- Automotive

- Fuel Cell Commercial Vehicle Market

Fuel Cell Commercial Vehicle Market Size, Share, Trends, and Growth Forecast for 2025 - 2032

Fuel Cell Commercial Vehicle Market By Fuel Cell Type (Proton Exchange Membrane FC, Solid Oxide FC, Molten Carbonate FC, Phosphoric Acid FC, Other), Range (Below 400 km, 400 to 600 km, Above 600 km), Vehicle Type, and Regional Analysis for 2025 - 2032

Fuel Cell Commercial Vehicle Market Size and Trends

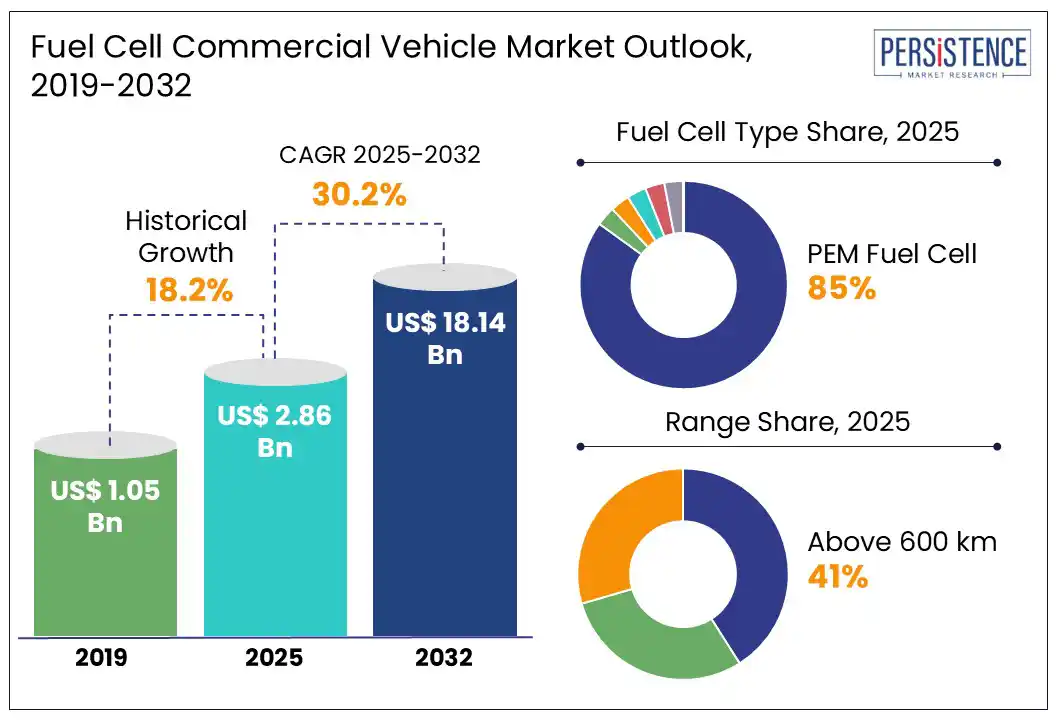

The global fuel cell commercial vehicle market size is likely to be valued at US$ 2.86 Bn in 2025 and is estimated to reach US$ 18.14 Bn in 2032, growing at a CAGR of 30.2% during the forecast period 2025 - 2032. The fuel cell commercial vehicle market is expected to grow through 2032, driven by strict GHG emission regulations and government support for fuel cell hybrid technologies, which is boosting innovation in vehicle design for enhanced efficiency and extended driving range.

According to the IEA, global electric vehicle sales were around 2.2 million units in 2019 and reached 18.3 million units in 2024. This represents a massive growth in just five years. The surge highlights accelerating adoption, fueled by technological advancements, government incentives, and growing consumer demand.

Key Industry Highlights:

- Government incentives and emission regulations are driving global fuel cell vehicle adoption through subsidies, tax breaks, and hydrogen infrastructure investments in countries including the U.S., Germany, Japan, and China.

- The integration of hydrogen refueling stations along long-haul freight corridors presents strong growth potential for heavy commercial fuel cell vehicles.

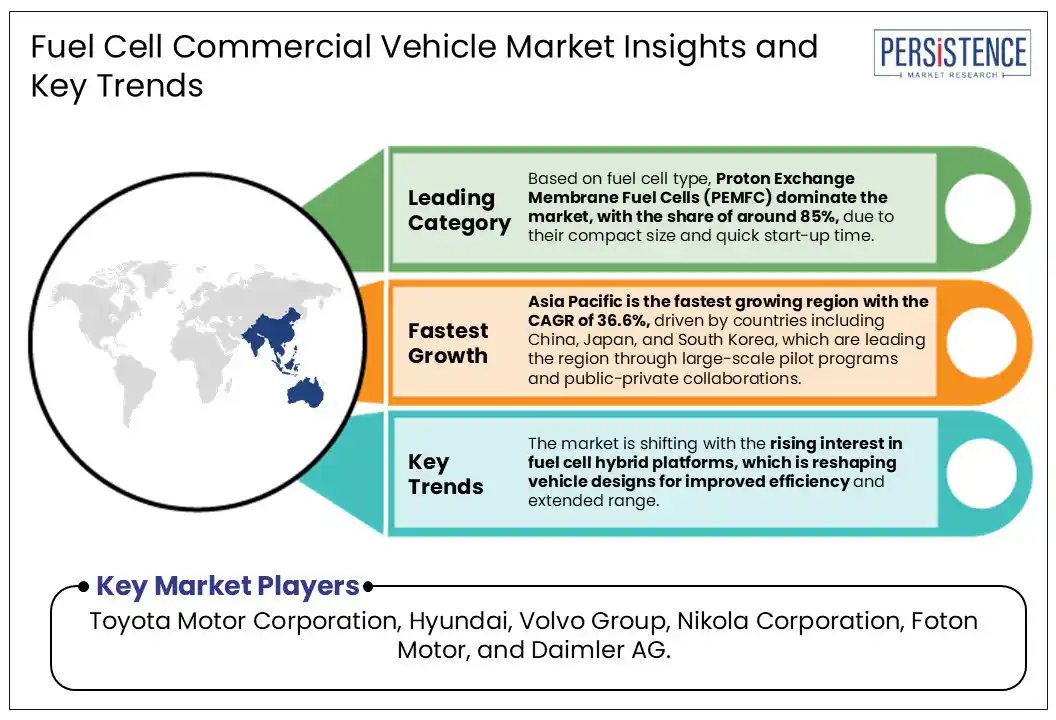

- Based on fuel cell type, the Proton Exchange Membrane Fuel Cells (PEMFC) segment is likely to dominate with a market share of around 85%, due to their compact size and quick start-up time.

- Based on range, the above 600 km segment is expected to lead with around 41% market share, due to increasing adoption of FCCVs in inter-city and transnational freight operations.

- Based on vehicle type, the heavy commercial vehicle segment is projected to lead with approximately 40% market share, driven by demand for decarbonized freight movement in Asia Pacific and Europe.

- Asia Pacific is anticipated to dominate with over 65% market share, through large-scale pilot programs and public-private collaborations.

- North America is focused on LCVs powered by PEMFCs, targeting last-mile delivery and urban freight.

- Europe is investing in MCVs, suitable for regional logistics, supported by the EU’s “Fit for 55” and Hydrogen Strategy to promote decarbonization across the transport sector.

|

Market Attribute |

Key Insights |

|

Fuel Cell Commercial Vehicle Market Size (2025E) |

US$ 2.86 Bn |

|

Projected Market Value (2032F) |

US$ 18.14 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

30.2% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

18.2% |

Market Dynamics

Driver - Government Incentives and Emission Targets Drive Fuel Cell Vehicle Deployment

The fuel cell commercial vehicle market is experiencing rapid growth, driven by strong government support, expanding infrastructure, and strategic industry investments. In 2023, China emerged as the largest market, accounting for an impressive 92% of total global registrations of fuel cell vehicles. The U.S. government, under the Biden-Harris administration, announced over US$ 600 Mn in grants to develop hydrogen refueling and EV charging infrastructure. Europe added over 37 hydrogen refueling stations in 2023 alone, underlining its commitment to hydrogen mobility.

Industry players are investing in product innovation to reinforce this momentum. For instance, in February 2025, Toyota Motor Corporation introduced a new fuel cell (FC) system, its third-generation fuel cell system, designed to meet the particular needs of the commercial sector. In addition to passenger vehicles, the 3rd Gen FC System will be customized for use in heavy-duty commercial vehicles, and is set to be launched in Japan, Europe, North America, and China after 2026.

Restraint - High Costs and Infrastructure Gaps to Hamper Widespread Adoption of Fuel Cell Commercial Vehicles

The fuel cell commercial vehicle market faces major restraints, largely due to the high cost of hydrogen fuel cell production. Producing hydrogen is expensive due to high cost of fuel cell systems and materials such as platinum with the complex manufacturing process. These factors make the FCCVs more expensive as compared to conventional vehicles.

Furthermore, the global hydrogen refueling station network is not completely developed, having wide regional disparities. While countries including Japan, Germany, and China have made significant progress, most of Southeast Asia, Latin America, and parts of Eastern Europe lack the foundational hydrogen infrastructure.

These factors limit the vehicle adoption and investor confidence, particularly in emerging economies. Without the coordinated global expansion and cost reduction strategies, these challenges will continue to hinder large scale FCCV adoption.

Opportunity - Global Push for Decarbonization Opens Scalable Opportunities for Fuel Cell Truck and Bus Adoption

The global movement toward the decarbonization with the help of government initiatives, especially in transportation sector, presents a strong opportunity for the FCCV market. With a projected global fleet of 200,000 fuel cell EVs by 2030, the demand for hydrogen infrastructure and vehicle deployment is accelerating.

China’s aggressive hydrogen strategy positions the region as a key growth hub. The rapid rollout of city buses in China highlight the expanding role of public fleets. In South Korea, government support and plans to scale fuel cell bus deployments position it as a future global leader in the segment. These developments open significant opportunities for OEMs, fuel cell suppliers, and infrastructure developers.

The market players are expanding the hydrogen infrastructure to support market growth. For instance, in July 2025, Toyota announced plans to invest US$ 139 Mn through a joint venture with Shudao Investment Group to build a hydrogen fuel cell manufacturing base in Chengdu, China. The facility will focus on producing FC systems and components for heavy-duty commercial vehicles, aiming to bolster China’s hydrogen ecosystem.

Category-wise Analysis

Fuel Cell Type Insights

By fuel cell types, the proton exchange membrane fuel cells segment is projected to lead, accounting for approximately 85% market share in 2025, driven by their superior power density and adaptability to diverse duty cycles. The growing demand for PEMFC is owing to benefits such as flexibility in input fuel, compact design, and solidity of electrolyte.

PEM fuel cells are mostly applied in HCVs with a range of around 400 km. In February 2023, top fuel cell system vendors supplied a total of 127 fuel cell systems for buses and trucks, with a power rating of around 10,300 KW. Toyota ranked top in both installation units and power rating, with respective market shares of 47.2% and 43.4%.

The manufacturers are developing product systems to meet the growing demand as well as to comply with environmental regulations. For instance, in July 2025, Hyundai Hydrogen Mobility (HHM) assisted municipal services and recycling centers to take a major step toward zero-emission operations. Hyundai combined the proven advantages of the XCIENT Fuel Cell truck with a range of over 400 km, refueling in just 15 minutes, full-day usability, diesel-comparable payload, low-noise operation, and zero CO2 emissions.

Range Insights

By range, FCCVs with a range above 600 km are projected to lead in 2025, accounting for a market share of approximately 41%, due to their suitability for long-haul logistics and intercity transportation. Unlike battery-based EVs, fuel cell systems offer extended driving ranges with minimal refueling time, making them ideal for freight operations.

Owing to the growing interest in high range vehicles, China, a dominant player and is deploying the fuel cell commercial vehicles by offering favorable conditions for market players. In April 2025, Toyota, Shudao Investment Group, and Sichuan Shudao signed a joint venture, focusing on hydrogen fuel cell production, sales, and after-sales services, aiming to develop the hydrogen economy in China's southwestern region.

The global market players are investing in product innovation to meet the rising demand for high range vehicles. For instance, in September 2024, Ballard designed its most powerful fuel cell technology, the FCmove®-XD fuel cell engine, which delivered class-leading volumetric power density and the lightest in its power range. The module is designed with a driving range up to 800 km to support the volumetric power density that is the highest in the global truck industry.

Vehicle Type Insights

By vehicle type, the heavy commercial vehicles segment is expected to dominate the fuel cell commercial vehicle market with a share of around 40%, driven primarily due to their high energy demands and long run cycles. The demand is also increasing due to the limitations of battery-based alternatives in freight logistics.

Fuel cell technology, offering fast refueling and extended ranges over 600 km is particularly well-suited for trucks, intercity buses, and logistics fleets. China remains at the forefront, with city and long-haul buses driving the majority of new energy vehicle adoption.

The manufacturers are partnering with players in the emerging region to expand their market reach. For instance, in March 2025, TR Group, in partnership with Global Bus Ventures (GBV), and Toyota New Zealand, launched a hydrogen 50-tonne prime mover. The truck, retrofitted as a zero-emission fuel cell electric vehicle conversion by local experts at GBV, offers a practical zero-emissions solution for heavy freight transport.

Regional Insights

Asia Pacific Fuel Cell Commercial Vehicle Market Trends

Asia Pacific is anticipated to lead, accounting for a market share of 65% in 2025, driven by ambitious hydrogen strategies and strong OEM participation across China, South Korea, and Japan. In 2023, China overtook South Korea as the largest market for fuel cell vehicle registrations. In South Korea, despite a decline in passenger FCV sales, commercial fuel cell vehicle registrations grew to 381 units in 2023. The country is also projected to become the world’s largest fuel cell bus market. In Japan, automakers including Toyota, Hino, Isuzu, and Honda are shifting focus to fuel cell trucks, backed by pilot programs and government support.

The other emerging economies are also investing in the market. For instance, in May 2025, Adani Group, a multinational conglomerate, took a major step toward more sustainable practices in mining logistics by introducing India’s first hydrogen-powered truck, to gradually replace its diesel-based fleet with fuel cell alternatives. Ballard powered the initiative with its FCmove®-XD fuel cell engine in collaboration with automotive manufacturer Ashok Leyland.

North America Fuel Cell Commercial Vehicle Market Trends

North America is a growing market for FCCV deployment, supported by strong federal initiatives and growing investments in clean transportation infrastructure. The U.S. FCCV market is steadily advancing, with states including California emerging as the epicenter of development. The California Air Resources Board (CARB) mandates that, beginning in 2024, only zero-emission trucks may be purchased for port operations.

The U.S. market is particularly focused on light and heavy commercial vehicles, including long-haul trucks and delivery fleets, where fuel cells offer superior range and rapid refueling advantages over battery-electric alternatives. The manufacturers are investing heavily in hydrogen stations. For instance, Nikola Corporation launched its first mobile hydrogen station under the HYLA brand in 2024, with plans to deploy nine more by year-end, signaling a shift toward freight-focused hydrogen infrastructure.

Europe Fuel Cell Commercial Vehicle Market Trends

Europe fuel cell commercial vehicle market is shifting strategically toward heavy-duty applications, driven primarily by robust policy mandates and industry realignment. In 2023, the EU approved the Alternative Fuels Infrastructure Regulation (AFIR), mandating hydrogen refueling infrastructure across all urban nodes and every 200 km along the TEN-T core network by 2030.

The European Union’s “Fit for 55” and Hydrogen Strategy are driving the decarbonization efforts in the transport sector, especially in heavy-duty segments. In January 2025, the Federal Ministry for Digital and Transport and the federal states of Germany approved funding totaling € 226 Mn (US$ 235 Mn) for the development, small-series production, and customer deployment of 100 fuel cell trucks. For instance, in January 2024, Air Liquide and TotalEnergies formed TEAL Mobility to deploy over 100 hydrogen refueling stations for heavy-duty vehicles across Europe.

Competitive Landscape

The global fuel cell commercial vehicle market is moderately consolidated with intense participation from established automotive manufacturers and fuel cell technology providers. Leading players are focusing on expanding their regional presence, enhancing fuel cell power, and reducing production costs to improve their market presence.

The market is witnessing increased collaboration between vehicle OEMs and hydrogen infrastructure developers to address fueling challenges. The competition is especially strong in regions including Asia Pacific, Europe, and North America, where regulatory mandates and public funding are accelerating fuel cell truck and bus adoption.

Key Industry Developments

- In March 2025, Ballard Power Systems announced a multi-year supply agreement from Manufacturing Commercial Vehicles, a leading commercial vehicle manufacturer based in Egypt, for fuel cell engines totaling approximately 5 MW. The agreement includes the supply of 50 FCmove®-HD+ engines, with an initial order of 35 units.

- In June 2025, Foton Mobility and KRW Hydron launched a full range of hydrogen, electric, and diesel commercial vehicles in New Zealand, including the Quantum H53 hydrogen prime mover. The portfolio comprises a full lineup of zero-emission and low-emission trucks and buses, including hydrogen fuel cell models.

Companies Covered in Fuel Cell Commercial Vehicle Market

- Hyundai Motor Company

- Toyota Motor Corporation

- Ballard Power Systems

- Volvo Group

- Nikola Corporation

- Foton Motor

- Scania

- Daimler AG

- General Motors

- Traton Group

Frequently Asked Questions

Yes, the fuel cell commercial vehicle market is set to reach US$ 18.14 Bn by 2032.

The strong policy frameworks from the government, infrastructure development, and escalating OEM activities are propelling the FCCV market growth.

The Heavy Commercial Vehicle (HCV) is the fastest-growing vehicle type.

India is estimated to witness a positive CAGR during the forecast period from 2025 to 2032.

Toyota Motor Corporation is considered the leading player.