- Energy Storage Solutions

- Proton Exchange Membrane Fuel Cell Market

Proton Exchange Membrane Fuel Cell Market Size, Share, and Growth Forecast 2026 - 2033

Proton Exchange Membrane Fuel Cell Market by Product Type (High Temperature, Low Temperature), by Material (Membrane Electrode Assembly, Hardware, Others), by Application (Automotive, Portable, Stationary, Others), and Regional Analysis for 2026 - 2033

Proton Exchange Membrane Fuel Cell Market Size and Trend Analysis

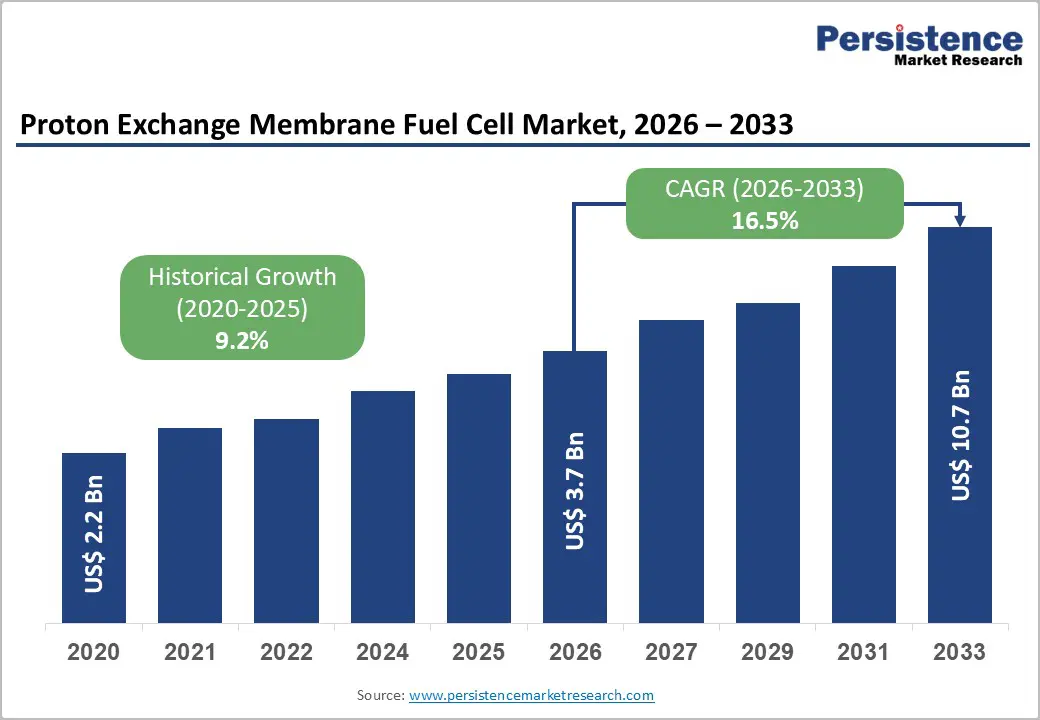

The global Proton Exchange Membrane Fuel Cell market size is supposed to be valued at US$ 3.7 Billion in 2026 and is projected to reach US$ 10.8 Billion by 2033, growing at a CAGR of 16.5% between 2026 and 2033.

The market's exceptional double-digit growth trajectory is driven by the global energy transition's accelerating shift toward zero-emission power solutions, government hydrogen economy investment programs, and the rapid commercial deployment of fuel cell electric vehicles (FCEVs) and stationary power applications across North America, Europe, and the Asia Pacific.

Key Industry Highlights:

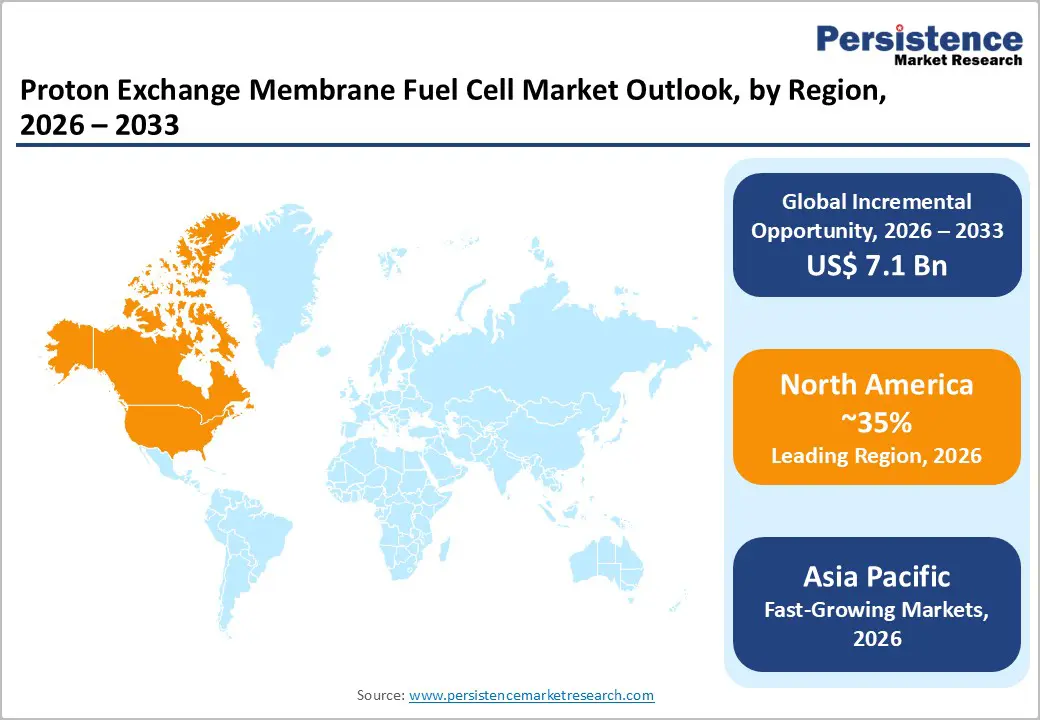

- Leading Region: North America leads the global Proton Exchange Membrane Fuel Cell market, anchored by the U.S. DOE's US$ 9.5 billion hydrogen program under the Bipartisan Infrastructure Law, the IRA's US$ 3/kg clean hydrogen tax credit, and Plug Power's globally largest installed PEMFC base exceeding 69,000 units across materials handling and stationary power applications.

- Fastest-growing region: Asia Pacific is the fastest-growing region, driven by Japan's 500,000+ residential Ene-Farm PEMFC installations, South Korea's target of 6.2 million FCEVs by 2040 under its Hydrogen Economy Roadmap, and China's MIIT-backed national fuel cell vehicle program targeting 50,000 FCEVs in commercial deployment with substantial central government subsidies.

- Leading region: Low Temperature PEMFC systems dominate the Product Type segment with approximately 73% revenue share in 2026, anchored by commercial deployment across Toyota Mirai, Hyundai NEXO, and Ballard Power Systems' transit bus and truck modules, reflecting decades of technology maturation and the established automotive OEM supply chain built around Nafion membrane and platinum catalyst systems.

- Fastest-growing segment: Stationary application is the fastest-growing segment, fueled by hyperscale data center backup power adoption validated by Microsoft's successful 3 MW PEMFC data center pilot in 2023and residential energy programs like Panasonic's Ene-Farm, with the IDC's forecast of over US$ 1 trillion in cumulative data center investment through 2027, sustaining accelerating procurement demand.

- Opportunity: Green hydrogen integration and electrolyze-PEMFC vertical ecosystem development represent the key market opportunity, with the EU's IPCEI Hy2Tech program committing €5.4 billion and the IEA documenting global PEM electrolyze shipments exceeding 1 GW in 2023creating technology transfer, cost reduction, vertically integrated business model opportunities for manufacturers commanding both electrolyze and fuel cell competencies.

| Key Insights | Details |

|---|---|

|

Proton Exchange Membrane Fuel Cell Market Size (2026A) |

US$ 3.7 Bn |

|

Projected Year Value (2033F) |

US$ 10.8 Bn |

|

Value CAGR (2026-2033) |

16.5% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

9.2% |

Market Dynamics

Drivers - Global Hydrogen Economy Policy Frameworks and Clean Energy Investment Programs Accelerating PEMFC Adoption

The establishment of comprehensive national hydrogen economy strategies and clean energy investment frameworks across major economies is the most powerful structural driver propelling the global Proton Exchange Membrane Fuel Cell market toward accelerated growth. The European Union's Repower EU Plan targets production of 10 million tons of domestic renewable hydrogen and import of a further 10 million tons by 2030with PEMFC systems identified as the primary electrochemical conversion technology for hydrogen utilization in transportation and stationary applications. The U.S. Department of Energy (DOE)'s Hydrogen Shot initiative targets reducing the cost of clean hydrogen to US$ 1 per 1 kilogram in 1 decade ("1-1-1"), catalyzing commercial PEMFC system deployment by dramatically improving the fuel cost economics of hydrogen-powered vehicles and industrial backup power systems.

Rapid Commercialization of Hydrogen Fuel Cell Vehicles Expanding the Automotive PEMFC Demand Base

The global automotive sector's accelerating commercial deployment of Fuel Cell Electric Vehicles (FCEVs)including passenger cars, commercial trucks, buses, and forklifts is creating the largest and most rapidly growing single demand category for PEMFC systems, anchored by the compelling zero-emission and rapid-refueling advantages of hydrogen over battery-electric alternatives in heavy and long-range transport applications. Toyota Motor Corporation has been producing its Mirai FCEV since 2014, with second-generation models deployed globally, while Hyundai Motor Company's NEXO SUV and XCIENT Fuel Cell heavy trucks have established commercial traction in Europe, South Korea, and the United States. The International Council on Clean Transportation (ICCT) has documented that heavy-duty fuel cell trucks achieve total cost of ownership parity with diesel alternatives in high-utilization fleet operations conclusion that is driving acceleration FCEV procurement commitments from major logistics operators including Amazon, DHL, and UPS.

Restraints - High Manufacturing Cost of Platinum Group Metal Catalysts Constraining PEMFC System Affordability

The dominant use of platinum group metals (PGMs) specifically platinum and platinum-palladium alloysas electrocatalysts in PEMFC membrane electrode assemblies remains the most significant cost barrier preventing broader commercial adoption across price-sensitive application segments. The World Platinum Investment Council (WPIC) reported that platinum prices averaged approximately US$ 950–1,050 per troy ounce in 2024, and each PEMFC passenger vehicle stack requires approximately 30–50 grams of platinum loading representing a material cost component that is difficult to fully offset through system integration efficiency gains. Despite meaningful catalyst loading reductions achieved through nanotechnology-based dispersion techniques and platinum alloy formulations, PGM dependency continues to create cost-competitiveness challenges for PEMFC systems compared to solid oxide fuel cells for stationary applications and lithium-ion batteries for short-range electric mobility, limiting the addressable market penetration in cost-sensitive fleet procurement decisions.

Hydrogen Refueling Infrastructure Deficit Limiting FCEV Market Expansion in Key Regions

The global deployment of Proton Exchange Membrane Fuel Cell vehicles remains constrained by the critically underdeveloped hydrogen refueling infrastructure in most markets outside Japan, South Korea, and California. The U.S. Department of Energy (DOE) reported that as of 2024, fewer than 60 public hydrogen refueling stations were operational in the entire United States concentrated almost exclusively in California compared to over 150,000 conventional gasoline stations. This infrastructure deficit creates a fundamental "chicken-and-egg" adoption barrier: consumers are reluctant to purchase FCEVs without assured refueling access, while infrastructure investors require demonstrated vehicle deployment commitments before committing capital. The European Hydrogen Backbone initiative is planning a 53,000 km hydrogen pipeline network by 2040, but near-term infrastructure gaps continue to moderate FCEV adoption rates and dampen automotive PEMFC procurement growth in infrastructure-deficient markets.

Opportunity - Stationary Backup Power and Data Center Applications Emerging as High-Growth PEMFC Deployment Frontier

The global expansion of critical infrastructure requiring clean, reliable, and extended-duration backup power encompassing data centers, telecommunications base stations, hospitals, and military facilities is creating a structurally large and rapidly growing commercial opportunity for stationary PEMFC systems that deliver significant advantages over conventional diesel generator backup solutions. The International Data Corporation (IDC) forecasts that global data center infrastructure investment will exceed US$ 1 trillion cumulatively through 2027, with hyperscale operators including Microsoft, Google, and Amazon Web Services publicly committing to eliminate diesel backup generators from their facilities under corporate sustainability mandates. Microsoft announced in 2023 that it had successfully tested a 3-megawatt PEMFC backup power system capable of powering a data center row for 48 hours on hydrogen representing a landmark commercial validation of PEMFC technology in the critical infrastructure backup market.

Green Hydrogen Integration and Electrolyzed-PEMFC Ecosystem Creating Vertically Integrated Value Chain Opportunities

The convergence of Proton Exchange Membrane (PEM) electrolysis used for green hydrogen production with PEMFC power generation technology creates a unique vertically integrated value chain opportunity for manufacturers with competencies across both electrolyzer and fuel cell product families, enabling them to offer complete hydrogen energy ecosystem solutions from generation to utilization. ITM Power PLC a leading PEM electrolyze manufacturer headquartered in Sheffield, UK exemplifies this strategic positioning, offering industrial-scale green hydrogen production systems that generate the fuel consumed by downstream PEMFC power systems, thereby addressing both the supply and demand sides of the hydrogen economy simultaneously.

Category-wise Insights

By Product Type

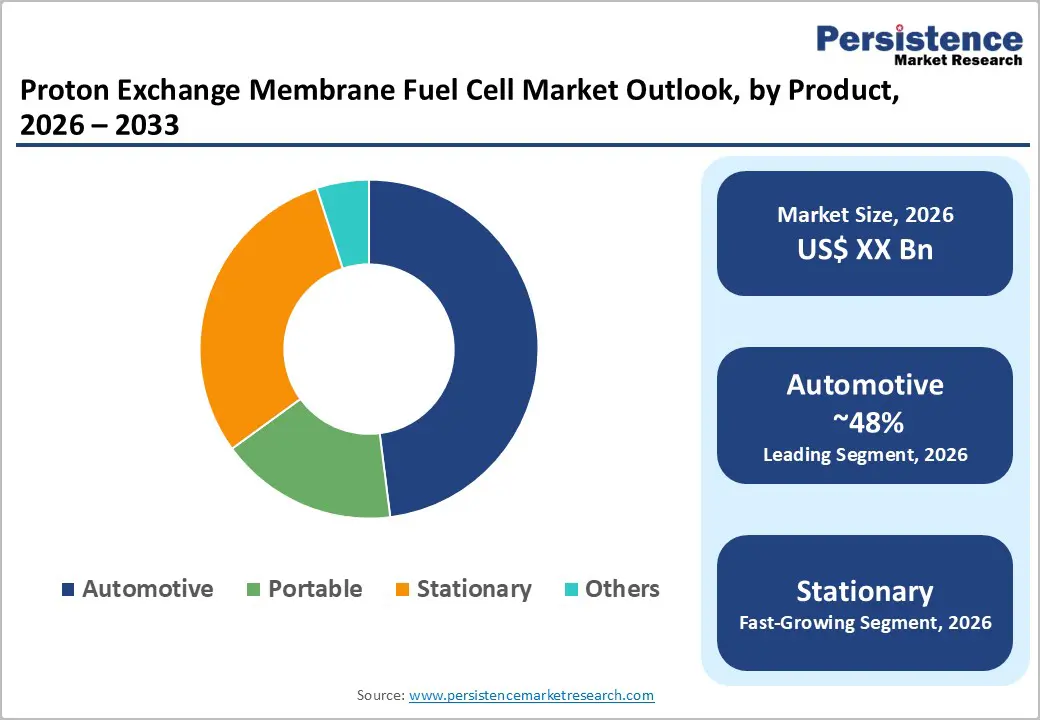

Low Temperature PEMFC systems dominate the global Proton Exchange Membrane Fuel Cell market by product type, accounting for approximately 73% of total product type segment revenue in 2026. Low temperature PEMFCs operating at 60–80°Crepresent the commercially dominant and most widely deployed PEMFC technology across automotive, portable, and light-duty stationary applications, benefiting from decades of product maturation, established supply chain infrastructure for Nafion-based membranes and platinum catalyst systems, and strong OEM adoption in commercial FCEV platforms. Toyota's Mirai and Hyundai's NEXO both utilize low temperature PEMFC stacks as their core propulsion technology, and Ballard Power Systems' commercially deployed transit bus and truck fuel cell modules operate within the low temperature range confirming this segment's dominant real-world application footprint.

By Material

The Membrane Electrode Assembly (MEA) segment leads the global Proton Exchange Membrane Fuel Cell market by material, commanding approximately 54% of total material segment revenue in 2026. The MEA comprising the proton-conducting polymer membrane, platinum-based catalyst layers, and gas diffusion layers is the electrochemical heart of every PEMFC system, representing the highest value-added, most technically differentiated, and most IP-protected component in the entire PEMFC bill of materials. MEA cost reduction is the primary focus of global PEMFC R&D programs, with the U.S. DOE's Fuel Cell Technologies Office targeting a PEMFC stack cost of US$ 80 per kilowatt for automotive applications by 2025down from over US$ 200 per kilowatt a decade earlier primarily through MEA catalyst loading reduction, ionomer optimization, and advanced manufacturing process development.

By Application

The Automotive application segment leads the global Proton Exchange Membrane Fuel Cell market, representing approximately 48% of total application segment revenue in 2026. Automotive applications encompassing passenger FCEVs, heavy-duty trucks, commercial buses, and industrial forklifts command the largest PEMFC revenue share due to their high per-system PEMFC stack power density requirements (80–150 kW per vehicle), large and growing commercial deployment volumes, and the premium value placed on PEMFC's rapid refueling and long driving range characteristics relative to battery-electric alternatives in demanding transport duty cycles. The California Air Resources Board (CARB) reports that cumulative FCEV registrations in California exceeded 15,000 vehicles by 2024, demonstrating the established consumer market foundation for automotive PEMFC deployment.

Regional Insights

North America Proton Exchange Membrane Fuel Cell Market Trends

North America leads the global Proton Exchange Membrane Fuel Cell market, anchored by the United States' world-leading position in PEMFC technology innovation, the deepest government funding commitment to hydrogen infrastructure development, and the most advanced regulatory framework mandating zero-emission transportation. The U.S. DOE's Hydrogen Shot initiative, US$ 9.5 billion Bipartisan Infrastructure Law hydrogen program, and US$ 3 per kilogram clean hydrogen production tax credit under the Inflation Reduction Act (IRA) collectively constitute the world's most comprehensive and commercially impactful hydrogen economy policy package directly stimulating PEMFC system deployment across automotive, stationary, and portable applications.

California's CARB zero-emission vehicle mandates and the state's US$ 2.9 billion investment in hydrogen infrastructure are creating the nation's most commercially advanced FCEV deployment ecosystem, with fuel cell heavy-duty truck pilots conducted by Kenworth, Toyota, and Hyundai along California freight corridors demonstrating the pathway to large-volume commercial PEMFC procurement in long-haul trucking.

Europe Proton Exchange Membrane Fuel Cell Market Trends

Europe is the world's most policy-driven and rapidly developing regional market for Proton Exchange Membrane Fuel Cell technology, underpinned by the EU's Green Deal, Repower EU, and Hydrogen Strategy which collectively represent the most ambitious and comprehensive hydrogen economy legislative framework of any regional governing body globally. Germany leads European PEMFC adoption, with the country's National Hydrogen Strategy committing €9 billion in public investment toward building a complete hydrogen value chain encompassing production, transportation, and utilization.

The United Kingdom's Hydrogen Strategy and Net Zero Hydrogen Fund committing £240 million to support early-stage hydrogen projects are stimulating PEMFC deployment in bus transport, rail, and stationary power applications. France's Hydrogen National Plan targets 6.5 GW of electrolytic hydrogen production by 2030, creating substantial downstream demand for stationary PEMFC power systems integrated with French renewable energy assets.

Asia Pacific Proton Exchange Membrane Fuel Cell Market Trends

Asia Pacific is the fastest-growing regional market for Proton Exchange Membrane Fuel Cell systems globally, anchored by Japan and South Korea's world-leading positions in PEMFC commercialization, China's ambitious hydrogen economy industrial policy, and rapidly accelerating PEMFC adoption across India and ASEAN. Japan is the world's most advanced PEMFC deployment market with Panasonic Corporation's residential Ene-Farm stationary PEMFC units having recorded over 500,000 cumulative installations in Japanese homes as of 2024demonstrating the unparalleled depth of civilian PEMFC penetration achieved through Japan's long-term hydrogen society policy.

South Korea's Hydrogen Economy Roadmap targets 6.2 million FCEVs and 2,900 hydrogen refueling stations by 2040the most ambitious national FCEV deployment target of any government globally with Hyundai Motor Company supplying PEMFC-powered NEXO passenger vehicles and XCIENT heavy trucks to markets across Europe, North America, and Asia.

Competitive Landscape

The global proton exchange membrane fuel cell market is moderately fragmented, with a select group of technology-pioneering companies Ballard Power Systems, Plug Power Inc., Cummins Inc., Intelligent Energy Limited, and ITM Power PLC leading on technology maturity, installed base scale, and application breadth. Key differentiators include membrane electrode assembly proprietary IP, stack power density, demonstrated durability exceeding 30,000 hours, and government-validated performance credentials. Emerging business model trends include hydrogen-as-a-service offerings where PEMFC operators supply fuel and maintenance under long-term power purchase agreements and PEMFC-electrolyze integrated ecosystem solutions targeting green industrial hydrogen hubs.

Key Developments:

- In December 2025, India launched its first fully indigenous hydrogen fuel cell passenger vessel into commercial service on the Ganga in Varanasi, marking a major milestone in the country’s green maritime push.

- In March 2024, Cummins launched its first e-compressor for fuel cell engine in Wuxi, China. The key characteristics of the e-compressor are low noise, high speed, and high efficiency. It is applicable for 150 - 200 kW fuel cell engines and 240 - 260 kW fuel cell engines under turbine energy recovery.

Companies Covered in Proton Exchange Membrane Fuel Cell Market

- Intelligent Energy Limited

- Plug Power Inc.

- ITM Power PLC

- Ballard Power Systems

- PowerCell Sweden AB

- Cummins Inc.

- Nedstack Fuel Cell Technology BV

- Horizon Fuel Cell Technologies

- SFC Energy AG

- Panasonic Corporation

- Other Market Players

Frequently Asked Questions

The global Proton Exchange Membrane Fuel Cell market is estimated to be valued at US$ 3.7 Billion in 2026 and is projected to reach US$ 10.8 Billion by 2033, registering a forecast CAGR of 16.5% between 2026 and 2033.

The key growth drivers are the global hydrogen economy policy frameworks including the U.S. DOE's Hydrogen Shot initiative, EU REPowerEU Plan's 20 million tons hydrogen target, and Japan's Basic Hydrogen Strategy targeting 3 million FCEVs by 2030 and the rapid commercial deployment of FCEVs in heavy transportation, validated by the ICCT's documented total cost of ownership parity between hydrogen trucks and diesel in high-utilization fleet operations.

Low Temperature PEMFC systems lead the Product Type category with approximately 73% revenue share in 2026, underpinned by their commercial adoption in Toyota Mirai, Hyundai NEXO, and Ballard Power Systems' transit bus modules.

North America leads the global PEMFC market, anchored by the U.S. DOE's US$ 9.5 billion hydrogen investment from the Bipartisan Infrastructure Law, the IRA's clean hydrogen production tax credit, California CARB's zero-emission transport mandates, and Plug Power Inc.'s globally largest PEMFC installed base.

The leading companies include Ballard Power Systems, Plug Power Inc., Cummins Inc., Hyundai Motor Company, Toyota Motor Corporation, and Bosch GmbH (through the Cell centric joint venture with Daimler Truck), among other leading PEMFC technology developers and system integrators globally.