- Bulk Chemicals

- Water & Wastewater Treatment Chemicals Market

Water & Wastewater Treatment Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

Water & Wastewater Treatment Chemicals Market by Chemical Type (Coagulants & Flocculants, Corrosion & Scale Inhibitors, Biocides & Disinfectants, pH Adjusters & Stabilizers, Anti‑Foaming Agents, Chelating Agents, Others), Form (Liquid, Powder, Granules), End‑user (Municipal Water and Water Treatment, Chemical & Petrochemical, Food & Beverages, Oil & Gas, Pulp, Healthcare, Other), and Regional Analysis, 2026 - 2033

Water & Wastewater Treatment Chemicals Market Size and Trend Analysis

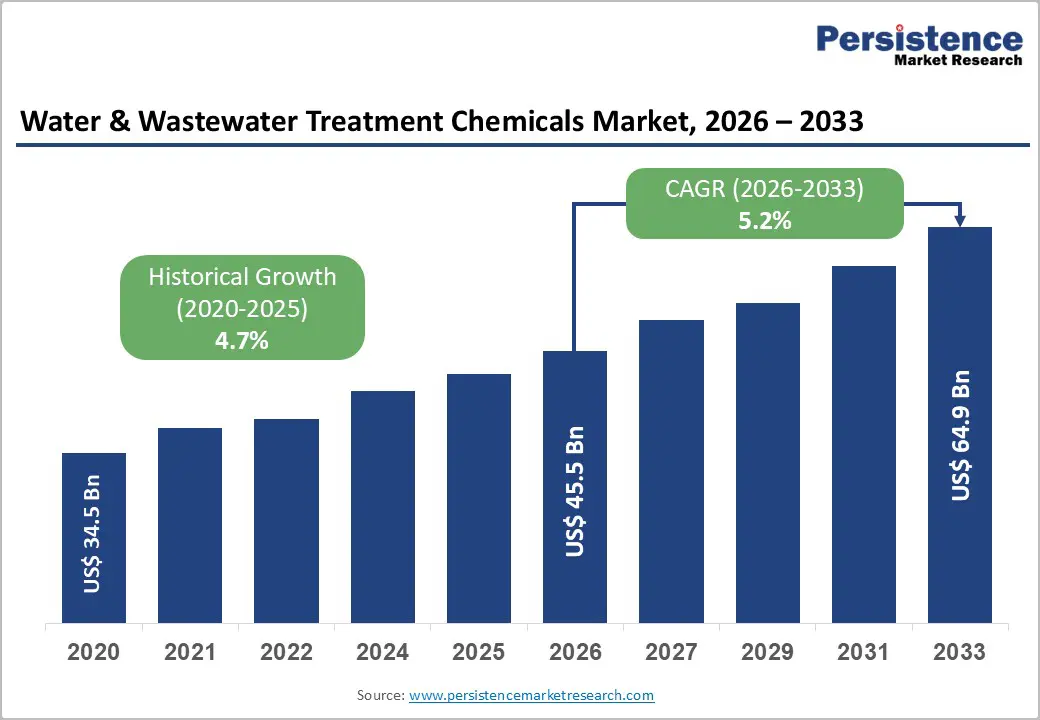

The global water & wastewater treatment chemicals market is projected to reach US$ 45.5 billion in 2026 and is expected to reach US$ 64.9 billion by 2033, growing at a CAGR of 5.2% over the forecast period. This expansion is driven by rising freshwater scarcity, stricter discharge regulations, and increasing investments in municipal and industrial water-treatment infrastructure worldwide.

Key Industry Highlights:

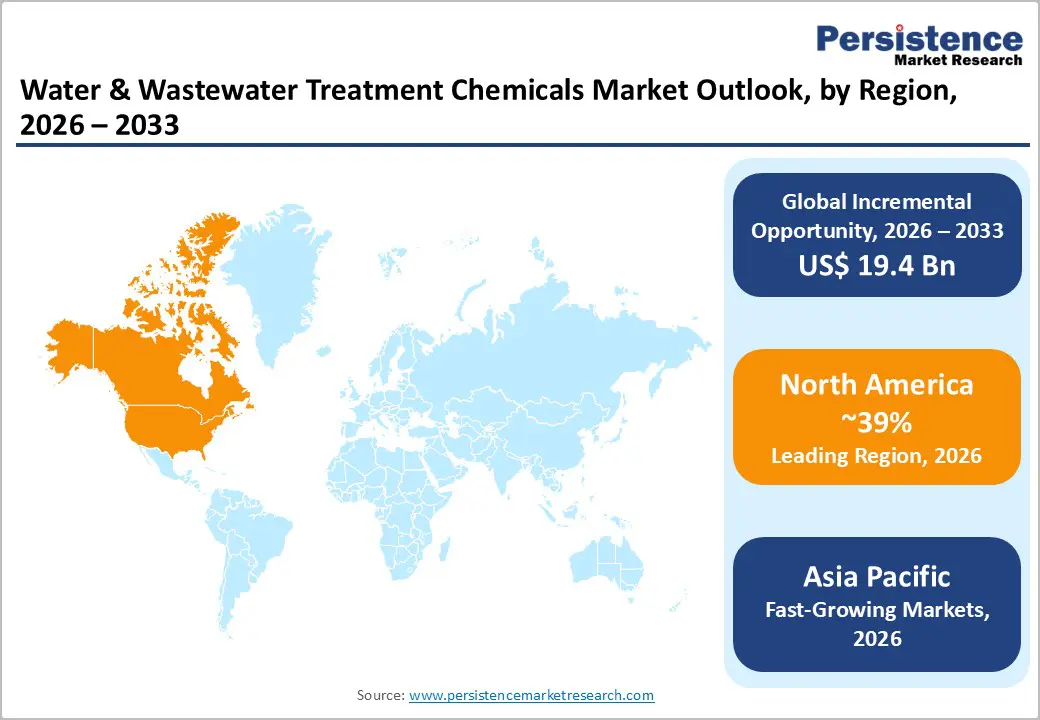

- Leading region: North America leads the Water & Wastewater Treatment Chemicals Market, with a 39% share, owing to stringent environmental regulations, high treatment coverage, and strong adoption of advanced coagulants, biocides, and disinfectants.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 6.7%, driven by rapid industrialization, urbanization, and large-scale investments in municipal and industrial wastewater-treatment infrastructure.

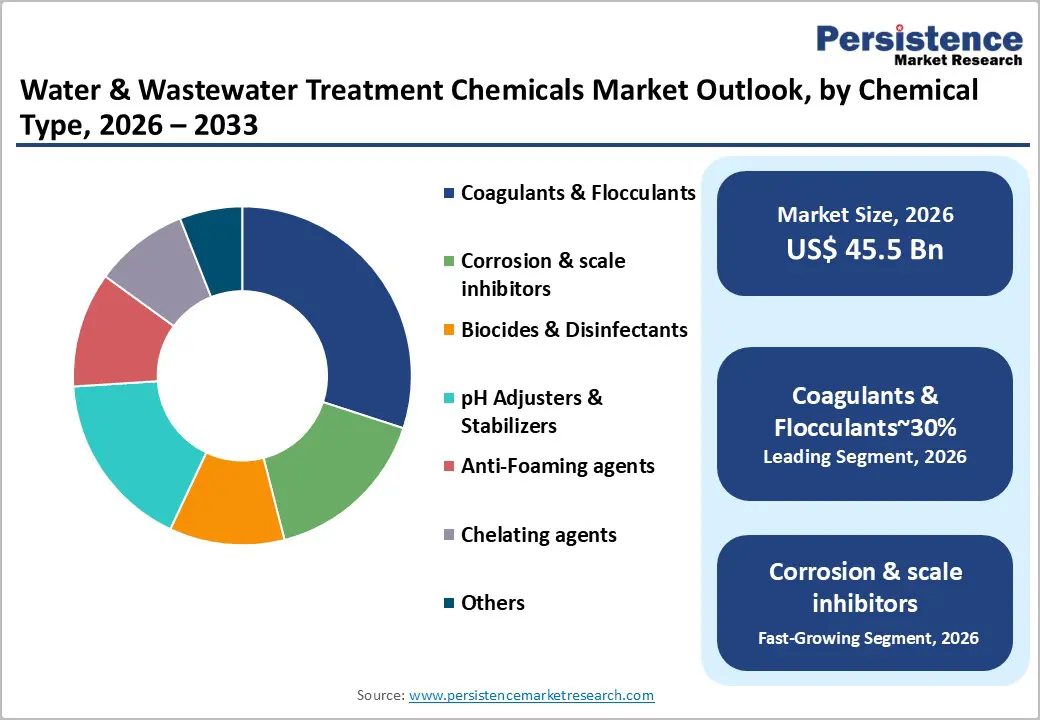

- Dominant Chemical Type: The Coagulants & Flocculants segment within Chemical Type is the dominant segment, holding 30 % share in the market revenue, supported by their essential role in removing suspended solids and turbidity in municipal and industrial effluents.

- Fastest Growing Chemical Type: The Biocides & Disinfectants segment within Chemical Type is one of the fastest-growing, as stricter pathogen-control regulations and rising biofouling concerns increase demand for advanced disinfection chemicals.

- Key Opportunity: The expansion of zero-liquid-discharge (ZLD) and industrial water-reuse schemes presents a major opportunity, particularly in chemical & petrochemical, power, and mining sectors that require high-performance treatment chemicals to meet reuse and discharge standards.

| Key Insights | Details |

|---|---|

|

Water & Wastewater Treatment Chemicals Market Size (2026E) |

US$ 45.5 Billion |

|

Market Value Forecast (2033F) |

US$ 64.9 Billion |

|

Projected Growth CAGR (2026–2033) |

5.2% |

|

Historical Market Growth (2020–2025) |

4.7% |

Market Dynamics

Drivers - Tightening global water pollution regulations are driving increased adoption of advanced wastewater treatment chemicals across industries and municipalities

Stricter environmental regulations on industrial and municipal wastewater discharge are a major growth driver for the Water & Wastewater Treatment Chemicals Market. Regulatory authorities such as the U.S. Environmental Protection Agency (EPA), the European Environment Agency (EEA), and national water quality bodies have significantly reduced allowable limits for pollutants, nutrients, and heavy metals. This has pushed treatment facilities and industries to adopt advanced coagulants, flocculants, disinfectants, and specialty chemicals to meet compliance standards.

The EU Water Framework Directive and the Industrial Emissions Directive require continuous improvements in wastewater quality, resulting in higher chemical use per treatment plant. Similarly, China’s Water Pollution Prevention and Control Action Plan has implemented stricter discharge standards across industrial parks and municipal systems, increasing the demand for high-performance treatment chemicals. As regulations become more demanding worldwide, the reliance on chemical-based treatment solutions continues to grow steadily.

Rapid industrial growth in emerging economies is significantly increasing wastewater generation and demand for treatment chemicals

Rapid industrial growth across the Asia Pacific, Latin America, and Africa is generating large volumes of wastewater that require proper treatment before disposal or reuse. Industries such as chemicals, oil and gas, pulp and paper, food and beverages, and power generation generate complex effluents that contain suspended solids, contaminants, and biological matter. These sectors depend heavily on coagulants, corrosion inhibitors, biocides, and scale-control chemicals to maintain water quality and comply with environmental regulations.

Data from global organizations, including the International Energy Agency (IEA) and World Bank, indicate that industrial water usage is rising faster than population growth, directly increasing chemical demand. At the same time, industries are adopting water reuse and zero-liquid-discharge systems to reduce freshwater consumption, which require multiple chemical treatment stages. This trend is significantly increasing the global consumption of specialized water treatment chemicals.

Restraints - Fluctuating raw material costs and supply disruptions are creating pricing pressure for water treatment chemical manufacturers

The Water & Wastewater Treatment Chemicals Market is highly affected by fluctuations in raw-material prices, including aluminum compounds, chlorine derivatives, polyacrylamides, and phosphates, which are linked to the petrochemical and mining industries. Changes in energy costs, geopolitical tensions, trade restrictions, and transportation disruptions often lead to price volatility and supply shortages. These challenges can reduce profit margins for major manufacturers such as Kemira, Ecolab, and DuPont, particularly in Europe and North America.

In some regions, sudden shortages force treatment plants to switch products or reduce chemical dosages, which can temporarily slow market growth. In addition, strict environmental and safety regulations related to chemical manufacturing, storage, and transport increase compliance costs for suppliers. Smaller regional players often struggle with these rising costs, limiting their ability to compete effectively and restraining overall market expansion.

Infrastructure gaps and limited technical capacity in developing regions are slowing advanced chemical adoption

In many developing regions, outdated infrastructure, limited technical expertise, and inconsistent electricity supply reduce the efficiency of modern wastewater treatment operations. Municipal utilities across parts of South Asia, Africa, and Latin America often operate old treatment plants that are not designed for advanced chemical processes. This results in poor dosing control, higher chemical consumption, and inconsistent treatment performance. The lack of automation and real-time monitoring further reduces the effectiveness of high-performance treatment chemicals.

Budget constraints limit investment in modern equipment and in training for the skilled workforce. As a result, many utilities prefer low-cost traditional chemicals over premium specialty products. These operational challenges impede the adoption of advanced treatment solutions, such as smart dosing systems and high-efficiency biocides, thereby limiting revenue growth opportunities for global chemical suppliers in emerging markets.

Opportunity - Rising industrial focus on water reuse and ZLD systems is expanding demand for specialty treatment chemicals

The increasing focus on water conservation and sustainability is driving strong demand for zero-liquid-discharge (ZLD) and industrial water reuse systems. Industries such as power generation, chemicals, textiles, mining, and oil refining are adopting closed-loop water management to reduce freshwater consumption and environmental impact. These systems require extensive use of coagulants, flocculants, scale inhibitors, and biocides to manage solids, prevent equipment scaling, and control biological fouling. Countries including China, India, and Saudi Arabia are implementing stricter water reuse mandates in industrial zones, accelerating investment in advanced treatment processes.

Companies such as Veolia, SUEZ, and Xylem provide customized chemical solutions to support complex ZLD operations. As water scarcity becomes a global concern, industries are expected to intensify reuse efforts, significantly increasing long-term demand for specialty treatment chemicals.

Urban population growth is accelerating municipal wastewater infrastructure investments and chemical consumption

Rapid urban population growth in Asia Pacific, Africa, and Latin America is driving massive investments in municipal wastewater treatment infrastructure. Cities such as Delhi, Mumbai, Jakarta, and Lagos are expanding sewage treatment capacity to manage rising domestic wastewater volumes. Many of these projects receive funding from international institutions such as the World Bank and the Asian Development Bank, thereby supporting long-term development. Modern plants increasingly include tertiary treatment and advanced disinfection processes to meet stricter environmental and reuse standards.

This directly increases demand for high-performance coagulants, disinfectants, pH adjusters, and specialty chemicals. Municipalities are promoting treated wastewater reuse for irrigation, industrial supply, and groundwater recharge. This creates continuous chemical consumption throughout the treatment lifecycle. As urbanization continues, municipal utilities will remain one of the most reliable and high-volume customers for treatment chemical suppliers.

Category-wise Analysis

Chemical Type Insights

Coagulants and flocculants represent the largest segment within the Water & Wastewater Treatment Chemicals Market, accounting for nearly 30% of total volume consumption. These chemicals play a vital role in removing suspended solids, turbidity, and fine particles by neutralising electrical charges and forming larger settleable flocs. Aluminium-based coagulants such as alum and polyaluminum chloride are widely used alongside synthetic and natural flocculants in both municipal and industrial treatment systems.

They are essential in primary and secondary clarification processes, ensuring efficient contaminant removal at relatively low cost. According to public-sector water authorities and global health organisations, coagulation-flocculation remains one of the most effective and cost-effective treatment steps for large-scale water processing. Their proven reliability, wide availability, and cost efficiency continue to support strong market demand across developed and emerging regions.

Form Insights

Liquid treatment chemicals dominate the market, holding approximately 55% of total consumption due to their operational convenience and superior performance in automated systems. Liquid formulations dissolve quickly in water, ensuring faster reaction times and more precise dosing compared to solid alternatives. Municipal treatment plants and large industrial facilities increasingly prefer liquid coagulants, disinfectants, corrosion inhibitors, and specialty chemicals supplied in bulk. These products integrate easily with digital metering systems, improving process control and reducing handling risks for workers.

Industry associations such as the Water Environmen t Federation and American Water Works Association highlight that liquid chemicals are particularly favored in high-volume continuous operations. Their ease of storage, reduced preparation time, and improved safety profile make them the preferred choice in regions with advanced infrastructure, especially in North America and Europe, driving sustained market growth.

End-user Insights

Municipal water and wastewater utilities constitute the largest end-user segment, accounting for nearly 50% of total market demand. This dominance is driven by the continuous need to treat large volumes of domestic sewage and drinking water to meet public health and environmental standards. Developed regions such as North America and Europe treat over 80% of collected wastewater, requiring consistent use of coagulants, disinfectants, and specialty treatment chemicals.

In emerging economies, government-led infrastructure expansion is rapidly increasing sewage treatment coverage, further boosting chemical consumption. Municipal plants rely heavily on long-term chemical supply contracts, which provide stable revenue for suppliers such as Veolia, SUEZ, and ACCIONA worldwide. As urban populations continue to grow and regulations become stricter, municipal utilities will remain the backbone of demand within the global treatment chemicals market.

Regional Insights

North America Water & Wastewater Treatment Chemicals Market Trends

North America represents a mature and highly regulated market driven by advanced infrastructure and strict environmental standards. In the United States, regulations such as the Clean Water Act and Safe Drinking Water Act enforce tight control over contaminants and pathogens, ensuring continuous demand for high-performance treatment chemicals. Over 90% of municipal wastewater is treated before discharge, creating a strong and stable base for chemical consumption. Industries also invest heavily in water recycling and compliance systems, further increasing demand for specialty chemicals.

Major companies including Ecolab, DuPont, and Xylem are leading innovation through digital dosing technologies and predictive monitoring solutions. These advancements help utilities optimize chemical usage while reducing operational costs. As sustainability and efficiency become key priorities, North America continues to serve as a technology-driven hub for water treatment chemical development.

Europe Water & Wastewater Treatment Chemicals Market Trends

Europe’s market is largely driven by strong environmental policies and harmonized regulatory standards across member states. Countries such as Germany, the United Kingdom, France, and Spain lead in adopting advanced wastewater treatment technologies and high-efficiency chemicals. EU directives including the Urban Wastewater Treatment Directive and Water Framework Directive require higher treatment levels, nutrient removal, and improved effluent quality. This has increased per-capita chemical consumption across municipal and industrial facilities.

Many utilities have upgraded systems to address emerging pollutants and stricter discharge limits using advanced chemical-based processes. In addition, chemical suppliers must comply with EU safety frameworks such as REACH, encouraging the development of eco-efficient and low-toxicity products. Companies like Kemira, Veolia, and SUEZ worldwide are well positioned to meet these evolving standards, driving steady market growth.

Asia Pacific Water & Wastewater Treatment Chemicals Market Trends

Asia-Pacific is the fastest-growing regional market, driven by rapid industrialization, urban expansion, and government investment in water infrastructure. China has strengthened environmental enforcement through its Water Pollution Prevention and Control Action Plan, pushing industries and municipalities to adopt advanced treatment chemicals. India is significantly expanding sewage treatment under national programs such as Namami Gange and AMRUT, increasing chemical consumption across urban centers.

Southeast Asian countries, including Indonesia, Vietnam, and Thailand, are developing new industrial zones that require integrated water management systems. These developments are driving strong demand for coagulants, disinfectants, and specialty chemicals. Global players such as Gradiant Corporation, Pentair, and Hydro International are actively expanding operations in the region. With rising environmental awareness and infrastructure development, Asia Pacific region remains the key growth engine of the global market.

Competitive Landscape

The global water & wastewater treatment chemicals market is moderately consolidated, with a combination of global chemical producers, water technology firms, and regional distributors competing across segments. Major companies, including Veolia, SUEZ worldwide, DuPont, Xylem, Kemira, Evoqua, Ecolab, Pentair, ACCIONA, Gradiant Corporation, Trojan Technologies, Hydro International, BioMicrobics, and Rinnai, collectively hold a substantial market share.

These players focus on expanding into high-growth regions such as the Asia Pacific and Latin America while strengthening partnerships with engineering and infrastructure firms. Many companies are offering integrated solutions that combine chemicals, equipment, and digital monitoring platforms. Competitive differentiation increasingly depends on sustainability-focused products, optimized dosing technologies, and customized treatment programs. As environmental regulations tighten and water reuse expands, companies that provide efficient, eco-friendly, and data-driven solutions are expected to gain long-term market leadership.

Key Developments:

- In February 2025, Ecolab introduced a new non-oxidizing biocide solution for cooling-tower and membrane applications, helping industrial customers in North America and Europe reduce biofouling, cut chemical usage, and improve system efficiency.

- In September 2024, Kemira announced expanded coagulant production capacity in Europe, aiming to support stricter wastewater treatment standards under EU regulations and growing demand from municipal utilities for higher-performance chemicals.

- In March 2024, Xylem formed a strategic partnership with a leading Indian municipal utility to deploy integrated chemical-and-equipment water-treatment and reuse solutions for sewage management projects across South Asia.

Companies Covered in Water & Wastewater Treatment Chemicals Market

- Veolia

- SUEZ worldwide

- DuPont

- Xylem

- Kemira

- Evoqua Water Technologies LLC

- Gradiant Corporation

- Trojan Technologies Group ULC.

- Hydro International Ltd.

- ACCIONA

- Pentair

- Ecolab

- BioMicrobics, Inc.

- Kurita Water Industries Ltd.

- Solenis LLC

- BASF SE

- AkzoNobel N.V.

- Suez Water Technologies & Solutions

Frequently Asked Questions

The Water & Wastewater Treatment Chemicals Market is projected to reach US$ 64.9 Billion by 2033, growing at a CAGR of 5.2% from 2026 to 2033, driven by stricter regulations, rising industrialization, and expanding municipal wastewater‑treatment infrastructure.

Key demand drivers include rising freshwater scarcity, stricter effluent discharge regulations, increasing industrialization, and expanding municipal wastewater‑treatment coverage, which together boost consumption of coagulants, flocculants, biocides, and corrosion inhibitors.

The coagulants & flocculants segment dominates the Water & Wastewater Treatment Chemicals Market by chemical type, accounting for about 30% of the market due to their essential role in removing suspended solids and turbidity in municipal and industrial effluents.

North America leads the Water & Wastewater Treatment Chemicals Market, supported by stringent EU water‑quality directives, high treatment coverage, and strong adoption of advanced coagulants, biocides, and disinfectants.

A key growth opportunity lies in zero‑liquid‑discharge (ZLD) and industrial water‑reuse schemes, which require high‑performance treatment chemicals to meet reuse and discharge standards in sectors such as chemical & petrochemical, power, and mining.