- Renewable Energy

- Biodiesel Fuel Market

Biodiesel Fuel Market Size, Share, and Growth Forecast 2026 - 2033

Biodiesel Fuel Market by Feedstock Type (Vegetable Oil (Soybean Oil, Corn Oil, Canola Oil, Palm Oil, Jatropha Curcas, Others), Animal Oil (White Grease, Tallow, Poultry Fat, Yellow Grease), UCO), Application (Fuel (Automobile, Industrial, Marine), Power Generation, Agriculture), Production Process (Alcohol Trans-Esterification, Hydro-Heating), and Regional Analysis, 2026 - 2033

Biodiesel Fuel Market Size and Trend Analysis

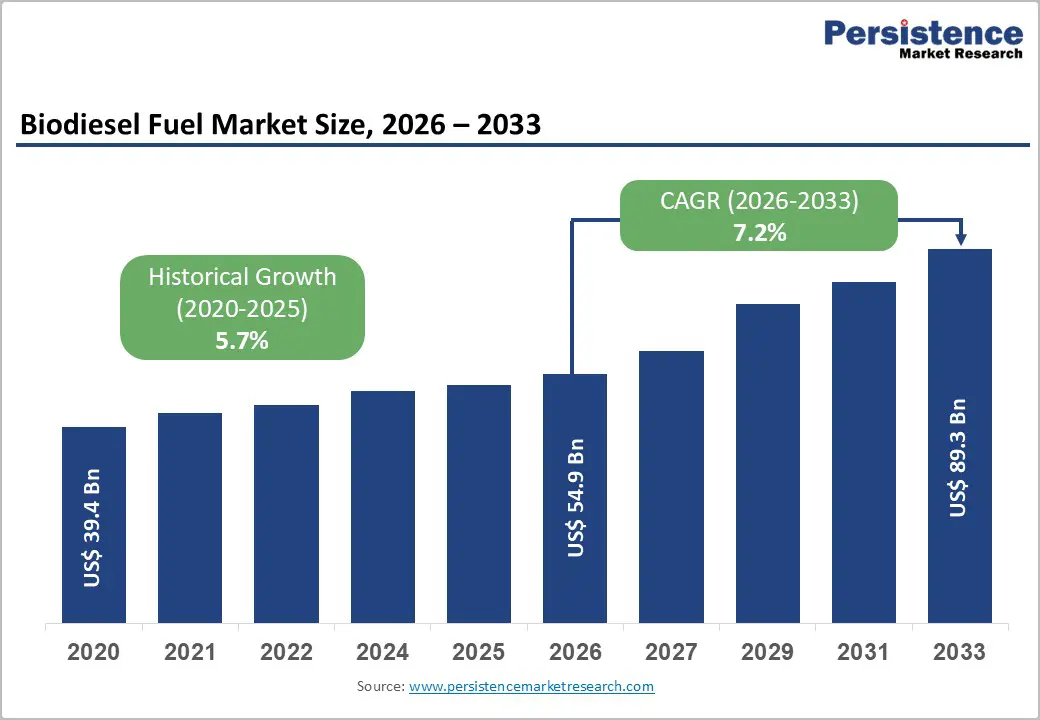

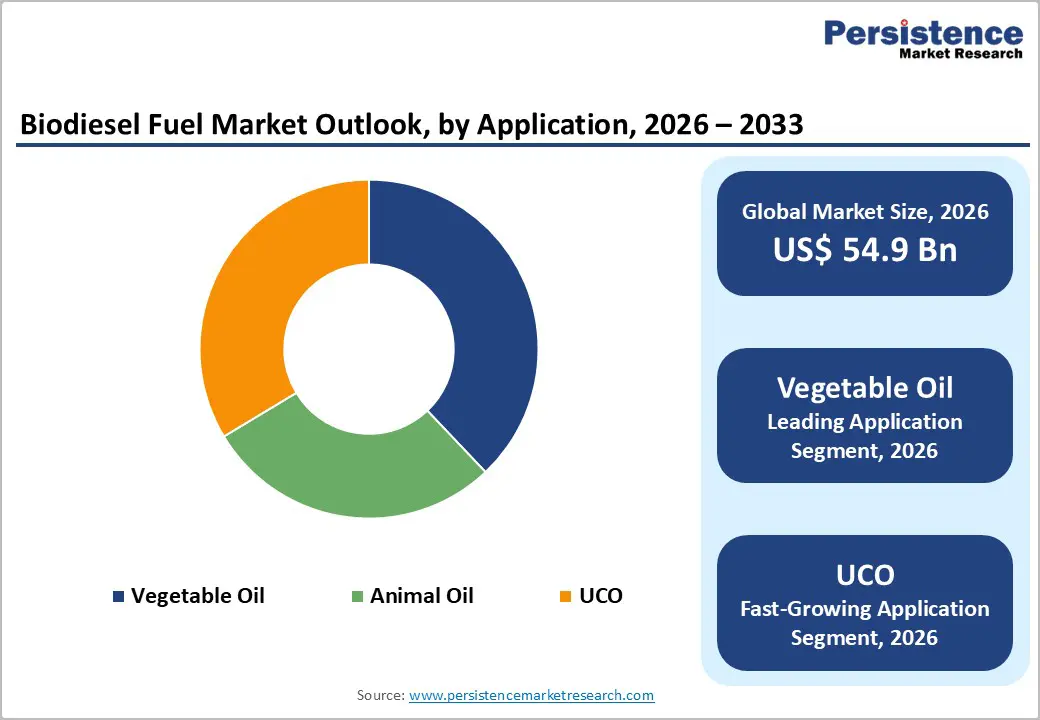

The global biodiesel fuel market size is expected to be valued at US$ 54.9 billion in 2026 and projected to reach US$ 89.3 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

Growth is primarily driven by stringent environmental regulations, renewable fuel mandates, and accelerating decarbonization targets worldwide. Programs such as the U.S. Renewable Fuel Standard, which supports 5.61 billion gallons of biomass-based diesel for 2026, reflect strong policy support. Expanding feedstock availability, including soybean oil and waste cooking oil, alongside advances in production efficiency, is strengthening supply capacity to meet rising demand in the transportation and power sectors.

Key Industry Highlights:

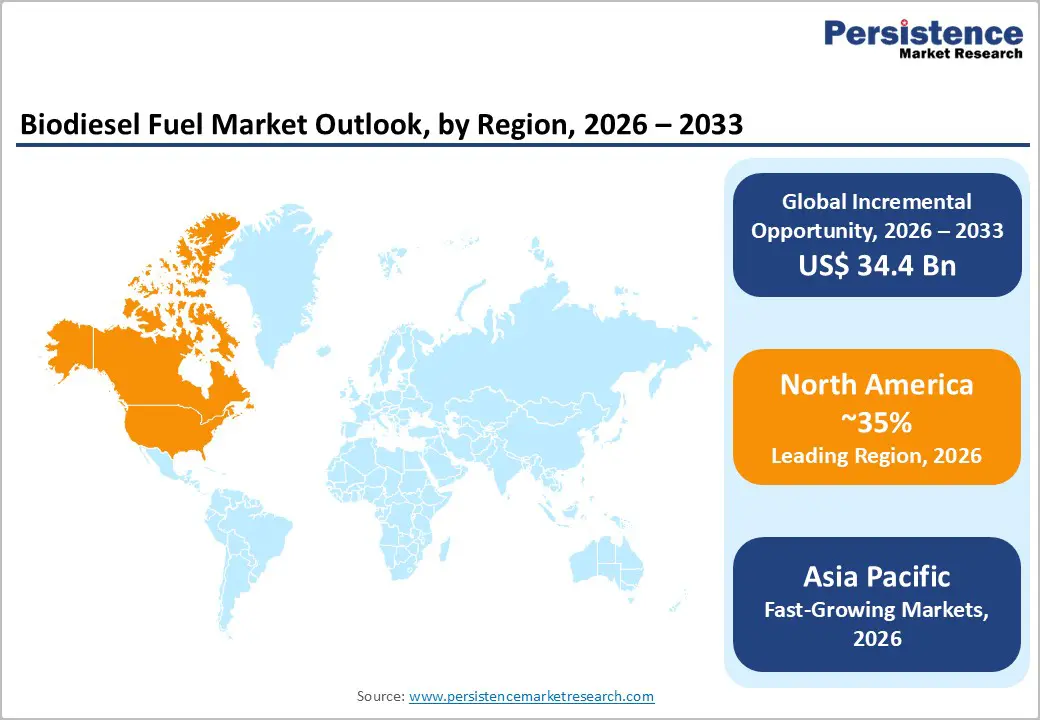

- Leading Region: North America dominates with 35% share (2025), supported by Renewable Fuel Standard mandates and strong soybean-based feedstock integration.

- Fastest-Growing Region: Asia Pacific holds 30% share (2025) and is expanding rapidly at 9% CAGR, driven by Indonesia’s palm-based blending mandates and rising regional fuel demand.

- Leading Feedstock Category: Vegetable oil leads with 60% share (2025), primarily supported by abundant soybean and palm oil supply chains.

- Leading Production Process: Alcohol transesterification accounts for 80% of the market (2025) due to its high conversion efficiency and scalability.

- Key Opportunity: Hydrotreated Vegetable Oil (HVO) presents strong growth potential in the marine and power sectors, offering up to 92% lifecycle emission reductions.

| Key Insights | Details |

|---|---|

|

Biodiesel Fuel Size (2026E) |

US$ 54.9 billion |

|

Market Value Forecast (2033F) |

US$ 89.3 billion |

|

Projected Growth CAGR(2026-2033) |

7.2% |

|

Historical Market Growth (2020-2025) |

5.7% |

Market Dynamics

Drivers - Stringent Global Emission Regulations and Renewable Mandates Accelerating Biodiesel Adoption

Governments worldwide are tightening emission norms and enforcing renewable fuel blending mandates, significantly driving biodiesel adoption as a lower-carbon substitute for fossil diesel. In the United States, the Environmental Protection Agency’s Renewable Fuel Standard (RFS) has proposed 5.61 billion gallons of biomass-based diesel for 2026, reflecting a policy commitment to reduce lifecycle greenhouse gas emissions by more than 50% relative to petroleum diesel.

Similarly, Europe’s Renewable Energy Directive (RED II) promotes advanced biofuels and higher renewable energy shares in transport. Biodiesel consumption has rebounded strongly, supported by blending mandates such as B20 and B30 across fleets. These policies not only reduce particulate and sulfur emissions but also enhance engine lubricity, thereby supporting broader adoption across commercial transportation and industrial applications.

Growing Agricultural Feedstock Availability Strengthening Biodiesel Supply Chains

Expanding agricultural output and improved oilseed processing capacities are reinforcing biodiesel production globally. Soybean oil remains a dominant feedstock, accounting for a significant portion of U.S. biodiesel production, supported by rising domestic crush capacity and integrated value chains. This growth stimulates rural economic activity while ensuring a stable feedstock supply for renewable fuel manufacturers.

Globally, palm oil in Indonesia and rapeseed oil in Europe contribute to the production of biodiesel on a large scale. Increasing utilization of used cooking oil (UCO) further enhances sustainability by recycling waste streams into fuel. With an energy return ratio of approximately 3.5:1, biodiesel production offers improved energy efficiency and reduced exposure to fossil fuel price volatility, supporting consistent long-term market expansion.

Restraints - Volatility in Feedstock Prices and Food-Versus-Fuel Competition Limiting Profit Margins

Fluctuating prices of vegetable oils and animal fats remain a significant restraint for biodiesel producers, particularly due to competition with food, feed, and industrial applications. Soybean oil prices have experienced periodic spikes driven by export demand and supply imbalances, which increase biodiesel production costs by 20–30% during volatile periods, according to USDA assessments.

Similarly, diversion of palm oil toward food markets in Asia and other regions places additional pressure on feedstock availability and pricing. This ongoing “food versus fuel” debate creates uncertainty for investors and producers, discouraging large-scale capacity expansions in cost-sensitive markets and constraining long-term scalability despite supportive blending mandates.

Logistical Complexities in Waste Oil Collection Restricting Supply Reliability

Although used cooking oil (UCO) and yellow grease present sustainable alternatives to virgin oils, their collection and aggregation involve complex, fragmented supply chains. Inconsistent sourcing from restaurants, food processors, and small vendors makes maintaining reliable volumes challenging, particularly in regions lacking organized waste management systems.

While Europe processes millions of tons of waste oils annually, traceability concerns and fraud risks inflate operational costs by an estimated 10–15%. In developing economies, inadequate infrastructure and limited monitoring mechanisms further delay scaling efforts. These logistical hurdles constrain feedstock diversification and limit the full potential of global waste-based biodiesel expansion.

Opportunity - Technological Advancements in UCO Processing and HVO Production Expanding Growth Potential

Advancements in the processing of used cooking oil (UCO) and in hydrotreated vegetable oil (HVO) technologies are creating significant opportunities in the biodiesel landscape. UCO-based biodiesel is gaining traction due to its cost advantages and strong greenhouse gas reduction profile. Improved collection systems and refining technologies are enabling higher-quality outputs, enhancing scalability across global markets.

HVO technology, capable of delivering 82–92% lifecycle emission reductions, is particularly suited for hard-to-abate sectors such as marine and aviation. Regulatory approvals for higher blending ratios, combined with sustainable aviation fuel mandates in Europe and supportive EPA policies, are unlocking incremental demand. Companies investing in feedstock aggregation and advanced refining capacity stand to benefit, particularly in waste-rich Asia-Pacific markets.

Policy-Driven Expansion in Marine and Decentralized Power Generation Applications

Decarbonization targets in the marine sector under the International Maritime Organization (IMO) frameworks are opening new avenues for biodiesel adoption. Fleet trials using biodiesel blends have demonstrated carbon dioxide reductions of up to 70%, positioning biodiesel as a viable transitional fuel for shipping operators seeking compliance without major engine retrofits.

In parallel, biodiesel-powered generators are gaining adoption in remote and off-grid power applications, where B100 offers a cleaner alternative to conventional diesel. Incentives under frameworks such as the U.S. Renewable Fuel Standard and the EU Renewable Energy Directive support diversification into industrial, marine, and distributed power segments, strengthening long-term growth prospects beyond traditional road transportation.

Category-wise Analysis

Feedstock Type Insights

Vegetable oil remains the dominant feedstock segment in 2025, accounting for approximately 60% of global biodiesel production. Soybean oil leads in the United States, supported by well-established crushing infrastructure and strong domestic supply chains, contributing the majority of national feedstock usage. In Asia, palm oil plays a central role, particularly in Indonesia, where blending mandates such as B30 reinforce large-scale utilization across transport fuels.

Used cooking oil (UCO) is emerging as the fastest-growing feedstock category owing to its sustainability advantages and waste-recycling initiatives. Governments are promoting circular economy frameworks that encourage the collection and reuse of waste oils. Technological advances in purification and traceability systems further strengthen confidence in waste-based biodiesel, thereby supporting diversification beyond traditional vegetable oil sources.

Application Insights

The automotive fuel segment accounts for nearly 57.2% of total biodiesel consumption in 2025. Adoption is particularly strong in North America and Europe, where logistics fleets and public transportation systems utilize B20 and higher blends to meet emission compliance requirements. Regulatory frameworks such as renewable fuel mandates continue to drive highway diesel substitution and large-scale fleet integration.

Power generation is emerging as the fastest-growing application area, particularly in remote and off-grid regions. Biodiesel-powered generators are increasingly used to reduce dependence on conventional diesel and to lower emissions. The marine and industrial sectors are also exploring biodiesel blends to meet decarbonization targets, thereby broadening the scope of applications beyond road transportation.

Production Process Insights

Alcohol transesterification remains the leading production process in 2025, accounting for around 80% of global biodiesel output. The method is widely adopted for its high conversion efficiency and compatibility with diverse feedstocks, including soybean oil and used cooking oil. Its cost-effectiveness and established industrial scalability make it the preferred choice across major producing regions.

Hydrotreatment processes, commonly associated with hydrotreated vegetable oil (HVO), represent the fastest-growing technological segment. These processes enhance cold-flow properties and fuel stability, making them suitable for colder climates and advanced applications. Growing investment in next-generation bio-refining technologies is expected to enhance product performance and expand global production capacity.

Regional Insights

North America Biodiesel Fuel Market Trends

North America leads the global biodiesel fuel market with approximately 35% share in 2025, driven primarily by strong policy support in the United States. The Renewable Fuel Standard (RFS) continues to anchor demand, with proposed biomass-based diesel volumes projected to reach 5.61 billion gallons in 2026. State-level blending mandates and Low Carbon Fuel Standards further reinforce adoption across transportation fleets.

Soybean oil remains the dominant feedstock, accounting for the majority of U.S. biodiesel production and supporting extensive agricultural and crushing infrastructure. Industry innovation is accelerating, particularly in hydrotreated vegetable oil (HVO) and sustainable aviation fuel pathways. Backed by federal incentives and farmer-led investments, North America maintains technological leadership and stable domestic production capacity.

Europe Biodiesel Fuel Market Trends

Europe represents a mature and policy-driven biodiesel market, supported by harmonized regulations under the Renewable Energy Directive (RED II). Major producers such as Germany, France, and Spain collectively account for a substantial portion of regional output. Biodiesel consumption has rebounded strongly, supported by blending mandates and expanding targets for advanced biofuels.

The region is projected to grow at a steady CAGR through 2032, driven by increasing adoption of used cooking oil (UCO) and hydrotreated vegetable oil (HVO). Sustainable aviation fuel mandates and cross-border trade alignment are strengthening demand for sustainable aviation fuel. However, regulatory scrutiny around feedstock traceability and fraud prevention remains critical to ensuring long-term supply chain integrity.

Asia Pacific Biodiesel Fuel Market Trends

Asia-Pacific accounts for approximately 30% of the global biodiesel market in 2025 and is emerging as one of the fastest-growing regions. Indonesia plays a pivotal role through its palm oil-based B30 blending mandate, which supports large-scale domestic consumption. Expanding urbanization and industrial growth across Southeast Asia further reinforce regional fuel demand.

Countries such as India and China are actively strengthening their biofuel strategies to reduce dependence on crude oil. India is advancing the cultivation of non-edible oilseeds under national biofuel policies, while China’s imports and processing capacity continue to expand. Growing utilization of used cooking oil and supportive government frameworks are positioning the Asia Pacific as a dynamic growth hub for biodiesel production and consumption.

Competitive Landscape

The biodiesel fuel market is moderately consolidated, characterized by vertically integrated producers with strong control over feedstock sourcing, refining, and distribution networks. Leading participants focus on expanding renewable diesel and advanced biofuel capacities while strengthening supply chain integration to mitigate feedstock volatility. Strategic investments in refining efficiency, process optimization, and certification standards enhance competitive positioning in regulated markets.

Innovation remains central to competition, with growing emphasis on hydrotreated technologies, waste-based feedstocks, and circular economy models. Partnerships across sustainable aviation fuel, marine fuels, and low-carbon mobility ecosystems are expanding revenue streams. Companies are differentiating through technological advancements, traceability systems, and compliance-driven solutions aligned with global decarbonization policies.

Key Developments:

- In June 2025, the U.S. Environmental Protection Agency proposed a Renewable Fuel Standard volume of 5.61 billion gallons for biomass-based diesel in 2026, aligning federal targets with the expansion of domestic production capacity and reinforcing long-term policy support for advanced biofuels and decarbonization goals.

- In January 2026, Clean Fuels Alliance America reported that U.S. biodiesel and renewable diesel consumption reached 5 billion gallons in 2025, marking a record year for industry demand and reflecting strong uptake across transportation fleets supported by federal and state-level blending mandates.

- In July 2025, the European Biodiesel Board released updated statistics indicating that EU biodiesel production rebounded to 16.75 billion liters, driven by Renewable Energy Directive targets, improved trade flows, and strengthening adoption of advanced and waste-based biofuel feedstocks.

Companies Covered in Biodiesel Fuel Market

- Cargill Inc.

- Renewable Energy Group, Inc. (Chevron)

- VERBIO SE

- MOL Group

- Archer Daniels Midland Company

- Ag Processing Inc.

- Emami Group

- HERO BX

- Meroco, a.s.

- Rossi Biofuel Plc.

- ARGENT ENERGY

- Marathon Biodiesel

Frequently Asked Questions

The global Biodiesel Fuel market is projected to reach US$ 54.9 billion in 2026, driven by expanding renewable fuel mandates and transportation sector adoption.

Stringent regulations like RFS and RED II drive demand, mandating billions of gallons for emission reductions.

North America leads with 35% share in 2025, supported by strong U.S. policy mandates and soybean-based feedstock dominance.

Growth in UCO-based feedstocks and HVO technologies presents strong opportunity, alongside Asia Pacific’s expansion, which holds 30% share (2025).

Leading players include Cargill Inc., Renewable Energy Group, Inc. (Chevron), VERBIO SE, MOL Group, and Archer Daniels Midland Company, focusing on expansions and innovations.