- Electrical Equipment & Services

- Digital Pump Controller Market

Digital Pump Controller Market Size, Share, and Growth Forecast 2026 - 2033

Digital Pump Controller Market by Product Type (Constant Pressure Controller, Others), Pump Type (Centrifugal Pump Controllers, Others), Power Rating (Low Power (Up to 10 HP), Others), End-use (Commercial Buildings, Others), and Regional Analysis, for 2026 - 2033

Digital Pump Controller Market Size and Trends Analysis

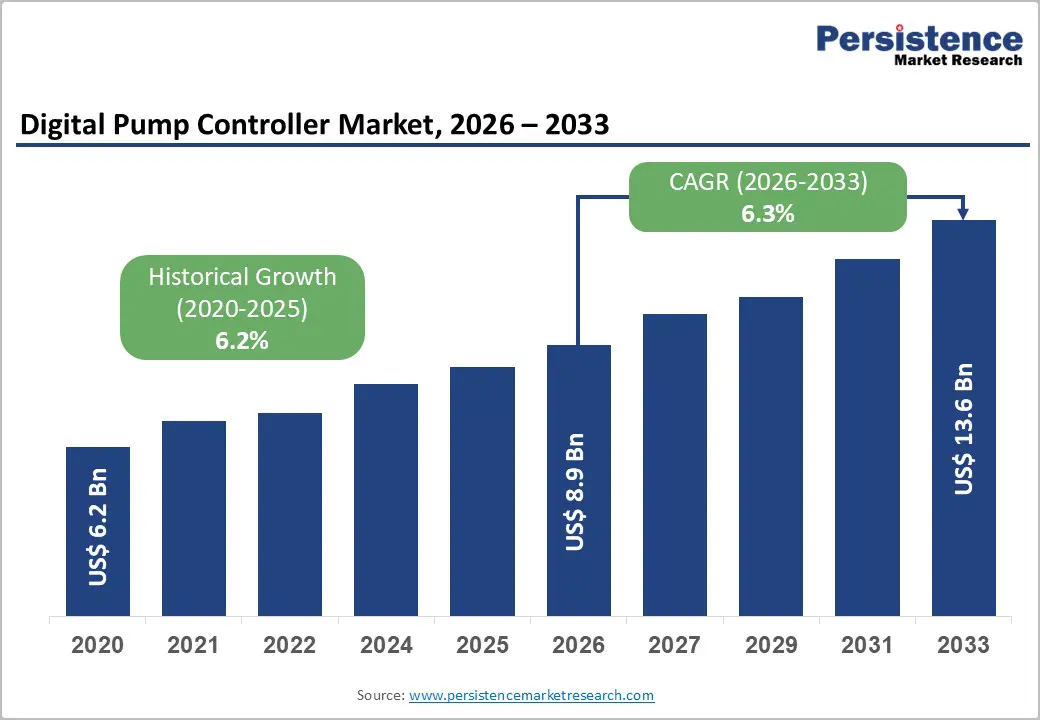

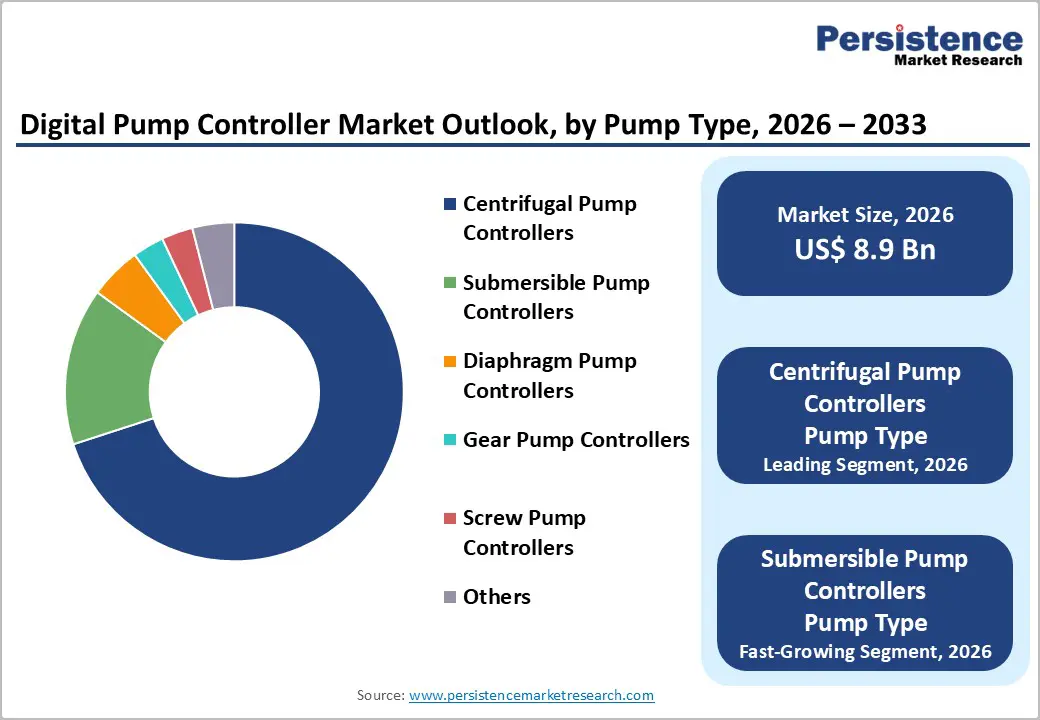

The global digital pump controller market size is expected to be valued at US$8.9 billion in 2026 and projected to reach US$13.6 billion by 2033, growing at a CAGR of 6.3% during the forecast period from 2026 to 2033, driven by escalating demands for energy-efficient water management amid global resource scarcity. This expansion is fueled by regulatory mandates for smart grid integration and IoT adoption in utilities, enabling precise pump operations that cut energy use by up to 30%.

Key Industry Highlights:

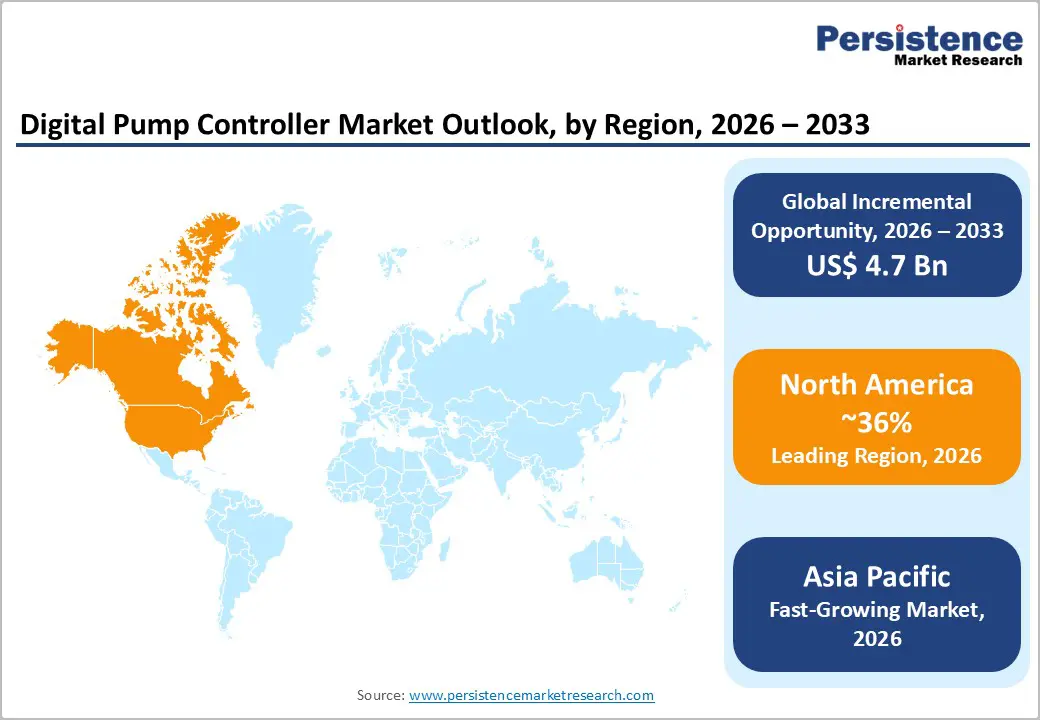

- Dominant Region: North America is expected to dominate with 36% share in 2026, driven by rapid automation adoption across industrial, municipal, and commercial sectors in the U.S. and Canada.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in 2026, propelled by governments, utilities, and industries adopting connected and intelligent pumping solutions to address water scarcity, agricultural demands, and infrastructure modernization.

- Leading Product Type: Variable frequency drive controllers are expected to lead the market, accounting for over 42% share in 2026, as they help pump system operators improve energy efficiency, optimize performance, and reduce operating costs.

- Dominant Pump Type: Centrifugal pump controllers are expected to dominate the market, accounting for around 70% share in 2026, as centrifugal pumps are the most widely used fluid-handling equipment across water management, industrial, and municipal applications.

| Key Insights | Details |

|---|---|

|

Digital Pump Controller Market Size (2026E) |

US$8.9 Bn |

|

Market Value Forecast (2033F) |

US$13.6 Bn |

|

Projected Growth CAGR (2026-2033) |

6.3% |

|

Historical Market Growth (2020-2025) |

6.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Energy Efficiency Regulations and Sustainability Mandates

Governments are tightening minimum energy performance standards and climate commitments, pushing industries to replace fixed-speed pumping with digitally controlled systems that cut electricity use through real-time flow and pressure optimization. The U.S. Department of Energy reports that motor-driven systems consume about 70% of industrial electricity in the U.S., making pumps a prime target for efficiency upgrades; variable speed control can deliver energy savings of 20–50% in suitable pump applications. European Union’s Ecodesign framework sets mandatory efficiency thresholds for water pumps and circulators sold in the EU, raising compliance risk for legacy controllers and accelerating adoption of digital pump controllers that enable precise duty-point control and energy monitoring.

National net-zero roadmaps and mandatory energy audits reinforce demand for digital controllers by linking operational efficiency to compliance reporting and carbon reduction. The U.K. government’s Energy Savings Opportunity Scheme requires large enterprises to assess energy use every four years, with pumping systems identified as high-impact assets for savings actions. India’s Bureau of Energy Efficiency mandates energy management practices under the Perform, Achieve, and Trade scheme, driving industrial retrofits in water, process, and HVAC services where digital pump controllers enable continuous optimization and verifiable savings.

Smart Water Management Initiatives

Government-led smart water management programs are significantly driving the adoption of digital pump controllers by fostering data-driven water systems that optimize consumption, reduce losses, and enhance service delivery. In India, National initiatives such as the Jal Jeevan Mission (JJM) aim to deliver safe, adequate drinking water to rural households through extensive digital monitoring, including IoT-enabled real-time tracking of supply schemes and integrated management dashboards that strengthen transparency and review systems across the Panchayat, district, state, and national levels. Under JJM, integrated management information systems and mobile portals support real-time review of key water supply parameters, enabling proactive issue resolution and efficient operations. These digital platforms underpin the need for advanced controllers and sensors in distribution networks, encouraging municipalities and utilities to invest in automated pump control and monitoring technologies that enhance precision and reduce wastage.

In urban environments, Smart Cities Mission projects include widespread installation of smart meters and IoT-linked flow and pressure sensors to reduce non-revenue water and support dynamic water balancing. Quantifiable impacts reinforce this trend: pilot smart water metering in Indian cities has shown non-revenue water reductions from around 61% to 14%, demonstrating the effectiveness of digital monitoring in cutting losses and conserving resources. International models such as Singapore’s requirement for smart meter installation in new developments further illustrate how government mandates for real-time data integration support predictive maintenance and leak detection across networks.

Barrier Analysis - High Upfront Integration Costs

High upfront integration costs slow the adoption of digital pump controllers across utilities and industrial sites. Deployment requires controllers, sensors, variable frequency drives, communication gateways, cybersecurity layers, and software licenses. Legacy pumping stations often lack compatible wiring, panels, and protocols, so retrofits demand panel redesign, cabling upgrades, and downtime planning. Engineering surveys, commissioning, and operator training add to capital outlay. Procurement cycles and compliance testing extend project timelines, tying up budgets before performance gains appear.

Budget pressure is sharper for municipal bodies and small operators with aging assets and limited capital envelopes. Financing constraints push phased rollouts, which delay network-wide optimization and reduce early returns from energy savings and leakage control. Integration across mixed vendor equipment raises interoperability work, customization, and validation costs. Spare parts stocking, service contracts, and cybersecurity audits lift the total cost of ownership in year one.

Cybersecurity Vulnerabilities in Connected Systems

Connected digital pump controller systems increase exposure to cybersecurity vulnerabilities as they rely on networked communications, cloud connectivity, and remote access. Data flows between sensors, controllers, and central management platforms can be intercepted or manipulated if encryption, authentication, and secure protocols are not rigorously implemented. Legacy industrial control systems, which were not designed with security in mind, often form part of pumping infrastructure; integrating them with modern IoT networks can create weak points that threat actors may exploit.

The impact of cyber threats on water and utility infrastructure can be severe, potentially causing service disruptions, equipment damage, and compromised water quality. Remote access portals, if inadequately protected, are attractive targets for brute-force or credential-theft attacks. Effective mitigation requires robust firewalls, multi-factor authentication, continuous monitoring, and regular patching to protect connected controllers and endpoints.

Opportunity Analysis - Remote Monitoring Control Segment Expansion

Government programs integrating remote monitoring and control technologies into water management infrastructure are creating substantial opportunities for the digital pump controller market by accelerating demand for connected devices that enable real-time oversight and operational efficiency. Under India’s Jal Jeevan Mission, IoT-based monitoring systems are being deployed across rural water supply schemes, connecting field sensors and controllers to central dashboards so authorities can track service delivery metrics such as flow, pressure, and pump status in real time. These pilots operating in hundreds of villages demonstrate governmental commitment to leveraging remote control solutions to improve the reliability and responsiveness of water distribution services. By embedding telemetry and automated controls into infrastructure, utilities, and local bodies are motivated to procure digital pump controllers that integrate seamlessly with cloud platforms and supervisory systems.

Quantitative examples of the impact of such remote systems reinforce their value: pilot smart water supply monitoring projects under Jal Jeevan Mission cover thousands of rural locations, reflecting scale and policy support for connected water systems. By equipping pumps with connectivity and control interfaces, operators can adjust operations remotely, reduce non-revenue water, and respond swiftly to faults without physical site visits. This expansion of remote monitoring and control capabilities not only improves service outcomes but also generates sustained demand for advanced digital pump controllers across municipal, agricultural, and industrial segments, positioning the segment as a key beneficiary of government-driven digitalization in water management.

Municipalities and Water Utilities Modernization

Municipalities and water utilities worldwide are increasingly investing in modernization efforts to improve service delivery, reduce losses, and meet regulatory and citizen expectations. Aging infrastructure, rising urban populations, and tighter water quality and efficiency standards are prompting utilities to upgrade legacy systems with digital technologies that improve visibility and control over water networks. Digital pump controllers play a crucial role in these modernization programs by enabling automated operation of pumping stations, adaptive speed control based on demand, and integration with supervisory systems for coordinated network management. By replacing manual or analog controls with digital solutions, utilities can optimize energy use, extend equipment life, and respond more quickly to system anomalies such as leaks or pressure fluctuations.

Modernization also involves adopting data-driven practices where real-time metrics from sensors and controllers feed into centralized dashboards and analytics platforms. This supports predictive maintenance planning, reduces unplanned downtime, and helps utilities justify capital investment through measurable performance improvements. As governments and regulators emphasize resilience, sustainability, and accountability, municipalities are prioritizing digital upgrades that deliver quantifiable benefits in efficiency and service consistency. Digital pump controllers, with their ability to interface with IoT networks and automation frameworks, are increasingly viewed as foundational components in the broader modernization of water utility operations.

Category-wise Analysis

Product Type Insights

Variable frequency drive controllers are anticipated to dominate, with over 42% share in 2026, as they directly address key performance and cost priorities for pump system operators. By continuously adjusting motor speed to match real-time demand, VFDs significantly reduce energy consumption compared with fixed-speed or simple on/off controllers. This efficiency helps lower operating costs and reduce mechanical wear, which is especially important for high-usage systems in water utilities, industrial plants, and commercial buildings. VFDs also enable precise control of pressure and flow, improving overall system responsiveness. For example, the wastewater pumping station operated by the city of Columbus, Ohio, U.S., demonstrated the benefits of variable frequency drive controllers after retrofitting three constant-speed influent pumps with VFD-driven systems, achieving roughly a 30% reduction in energy consumption per million gallons pumped compared with the previous fixed-speed configuration.

Remote monitoring control is likely to be the fastest-growing product type, as it enables real-time visibility and management of pump operations across dispersed sites without requiring on-site personnel. By transmitting data on flow, pressure, energy use, and fault conditions to centralized dashboards or mobile apps, these systems allow operators to quickly detect issues, optimize performance, and schedule maintenance before failures occur. Growing adoption of IoT networks, cloud analytics, and cellular connectivity in utilities, agriculture, and industrial facilities further accelerates this trend. Kirloskar Brothers Ltd (KBL) developed an IoT-based solution called KirloSmart that enables users to remotely monitor pump health, operational behavior, and performance data through a cloud-connected portal and mobile app, without needing to physically visit the pump site.

Pump Type Insights

Centrifugal pump controllers are expected to dominate, accounting for 70% in 2026, fueled by the fact that centrifugal pumps themselves represent most of the fluid-handling equipment in water, industrial, and municipal systems. Centrifugal pumps are widely used for general water supply, wastewater handling, irrigation, HVAC, and industrial processes due to their versatile flow handling and simpler design, meaning controllers that optimize their operation are in the highest demand. Centrifugal pump controllers delivering measurable benefits come from Rockwell Automation’s Centrifugal Pump Optimizer solution deployed in industrial settings. The system integrates digital controllers with Variable Frequency Drives (VFDs) to manage up to six centrifugal pumps, adjusting speeds and lead/lag operations for optimal energy use.

Submersible pump controllers represent the fastest-growing segments, widely used in agricultural irrigation, groundwater extraction, and decentralized water supply systems where manual operation is less feasible. These applications benefit significantly from digital control, as controllers can adjust speed, monitor motor health, and protect against dry-run or overload conditions automatically. Growing emphasis on water-efficient agriculture, rising rural electrification, and the deployment of solar-powered submersible systems further accelerate demand for smart controllers that enhance energy performance and reliability. Nelso Technology Pvt. Ltd.’s P403 4G IoT/GSM Mobile Pump Controller, which supports remote control and monitoring of submersible pump sets via a mobile app over 4G networks. This controller allows users to start/stop submersible pumps from a distance, set operational schedules, and receive status updates and protections such as dry-run and power notifications directly on their smartphone, enhancing efficiency and reducing manual intervention in agricultural and water management applications.

Regional Insights

North America Digital Pump Controller Market Trends

North America is expected to dominate, capturing 36% share in 2026, shaped by the strong adoption of automation technologies across industrial, municipal, and commercial sectors. The U.S. and Canada are modernizing aging water treatment and distribution systems, expanding the use of IoT-enabled controllers that offer real-time monitoring, fault alerts, and remote adjustments to improve reliability and reduce operational costs.

Many utilities and manufacturers in the region emphasize energy efficiency and sustainability, driving specifications for advanced controllers that can integrate with SCADA and cloud platforms. North America also benefits from high digital literacy among end users and robust infrastructure investment, which supports ongoing upgrades to connected control systems and predictive maintenance frameworks.

Europe Digital Pump Controller Market Trends

Market growth in Europe is driven by a combination of regulatory emphasis on energy efficiency, sustainability goals, and the ongoing modernization of water infrastructure. Utilities and industrial players are increasingly integrating smart controllers to comply with stringent environmental standards and to reduce operational costs by optimizing pump performance through real-time monitoring and adaptive control. Strong environmental policy frameworks across the European Union encourage the adoption of advanced controllers that support pressure management, leak detection, and remote diagnostics in municipal water networks and industrial facilities.

Germany, France, and the U.K. are among the leading adopters, supported by robust industrial bases and substantial investments in automation technologies that enhance resource efficiency and regulatory compliance. Demand is also growing due to Industry 4.0 initiatives, where connectivity and data analytics are being embedded into manufacturing processes, driving the use of controllers with IoT capabilities that enable predictive maintenance and integration with broader automation systems.

Asia Pacific Digital Pump Controller Market Trends

Asia Pacific is likely to be the fastest-growing region in 2026, propelled by governments, utilities, and industries adopting connected and intelligent pumping solutions to address water scarcity, agricultural demands, and infrastructure modernization. Urbanization and industrial growth in countries such as China, India, Australia, and Southeast Asian nations are driving investment in smart water distribution, irrigation efficiency, and industrial automation, where digital controllers with IoT connectivity and real-time monitoring are increasingly specified. Utilities are integrating pump controllers with SCADA, cloud analytics, and remote telemetry to enhance leak detection, pressure management, and operational oversight across large networks.

Governments in the region are embedding digital tools in smart city frameworks and water utility programs to improve resilience and customer service performance. Digitalization also enables predictive maintenance and energy optimization, reducing downtime and lowering lifecycle costs in both municipal and industrial pumping systems. IoT-enabled pump systems and remote-control technologies are especially prominent as operators seek greater operational transparency and automation in diverse application environments.

Competitive Landscape

The global digital pump controller market is consolidating around automation leaders that offer end-to-end control, drives, software, and lifecycle services. Integrated ecosystems from companies such as Siemens and ABB attract utilities and industries seeking interoperable hardware, secure connectivity, and unified service support across assets. This ecosystem approach concentrates on lowering integration risk, simplifying procurement, and enabling standardized upgrades across fleets of pumps and stations.

Leaders accelerate IoT and cloud R&D to deliver remote monitoring, predictive maintenance, and energy optimization at scale. Compliance with substation and grid communication standards such as IEC 61850 strengthens acceptance in utility environments that demand deterministic, cyber-hardened control. Competitive differentiation also comes from digital services, with subscription analytics supporting condition monitoring, anomaly detection, and performance benchmarking for utilities managing distributed pump networks.

Key Industry Developments:

- In January 2026, Grundfos launched the GENIECON smart pump controller, introducing secure connectivity, real-time performance monitoring, and energy optimization for parallel pumping systems to improve efficiency and uptime.

- In September 2025, ABB launched its Baldor-Reliance SP4 close-coupled pump motor at WEFTEC, held from September 29 to October 1 at McCormick Place in Chicago, Illinois, U.S. The company invited media to visit booth #1243 to see how its engineering team designed the NEMA Super Premium™ (IE4) efficiency motor with a compact footprint.

- In April 2025, CG Pumps launched SmartSENSE, India’s first cordless, float-free automatic water pump controller. The company introduced the system to remove manual wiring and float switches, delivering a truly smart and intelligent water control solution for Indian households.

Companies Covered in Digital Pump Controller Market

- Schneider Electric

- Siemens

- Honeywell International

- ABB

- Johnson Control

- Rockwell Automation

- Mitsubishi Electric

- Franklin Electric

- Xylem

- Fuji Electric

- Grundfos

- KSB SE & Co.

Frequently Asked Questions

The global digital pump controller market is expected to reach US$8.9 billion in 2026.

Rapid automation of water and industrial infrastructure is pushing utilities and plants to adopt digital controllers for energy savings, real-time monitoring, and reduced downtime across pumping systems.

The digital pump controller market is poised to grow at a CAGR at 6.3% in 2026.

Expansion of remote monitoring and cloud-connected control opens new revenue via subscription analytics, predictive maintenance, and fleet-level optimization for utilities and multi-site operators.

Leading players include Schneider Electric, Siemens, Honeywell International, ABB, Johnson Controls, and Rockwell Automation.