- Electric Mobility

- Electric Bus Market

Electric Bus Market Size, Share, and Growth Forecast, 2025 - 2032

Electric Bus Market By Vehicle Type (Battery Electric Vehicle (BEV), Others), Range (Less than 150 Km, Others), Battery Capacity (≤200 kWh, 201-300 kWh, Others), Power Output (100 hp (~75 kW), Others), Length (Mini (≤9 m), Standard (10-12 m), Long (>12 m)), and Regional Analysis for 2025 - 2032

Electric Bus Market Share and Trends Analysis

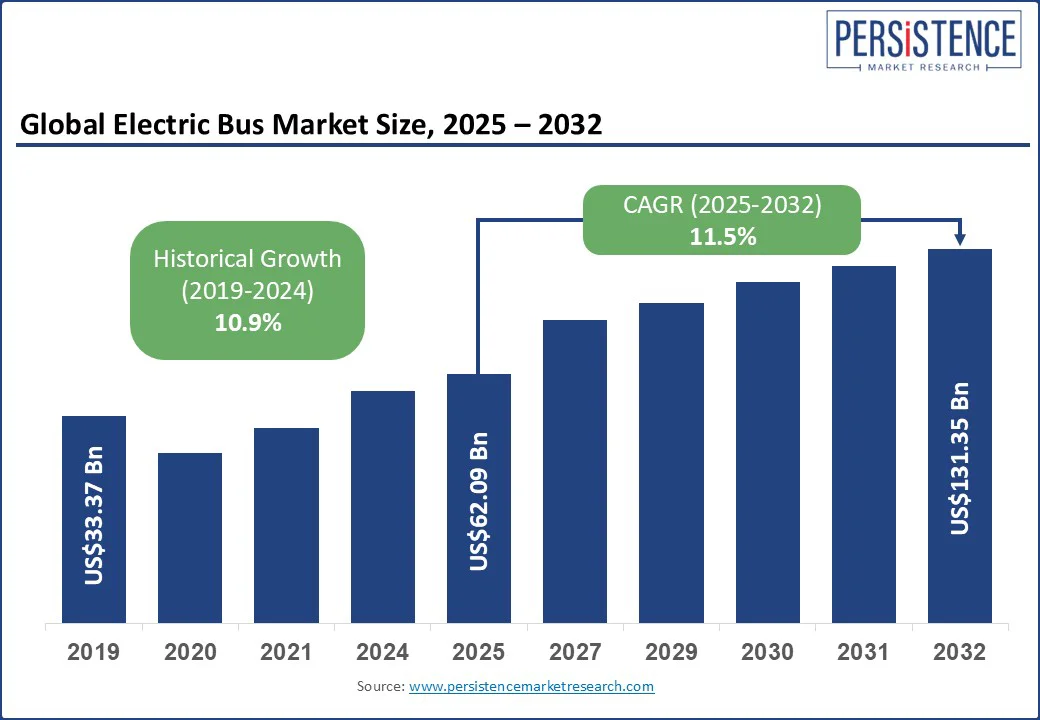

The global electric bus market size is projected to rise from US$62.09 Bn in 2025 to US$131.35 Bn by 2032. It is anticipated to witness a CAGR of 11.5% during the forecast period from 2025 to 2032.

The electric bus industry growth is driven by declining lithium-ion battery costs, which have fallen by nearly 89% since 2010, the rise of electric bus-as-a-service (eBaaS) models, and increasing investments in interoperable fast-charging infrastructure.

Electric buses (e-buses) offer sustainable alternatives to diesel fleets amid mounting global pressure to decarbonize urban mobility. With zero tailpipe emissions, rapid advances in battery technology, reduced noise pollution, and a lower total cost of ownership over time, e-buses are rapidly becoming the backbone of next-generation smart cities and clean transit initiatives. The “Fit for 55” package of the European Union (EU) mandates that 100% of new city buses sold from 2030 onward be zero-emission, stimulating aggressive procurement targets across France, Germany, and the Netherlands.

Key Industry Highlights:

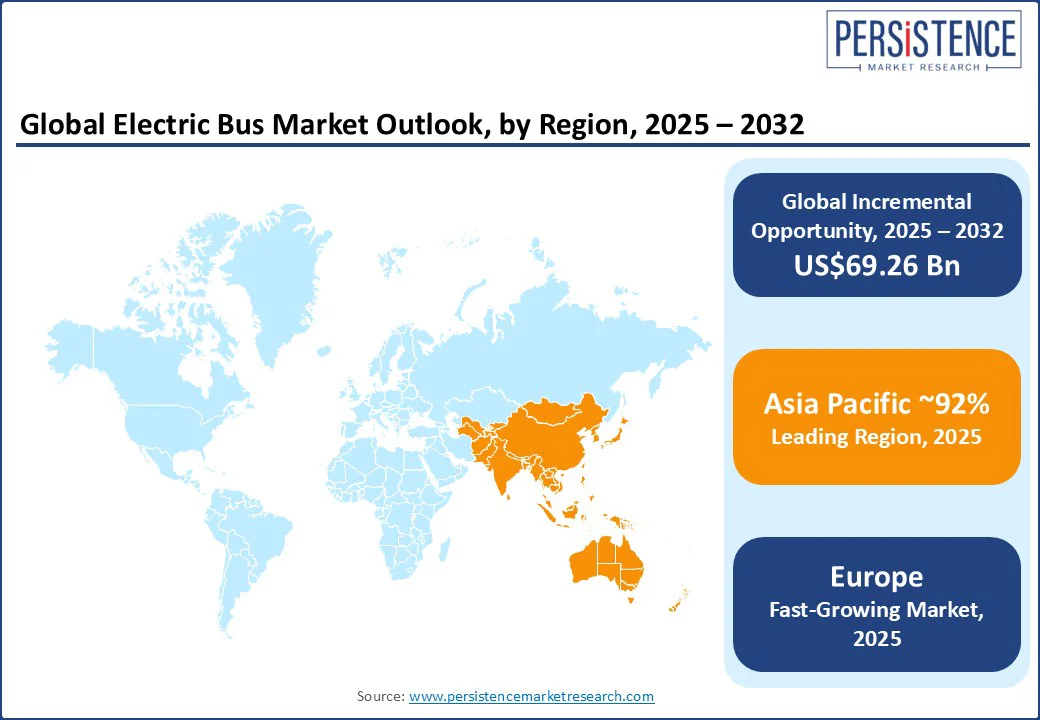

- Leading Region: Asia Pacific is expected to lead the electric bus market in 2025 with over 92% market share, driven by China’s mature EV ecosystem and India’s growing government-led schemes for clean public transport.

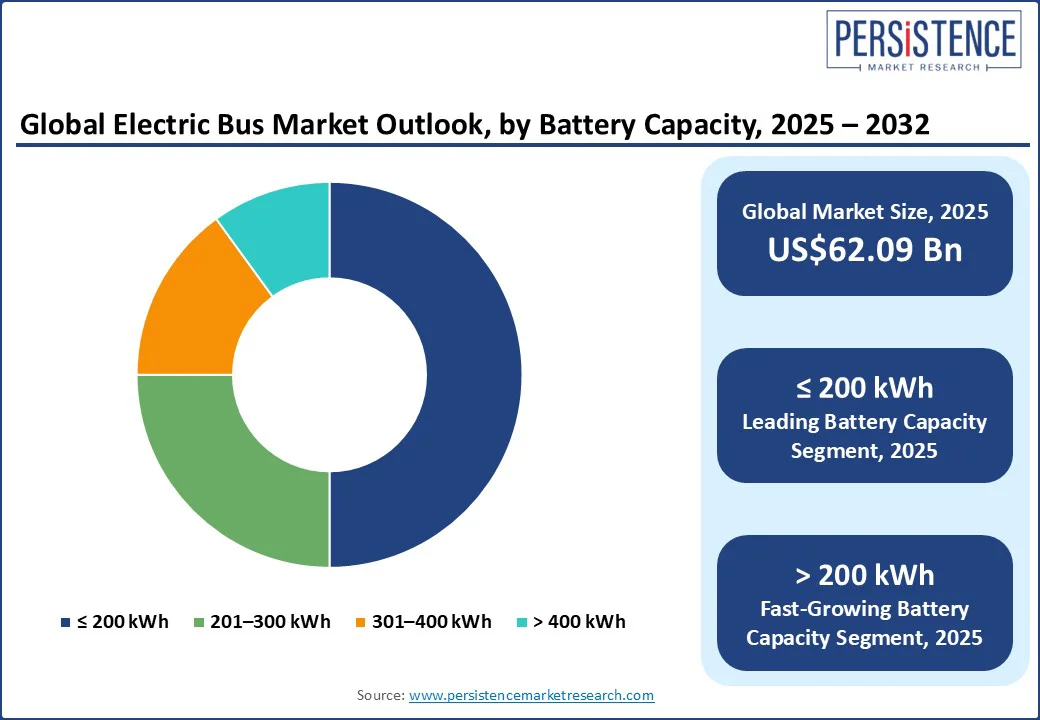

- Leading Battery Capacity: Buses equipped with ≤ 200 kWh battery capacity will dominate the vehicle type segment with a share of nearly 50% in 2025, as transit operators in metro cities are favoring low-cost, lightweight battery electric buses.

- Dominant Vehicle Type: The extensive deployment of battery electric vehicles (BEVs) across major metropolitan transit networks, particularly in the Asia Pacific and Europe, will enable the BEV segment to hold a commanding share of approximately 86% in 2025.

- Fuel cell electric vehicles (FCEVs) are set to record the highest CAGR through 2032 due to hydrogen infrastructure pilots in Japan, South Korea, and Europe.

- Fastest-growing Region: Exhibiting a CAGR of approximately 16%, Europe is set to be the fastest-growing regional market from 2025 to 2032, fueled by the EU’s zero-emission public transport mandates and increasing investment in depot electrification.

- Global Shifts: The global shift toward net-zero transport goals, with over 40 countries setting electric bus adoption targets under the UN’s “Race to Zero” campaign, is proving to be a major growth determinant for the e-bus market.

|

Global Market Attribute |

Key Insights |

|

Electric Bus Market Size (2025E) |

US$62.09 Bn |

|

Market Value Forecast (2032F) |

US$131.35 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

11.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

10.9% |

Market Dynamics

Driver - Public Transit Electrification Mandates to Spark an Upsurge in E-bus Adoption

The progress of the electric bus market is attributed to the wave of public transit electrification mandates set by national and municipal governments. These policy interventions are designed as legally enforceable commitments that are changing procurement strategies and fleet replacement cycles.

For instance, the U.S. Environmental Protection Agency’s US$5 Bn Clean School Bus Program aims to deploy 2,500 zero-emission school buses by 2026. This move has accelerated the demand for battery electric buses in regional transit networks.

Similarly, in Europe, the Clean Vehicles Directive mandates that a minimum of 45% of new public buses procured between 2025 and 2030 must be zero-emission vehicles, which will directly influence tender conditions and investment priorities of original equipment manufacturers (OEMs). In response, electric bus manufacturers are fast-tracking R&D in modular EV platforms and next-gen solid-state batteries to meet compliance thresholds and cost-performance benchmarks.

Restraint - Glaring Infrastructure Deficiencies to Stall Bus Fleet Electrification Momentum

The most pressing restraint stifling the market growth is the chronic underdevelopment of the charging infrastructure required to support large-scale fleet electrification. While global e-bus stock, led by China, reached around 635,000 in 2023, according to the International Energy Agency (IEA), most regions outside East Asia lack the grid resilience, depot capacity, and standardized fast-charging systems needed to sustain this pace of expansion.

For example, the U.K.’s Zero Emission Bus Regional Area (ZEBRA) scheme, which earmarked over £270 Mn (US$ 342.9 Mn) to deploy 1,300 electric buses, has encountered project delays due to local authorities struggling with substation upgrades and land acquisition for charging depots.

In Latin America, despite support from the C40 Cities Finance Facility, countries such as Colombia and Brazil face logistical hurdles in retrofitting existing terminals for high-power chargers, especially in dense urban zones with aging grid infrastructure. The absence of interoperable charging protocols across OEMs has further exacerbated existing operational inefficiencies, making it difficult for transit operators to scale fleets or engage in vendor-agnostic procurement.

Opportunity - Potential Circular Economy of Large Batteries to Produce Lucrative Market Opportunities

One of the most promising yet underleveraged avenues in the market for electric buses is the circular economy potential of high-capacity EV batteries, specifically, second-life energy storage systems (ESS) and battery repurposing solutions.

As the first strand of electric buses deployed in China and parts of Europe reaches its end-of-first-life battery status, which is typically after six to eight years, transit operators and OEMs need to start exploring economically feasible pathways to monetize residual battery value through grid-balancing and stationary storage projects. Some of the biggest bus companies are already tapping into this space. For instance, Volvo Buses and Stena Recycling launched a partnership in 2023 to repurpose retired bus batteries for use in commercial solar energy systems.

In Asia, China’s CATL has pioneered the use of second-life lithium-ion batteries in energy storage stations powering low-income communities. These initiatives help mitigate supply chain pressures for lithium, cobalt, and nickel by extending battery utility beyond transport, and also reduce the total cost of ownership (TCO) for e-buses. Furthermore, the rise of battery lifecycle management platforms, supported by blockchain-based traceability and AI-driven performance analytics, is enabling OEMs and energy utilities to build new electric bus-as-a-service (eBaaS) revenue models.

Category-wise Analysis

Battery Capacity Insights

Buses equipped with ≤ 200 kWh battery capacity are projected to hold the largest market share of approximately 50% in 2025. Many transit operators in densely populated cities favor low-cost, lightweight battery electric buses optimized for frequent stops and depot charging models.

With lower upfront TCO, easier integration with existing power infrastructure, and superior operational flexibility, short-range electric bus variants cater perfectly to urban and last-mile mobility. Transit authorities opted for 150-180 kWh buses in Paris and Bogotá to meet daily run patterns while minimizing infrastructure upgrade needs.

The > 200 kWh battery capacity segment is poised to showcase the highest CAGR through 2032, attributable to the booming demand for long route intercity, coach, and airport shuttle applications. Declining lithium-ion battery costs and OEM innovations, such as Volvo’s BZL platform (282-470 kWh) and Yutong’s U11DD double-deckers (385-422 kWh), are driving operators to choose higher battery capacities for longer range and reduced route queuing.

Governments in regions, such as Gulf Cooperation Council (GCC) countries and Southeast Asia, are leasing high-capacity electric buses for rural-to-urban and intercity corridors, forging partnerships to develop modular EV platforms and dedicated fast-charging hubs.

Vehicle Type Insights

Battery electric vehicles (BEVs) are set to dominate the market in 2025, accounting for approximately 86% of the total revenue share in the vehicle type segment. The massive share of BEVs is due to their widespread adoption across major metropolitan transit networks, particularly in the Asia Pacific and Europe, where zero-emission mandates and fleet electrification goals are accelerating public bus procurement. Leading OEMs such as BYD, which crossed the milestone of delivering over 100,000 battery electric buses globally, are scaling operations to meet the surging demand.

Transit agencies are increasingly favoring BEVs for their lower maintenance costs, compatibility with depot-based charging models, and improved battery efficiency. BEVs continue to be the preferred vehicle type in cities such as Bogotá and London. For example, in 2021, Bogota launched the United for a New Air Initiative to address air pollution in the city while also tackling the climate change crisis and improving public health.

In terms of CAGR, fuel cell electric vehicles (FCEVs) are anticipated to grow the fastest through 2032. FCEVs are finding momentum in regions where longer routes, extreme climates, or hilly terrains demand greater range and fast refueling capabilities. Countries such as South Korea and Germany are scaling hydrogen-powered public transportation, with Seoul investing in over 1,300 hydrogen buses and Italy’s TPER deploying Solaris fuel cell buses in Bologna.

The appeal of hydrogen fuel cell buses is based on their ability to support heavy-duty, long-range transit without compromising on refueling time or vehicle weight. This emerging demand has enabled OEMs to innovate for investors, fleet operators, and governments to build next-generation, low-carbon public mobility ecosystems.

Regional Insights

Asia Pacific Electric Bus Market Trends

Asia Pacific is slated to command approximately 92% of the electric bus market share in 2025, emerging as both the largest and fastest-expanding regional market. Its absolute dominance stems from the large-scale adoption of e-buses in China and India, which is a result of aggressive government-backed electrification programs, such as China’s New Energy Vehicle policy and India’s FAME II initiative. Some of the top OEMs in these countries, such as BYD and Tata Motors, are speedily scaling their production and export capacity, enhancing market penetration across geographies.

High-frequency urban routes are being increasingly electrified using depot-based charging infrastructure, while cities are actively adopting eBaaS models to mitigate procurement risks and optimize operational costs. Advancements in battery technologies, innovations in battery storage and recycling, favorable procurement incentives, and heavy investments in electric bus charging infrastructure have solidified Asia Pacific’s leadership in the zero-emission bus transition.

Europe Electric Bus Market Trends

Europe is anticipated to be the fastest-growing regional market, posting a high CAGR through 2032 in the e-bus market, driven by the EU’s stringent emission mandates and ambitious city-level electrification goals. Initiatives such as the EU Clean Vehicles Directive and London’s target for a fully electric fleet by 2034 are catalyzing the adoption of electric buses in large cities.

European manufacturers such as Solaris, Mercedes-Benz, and Volvo are advancing BEV designs tailored for urban and regional transit. At the same time, they are also piloting FCEVs to effectively resolve limitations related to range and refueling on long-haul routes. With several cities implementing low-emission zones (LEZs) and optimizing route planning with smart mobility platforms, Europe is entrenching its place as a technologically mature market for electric-powered urban mobility.

North America Electric Bus Market Trends

North America is projected to account for a significantly small market share in 2025. The market growth is mainly supported by robust policy frameworks and infrastructure investments intended to fuel the deployment of clean public transit solutions across the continent. For instance, the Innovative Clean Transit (ICT) rule in California mandates a full transition to zero-emission buses by 2040, while federal initiatives such as the Low or No Emission Grant Program of the Federal Transit Administration (FTA) subsidize electric bus purchases.

Domestic OEMs such as Proterra and New Flyer are using these incentives to expand fleet deployments, especially in metropolitan transit networks. There is also an increasing experimentation with vehicle-to-grid (V2G) technology and utility-scale pilot projects to maximize energy efficiency and reduce lifetime ownership costs in the region. Regulatory push and a strong emphasis on localized manufacturing promise long-term growth of the North America electric bus ecosystem.

Competitive Landscape

The global electric bus market pivots around technology integration, policy alignment, and strategic consolidation among OEMs. The critical driver is the race toward building and developing localized manufacturing ecosystems, particularly in response to the worsening geopolitical trade dynamics and climate-linked procurement mandates. For instance, in 2024, BYD inaugurated its third overseas electric bus assembly facility in Brazil, reflecting the success of its decentralized manufacturing model to avoid tariff barriers and reduce logistics costs.

Traditional automakers such as Daimler Truck AG and Volvo Group are increasingly focusing on battery-as-a-service (BaaS) and modular chassis platforms to bring down the total cost of ownership. Vertical integration, wherein players are incorporating proprietary battery and control systems to optimize performance and differentiate from pure-play EV startups, has become a prominent feature in this market. Besides this, joint ventures between automakers and energy utilities, such as Hyundai’s partnership with Korea Electric Power Corporation (KEPCO), enable the formulation of holistic solutions that cover vehicle delivery, depot electrification, and energy management.

Key Industry Developments

- In August 2025, Tata Motors signed an MoU with Green Energy Mobility Solutions (GEMS), the EV arm of Universal Bus Services (UBS), to supply 100 Magna EV intercity electric buses in Tamil Nadu. The Tata Magna EV offers a range of up to 300 km per charge and is equipped with EBS, ESC, and comfort-focused features for long-distance travel.

- In July 2025, Daimler Buses won a contract to deliver 37 battery-electric Mercedes-Benz eCitaro and eCitaro G buses to SWU (Stadtwerke Ulm/Neu-Ulm Verkehr GmbH). These buses will replace SWU’s diesel fleet and feature advanced NMC4 batteries (111 kWh per pack) with fast charging up to 300 kW via depot sockets or pantographs.

Companies Covered in Electric Bus Market

- BYD Company Limited

- Yutong Bus Co., Ltd.

- AB Volvo

- Daimler Truck AG

- Proterra Inc.

- Solaris Bus & Coach sp. z o.o.

- NFI Group Inc.

- Tata Motors Limited

- CRRC Corporation Limited

- Hyundai Motor Company

- Ashok Leyland Limited

- VDL Groep B.V.

Frequently Asked Questions

The global electric bus market is projected to reach US$ 62.09 Bn in 2025.

The rising wave of binding public transit electrification mandates set by national and municipal governments is driving the market.

The electric bus market is poised to witness a CAGR of 11.5% from 2025 to 2032.

The circular economy potential of second-life energy storage systems (ESS) and the emergence of battery lifecycle management platforms are key market opportunities.

BYD Company Limited, Yutong Bus Co., Ltd., and AB Volvo are some key market players.