- Automotive

- Europe Used Car Market

Europe Used Car Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Europe Used Car Market by Vehicle Type (Hatchback, Sedan, SUVs, Pickup Truck, Van & MPV, Others), Vehicle Age (Less than 3 Years, 3 to 7 Years, 7 to 10 Years, Above 10 Years), Fuel Type (Gasoline/Petrol, Diesel, CNG, EVs & Hybrids), Sales Channel (Organized Dealers / Platforms, Unorganized Dealers / Brokers), and Country Analysis for 2026 to 2033

Europe Used Car Market Trends & Analysis

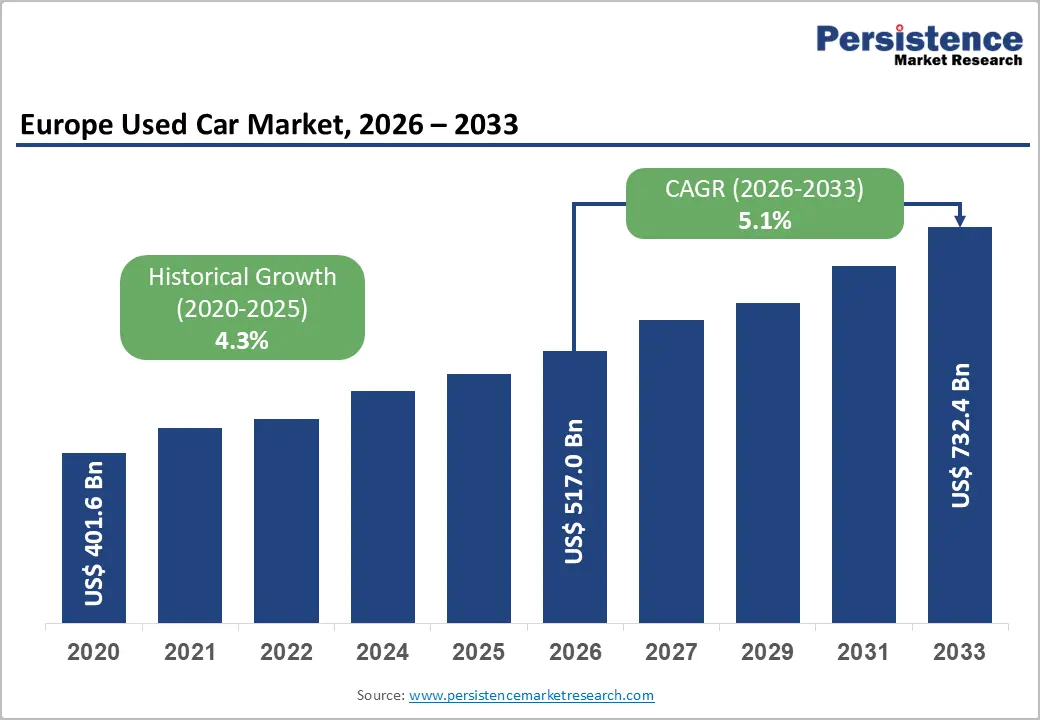

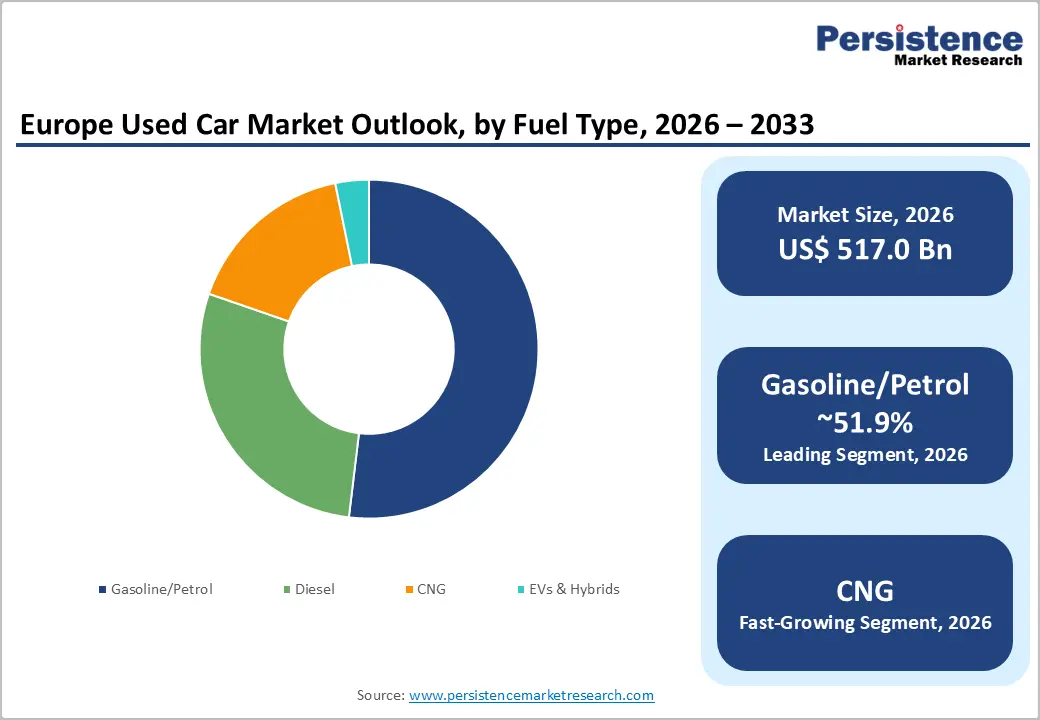

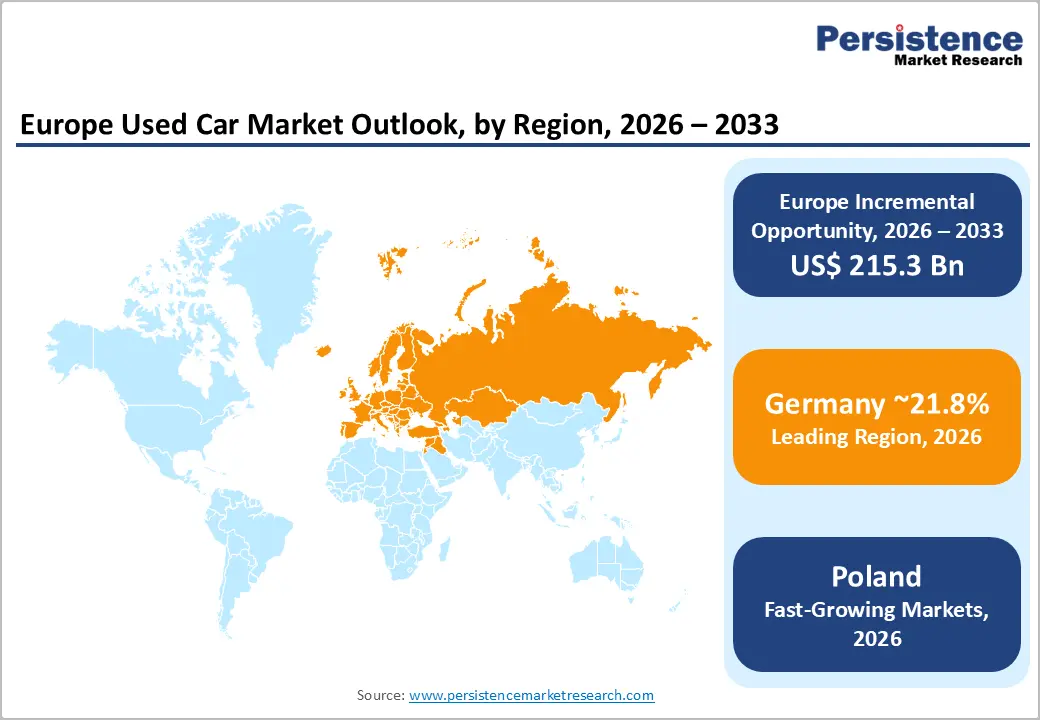

The Europe used car market size is anticipated at US$ 517.0 billion in 2026 and is projected to reach US$ 732.4 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

The demand is driven by cost-of-living pressures in European countries, tightening new-car affordability, and the accelerating transition to alternative-fuel vehicles that is generating high-quality, low-mileage trade-ins. Organized digital platforms are formalizing transactions across the continent.

EU emissions regulations under Euro 7 and the 2035 ICE ban roadmap are intensifying new-vehicle price inflation, systematically redirecting budget-conscious buyers toward the used-car channel. Platform consolidation, led by Mobile.de, AutoScout24, and BCA Group, is raising consumer trust and transaction efficiency across all major European markets.

Key Industry Highlights:

- Leading Sales Channel: Organized Dealers/Platforms dominate at ~63% share, with AutoScout24, Mobile.de, and Auto Trader driving digital transaction transparency and financing integration across Europe.

- Fast-Growing Fuel Type: CNG fuel type at ~12.9% CAGR and Vans & MPVs at 5.0% CAGR lead growth, driven by fleet operator fuel optimization and last-mile delivery demand, respectively.

- Country Leaders: Germany leads at 21.8% share on fleet depth and CPO infrastructure; Poland is expected to achieve ~6.9% CAGR on income convergence and accelerating platform adoption.

- Key Development: AUTO1 Group's pan-European used EV CPO program launch and BCA Group's acquisition of Autorola signal consolidation of the organized B2B and B2C remarketing infrastructure.

Market Dynamics Analysis

Drivers - New-Vehicle Price Inflation and Electrification Mandates Redirecting Demand

New passenger car prices in the European Union have risen substantially as manufacturers integrate electrification costs, with the European Automobile Manufacturers' Association (ACEA) reporting that the average new car transaction price surpassed €36,000 in 2023, a level that excludes the majority of European households from new-car ownership without significant financing. The European Central Bank's monetary tightening cycle elevated consumer lending rates to their highest levels in over a decade, further compressing new-car affordability and routing demand toward the pre-owned segment.

The European Commission's regulatory mandate to end sales of new internal combustion engine (ICE) passenger cars by 2035 is triggering accelerated fleet turnover, as consumers and leasing companies rush to sell or replace ICE assets before the deadline. The ACEA reported 9.2 million new car registrations in the EU in 2023, generating a large cohort of vehicles entering the used market within 1-3 years. This policy-driven inventory pipeline is sustaining used-car supply quality and transaction volumes through the forecast period.

Digital Platform Maturity Driving Transaction Efficiency and Cross-Border Market Integration

Europe's used-car digital marketplace ecosystem has reached institutional scale, with Autobiz Group, Mobile.de (Volkswagen Group), AutoScout24, and BCA Group processing millions of monthly transactions and progressively integrating financing, warranty, and logistics services. The European Commission's Digital Markets Act and Digital Services Act frameworks are enforcing platform transparency and data portability standards that further legitimize digital automotive commerce. Eurostat reports that 90% of EU consumers aged 16-74 regularly use the internet, providing the penetration base that sustains platform growth.

Cross-border used-car flows within the EU single market, particularly from Germany, Belgium, and the Netherlands toward Eastern Europe and the Balkans, have scaled significantly as digital listings enable buyers to efficiently source higher-specification vehicles from Western markets at competitive prices. The European Automobile Dealers Association (AECDA) estimates that cross-border used-car transactions account for approximately 5-8% of total European used-car volumes, a share that is growing as logistics and documentation barriers continue to fall under EU single-market harmonization.

Restraints - Divergent National Registration and Emissions Regulations Creating Cross-Border Trade Friction

Despite the EU single market framework, used-car cross-border transactions face significant friction from divergent national vehicle registration requirements, emissions-based taxation regimes, and homologation standards. Countries including France, Italy, and Denmark apply congestion or pollution-linked registration surcharges to imported used vehicles based on CO2 ratings, materially raising landed costs for cross-border buyers. The European Parliament has raised concerns that these national-level fiscal instruments, while nominally environmental, effectively function as non-tariff trade barriers that fragment the pan-European used-car market and sustain price disparity.

Shortage of Affordable Near-New EV Inventory Limiting Used Electric Vehicle Market Development

While EVs represent the fastest-growing fuel segment in European new car sales, the used EV market remains constrained by the limited availability of affordable pre-owned electric vehicles in the sub-€20,000 segment where volume demand is concentrated. Battery degradation uncertainty, absent standardized state-of-health (SOH) certification protocols, and residual value volatility, with the EV residual value index tracked by Autovista Group showing elevated depreciation in some segments, are deterring used-car buyers and suppressing transaction conversion rates for electric vehicles specifically.

Opportunities - Used EV Certification Programs Unlocking a High-Growth Premium Segment

The emerging certified pre-owned (CPO) electric vehicle segment represents one of Europe's most commercially compelling used-car opportunities, with OEM brands including Volkswagen, Renault, and BMW launching dedicated used EV inspection, battery certification, and warranty programs that address residual value uncertainty. The European Battery Alliance has advocated for standardized EV battery health reporting protocols, and the EU Battery Regulation, requiring battery passports for new EVs from 2026, will progressively create the data infrastructure that enables transparent used EV valuation.

For platform operators and organized dealers, CPO EV programs deliver higher gross margins per unit, stronger brand differentiation, and alignment with EU Green Deal consumer sentiment. OEM-certified used EV programs in Germany and the U.K. are already commanding 8-12% transaction premiums versus non-certified equivalents. Dealers investing in battery diagnostic infrastructure and EV-trained technicians in 2025-2026 are well positioned to lead this segment as EV fleet maturity creates an accelerating second-life inventory supply through the late 2020s.

Eastern European Market Digitization Creating Platform Expansion Opportunities

Poland, Czech Republic, Romania, and Hungary represent an underserved digital used-car market opportunity within Europe. These markets combine high used-car transaction volumes; Poland alone processes approximately 1.5 million used-car transactions annually, per data from the Polish Automotive Industry Association (PAIA), with relatively immature platform ecosystems dominated by generalist classifieds and informal brokers. The income convergence between Eastern and Western Europe, tracked by Eurostat's GDP per capita data, showing Eastern EU members closing the gap by approximately 1-2% annually, is raising consumer expectations for the service standards offered by organized digital platforms.

Western European platform operators that expand into Poland, the Czech Republic, and Romania via localized platform interfaces, regional dealer network partnerships, and adapted financing products are positioned to convert these markets' large informal transaction volumes into organized digital commerce. The EU's Digital Compass 2030 program targets 80% digital skills coverage across member states by 2030, accelerating the consumer readiness that underpins platform adoption in currently less-digitized Eastern markets.

Category-wise Analysis

Vehicle Type Insights

Hatchbacks lead Europe used car market by vehicle type with approximately 37% of total market share in 2026, a dominance reflecting their fit with European urban mobility conditions, compact dimensions, fuel efficiency, ease of parking, and lower insurance and running costs versus larger formats. Across Germany, France, the U.K., Italy, and Spain, the hatchback segment, anchored by high-volume models including Volkswagen Golf, Ford Focus, and Renault Clio, commands the widest buyer base across income segments and age cohorts. This leadership is stable, though Van & MPV and SUV segments are gaining value-share as family-formation demographics and remote-work lifestyle shifts sustain demand for larger, versatile formats in suburban and semi-rural markets.

Vans & MPVs are the fastest-growing vehicle type segment at a CAGR of 5.0% by 2033, driven by the growth of last-mile delivery, small business logistics, and micro-mobility fleet operators sourcing affordable commercial vans from the used-car channel across Germany, France, and Poland.

Vehicle Age Insights

Vehicles aged less than 3 years command the leading share within the vehicle age category at approximately 42% of European used-car market revenue in 2026. This cohort's dominance reflects Europe's large leasing market, the European Leasing and Finance Association (Leaseurope) reports that approximately 40% of new cars in Western Europe are acquired through leasing contracts, which generates a continuous, high-quality supply of 24-36 month-old vehicles re-entering the market with manufacturer service records, low mileage, and eligible residual warranty coverage.

OEM-certified programs are predominantly built around this age band, enabling premium pricing and financing integration that sustains its revenue share leadership relative to older vehicle cohorts commanding lower per-unit values.

The 3 to 7 years vehicle age segment is the fastest-growing category at a CAGR of approximately 6.6% by 2033, driven by expanding middle-income buyer access to quality mid-aged vehicles through digital platforms that improve price discovery and reduce the trust deficit historically associated with non-certified used-car transactions.

Fuel Type Analysis

Gasoline/Petrol vehicles maintain the leading fuel-type share at approximately 52% of European used-car market revenue in 2026, a position sustained by the massive installed base of petrol-engine vehicles in the European fleet, the widespread petrol station infrastructure, and consumer familiarity with petrol powertrains across all income segments. However, this share has declined from historical highs above 60% as diesel vehicles, despite regulatory headwinds from urban low-emission zones (LEZs), and increasingly EVs and hybrids gain transaction share.

Diesel's share erosion in major cities due to LEZ access restrictions enforced in Paris, London, Berlin, and Madrid is the primary structural factor slowly compressing petrol's relative dominance by reducing diesel supply, which indirectly redirects buyers toward petrol alternatives.

CNG (Compressed Natural Gas) vehicles are the fast-growing fuel type segment at a CAGR of approximately 12.9% by 2033, driven by fleet operator fuel-cost optimization in Italy and Germany, where CNG infrastructure is most developed, and by commercial vehicle operators seeking emission-compliant access to urban low-emission zones.

Sales Channel Insights

Organized dealers and platforms lead the sales channel category with approximately 63% of European used-car market revenue in 2026, a share built on the back of decades of dealership network development and accelerated by the digital transformation of automotive retail since 2018. Leading platforms, AutoScout24, Mobile.de, Gumtree Autos (U.K.), and La Centrale (France), have aggregated buyer demand at continental scale, while franchise and independent organized dealers have invested in digital forecourt tools, online finance origination, and click-and-collect transaction models.

EU consumer protection regulation and mandatory warranty provisions for used-car sales through commercial dealers further reinforce buyer preference for the organized channel versus informal broker transactions where recourse is limited.

Unorganized dealers and brokers represent the slower-growing channel at approximately 2.6% CAGR by 2033, retaining a meaningful share in price-sensitive Eastern European markets and private peer-to-peer transactions but progressively losing relative position as digital platforms lower the convenience barrier of the organized channel for price-segment buyers.

Country Market Insights

Germany Used Car Market Trends

Germany commands 21.8% of European used-car market revenue in 2026, reflecting its position as Europe's largest vehicle market, the home of Volkswagen Group, BMW, Mercedes-Benz, and a dense, organized dealer network. High new-car lease penetration generates continuous near-new inventory supply, and the Kraftfahrt-Bundesamt (KBA) reported approximately 7.3 million used-car re-registrations in 2023, validating deep transaction volumes.

Munich: Germany's Premium Used Car Transaction and CPO Hub

Munich anchors approximately 12% of Germany's used-car transaction value, driven by high per-capita income, proximity to BMW Group headquarters and certified pre-owned dealer networks, and strong luxury segment demand. Munich's used-car market, characterized by near-premium and premium inventory from lease returns, commands among Europe's highest average transaction values per vehicle. The city's market is projected to grow at approximately 4.8% CAGR by 2033, sustained by CPO program expansion.

Berlin, Hamburg, and Frankfurt collectively represent approximately 35% of Germany's used-car volume. Berlin's large young-adult population drives high-turnover compact and electric vehicle demand; Hamburg's port proximity supports import flows; Frankfurt's financial sector concentration sustains premium segment activity.

UK Used Car Market Trends

UK is likely to achieve a prominent 5.2% CAGR within the European used-car market, supported by its position as Europe's second-largest vehicle market. The Society of Motor Manufacturers and Traders (SMMT) reported approximately 7.6 million used-car transactions in 2023, with organized retailers including Arnold Clark, Cinch, and Auto Trader driving digital-channel expansion. Post-Brexit import dynamics and strong consumer credit infrastructure sustain market activity.

London: UK's Largest and Most Digitally Advanced Used Car Market

London accounts for approximately 18% of UK used-car market revenue, with demand concentrated in compact and hybrid vehicles driven by the Ultra Low Emission Zone (ULEZ) expansion that has made compliant used vehicles a high-priority purchase category for London residents. Auto Trader's data shows London as the platform's highest-transaction density city. The London used-car market is projected to grow at approximately 5.5% CAGR by 2033 as ULEZ-compliant inventory commands a sustained premium.

Birmingham, Manchester, and Glasgow collectively represent approximately 28% of the UK used-car volume. These cities combine large working-population bases with growing organized dealership density, with Motorpoint and We Buy Any Car actively expanding regional footprints as digital transaction adoption accelerates outside London.

Poland Used Car Market Insights

Poland is the fast-growing country market in Europe's used-car sector at approximately 6.9% CAGR through 2033, driven by rising household incomes, the world's highest per-capita used-car import volumes per Eurostat vehicle trade data, and a progressive shift from informal to organized retail channels as platform operators expand into Central Eastern Europe. The PAIA estimates over 1.5 million used-car registrations annually.

Warsaw: Poland's Dominant and Fast-Digitalizing Used Car Hub

Warsaw accounts for approximately 22% of Polish used-car market revenue, with rapidly rising digital transaction share as platforms including OtoMoto, Poland's leading automotive marketplace with over 300,000 active listings, achieve national scale. The capital's growing professional middle class is upgrading from older imported vehicles to near-new certified pre-owned models, raising average transaction values. Warsaw's market is projected to grow at approximately 7.2% CAGR through 2033.

Kraków, Wroclaw, and Gdansk account for approximately 30% of Polish used-car volume. These industrial and port cities combine active import-sourcing networks, particularly for German and Dutch trade-ins, with a growing organized retail infrastructure serving price-sensitive but quality-aware regional buyers.

Competitive Landscape

Europe's used car market is moderately fragmented at the dealer level but increasingly consolidated at the platform layer, with AutoScout24, Mobile.de (Volkswagen Group), BCA Group (Constellation Automotive), and Arnold Clark commanding leading positions. Key differentiators include CPO warranty depth, financing integration, and EV battery certification capability. Subscription and home-delivery transaction models are gaining adoption among digital-native players.

Dominant strategic themes include cross-border platform geographic expansion into Eastern Europe, investment in EV used-car inspection and certification infrastructure, and OEM partnerships for certified pre-owned programs. Cost leadership through digital procurement and auction automation remains a priority for wholesale operators while consumer-facing platforms invest in experience differentiation.

Key Market Players

- Constellation Automotive Group (BCA Group), Enfield, UK (Pan-European vehicle remarketing and auction)

- Mobile.de (Volkswagen Group), Berlin, Germany (Germany's largest digital used-car marketplace)

- AutoScout24 (Axel Springer), Munich, Germany (Pan-European used-car classified platform)

- Arnold Clark Automobiles, Glasgow, UK (UK's largest independent used-car retailer)

- Auto Trader Group plc, Manchester, UK (UK's leading digital automotive marketplace)

- Cazoo Group, London, UK (UK/European online used-car retailer with home delivery)

- Cinch Cars (Constellation Automotive), Enfield, UK (UK digital used-car marketplace)

- OtoMoto (OLX Group), Poznan, Poland (Central Eastern European automotive classifieds platform)

- La Centrale (Mobilité Banque), Paris, France (France's leading used-car classified platform)

- AutoHero (AUTO1 Group), Berlin, Germany (Pan-European digital used-car retailer)

- AUTO1 Group, Berlin, Germany (European B2B automotive e-commerce platform)

- Heycar (Volkswagen Financial Services), Berlin, Germany (Digital certified pre-owned platform)

- Motorpoint Group plc, Derby, UK (UK multi-brand nearly-new car superstore)

- Autobiz Group, Paris, France (B2B vehicle valuation and remarketing platform)

- Manheim Europe (Cox Automotive), Dartford, UK (Pan-European vehicle auction and remarketing)

Strategic Developments

- In February 2025, AUTO1 Group launched its AutoHero certified pre-owned electric vehicle program across Germany, France, and Spain, featuring standardized EV battery health reporting and 12-month drivetrain warranties, targeting the fast-growing used EV segment in Western European markets.

- In March 2024: Auto Trader Group launched its Retail Check vehicle provenance verification service across the UK, integrating DVLA, finance house, and insurance data to deliver real-time used-car history transparency, targeting conversion rate improvement for both dealers and private sellers.

- In November 2023: Heycar (Volkswagen Financial Services) expanded its certified pre-owned digital platform into Italy and Poland, partnering with Volkswagen Group franchise dealer networks to provide warranty-backed used-car listings with integrated Volkswagen Bank financing pre-approval in both markets.

Companies Covered in Europe Used Car Market

- Constellation Automotive Group

- Mobile.de

- AutoScout24

- Arnold Clark Automobiles

- Auto Trader Group plc

- Cazoo Group

- Cinch Cars

- OtoMoto

- La Centrale

- AutoHero

- AUTO1 Group

- Heycar

- Motorpoint Group plc

- Autobiz Group

- Manheim Europe

Frequently Asked Questions

Europe Used Car Market is likely to be valued at US$ 517.0 billion in 2026 and is projected to reach US$ 732.4 billion by 2033, creating an incremental opportunity of US$ 215.4 billion.

Key growth drivers include rising new-car prices, EU vehicle-emission regulations, strong digital marketplace adoption, and increasing demand for affordable mobility solutions.

Europe used car market is expected to achieve a CAGR of 5.1% from 2026 to 2033, supported by expanding used EV sales and organized online platforms.

Major opportunities include the growth of certified pre-owned EVs, expansion of digital used-car platforms, and increasing market formalization in Eastern Europe.