CIL)'s large-scale fleet procurement programs, with CIL being the world's largest coal mining company by production volume, and the expansion of iron ore, bauxite, and limestone mining operations by NMDC, Steel Authority of India (SAIL), and Vedanta Resources sustain premium industrial coating procurement from OEM coating suppliers including Asian Paints PPG's industrial coatings division, Axalta Coating Systems, and The Sherwin-Williams Company's India operations.

Restraints - Volatile Raw Material Prices for Resins, Pigments, and Solvents Creating OEM Coating Production Cost Instability

The Indian Construction Equipment OEM Coating market faces persistent production cost challenges arising from the price volatility of key coating raw materials, particularly titanium dioxide (TiO2) pigments, acrylic and polyurethane resin monomers, epoxy hardeners, and organic solvent carriers, which are substantially imported or derived from petroleum feedstocks whose prices fluctuate with global crude oil price movements, shipping cost dynamics, and foreign exchange rate variations. The Indian Chemical Council (ICC) and paint industry data document that raw material costs represent approximately 55–65% of total coatings production cost for Indian manufacturers, making the sector highly vulnerable to input cost inflation that compresses operating margins and reduces pricing competitiveness.

The INR/US exchange rate depreciation trajectory-which has seen the Indian Rupee depreciate from approximately INR74/US in 2021 to INR83+/US$ in 2025, directly inflates import costs for raw materials, creating structural cost pressure that smaller Indian OEM coating manufacturers find particularly challenging to absorb within competitive OEM supply contract pricing frameworks.

Environmental Compliance Costs for Solvent-Borne Coating Formulations Under India's Volatile Organic Compound Regulations

The Central Pollution Control Board (CPCB)'s environmental standards and Environment (Protection) Rules frameworks governing Volatile Organic Compound (VOC) emissions from industrial coating operations, and the progressive adoption of Bureau of Energy Efficiency (BEE) and National Action Plan on Climate Change (NAPCC)-aligned industrial environmental standards, are increasing compliance costs for construction equipment OEM coating manufacturers and applicators relying on solvent-borne coating formulations with high VOC content.

Transitioning from solvent-borne to water-borne or high-solids coating formulations requires capital investment in reformulated product R&D, application equipment upgrades, and surface preparation process modifications that impose incremental costs on Indian construction equipment OEMs without commensurate near-term revenue increases, creating a financial disincentive that slows the rate of voluntary compliance investment particularly among smaller domestic equipment manufacturers.

Opportunity - Water-Borne Coating Technology Adoption Driven by CPCB Regulations and Green Infrastructure Procurement Mandates

The Central Pollution Control Board (CPCB)'s progressively tightening environmental standards for VOC emissions from industrial paint shops, combined with the Ministry of Environment, Forest and Climate Change (MoEFCC)'s industrial pollution prevention guidelines and the Green Rating for Integrated Habitat Assessment (GRIHA) framework promoting environmentally responsible industrial manufacturing practices, are compelling India's construction equipment OEM manufacturers to transition their coating application systems from conventional solvent-borne formulations to compliant water-borne and high-solids coating alternatives, creating a substantial commercial opportunity for OEM coating suppliers with established water-borne technology portfolios able to serve this mandatory reformulation transition. Asian Paints PPG, India's most commercially significant construction equipment OEM coating supplier, has been investing in water-borne industrial coating product development through its joint venture with PPG Industries leveraging PPG's global water-borne coating technology portfolio to develop India-specific water-borne construction equipment coating formulations that meet CPCB VOC compliance standards while delivering performance equivalence to solvent-borne systems under Indian tropical climate application conditions.

The Green Public Procurement (GPP) guidelines being adopted within Government of India infrastructure project specifications, particularly for metro rail, smart city, and National Highway construction programs, are increasingly specifying low-VOC and environmentally certified coating systems for construction equipment deployed on public infrastructure sites, creating institutional procurement preference that directly favors water-borne OEM coating suppliers.

Electro-Coating Technology Expansion in Indian Construction Equipment Manufacturing Creating Premium Process Upgrade Opportunity

The rapid scaling of India's construction equipment domestic manufacturing capacity, stimulated by Make in India initiative incentives, Production Linked Incentive (PLI) scheme benefits for automotive and engineering equipment manufacturing, and major OEM capacity investments by JCB India (expanding its Pune and Faridabad plants), Tata Hitachi Construction Machinery (expanding its Dharwad facility), and L&T Construction Equipment (CASE India), is creating a compelling commercial opportunity for electro-coating (e-coat) technology suppliers and OEM coating service providers able to serve the captive paint shop infrastructure investment programs of India's construction equipment manufacturing expansion.

Electro-coating technology, which delivers exceptionally uniform coating thickness 20–30 micrometers on complex three-dimensional equipment components through electrodeposition, providing superior corrosion protection documentation compared to conventional spray application, is the premium coating application technology standard for equipment OEMs globally, with leading Indian equipment manufacturers progressively upgrading their paint shop infrastructure from conventional air-spray systems to automated electro-coat plus topcoat integrated paint lines. Axalta Coating Systems (a Carlyle Group company with significant Indian industrial coatings operations) and The Sherwin-Williams Company's India operations are both positioned to capture the premium e-coat capable OEM coating supply contracts generated by India's construction equipment manufacturing expansion programs through the forecast period.

Category-wise Analysis

By Material Type Insights

Epoxy leads the India Construction Equipment OEM Coating market by material type, accounting for approximately 34% of total material type segment revenue in 2026, a commercially dominant position anchored in epoxy coatings' technically superior anti-corrosion performance, exceptional adhesion to steel substrates, high film hardness, and chemical resistance that make them the universally preferred primer and intermediate coat material for construction equipment OEM paint systems operating in India's harsh tropical climate, high-humidity, and chemically aggressive construction site environments.

Epoxy coatings, particularly two-component epoxy zinc-rich primers and epoxy polyamide intermediate coats, are specified as the mandatory primer system in virtually all construction equipment OEM paint specifications from major Indian equipment manufacturers including JCB India, BEML, and Tata Hitachi due to their documented performance in corrosion protection qualification testing per IS 101 and ASTM B117 salt spray standards.

Polyurethane coatings hold the second-largest material type share at approximately 28%, dominant as topcoat materials for their UV resistance, gloss retention, and color durability in outdoor construction equipment applications, with Asian Paints PPG's polyurethane topcoat range and Berger Paints' industrial polyurethane products serving the dominant OEM coating procurement volumes.

By Formulation Insights

Solvent-borne Solutions currently lead the India Construction Equipment OEM Coating market by formulation, commanding approximately 58% of total formulation segment revenue in 2026, a dominant market position reflecting the established industrial preference for solvent-borne coating formulations in Indian construction equipment OEM manufacturing operations due to their wide application temperature window compatible with Indian ambient conditions, proven long-term corrosion protection performance under tropical climate exposure, compatibility with existing conventional spray application equipment infrastructure, and cost-competitiveness at the paint shop production economics level familiar to Indian OEM procurement teams.

India's tropical climate, characterized by high ambient temperature and humidity during monsoon seasons and extreme UV exposure during summer months, has historically favored solvent-borne epoxy and polyurethane formulations with proven field durability data from Indian construction site exposure conditions. However, Water-borne Solutions are the fastest-growing formulation segment, at approximately 32% of revenue in 2026 and accelerating, driven by CPCB VOC compliance mandates and OEM sustainability commitments, with Asian Paints PPG and Kansai Paints investing in water-borne product development for this structurally growing segment.

By Technology Insights

Spraying leads the India Construction Equipment OEM Coating market by technology, commanding approximately 62% of total technology segment revenue in 2026, reflecting the widespread deployment of conventional air atomization, airless, and high-volume-low-pressure (HVLP) spray application systems across Indian construction equipment manufacturing facilities as the established standard coating application technology for primer, intermediate, and topcoat layer application at Indian OEM production capacities and investment levels.

Spray application technology's versatility across coating formulation types, relatively low capital investment requirements, and established workforce skill base in Indian industrial paint shops sustain its dominant technology position across the Indian construction equipment OEM manufacturing ecosystem.

Electro-coating technology holds approximately 28% of technology revenue, and is the fastest-growing technology segment, driven by premium OEM manufacturing plant upgrades at JCB India's expanded production facilities and the adoption of automated e-coat plus topcoat integrated paint line systems by leading Indian construction equipment manufacturers investing in global production quality standards.

By Application Insights

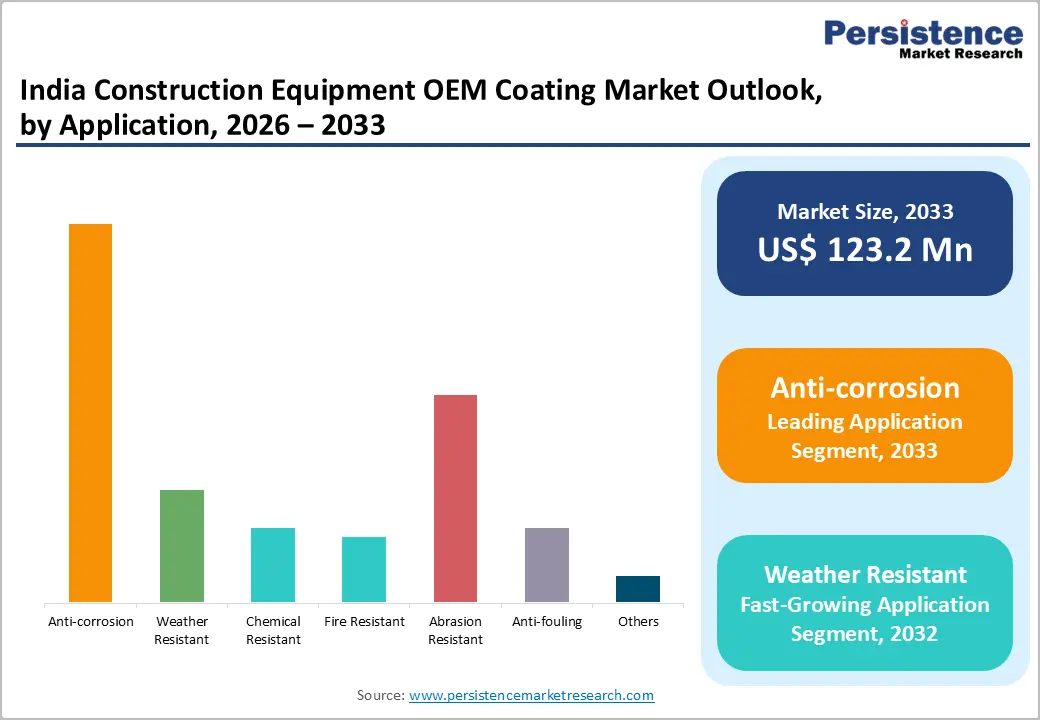

Anti-corrosion leads the India Construction Equipment OEM Coating market by application, commanding approximately 40% of total application segment revenue in 2026, a dominant position reflecting corrosion protection's foundational and commercially non-negotiable role in construction equipment OEM coating specifications across all equipment categories and end-use operating environments in India. India's tropical climate, with annual average humidity above 70% across most of the country's construction-active geographies and monsoon-season rainfall generating prolonged equipment surface moisture exposure, creates some of the world's most aggressive corrosion environments for steel-bodied construction equipment operating outdoors on road, railway, port, and building construction sites.

The National Corrosion Council of India (NCCI) has documented that corrosion causes economic losses of approximately INR1.5 lakh crore annually in India, with construction equipment and industrial machinery representing significant contributors to this national corrosion cost burden, reinforcing the commercial justification for premium anti-corrosion OEM coating system investment by equipment manufacturers seeking to deliver longer equipment service life and reduced field maintenance costs to their institutional government procurement customers. Abrasion Resistant coatings hold the second-largest application share at approximately 22%, driven by mining equipment applications.

By End-user Insights

Earthmoving Equipment leads the India Construction Equipment OEM Coating market by end use, accounting for approximately 45% of total end-use segment revenue in 2026, a dominant market position reflecting earthmoving equipment's structural concentration of the highest-volume and most widely deployed construction equipment categories in India's infrastructure construction ecosystem, encompassing hydraulic excavators, backhoe loaders, motor graders, compactors, and wheel loaders that collectively represent the dominant portion of ICEMA's documented 125,000 unit annual construction equipment sales volume.

ICEMA's market data confirms hydraulic excavators as India's single highest-volume construction equipment category, with 50,000+ units sold annually representing the largest individual equipment segment driving OEM coating procurement from suppliers including Asian Paints PPG, Berger Paints, and Kansai Paints for domestically manufactured equipment. Mining and Digging Equipment holds the second-largest end-use share at approximately 27%, driven by Coal India Limited, NMDC, and Vedanta's equipment fleet expansion programs procuring heavy-duty mining equipment requiring premium abrasion-resistant and chemical-resistant coating systems.

Regional Insights

North India Construction Equipment OEM Coating Trends

North India leads the Indian Construction Equipment OEM Coating market, anchored by the concentration of major infrastructure construction activity along the Delhi–Mumbai Industrial Corridor (DMIC), the Eastern Dedicated Freight Corridor (EDFC), and the National Capital Region (NCR)'s massive metro rail, expressway, and smart city development programs generating the highest equipment utilization density in India. The National Highways Authority of India (NHAI) has documented Uttar Pradesh, Haryana, Punjab, and Rajasthan as among the highest national highway construction activity states, generating large and sustained construction equipment fleet deployment volumes sustaining OEM coating procurement from the region's industrial coating supply chain. JCB India's manufacturing plant in Faridabad, Haryana and BEML's equipment assembly operations in Delhi NCR sustain substantial regional OEM coating procurement volumes from North Indian industrial coating suppliers.

Uttar Pradesh's infrastructure development acceleration under the UP Expressways Industrial Development Authority (UPEIDA) and the Bundelkhand Expressway, Poorvanchal Expressway, and Ganga Expressway construction programs, representing collectively over INR35,000 crore in expressway investment, are sustaining above-average construction equipment fleet demand in North India. The Delhi Metro Rail Corporation (DMRC)'s Phase IV expansion program and planned metro projects in Lucknow, Kanpur, and Varanasi further sustain North India's position as India's highest-concentration construction equipment deployment region, making it the dominant OEM coating consumption geography for Asian Paints PPG's and Berger Paints' industrial coating divisions serving North Indian OEM manufacturing facilities.

West India Construction Equipment OEM Coating Trends

West India is a commercially significant and rapidly growing regional market for Construction Equipment OEM Coatings, anchored by Maharashtra's position as India's largest state economy with the most active infrastructure and real estate construction investment, Gujarat's industrial manufacturing concentration including construction equipment OEM production facilities, and Rajasthan's large-scale renewable energy and mining construction program driving regional equipment fleet demand.

JCB India's primary manufacturing complex in Pune, Maharashtra, one of the company's largest global production facilities with over 100,000 sq. m. of manufacturing floor space, is West India's most significant construction equipment OEM coating procurement anchor, sourcing industrial coating products from Asian Paints PPG's Pune manufacturing operations and regional coating distributors.

The Mumbai-Ahmedabad High Speed Rail (MAHSR) project and Mumbai Metropolitan Region Development Authority (MMRDA)'s metro expansion programs sustain large construction equipment fleet deployments generating regional OEM coating demand.

Gujarat's industrial manufacturing ecosystem, stimulated by the Gujarat Industrial Development Corporation (GIDC) and the state's world-class GIFT City, Dholera Special Investment Region (DSIR), and Mandal Becharaji Special Investment Region manufacturing zone programs, is hosting new construction equipment manufacturing and maintenance facilities that sustain West India's OEM coating procurement growth. Axalta Coating Systems' India distribution network and The Sherwin-Williams Company's industrial coatings operations serve the West Indian construction equipment OEM coating market through established Pune and Mumbai distribution hubs. Grand Polycoats and Zigma Paints, both Indian specialty industrial coating companies, serve regional construction equipment OEM clients with customized anti-corrosion and weather-resistant coating solutions.

South India Construction Equipment OEM Coating Trends

South India is the fastest-growing regional market for Construction Equipment OEM Coatings in India, driven by Karnataka's technology-led infrastructure expansion, Tamil Nadu's world-class manufacturing industry attracting construction equipment OEM investment, Telangana's aggressive industrial infrastructure development, and the region's significant mining activity across iron ore, granite, and mineral sand extraction operations generating above-average heavy-duty OEM coating demand from mining equipment operators.

Tata Hitachi Construction Machinery's manufacturing facility in Dharwad, Karnataka, one of India's most modern construction equipment production plants, and L&T Construction Equipment (CASE India)'s South Indian manufacturing presence sustain substantial regional OEM coating procurement volumes that make South India a strategically important geography for coating suppliers establishing regional manufacturing and distribution capabilities.

Tamil Nadu's manufacturing competitiveness, anchored by the Tamil Nadu Industrial Development Corporation (TIDCO) and the state's globally recognized automotive and engineering manufacturing clusters in Chennai, Coimbatore, and Hosur, is attracting construction equipment component manufacturing investment that sustainably expands the OEM coating procurement base.

Sheenlac Paints (headquartered in Chennai, Tamil Nadu), a specialist Indian industrial coating company with a focused construction equipment and industrial machinery coating portfolio, is uniquely positioned as a South India-headquartered OEM coating supplier serving regional construction equipment manufacturers with technically certified coating solutions aligned with tropical climate exposure durability requirements documented by the Bureau of Indian Standards (BIS).

Competitive Landscape

The India Construction Equipment OEM Coating market is moderately fragmented, with Asian Paints PPG, Berger Paints, and Kansai Paints commanding tier-1 positions through large-scale manufacturing infrastructure, technically certified industrial coating portfolios, and long-term OEM supply agreements with major construction equipment manufacturers. Axalta Coating Systems and The Sherwin-Williams Company compete through global technology transfer, premium e-coat system capabilities, and multinational OEM customer alignment.

Domestic specialists Sheenlac, Grand Polycoats, Dev Industrial Coatings, and Zigma Paints compete on regional market proximity, customization responsiveness, and cost-competitive pricing for Indian OEM procurement. Emerging trends include water-borne coating system transition driven by CPCB compliance mandates, automated electro-coat line supply contracts tied to OEM plant upgrades, and digitally integrated color management and supply chain service models.

Key Developments:

- In February 2025, Asian Paints PPG launched an expanded range of water-borne industrial anti-corrosion primers and polyurethane topcoats specifically engineered for construction equipment OEM applications, targeting CPCB VOC compliance requirements while delivering monsoon-climate durability performance benchmarks validated through accelerated weathering testing per BIS IS 101 standards at its Mumbai industrial coatings technical center.

- In October 2024, JCB India announced an expansion of its Pune manufacturing facility with a new automated electro-coat plus powder primer paint shop, representing an investment of approximately INR200 crore and establishing one of India's most technologically advanced construction equipment OEM coating application lines, generating premium e-coat capable coating supply procurement from qualified industrial coating partners.

- In March 2024, Axalta Coating Systems expanded its India industrial coatings distribution network by establishing three new regional technical service centers across Delhi NCR, Pune, and Chennai, targeting the growing construction equipment OEM and heavy industrial machinery coating market with application engineering support services and technically qualified coating system recommendations for Indian tropical climate exposure conditions.

Companies Covered in India Construction Equipment OEM Coating Market

- Asian Paints PPG

- Berger Paints India Ltd.

- Kansai Paints India Ltd.

- Axalta Coating Systems

- The Sherwin-Williams Company

- Zigma Paints

- Grand Polycoats

- Dev Industrial Coatings

- Sheenlac Paints

Frequently Asked Questions

The India Construction Equipment OEM Coating market is estimated to be valued at US$ 62.4 Million in 2026 and is projected to reach US$ 123.2 Million by 2033, registering a forecast CAGR of 10.2% from 2026 to 2033.

The primary drivers are the Government of India's Union Budget 2024–25 allocating a record INR11.11 lakh crore (3.4% of GDP) for capital expenditure funding NHAI highway construction, metro rail, and port modernization programs, and Coal India Limited, NMDC, and Vedanta's mining fleet expansion under the Ministry of Mines' accelerated mineral concession allocation program, collectively sustaining India's highest-ever construction equipment production volumes documented by ICEMA at approximately 125,000 units annually, generating structurally growing OEM coating procurement.

Epoxy leads the Material Type segment with approximately 34% revenue share in 2026, anchored by its mandatory specification as the primer system in construction equipment OEM paint standards at JCB India, BEML, and Tata Hitachi, validated corrosion protection per IS 101 and ASTM B117 salt spray standards, and technically superior adhesion and anti-corrosion performance under India's tropical climate exposure conditions. Asian Paints PPG and Berger Paints are the dominant epoxy-based OEM coating suppliers to Indian construction equipment manufacturers.

North India leads the India Construction Equipment OEM Coating market, anchored by JCB India's Faridabad manufacturing facility, NHAI's highest construction activity in Uttar Pradesh and Haryana, the Delhi–Mumbai Industrial Corridor (DMIC), Eastern Dedicated Freight Corridor (EDFC) construction programs, and Delhi NCR's metro rail Phase IV expansion program collectively generating India's highest construction equipment fleet deployment density and corresponding OEM coating procurement volumes.

The most significant opportunity is electro-coating technology adoption and water-borne coating formulation transition, with JCB India's INR200 crore automated e-coat plant investment (October 2024), PLI scheme construction equipment manufacturing expansion programs attracting multinational OEM paint shop upgrade investments, and CPCB VOC compliance mandates compelling water-borne system transition that creates premium supply contract opportunities for technically certified e-coat and compliant water-borne OEM coating providers through the 2026–2033 forecast period.