- Specialty & Fine Chemicals

- Car Wax Market

Car Wax Market Size, Share, and Growth Forecast, 2026 – 2033

Car Wax Market by Product Type (Paste Wax, Liquid Wax, Spray Wax, Gel Wax), Formulation (Natural Wax, Synthetic Wax, Hybrid Wax), End-User (Individual Consumers, Automotive Service Providers, Fleet Operators), and Regional Analysis for 2026-2033

Car Wax Market Share and Trends Analysis

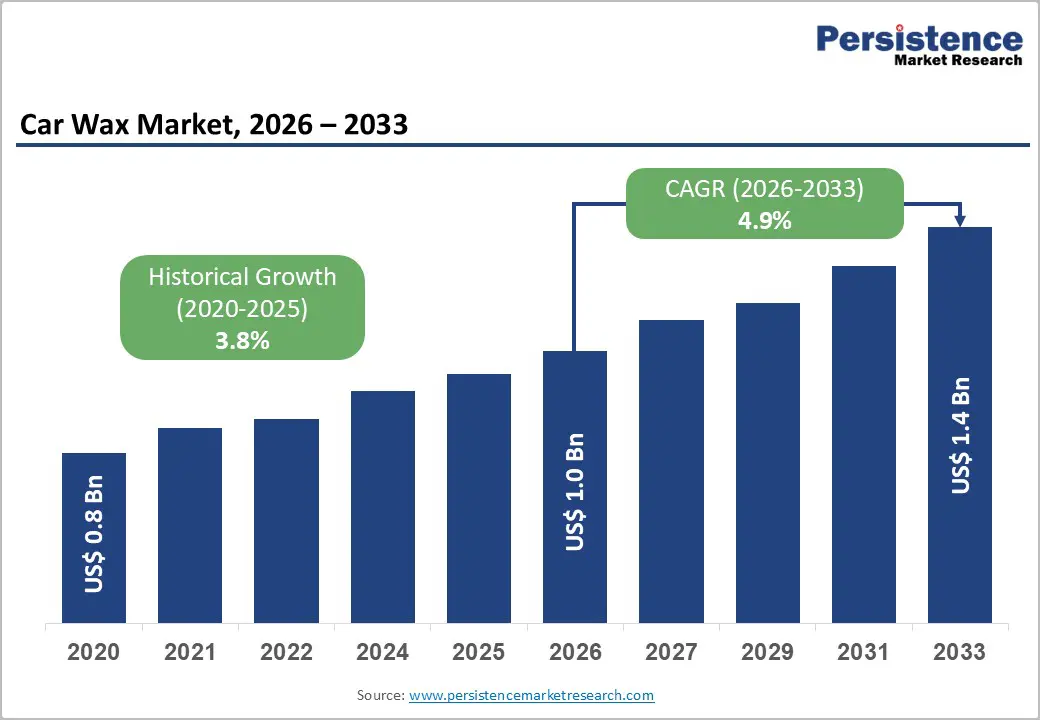

The global car wax market size is likely to be valued at US$ 1.0 billion in 2026, and is projected to reach US$ 1.4 billion by 2033, growing at a CAGR of 4.9% during the forecast period 2026−2033. Sustained expansion is expected due to convergence of automotive ownership growth, surface-protection awareness, maintenance culture, digital retail integration, and service-industry professionalization. Rising vehicle parc across urban regions increases demand for protective coatings that reduce paint degradation caused by ultraviolet radiation, airborne contaminants, and moisture exposure. Greater consumer knowledge regarding preventive vehicle care strengthens routine application frequency.

Expansion of detailing services enhances accessibility of specialized formulations designed for durability and gloss retention. Integration of advanced polymer chemistry improves performance characteristics, supporting higher perceived value. Strengthening automotive aftercare infrastructure across emerging economies expands distribution channels, which broadens product availability and stabilizes supply networks.

Key Industry Highlights

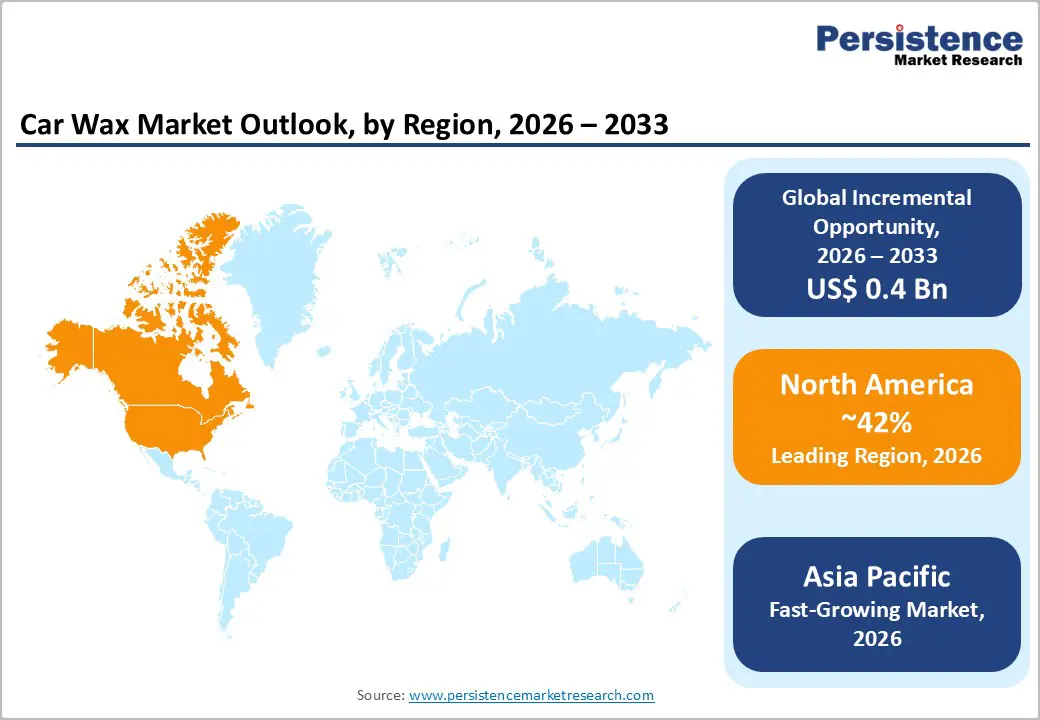

- Dominant Region: By 2026, North America is projected to hold 42% market share, driven by high vehicle ownership, strong aftermarket culture, and premium product adoption.

- Fastest-growing Market: Asia Pacific is poised to be the fastest-growing market from 2026 to 2033, fueled by expanding e-commerce and exploding demand for premium, eco-friendly formulations.

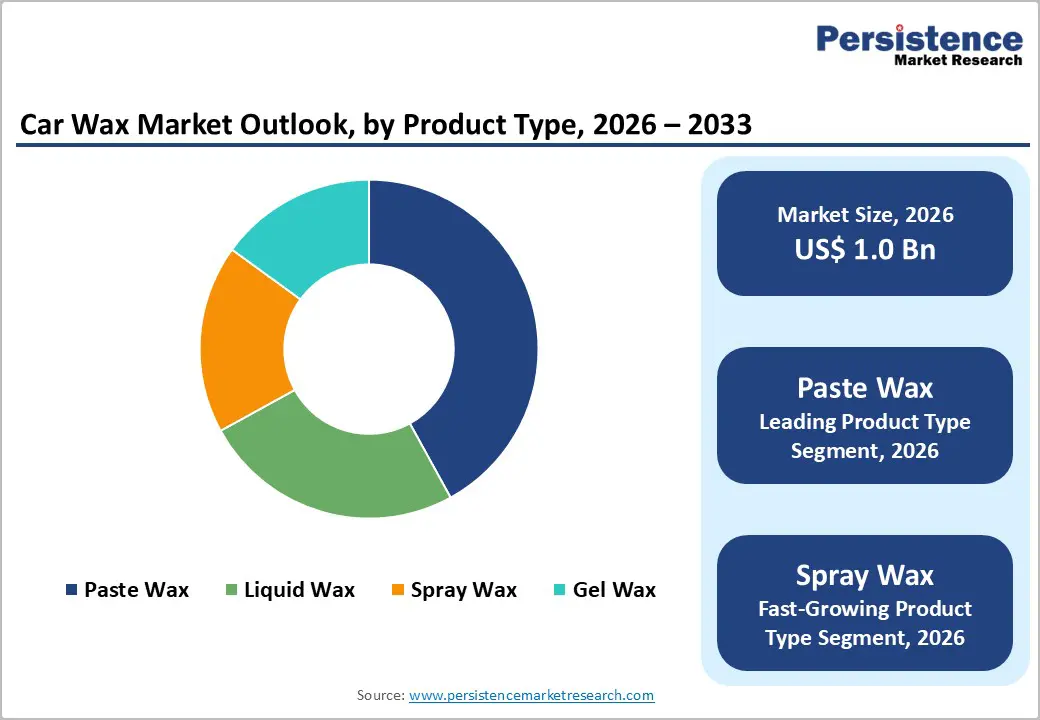

- Leading Product Type: Paste wax is expected to lead with nearly 42% revenue share in 2026, owing to durability, professional preference, and ease of application.

- Fastest-growing Product Type: Spray wax is likely to grow the fastest between 2026 and 2033, driven by convenience, time efficiency, and advanced formulations.

- July 2025: Nippon Paint rolled out its N-Shield paint protection film (PPF) range in India, aiming to strengthen its position in the automotive surface protection segment through advanced durability, self-healing properties, and an expanded installer network.

| Key Insights | Details |

|---|---|

|

Car Wax Market Size (2026E) |

US$ 1.0 Bn |

|

Market Value Forecast (2033F) |

US$ 1.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancement in Surface-Protection Chemistry

Advanced surface-protection chemistry transforms vehicle finish maintenance from routine polishing into performance-driven preservation. Nano-scale polymers, ceramic hybrids, and cross-linking resins form dense molecular lattices that resist oxidation, micro-scratches, and chemical contaminants. Such technical progress raises durability expectations across detailing networks, fleet operators, and certified service centers. A measurable expansion in vehicle population strengthens this demand base. Official data show 56.75 lakh registered electric vehicles (EVs) in India as of February 2025, reflecting rapid mobility expansion documented through government statistics. Higher volumes of technologically advanced vehicles create larger addressable surface area requiring protective treatment aligned with modern paint systems and composite body materials.

Scientific refinement of coating chemistry drives premiumization across aftermarket maintenance categories. Functional additives such as silane modifiers and fluoropolymer dispersions enhance gloss retention, hydrophobic performance, and thermal tolerance, enabling differentiation through quantifiable protection metrics rather than visual appeal alone. Regulatory focus on environmental durability and lifecycle efficiency encourages adoption of formulations engineered for longer service intervals and reduced material waste. Automotive manufacturers integrate advanced paint technologies with thinner clear-coat layers to reduce weight, elevating need for high-precision protective compounds compatible with delicate finishes.

Expansion of Global Vehicle Ownership and Usage Intensity

Rising vehicle parc volume and higher utilization cycles directly strengthen demand for surface-care products through accelerated paint degradation, oxidation, and contamination exposure. Greater commuting distance, urban congestion, and outdoor parking density intensify contact with ultraviolet radiation, particulate matter, acid deposition, and road salt, which increases coating wear frequency and raises maintenance cycles across private and commercial fleets. Protective detailing solutions gain operational relevance in such conditions since preservation of exterior finish supports residual value, fleet branding standards, and consumer perception of asset quality. A government statistical release from the Statistical Service of Cyprus reported 52,508 motor-vehicle registrations during January–December 2025, representing a 5.8% annual increase, indicating continued expansion of active vehicle base requiring routine appearance maintenance.

Intensive usage patterns amplify lifecycle exposure to mechanical abrasion from dust friction, automatic washing systems, and micro-scratches generated during daily driving. Fleet operators, ride-hailing providers, and logistics companies prioritize finish protection to reduce repaint frequency and maintain standardized visual condition across high-rotation assets. Consumer preference for aesthetic preservation aligns with resale-value optimization, especially within pre-owned vehicle channels where exterior condition strongly influences pricing benchmarks. Urbanization trends elevate parking density and environmental pollutant concentration, accelerating surface dullness and staining, which reinforces recurring purchase cycles for protective coatings and polishing formulations. Growth in electrified mobility further contributes to this dynamic through increased ownership diversification and broader participation across income segments, expanding total addressable user base for exterior-care solutions.

Competition from Alternative Paint-Protection Technologies

The rise of advanced coating systems and protective films is shifting consumer and original equipment manufacturer (OEM) focus toward longer lived paint preservation solutions with less frequent maintenance. Ceramic nano coatings chemically bond at the surface level and can deliver multi year protection with high resistance to ultraviolet (UV) degradation, bird droppings, acid rain and abrasion, making them technically superior to traditional surface polish products that wear off quickly. This technical distinction has driven increased adoption as owners of high value vehicles seek durable protection that aligns with resale value preservation strategies and reduced maintenance intervals. Government research in materials science highlights that these advanced coatings form hard, covalent networks on clear coats that resist environmental stressors more effectively than conventional polymer based barrier layers.

Consumer expectations are evolving toward higher performance, low maintenance protection rather than frequent reapplication of conventional protectants. Government led standards and environmental regulations continue to promote safer, longer lasting coating chemistries, influencing product development and professional service offerings. The capability of alternative coatings to deliver hydrophobic performance, enhanced gloss retention and extended durability extends the interval between professional maintenance cycles, putting pressure on the repeat use model of traditional protective applications.

Environmental and Regulatory Compliance Pressures

Stringent environmental and regulatory compliance requirements are increasing cost and operational pressures on manufacturers by imposing limits on volatile organic compounds (VOCs) and other chemical emissions in surface coatings and related automotive products. In the United States, the Environmental Protection Agency (EPA) finalized National VOC Emission Standards for aerosol coatings with updated reactivity based limits that take effect in 2025, requiring reformulation of products to meet stricter emissions criteria and enhanced reporting obligations such as electronic compliance documentation. These standards aim to reduce ground level ozone and other pollutants, and companies must adjust formulation chemistry, testing procedures, and manufacturing processes to remain compliant. Reformulation efforts often increase research and development expenditures and production costs as manufacturers balance performance with allowable VOC thresholds.

Meeting diverse regulatory frameworks across jurisdictions further complicates compliance strategy. Regulatory regimes such as the Clean Air Act’s performance and hazardous air pollutant standards compel manufacturers to limit emissions of specific compounds and adopt control technologies, raising capital intensity for compliance infrastructure. Global variations in chemical restrictions and reporting requirements can delay product launches and necessitate multiple formulation variants for different markets. Manufacturers also face penalties or delayed market entry if products fail to satisfy certification or labeling rules, which in turn can strain supply chains and reduce responsiveness to demand fluctuations. Government driven VOC limits directly translate into higher unit costs and operational complexity, constraining investment in other value creating initiatives and slowing growth in segments more exposed to regulatory scrutiny.

Development of Eco-Friendly and Multifunctional Formulations

Shifting regulatory frameworks and evolving consumer preferences create a strategic opportunity for eco-friendly and multifunctional formulations. Governments worldwide are implementing stricter standards on VOCs and hazardous chemicals in surface care products, prompting manufacturers to explore greener chemistries that reduce environmental impact while maintaining performance. Programs such as the EPA Safer Choice label guide businesses and buyers toward safer chemical profiles, increasing demand for formulations that align with sustainability and health considerations. Biodegradable ingredients, reduced toxic inputs, and environmentally compatible processes strengthen market positioning by lowering compliance risk and appealing to eco-conscious consumers.

Consumer behavior also drives demand for multifunctional solutions that simplify vehicle care and enhance perceived value. Products combining protective performance with convenience, such as polish-sealant blends or waterless protectants, meet expectations for efficiency and effectiveness. These formats support premium pricing, reduce distribution complexity, and cater to both DIY enthusiasts and professional detailers seeking comprehensive solutions. Innovations in formulation science that deliver extended protection, hydrophobic performance, and environmental compatibility align closely with regulatory incentives and buyer priorities, providing companies an avenue to differentiate offerings and capture growth in a competitive landscape.

Expansion across Burgeoning Automotive Markets

Emerging automotive markets are driving significant demand growth and widening geographic sales channels, supported by rapid vehicle adoption and progressive public policy. Rising personal income and expanding urbanization in regions such as Southeast Asia, Latin America, and Africa are increasing vehicle ownership rates, creating new avenues for aftermarket products. Growing consumer awareness of vehicle maintenance and aesthetic care is shaping purchasing behavior, encouraging uptake of protective coatings and surface care solutions. Localized manufacturing and distribution networks are also enabling companies to meet diverse regulatory environments and price sensitivities while maintaining operational efficiency.

Government incentives promoting cleaner vehicles and improved transport infrastructure are accelerating market potential in these regions. Policies including tax reductions, import duty adjustments, and investment in public transport networks lower barriers to vehicle acquisition, supporting broader adoption of passenger and commercial vehicles. Automotive manufacturers are strategically diversifying operations to capture incremental demand and mitigate exposure to slower-growing mature markets. Expansion of production capacity and regional supply chains aligns with evolving consumer needs, ensuring timely availability of vehicle care solutions. Integration of these factors is fostering structural opportunities for sustained growth across emerging economies.

Category-wise Analysis

Product Type Insights

Paste wax is likely to be the leading segment with approximately 42% of the car wax market revenue share in 2026, due to durability advantages, professional preference, and established consumer familiarity. Paste formulations deliver thicker protective layers that resist environmental contaminants and ultraviolet exposure. Automotive detailing professionals prefer paste variants because consistency allows controlled application and buffing, which produces uniform surface finish. Training programs within detailing institutes often emphasize paste usage techniques, reinforcing practitioner familiarity. Retail availability across automotive accessory stores increases accessibility for individual consumers seeking long-lasting protection. Traditional perception associating paste wax with premium finish quality sustains adoption across enthusiast communities. Product stability during storage supports inventory management for distributors and service providers.

Spray wax is expected to witness the fastest growth between 2026 and 2033, as convenience, time efficiency, and technological formulation improvements support broader adoption. Spray formats simplify application processes, reducing labor time and physical effort. Individual users benefit from quick-application properties suitable for routine maintenance, encouraging frequent usage. Professional detailing providers integrate spray wax as a finishing layer following washing or polishing, improving service throughput. Advances in emulsion chemistry enable spray formulations to deliver protective performance approaching traditional wax types. Online retail platforms highlight ease-of-use demonstrations, strengthening consumer confidence.

End-User Insights

Individual consumers is positioned to dominate with nearly 70% market share in 2026, supported by widespread vehicle ownership, accessibility of retail channels, and preventive maintenance awareness. Personal vehicle owners represent a broad addressable base. Retail availability across automotive accessory stores, supermarkets, and online platforms enables convenient procurement. Educational campaigns conducted by transportation authorities and automotive associations emphasize importance of exterior maintenance, strengthening consumer motivation. Cost efficiency of do-it-yourself application compared with professional detailing services encourages adoption. Product packaging innovations including applicator kits and instructional guides enhance usability for non-professional users.

Fleet operators is expected to emerge as the fastest-growing segment between 2026 and 2033, driven by asset preservation priorities, digitalization of maintenance management, and cost-optimization strategies. Commercial fleets require systematic maintenance protocols to preserve vehicle value and corporate brand image. Digital fleet-management systems schedule routine surface protection treatments, ensuring consistent upkeep. Logistics, transportation, and mobility service providers implement preventive care programs to minimize refurbishment expenses. Bulk procurement contracts with suppliers enable cost savings, encouraging regular usage. Integration of automated washing and waxing equipment within fleet depots increases efficiency and reduces labor requirements.

Regional Insights

North America Car Wax Market Trends

North America is expected to lead with an estimated 42% of the car wax market share in 2026, on the back of high vehicle ownership rates that sustain demand for maintenance products. Strong aftermarket culture in the region drives consumer preference for protective and aesthetic enhancements, reinforcing recurring purchase patterns. Well-established distribution networks, including specialty automotive retailers and e-commerce platforms, ensure product availability across urban and suburban areas. Premiumization trends further strengthen adoption, as consumers increasingly select advanced formulations offering long-lasting protection, water repellency, and surface shine. Regulatory emphasis on vehicle safety and environmental standards indirectly encourages use of high-quality coatings designed to preserve vehicle condition over time.

Automotive fleet growth and luxury vehicle penetration contribute additional support for market dominance. Corporate fleets, rental services, and ride-sharing operations maintain regular surface care routines, generating stable commercial demand. Consumer education campaigns and marketing initiatives highlighting benefits of advanced coatings reinforce product preference, particularly among high-income segments. Research and development investment by key players in durable, environmentally friendly formulations enhances differentiation and retention. Strategic partnerships with service centers and auto detailing networks further consolidate presence, creating a structural advantage in both volume and premium segments.

Europe Car Wax Market Trends

Europe exhibits a mature market for car wax solutions, characterized by high consumer awareness and well-established automotive culture. Premium vehicle ownership is significant across countries such as Germany, France, and Italy, driving consistent demand for protective and aesthetic maintenance products. Consumers demonstrate strong preference for advanced formulations, including synthetic polymers, ceramic coatings, and eco-friendly variants that align with environmental regulations and sustainability standards. Well-developed distribution networks, spanning specialty retailers, automotive service centers, and online platforms, ensure widespread product availability and facilitate repeat purchases.

Fleet operations, including commercial logistics, car rental services, and corporate vehicles, contribute to recurring demand, reinforcing market stability. Marketing initiatives emphasizing long-term cost savings, surface protection, and resale value strengthen consumer engagement and drive adoption of premium coatings. Investment in R&D has resulted in formulations that resist extreme weather conditions, UV exposure, and corrosion, catering to regional climatic variations. Collaborative initiatives between manufacturers and auto detailing networks enhance service penetration and brand visibility, ensuring products reach both urban and suburban areas efficiently.

Asia Pacific Car Wax Market Trends

Asia Pacific is forecasted to be the fastest-growing market for car wax between 2026 and 2033, stimulated by rapid urbanization and rising disposable income that drive vehicle acquisition across both personal and commercial segments. The regional market is witnessing significant growth in mid-size and compact vehicle ownership, particularly in India, China, and Southeast Asian economies, which increases demand for aftermarket maintenance products. Expanding e-commerce penetration and modern retail infrastructure enhance product accessibility, enabling small and medium enterprises to reach a wider consumer base. Preference for advanced formulations offering long-lasting protection and environmental compliance supports premiumization trends.

Government initiatives promoting cleaner transport and vehicle longevity indirectly boost demand for protective coatings. Rising fleet operations, including taxis, logistics, and ride-sharing services, create recurring commercial demand for surface maintenance products. Regional automotive culture is evolving, with consumers increasingly prioritizing aesthetics, performance, and vehicle resale value, fueling repeat purchases. Investments in R&D for heat-resistant and water-repellent formulations tailored to tropical and humid climates further enhance market potential.

Competitive Landscape

The global car wax market exhibits a moderately fragmented structure, encompassing multinational chemical manufacturers, specialized automotive care companies, and regional niche brands. Key players such as Henkel, Turtle Wax, Mothers Polishes Wax Cleaners, and Darent Wax Company maintain substantial influence through strong brand recognition, extensive distribution networks, and consistent product innovation. Consumer preference is increasingly shaped by product efficacy, ease of application, and long-term protective performance, prompting companies to invest in advanced formulations and value-added features. Retail partnerships with automotive outlets, e-commerce platforms, and detailing service providers reinforce market presence and facilitate consumer access.

Competitive positioning in the market hinges on formulation performance, regulatory compliance capability, and collaboration with retail and service networks. Moderate entry barriers exist due to the technical expertise required for high-quality formulations and the need to meet stringent chemical and environmental standards. New entrants must balance innovation with compliance and distribution effectiveness to gain traction. Established participants leverage brand equity and research investments to sustain market share while exploring niche segments and premium product lines. Continuous development of eco-friendly, long-lasting coatings and strategic alignment with automotive service providers strengthens market foothold.

Key Industry Developments

- In February 2026, Garware Hi-Tech Films introduced four new automotive care products, including ceramic and graphene coatings, windshield protection, detailing kits, and window film kits, to strengthen its vehicle protection portfolio and enhance user convenience and durability.

- In December 2025, Castrol India Limited expanded its vehicle maintenance portfolio in India with a new Aesthetic Care range featuring products such as Castrol Ultra Protect Shampoo, Ultra Protect Wax, Glass Cleaner and Dash & Leather Dresser to support everyday cleaning and protection for cars and motorcycles.

- In June 2025, Turtle Wax launched its global “You Are How You Car™” campaign across the U.S., U.K., and India, positioning car care as a reflection of personal identity through surreal advertising, digital engagement, and a consumer sweepstakes featuring personalized car-themed collectibles.

Companies Covered in Car Wax Market

- Henkel

- Turtle Wax Inc.

- Mothers Polishes Wax Cleaners Inc.

- Darent Wax Company Ltd.

- SONAX

- Chempace Corporation

- Malco Products

- Treatment Products Ltd.

- Sonax GmbH

Frequently Asked Questions

The global car wax market is projected to reach US$ 1.0 billion in 2026.

Rising vehicle ownership, increasing consumer focus on vehicle appearance, and growing demand for long-lasting protective coatings are driving the market.

The market is poised to witness a CAGR of 4.9% from 2026 to 2033.

Rapid growth in emerging automotive markets and expanding demand for premium and eco-friendly vehicle care solutions present key opportunities.

Some of the key market players include Henkel, Turtle Wax Inc., Mothers Polishes Wax Cleaners Inc., and Darent Wax Company Ltd.