- Power Generation, Transmission, & Distribution

- Nuclear Fuel Market

Nuclear Fuel Market Size, Share, and Growth Forecast, 2025 - 2032

Nuclear Fuel Market By Product Type (Mixed Oxide (MOX) Fuel, Uranium Fuel, Others), Application (Nuclear Power Plants, Nuclear Research Labs, Others), End-use (Chemical Petrochemical, Energy Power, Others), and Regional Analysis for 2025 – 2032

Nuclear Fuel Market Size and Trends Analysis

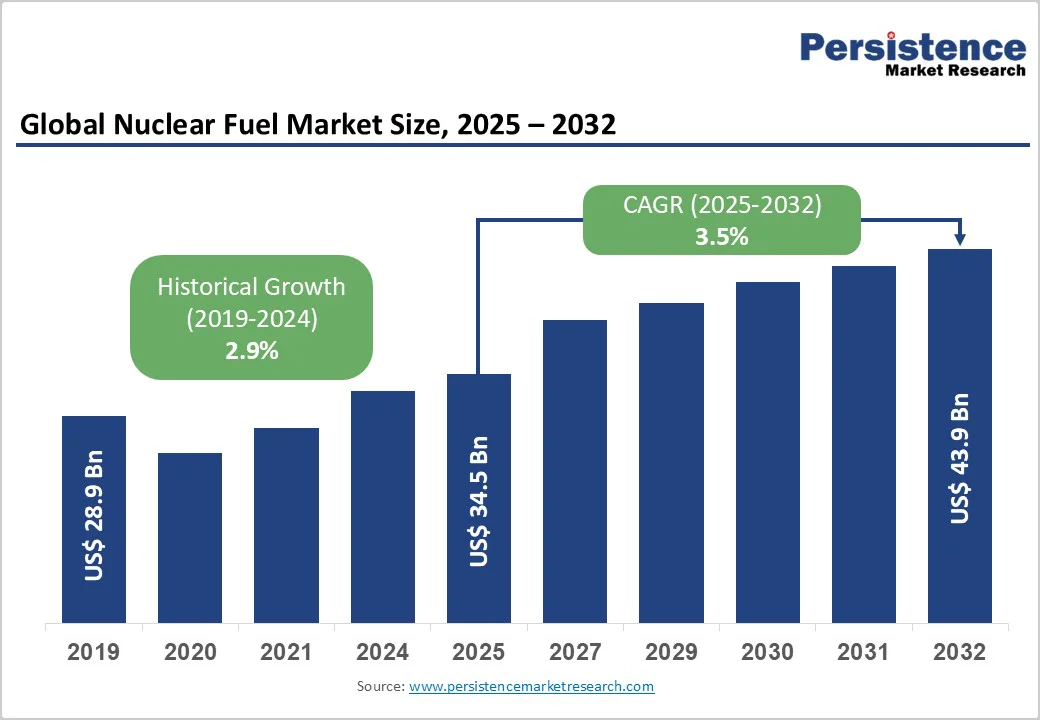

The global nuclear fuel market size is likely to be valued US$34.5 Billion in 2025, forecasted to reach at US$43.9 Billion by 2032 with growing at a CAGR of 3.5% during the forecast period from 2025 to 2032, driven by the increasing emphasis on low-carbon energy sources, rising demand for reliable baseload power amid global energy security concerns, and advancements in nuclear reactor technologies.

The market is further propelled by innovations in MOX fuel recycling and high-assay low-enriched uranium (HALEU), catering to preferences for efficient and waste-reducing options. The growing acceptance of atomic fuel as a key enabler for net-zero emissions, especially in regions with ambitious climate goals, is a key growth factor.

Key Industry Highlights:

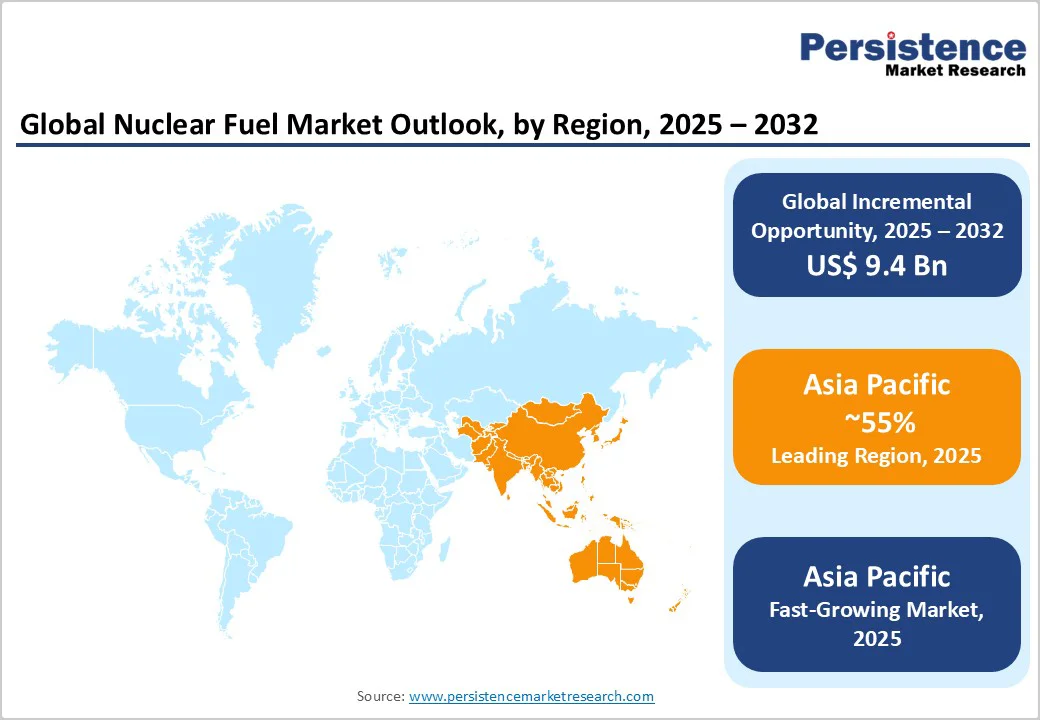

- Leading Region: Asia Pacific, commanding a 55% market share in 2025, driven by massive capacity expansions in China and India.

- Fastest-growing Region: Asia Pacific, fueled by surging energy demand and low-carbon transition initiatives.

- Dominant Product Type: Uranium Fuel, holding approximately 95% of the market share, due to its established use in light-water reactors.

- Leading Application: Nuclear Power Plants, accounting for over 90% of market revenue, driven by global reactor fleet growth.

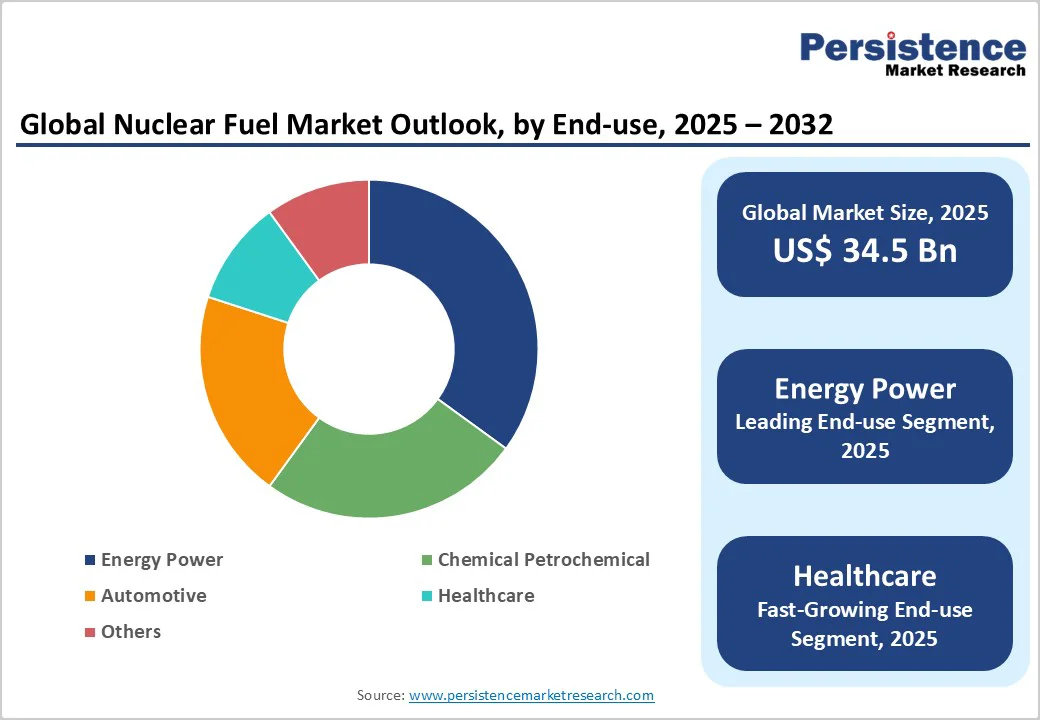

- Leading End-use: Energy Power, contributing nearly 80% of market revenue, owing to baseload electricity generation needs.

- Key Market Driver: The market driver for the nuclear fuel sector is the growing demand for low-carbon, reliable baseload electricity combined with energy security concerns.

- Growth Opportunity: Advancements in MOX recycling and HALEU for advanced reactors, enabling waste reduction and efficiency gains.

| Key Insights | Details |

|---|---|

|

Nuclear Fuel Market Size (2025E) |

US$34.5 Bn |

|

Market Value Forecast (2032F) |

US$43.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Demand for Low-Carbon Baseload Power and Energy Security

The nuclear fuel market is strongly driven by the growing demand for low-carbon baseload power and the need for energy security. Nuclear energy provides a reliable, continuous source of electricity, unlike intermittent renewables such as solar and wind, making it essential for stable grid operations. Governments worldwide are increasingly prioritising nuclear power to meet climate targets, reduce greenhouse gas emissions, and transition toward sustainable energy systems. This is particularly relevant as countries aim to achieve net-zero goals, with nuclear power offering a scalable solution for decarbonising electricity generation.

Energy security concerns further amplify fission fuel demand. Geopolitical tensions, fluctuating fossil fuel prices, and dependence on imported energy sources have motivated nations to diversify their energy mix. Nuclear power, supported by domestic uranium mining and fuel fabrication where possible, reduces vulnerability to supply disruptions and price volatility. Emerging markets in the Asia Pacific, led by China and India, are expanding nuclear fleets to satisfy rising electricity consumption, while established markets in North America and Europe are modernising reactors and pursuing fuel recycling programs

Regulatory Hurdles and High Capital Costs

The nuclear fuel market faces substantial challenges due to stringent regulatory hurdles and high capital costs, which collectively slow expansion and increase financial risk. Nuclear projects are heavily regulated to ensure safety, security, and environmental compliance, with oversight from national authorities and international organisations such as the International Atomic Energy Agency (IAEA). Licensing processes for uranium mining, enrichment, fuel fabrication, and reactor operations are lengthy and complex, often taking several years to complete. These regulations, while essential for public safety, increase project timelines and administrative costs, creating barriers for new entrants and smaller players.

High capital costs further constrain market growth. Construction of nuclear reactors, fuel fabrication facilities, and enrichment plants requires billions of dollars in upfront investment, often with extended payback periods due to long operational lifespans. Advanced reactor designs and fuel recycling initiatives, while technologically promising, demand additional R&D expenditures and specialised infrastructure.

Expansion in Advanced Reactors and Fuel Recycling

The nuclear fuel market is experiencing significant expansion driven by the development of advanced reactors and fuel recycling technologies. Advanced reactors, including small modular reactors (SMRs) and Generation IV designs, offer enhanced safety, higher efficiency, and greater fuel flexibility compared to traditional light-water reactors. These reactors can utilise alternative fuels such as high-assay low-enriched uranium (HALEU) and thorium, enabling more sustainable and long-term energy solutions. Governments and private players worldwide are investing heavily in these technologies to meet rising electricity demand, reduce carbon emissions, and strengthen energy security.

Fuel recycling, particularly through mixed oxide (MOX) programs, is complementing this growth by reprocessing spent fuel to recover usable plutonium and uranium. This reduces nuclear waste, optimizes resource utilization, and supports circular fuel cycles. Europe and Japan are leading these initiatives, while emerging economies are beginning to adopt similar approaches. The combination of advanced reactors and recycling technologies not only extends fuel life but also opens new market opportunities for enrichment, fabrication, and waste management services.

Category-wise Analysis

Product Type Insights

Uranium Fuel dominates the market, accounting for 95% of the share in 2025. Owing to its compatibility with widely used light-water reactors and a stable global supply from leading producers like Kazakhstan, Canada, and Australia. Its proven efficiency, established infrastructure, and cost-effectiveness make uranium the primary choice for large-scale nuclear power generation worldwide.

Mixed Oxide (MOX) Fuel is the fastest-growing segment, driven by recycling initiatives in Europe and Japan aimed at reducing nuclear waste and optimising resource use. By reusing plutonium and uranium from spent fuel, MOX supports sustainability goals, enhances energy security, and aligns with global efforts to establish closed-loop fission fuel cycles.

Application Insights

Nuclear Power Plants lead with over 90% share, supported by the global expansion of reactor fleets exceeding 440 operational units. Rising electricity demand, coupled with the shift toward low-carbon energy, is driving investments in new builds and life-extension projects, reinforcing nuclear power’s role as a cornerstone of sustainable energy generation worldwide.

Nuclear Research Labs are the fastest-growing, driven by intensive R&D efforts focused on developing next-generation fuels such as thorium and high-assay low-enriched uranium (HALEU). These initiatives aim to enhance reactor efficiency, safety, and waste management. Global collaborations and government funding are accelerating advancements in advanced reactor and fuel cycle technologies.

End-use Insights

Energy Power holds an 80% share, driven by its critical role in generating stable baseload electricity. Atomic fuel enables continuous, low-carbon power production, supporting national energy security and decarbonization goals. Governments worldwide are investing in reactor expansions and life extensions, reinforcing nuclear energy’s dominance in the global power sector.

Healthcare is the fastest-growing, driven by the expanding use of radioisotopes in diagnostics and treatment. Isotopes such as Technetium-99m and Iodine-131 are increasingly utilized in imaging, cancer therapy, and cardiovascular diagnostics. Rising demand for precision medicine and advanced diagnostic tools is further accelerating fission fuel applications in healthcare.

Regional Insights

Asia Pacific Nuclear Fuel Market Trends

Asia Pacific commands around a 55% share and is the fastest-growing region, driven by expanding nuclear power infrastructure and rising energy demand. China leads this growth with 22 nuclear reactors currently under construction, supported by strong government policies to reduce carbon emissions and ensure energy security. Its ambitious nuclear expansion aims to achieve over 150 operational reactors by 2035, significantly boosting demand for enriched uranium and advanced fuel cycles.

India is also emerging as a key contributor, propelled by its thorium-based nuclear initiatives and indigenous development of advanced heavy-water reactors. The country’s three-stage nuclear program focuses on leveraging abundant thorium reserves to achieve long-term energy independence and sustainability. Other nations, including South Korea and Japan, are reviving or modernising their nuclear programs to stabilise power supply amid fossil fuel volatility. Favourable regulatory frameworks, strategic investments in uranium mining, and regional cooperation for fuel supply are further enhancing the Asia Pacific’s leadership, making it the core growth hub for the global fission fuel market in the coming decade.

North America Nuclear Fuel Market Trends

North America accounts for 25% in 2025, driven by the United States’ reactor restarts and strategic uranium stockpiling initiatives. The U.S. government’s renewed emphasis on energy independence and carbon reduction has led to the reactivation of dormant reactors and the expansion of enrichment facilities. Trends strongly favour domestic sourcing of uranium and fuel fabrication to reduce reliance on foreign suppliers, particularly in light of global geopolitical tensions. The Department of Energy’s support for high-assay low-enriched uranium (HALEU) production further strengthens the region’s competitive edge in advanced reactor fuels.

While geographically part of Europe, the U.K. market reflects similar trends through projects like Hinkley Point C, which is expected to significantly enhance domestic nuclear capacity upon completion. The U.K. is also advancing MOX fuel recycling and exploring small modular reactor (SMR) technologies to improve efficiency and sustainability.

Europe Nuclear Fuel Market Trends

Europe holds about 20% market share, led by France and Russia playing pivotal roles due to their advanced fuel technologies and strong regulatory frameworks. France leads the region with its mixed oxide (MOX) fuel programs, which recycle plutonium and uranium from spent fuel, enhancing sustainability and reducing nuclear waste. Operated primarily by Orano and EDF, these initiatives support the European Union’s goals of achieving low-carbon energy while maintaining a secure and diversified fuel supply.

Russia, through Rosatom, remains a key supplier of enriched uranium and atomic fuel assemblies to several European countries, reinforcing its strategic influence in the region. However, the EU’s energy security directives are encouraging diversification away from Russian fuel dependencies, prompting investments in domestic enrichment capacities and collaborative research under Euratom. The United Kingdom, Finland, and the Czech Republic are also expanding or upgrading their nuclear capabilities to meet rising electricity demands.

Competitive Landscape

The global nuclear fuel market is highly competitive, characterised by a limited number of key players that dominate the entire value chain from uranium mining and conversion to enrichment and fuel fabrication. These companies, such as Orano (France), Cameco Corporation (Canada), Rosatom (Russia), and Kazatomprom (Kazakhstan), hold strategic control over global uranium reserves and advanced enrichment technologies. This vertical integration allows them to influence pricing, supply stability, and long-term fuel contracts with utilities worldwide.

Competition intensifies due to geopolitical factors, as atomic fuel supply is closely linked to national energy security. Western nations are increasingly diversifying supply chains to reduce dependence on Russian enrichment services, while emerging economies are investing in domestic capabilities. Technological advancements in fuel reprocessing and small modular reactors (SMRs) are reshaping market dynamics, prompting companies to expand R&D and strategic partnerships.

Key Industry Developments

- In September 2025, Orano has entered a strategic partnership with Zeno Power to provide americium-241 (Am-241), a long-lived isotope from its used nuclear fuel recycling operations. Am-241 is ideal for space power applications due to its extended half-life, enabling systems to operate for decades without maintenance

- In August 2025, the national atomic company of Kazakhstan announced plans for a roughly 10% cut in its uranium production in 2026, saying it does not view the current supply-demand balance and existing uncovered demand as sufficient to incentivise a return to its 100% levels at this time.

Companies Covered in Nuclear Fuel Market

- Cameco Corporation

- Kazatomprom

- Orano

- China National Nuclear Corporation (CNNC)

- Rosatom

- Energy Resources of Australia (ERA)

- BHP Group (Australia/Global)

- Uranium One

- Navoi Mining & Metallurgy Combinat (NMMC)

- NAC Kazatomprom Marketing AG

Frequently Asked Questions

The global nuclear fuel market is projected to reach US$34.5 Billion in 2025, driven by low-carbon energy transition and reactor expansions worldwide.

Rising electricity consumption, climate change mitigation targets, and geopolitical considerations are prompting governments and utilities to invest in nuclear power, advanced reactors, and fuel recycling, ensuring a stable, sustainable, and secure energy supply.

The market is poised to witness a CAGR of 3.5% from 2025 to 2032, supported by SMR advancements and fuel recycling.

Advancements in MOX recycling and HALEU for advanced reactors offer opportunities for waste reduction and efficiency.

Key players include Cameco Corporation, Kazatomprom, Orano, Rosatom, and CNNC, leading through mining and enrichment dominance.