- Oil & Gas

- Bunker Fuel Market

Bunker Fuel Market Size, Share, and Growth Forecast, 2025 - 2032

Bunker Fuel Market By Fuel Type (VLSFO, HSFO, Others), Application (Container, Tanker, Others), Supplier Type, and Regional Analysis for 2025 - 2032

Bunker Fuel Market Size and Trends Analysis

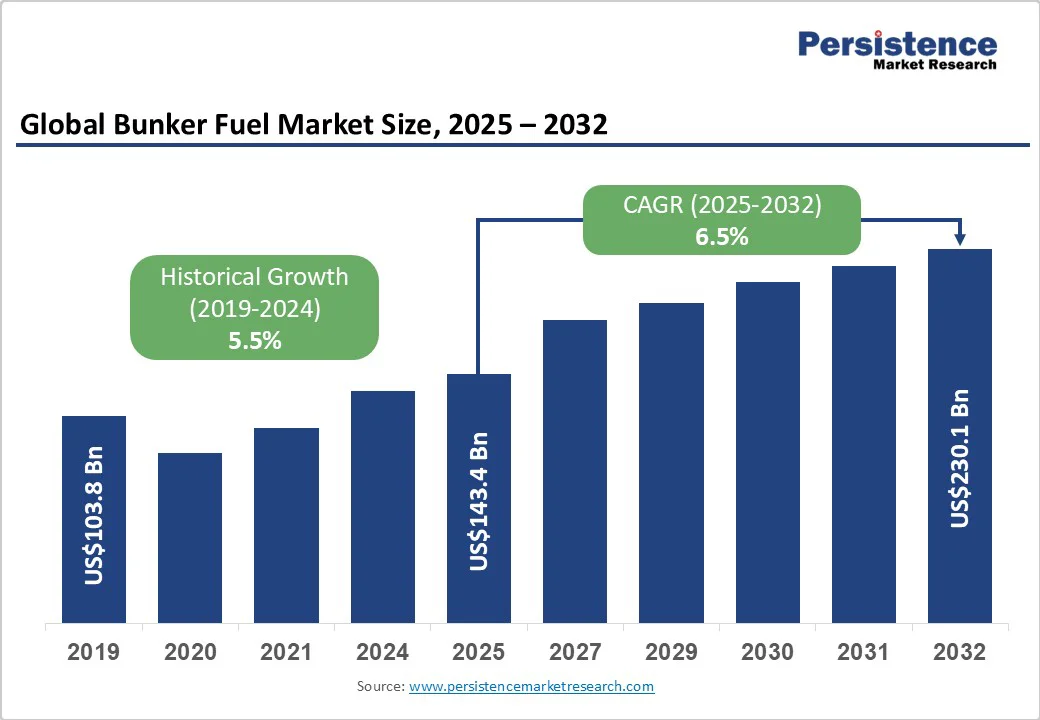

The global bunker fuel market size is likely to be valued at US$143.4 Bn in 2025. It is expected to reach US$230.1 Bn by 2032, growing at a CAGR of 6.5% during the forecast period from 2025 to 2032, driven by post-pandemic recovery in global seaborne trade, regulatory compliance shifts from high-sulfur to very-low-sulfur fuels (VLSFO), and the gradual adoption of alternative fuels such as LNG, methanol, and bio-blends. Regulatory and commercial initiatives are accelerating the replacement of legacy fuels, creating a transitional multi-fuel market.

Key Industry Highlights

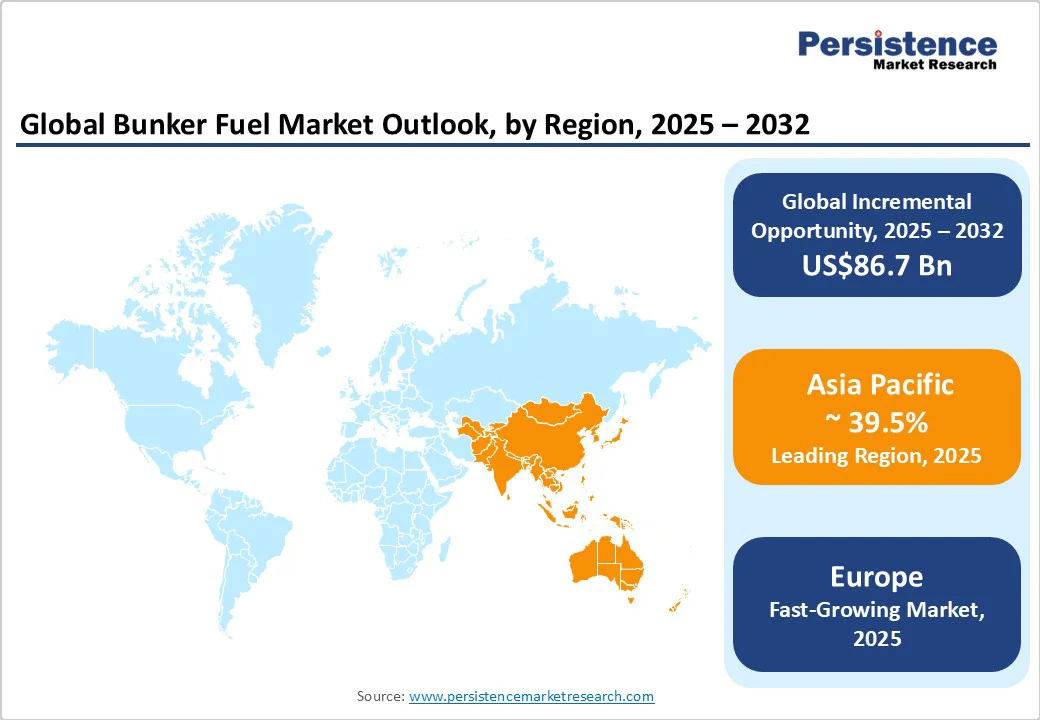

- Leading Region: Asia Pacific, accounting for 39.5% of global bunker revenue in 2024, led by Singapore and major hubs in China, South Korea, and Japan.

- Fastest-growing Region: Europe, projected CAGR 5.6% between 2025 - 2032, driven by LNG adoption, FuelEU Maritime regulations, and biofuel offtake agreements.

- Investment Plans: Significant investments in LNG bunkering infrastructure and alternative fuels across North America (Houston, Los Angeles), Europe (Rotterdam, Hamburg), and Asia Pacific (Singapore, Yokohama, Shanghai), including dual-fuel fleet support and digital fuel management systems.

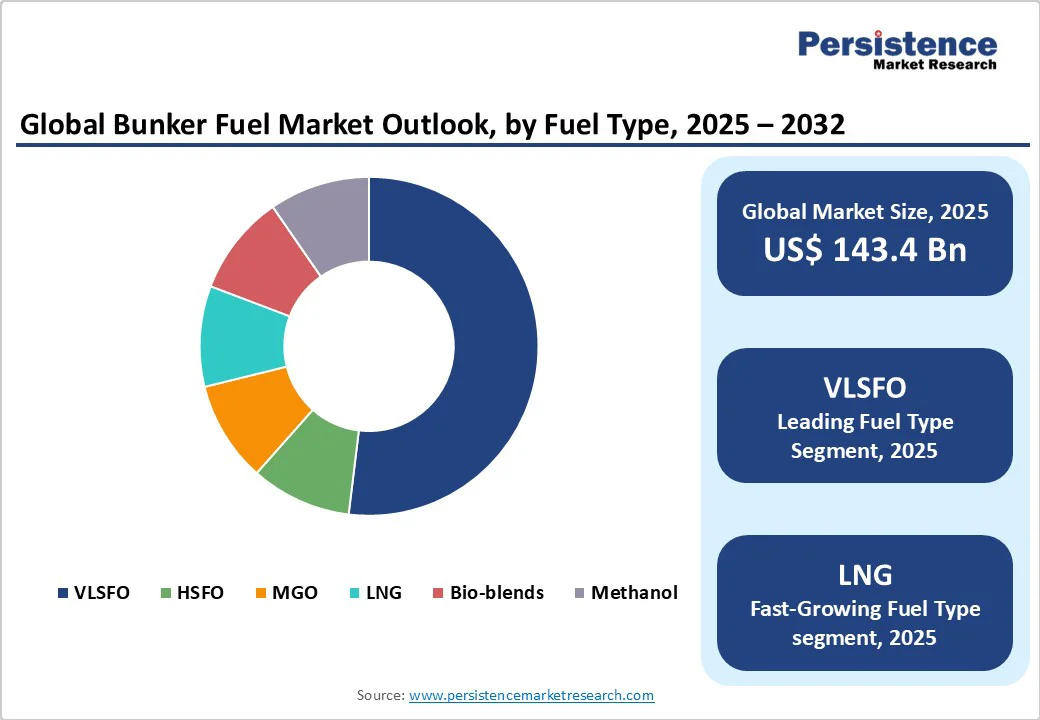

- Dominant Fuel Type: Very Low Sulfur Fuel Oil (VLSFO) with 53.4% revenue share in 2024, driven by IMO 2020 compliance and engine compatibility.

- Leading Application: Container and tanker vessels dominate fuel consumption, accounting for approximately 43.2% of total market share in 2025, reflecting high volume requirements on long-haul and transoceanic routes.

| Key Insights | Details |

|---|---|

| Bunker Fuel Market Size (2025E) | US$143.4 Bn |

| Market Value Forecast (2032F) | US$230.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Shift to Low-sulfur Fuels and IMO Policy

The IMO 2020 sulfur cap and further tightening of emissions policy are decisive drivers for bunker fuel demand. In 2024, VLSFO accounted for approximately 54% of bunker revenue as shipowners replaced or blended legacy Heavy Fuel Oil. Upcoming carbon pricing discussions are accelerating investments in alternative bunkers and dual-fuel retrofits. This drives higher demand for compliant fuels, premium pricing for alternatives, and increased investments in ports and storage.

Trade Volumes and Route Disruptions

Global seaborne trade volumes, port throughput, and temporary route adjustments significantly impact bunker demand. Singapore recorded approximately 54.9 million metric tons in 2024, with Rotterdam and Fujairah showing similar trends due to growth in container throughput and diversions to the Red Sea. These disruptions create short-term volume spikes, reshaping bunkering patterns and highlighting the importance of resilient supply chains and storage capacities.

Alternative Fuels and Shipowner Decarbonization Programs

Shipowners are investing in LNG, methanol, and biofuel supply chains to meet decarbonization targets. LNG bunkering volumes have grown substantially and are expected to double by 2030. Fleet conversions to dual-fuel ships and long-term bio-methanol contracts are creating a bifurcated market: steady demand for conventional bunkers alongside a high-growth alternative fuels segment requiring significant infrastructure investment.

Barrier Analysis - Price Volatility and Feedstock Exposure

Bunker pricing remains closely tied to fluctuations in crude oil, affecting shipowner operating costs. Historical crude shocks caused intra-year price variance of 20-40%, increasing working capital needs and tightening distributor margins. This uncertainty can suppress demand or shift vessels toward scrubber-equipped High Sulfur Fuel Oil (HSFO), where price differentials allow.

Infrastructure and Feedstock Constraints

The scale-up of LNG, methanol, and biofuel bunkering is limited by terminal capacity, vessel compatibility, and high capital expenditure (Capex) requirements. LNG bunkering volumes currently account for a small share of global bunker consumption, limiting their immediate displacement potential absent significant investment. Limited availability and premium pricing constrain adoption by price-sensitive carriers.

Opportunity Analysis - LNG and Dual-fuel Bunkering Build-out

Ports and energy majors are expanding LNG bunkering capacity. LNG volumes are expected to at least double by 2030, creating multi-billion-dollar commercial opportunities for terminal operators, bunker vessels, and fuel traders. Early investments and joint ventures in LNG infrastructure can secure a first-mover advantage.

Low-carbon Fuels and Green Corridors

Sustainable marine biofuels, green methanol, and e-fuels represent a growing opportunity. Early adoption corridors in Europe-Asia could account for a meaningful share of global tonnage uplift by 2030. Even a 5-10% displacement of global bunker revenue to low-carbon fuels represents a multi-billion-dollar market opportunity, incentivizing feedstock contracts and supply logistics partnerships.

Category-wise Analysis

Fuel Type Insights

Very Low Sulfur Fuel Oil (VLSFO) remains the largest contributor to bunker fuel revenue, accounting for a 53.4% market share in 2024. This dominance is primarily due to global compliance with IMO 2020 regulations, which mandated a maximum sulfur content of 0.5% for marine fuels outside Emission Control Areas (ECAs).

VLSFO is compatible with existing marine engines, requiring minimal retrofits, making it the preferred choice for most shipowners. Key examples include major carriers such as Maersk and MSC, which rely extensively on VLSFO for their container fleets operating on Asia-Europe and Transpacific routes. Port hubs such as Singapore, Rotterdam, and Fujairah offer widespread VLSFO availability, reinforcing their dominance.

LNG is experiencing the fastest growth, with double-digit CAGR projections in several markets. LNG adoption is accelerating due to its lower sulfur emissions and potential for carbon reduction when paired with renewable gas or bio-LNG. Companies such as CMA CGM and Wärtsilä are expanding their LNG dual-fuel fleets, while ports like Rotterdam and Singapore have commissioned LNG bunker vessels to meet the growing demand.

Methanol and bio-blends are gaining traction in Europe and Asia, particularly on short-sea shipping routes and ferries that benefit from predictable refueling schedules. Growth drivers include regulatory incentives, investment in bunkering infrastructure, and rising demand for lower-emission alternatives.

Application Insights

Container ships and oil tankers dominate bunker fuel consumption due to their high fuel intensity and global operational reach. Container vessels, particularly ultra-large container ships (ULCS), consume vast quantities of fuel on transoceanic routes, such as Asia-Europe and Transpacific trade lanes.

Oil tankers operating in long-haul crude transport, including routes from the Middle East to Asia or Europe, also represent a significant portion of total bunker demand. Together, these segments account for the majority of revenue due to both high fuel volumes and the frequency of voyages.

Specialist vessels and short-sea ferries, including ro-ro vessels, passenger ferries, and smaller coastal operators, are rapidly adopting LNG and methanol as fuel alternatives. For example, the Scandlines ferry fleet in Northern Europe and the Shenzhen-Hong Kong short-sea ferries are being retrofitted for LNG, supported by accessible port infrastructure.

These segments experience faster adoption rates due to predictable routing, port proximity, and early exposure to environmental regulations. As low-carbon fuel availability expands, these vessels are expected to achieve the highest compound growth in fuel consumption share among all vessel types.

Regional Insights

Asia Pacific Bunker Fuel Market Trends - Singapore Dominates as LNG and Methanol Adoption Expands

Asia Pacific is the largest global bunker fuel market, accounting for 39.5% of total revenue in 2024, led by Singapore, China, South Korea, and Japan. Singapore remains the dominant hub, with 54.9 million tonnes bunkered in 2024, supported by its strategic location along the Strait of Malacca and comprehensive multi-fuel infrastructure.

Growth drivers include expansion of freight trade, increasing port throughput, and proximity to major east-west trade lanes. Regulatory incentives and infrastructure development encourage the adoption of LNG, methanol, and biofuels.

Recent developments include China COSCO Shipping’s LNG dual-fuel fleet expansion in 2025 and Japan’s Port of Yokohama introducing LNG bunkering services for short-sea and feeder vessels. Country-specific insight: China is rapidly scaling its coastal bunkering infrastructure to support alternative fuels and reduce emissions from the country’s growing fleet of container, bulk, and tanker vessels.

Europe Bunker Fuel Market Trends - ARA Cluster Leads with LNG and Biofuel Bunkering Initiatives

Europe is the fastest-growing market, and activity is concentrated in the Rotterdam-Antwerp-Amsterdam (ARA) cluster, with the Netherlands leading in LNG infrastructure deployment. The region benefits from decarbonization policies, including FuelEU Maritime regulations, which incentivize the use of low- and zero-carbon fuels.

In 2024, investments focused on collaborative LNG bunker vessel projects and biofuel offtake agreements between ports, shipping lines, and energy majors.

Notable recent developments include TotalEnergies and CMA CGM’s joint LNG bunkering venture in Rotterdam, enhancing the availability of compliant fuels for container and tanker fleets. Country-specific insight: Germany is a key market, with Hamburg and Bremerhaven ports actively expanding LNG and methanol bunkering terminals to serve both short-sea shipping and international trade routes.

North America Bunker Fuel Market Trends - Growth Driven by U.S. Ports, LNG Pilots, and ECA Compliance

North America’s bunker fuel market is a key global segment, with the U.S. ports of New York/New Jersey, Los Angeles/Long Beach, and the Gulf of Mexico complex accounting for the majority of volumes. In 2024, the market size was estimated at US$22-24 Bn, supported by robust container trade growth and sustained offshore energy activity.

Environmental regulations, particularly within the North American Emission Control Areas (ECAs), have accelerated the adoption of low-sulfur fuels and cleaner alternatives.

Integrated oil majors such as ExxonMobil, Chevron, and Shell dominate the supply chain, offering multi-fuel bunkering solutions. Recent developments include Houston’s pilot LNG bunkering facility, launched in late 2024, aimed at supporting dual-fuel vessels and expanding alternative fuel availability.

Country-specific insight: The U.S. leads the region, with West Coast ports implementing digital fuel management systems and enhanced storage capacity to support growing container and tanker throughput.

Competitive Landscape

The global bunker market is dominated by oil majors and large trading houses, but functionally fragmented by port and supplier type. Top suppliers capture most revenue through refinery integration and trading platforms, while specialist and regional independents handle local volumes.

Key strategies include integrated supply chain control, port infrastructure investments, long-term offtake contracts for low-carbon fuels, and technology partnerships for fuel quality and emissions compliance.

Key Industry Developments

- In October 2025, BIMCO adopted a Methanol Annex to standardize marine fuel supply contracts for methanol, building on its earlier success with the LNG annex adopted in 2023.

- In April 2025, the Maritime and Port Authority of Singapore announced plans to supply over 1 million metric tons of low-carbon methanol annually by 2030, aiming to address the growing demand for alternative bunker fuels.

Companies Covered in Bunker Fuel Market

- Shell

- BP

- ExxonMobil

- TotalEnergies

- Vitol

- Trafigura

- Bunker Holding

- Chevron

- PetroChina

- Sinopec

- Neste

- Glencore

- Koch Supply & Trading

- Oiltanking

- Marquard & Bahls

- Engen

- Lukoil

- Valero Energy

- Petronas

- MOL Group

Frequently Asked Questions

The market size in 2025 is estimated at US$143.4 Billion.

By 2032, the market is projected to reach US$230.1 Billion.

Key trends are investment in LNG bunkering infrastructure at major ports and rapid uptake of LNG, methanol, and bio-blends as alternative fuels.

The Very Low Sulfur Fuel Oil (VLSFO) segment is the leading fuel type, accounting for 54.4% of revenue in 2024, due to its compliance with international sulfur regulations and compatibility with existing ship engines.

The bunker fuel market is expected to grow at a CAGR of 6.5% between 2025 and 2032.

Major players include Shell, BP, ExxonMobil, TotalEnergies, and Vitol.