- Food Ingredients & Additives

- Carrageenan Market

Carrageenan Market Size, Share, and Growth Forecast, 2026-2033

Carrageenan Market by Product Type (Kappa, Lota, Lambda), Function (Coating, Gelling, Thickening, Stabilization), Application (Beverages, Bakery, Dairy, Meat & Products, Confectionary, Others), and Regional Analysis for 2026-2033

Carrageenan Market Share and Trends Analysis

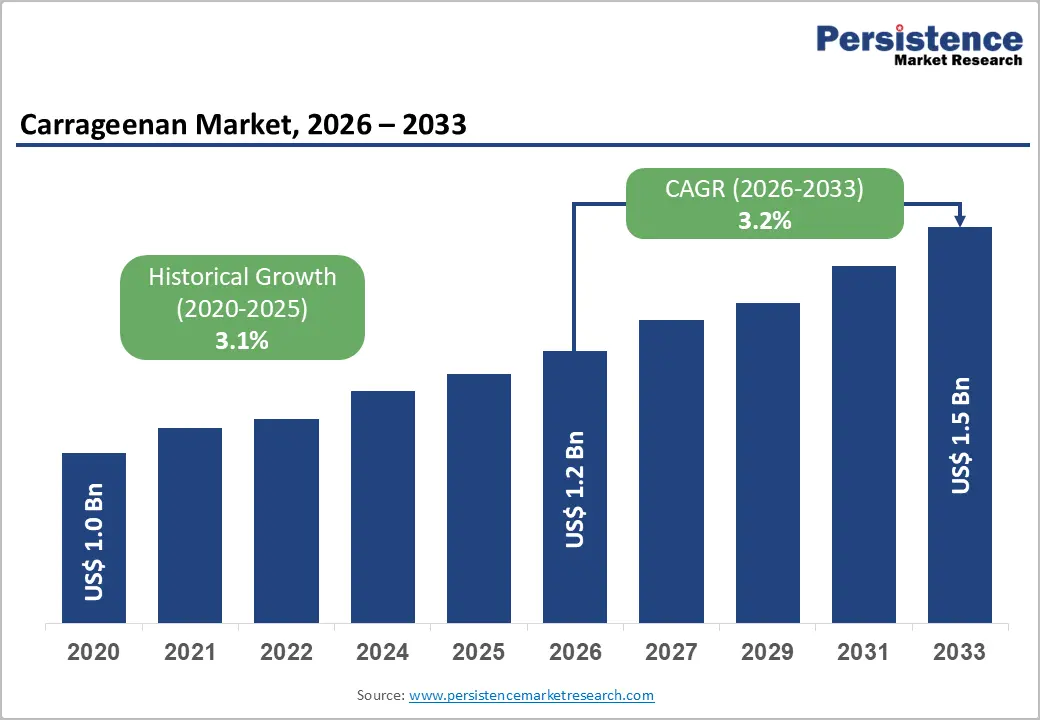

The global carrageenan market size is likely to be valued at US$1.2 billion in 2026, and is projected to reach US$ 1.5 billion by 2033, growing at a CAGR of 3.2% during the forecast period 2026–2033.

Market expansion is gaining traction as a result of rising consumer preference for natural and clean-label ingredients across packaged food categories. Food manufacturers are reformulating products to replace synthetic hydrocolloids with plant-derived alternatives, and carrageenan, extracted from red seaweed, is meeting this demand. The rapid growth of plant-based beverages and dairy alternatives is further accelerating adoption, as producers require stabilizing agents that maintain uniform texture and prevent ingredient separation. The ability of carrageenan to enhance viscosity and structural consistency is making it a functional ingredient in modern plant-based formulations.

Carrageenan is also utilized extensively as a stabilizer, thickener, and gelling agent in processed foods such as bakery items, processed meats, and confectionery products. Its multifunctional characteristics allow manufacturers to optimize mouthfeel, shelf stability, and moisture retention within a single formulation. Applications are also expanding in cosmetics and pharmaceutical preparations, where controlled viscosity and suspension properties are critical. A well-established cultivation and processing base in Asia Pacific is ensuring steady raw material supply, while regulatory approvals in major markets are sustaining commercial confidence.

Key Industry Highlights

- Leading Products: Kappa carrageenan is expected to account for approximately 45% of the revenue share in 2026, while lambda carrageenan is projected to register the fastest 2026-2033 CAGR, driven by cold-soluble applications in liquid formulations.

- Functional Leaders: Gelling applications are forecast to dominate with nearly 38% market share in 2026, whereas stabilization is likely to grow the fastest through 2033, supported by the massive demand for phase-stable beverages and sauces.

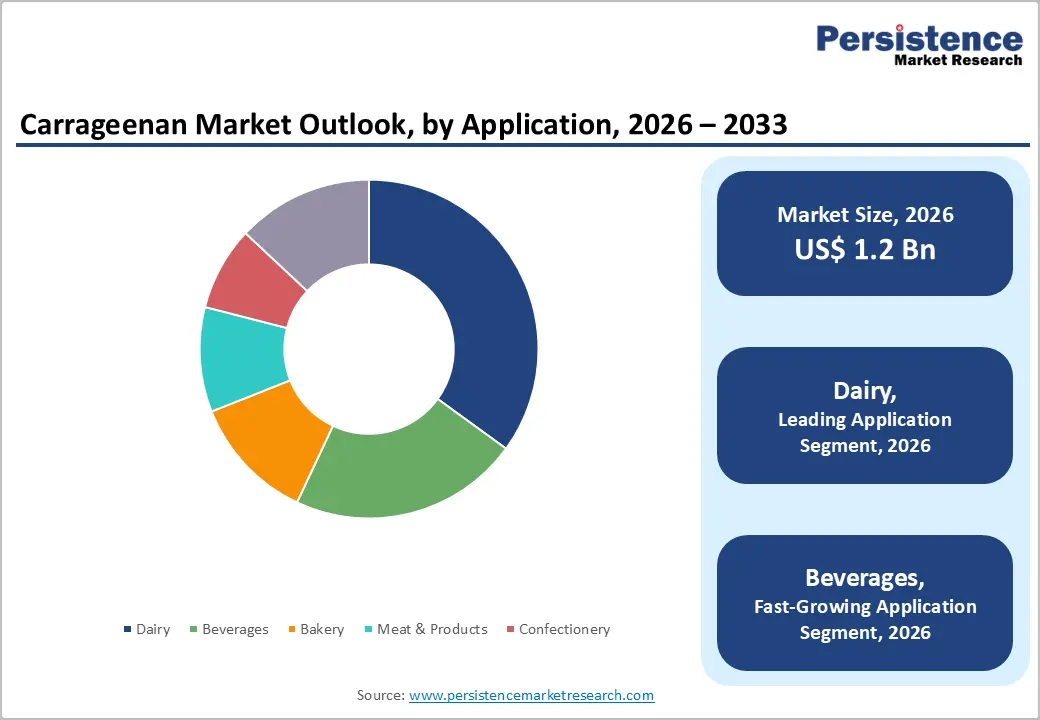

- Top Applications: Dairy products are set to contribute around 35% of revenue in 2026, while beverages are projected to record the highest 2026-2033 CAGR of about 4.5%, fueled by plant-based drinks and functional beverages.

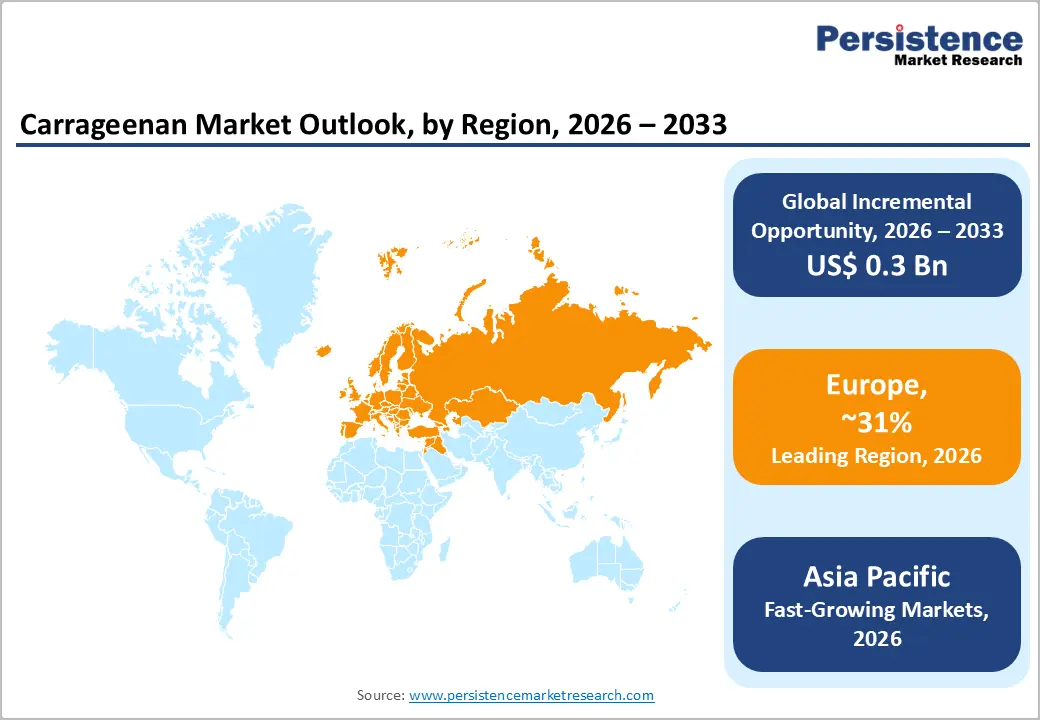

- Regional Growth: Europe is expected to lead with 31% market share in 2026, driven by robust consumer preference for natural ingredients, whereas the Asia Pacific market is likely to grow the fastest at 4.6% CAGR, supported by expanding food processing industries.

- Regulatory Compatibility: Carrageenan holds the Generally Recognized as Safe (GRAS) status of the U.S. Food and Drug Administration (FDA), sustaining market confidence and compliance adherence worldwide.

| Key Insights | Details |

|---|---|

| Carrageenan Market Size (2026E) | US$ 1.2 Bn |

| Market Value Forecast (2033F) | US$ 1.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Demand for Natural and Clean-Label Food Additives

Consumers and regulatory authorities are increasingly prioritizing natural and clean-label ingredients, prompting manufacturers to replace synthetic hydrocolloids with plant-derived alternatives in processed foods. Carrageenan, extracted from red seaweed, fulfills this demand by serving as a natural thickener, stabilizer, and gelling agent in products such as dairy, plant-based beverages, and meat analogues. It enhances texture, improves stability, and maintains product quality without artificial additives. Its versatility supports reformulation of traditional foods and aligns with global trends in health, sustainability, and ingredient transparency.

Recent industry movements support the accelerated clean-label adoption across the food and beverage sector, driven by increasing consumer demand for simplified, transparent ingredient lists. This widespread emphasis reinforces carrageenan’s role as a preferred natural additive, enabling manufacturers to diversify away from synthetics. Regulatory endorsements, including FDA GRAS classification and European Union (EU) approvals of seaweed-derived additives, further strengthen industry confidence and promote long-term adoption, supporting growth across multiple food segments.

Expansion of Plant-Based and Dairy Alternative Products

The shift toward plant-based diets and sustainable food consumption is driving carrageenan’s adoption in non-dairy milks, desserts, protein drinks, and specialty beverages. Its ability to replicate traditional textures and prevent phase separation is critical for maintaining product quality in plant-based formulations. Carrageenan enhances mouthfeel, supports suspension of particulates, and aligns with consumer demand for healthier, animal-free options. These functionalities enable manufacturers to produce plant-based products that meet sensory expectations while maintaining consistency and shelf stability. Its adaptability also allows for customized grades suitable for diverse processing conditions.

Industry developments reflects continued integration of carrageenan in plant-based and dairy alternative portfolios, with brands launching products emphasizing clean-label and minimal additive claims. Demand for customized carrageenan grades, such as kappa for gel strength and lambda for viscosity, is rising to meet diverse formulation needs. This trend not only drives growth in the plant-based segment but also allows manufacturers to diversify portfolios, capture new consumer segments, and strengthen market positioning across multiple food and beverage categories. Additionally, innovation in processing technology is enhancing efficiency and product quality, further boosting adoption.

Regulatory & Safety Scrutiny

Although carrageenan holds FDA GRAS status, regulatory bodies continue to evaluate its safety profile, leading to ongoing uncertainty for some applications. The European Food Safety Authority (EFSA) continues broad re-evaluations of permitted food additives, requesting updated safety data across multiple categories in 2025, signaling heightened scrutiny of ingredient safety frameworks. This trend can influence how food manufacturers approach formulation, especially for novel or sensitive products. Manufacturers may need to adjust formulations to meet stricter safety expectations while maintaining product performance and quality.

Regulatory expectations are especially pertinent for infant nutrition and medical foods, where safety margins are stringently reviewed. Additional documentation, toxicology evidence, or exposure data may be required before approvals are finalized, extending time to market for some manufacturers. The need for ongoing compliance with evolving scientific criteria underscores the complexity of regulatory pathways. Heightened scrutiny of permitted additives, regardless of long-standing approvals, creates incremental compliance costs and procedural steps, which can slow product launches, limit innovation speed, and increase operational overhead.

Raw Material Supply Constraints

Carrageenan production depends heavily on seaweed cultivation, and climatic variability remains a key constraint on consistent supply. The community-level reports from Southeast Asia highlighted increased storm frequency and unpredictable rainfall disrupting seaweed farms, forcing fishers and farmers to remove damaged crops more often due to loss risk, thereby affecting yields and reliability of supplies. These ecological pressures translate to seasonal harvest uncertainty and increased operational challenges for producers, requiring adaptive farming techniques and proactive risk management strategies.

Such climatic and environmental challenges can lead to price volatility and raw material scarcity, squeezing margins for carrageenan processors and complicating long-term supply commitments. Disruptions in key cultivation areas such as Indonesia or the Philippines can propagate through global value chains, impacting downstream food, beverage, and personal care ingredient availability. With seaweed cultivation concentrated in a few geographies, these supply risks underscore the importance of diversification strategies, infrastructure upgrades, and resilient sourcing models to stabilize raw material inflows and ensure reliable production across markets.

Expansion into Sustainable Packaging & Biomedical Applications

Carrageenan’s biodegradability and film-forming properties are creating promising avenues in sustainable packaging and biomedical materials. A collaborative study by researchers at Kongu Engineering College, Anna University, and IIT Kharagpur published in late 2025 explores carrageenan-based intelligent packaging that integrates active compounds (antimicrobials, antioxidants) to enhance food shelf life and quality, aligning with environmental and circular economy goals. Integrating sensors into carrageenan films can support food quality monitoring and reduce waste. These innovations are particularly relevant as global regulations increasingly favor eco-friendly packaging materials.

Beyond packaging, carrageenan’s biocompatible hydrocolloid nature is attracting interest for biomedical applications, including controlled-release drug delivery and wound care systems. As healthcare sectors pursue greener and safer solutions, carrageenan’s natural origin and functional versatility underpin its evolution from a traditional food additive to a material with cross-industry relevance. Continued innovation in extraction methods and composite formulations further strengthens its role in sustainability-oriented market expansion and supports new R&D collaborations.

Growth in Cosmetics & Specialized Pharmaceutical Uses

Natural seaweed derivatives such as carrageenan are gaining traction in cosmetics and personal care products as brands emphasize eco-friendly and clean-label formulations. DuPont de Nemours, Inc. has been noted in industry discussions for supplying cosmetic-grade carrageenan used in skincare and hair care products to improve texture and hydration, reinforcing its potential outside food applications. This highlights the use of seaweed polysaccharides for moisturizing, anti-inflammatory, and texture-enhancing benefits in skincare and hair care products, with formulations moving toward natural, biodegradable alternatives. Rising consumer demand for transparency and clean-label ingredients further reinforces this trend across global beauty markets.

Simultaneously, carrageenan’s functional properties are being explored in specialized pharmaceutical applications, such as excipients in controlled-release tablets, capsules, and gels. High-purity pharmaceutical grades offer opportunities to address formulation challenges, enabling manufacturers to expand beyond food into value-added healthcare segments. Cross-sector partnerships, regulatory support for natural excipients, and increasing interest in sustainable pharmaceutical solutions are amplifying this trend, creating new revenue streams and reinforcing carrageenan’s strategic value in high-growth markets.

Category-wise Analysis

Product Type Insights

Kappa carrageenan is likely to remain the leading product type, securing around 45% of the carrageenan market revenue share in 2026, due to its strong gel-forming properties that ensure firm texture and stability in dairy, processed meats, and confectionery. Its ability to form strong gels with proteins such as casein enhances mouthfeel and protein suspension in milk, yogurt, and plant-based alternatives, making it essential in mainstream food formulations. Industrial usage prioritizes gel strength and thermostability, while companies such as CP Kelco and Cargill invest in high-purity grades for premium applications.

The clean-label and organic kappa extracts gained traction in dairy alternatives and vegan desserts, with USDA Organic and EU Organic certifications enabling higher price points and label transparency.

Lambda carrageenan is projected to be the fastest growing product type through 2033, driven by its cold-soluble thickening ability that suits beverages, nutritional drinks, and cold-processed systems where gel formation is undesirable. Unlike kappa, it enhances texture while maintaining clarity and fluidity, supporting smooth liquid flow and product innovation. The industry applications increasingly incorporated lambda in ready-to-drink beverages, flavored milks, protein shakes, and functional drinks to ensure stability and sensory appeal.

Its effectiveness at room temperature and in heat-sensitive formulations reflects the broader trend toward natural hydrocolloids. The expanding use in beverages and personal care formats positions lambda as a key growth driver in the product type segment, accelerating adoption across emerging applications.

Application Insights

Dairy applications are expected to account of approximately 35% of global carrageenan usage in 2026, as it plays a vital role in enhancing protein suspension, texture, and consistency in products such as ultra-high temperature (UHT) milk, yogurts, custards, and plant-based alternatives. Carrageenan prevents syneresis, stabilizes emulsions, and improves mouthfeel, making it indispensable for high-volume dairy production where quality and shelf stability are critical.

The demand for organic carrageenan in plant-based dairy surged as brands adopted clean-label and sustainability credentials, with oat milk and almond yogurts exemplifying this trend. These premium formulations leverage carrageenan as a natural stabilizer, supporting label transparency, superior texture, and consumer-preferred taste, reinforcing dairy’s dominance in carrageenan applications.

The beverage application segment is anticipated as the fastest growing category, with a projected CAGR of 4.5% from 2026 to 2033, powered by carrageenan’s role in viscosity control and multi-component stabilization. It prevents phase separation in complex liquids, ensuring consistent texture and mouthfeel in ready-to-drink nutritional beverages, flavoured waters, protein drinks, fortified waters, botanical beverages, and functional shakes. Carrageenan also stabilizes cocoa particles and prevents sedimentation, broadening its utility across beverage formulations.

Industry innovation emphasized carrageenan as a natural alternative to synthetic gums, aligning with clean-label and functional beverage trends. Rising consumer demand for transparent ingredients and reliable performance continues to reinforce carrageenan adoption, solidifying beverages as the fastest-growing application segment in the market.

Regional Insights

North America Carrageenan Market Trends

North America is slated to control a major portion of the carrageenan market share in 2026, owing to strong demand for the ingredient in food processing, plant-based products, and functional beverages. The United States represents the largest portion of regional consumption, with widespread use in dairy alternatives, processed meats, and beverage stabilization. This adoption reflects a growing preference for natural hydrocolloids in clean-label formulations. The region benefits from mature supply chains, high consumer awareness, and well-established industrial networks, enabling efficient implementation of carrageenan across diverse food and beverage applications.

The expansion of Ingredion and Univar Solutions’ partnership in the Benelux region in June 2025 has strengthened global supply chains, supporting North American manufacturers in sourcing sustainable, clean-label hydrocolloids. This strategic move enhances domestic product availability and stimulates innovation in food and beverage formulations. At the same time, FDA GRAS recognition provides regulatory stability, though careful compliance remains essential for sensitive applications, such as infant nutrition.

Continuous investments in R&D, process optimization, and sustainable sourcing further bolster North America’s market leadership, establishing the region as a center for high-quality, premium carrageenan-based products.

Europe Carrageenan Market Trends

Europe is likely to be the leading regional market, accounting for an estimated 31% of global carrageenan demand in 2026, driven by stringent regulatory standards and a mature food processing industry. Strong adoption in clean-label dairy, bakery, and plant-based products reinforces its leadership, as natural hydrocolloids are essential for texture, stability, and mouthfeel. Elevated consumer awareness of ingredient transparency and sustainability further strengthens Europe’s dominant position. Key markets such as Germany, France, and the UK contribute significantly to regional consumption, underpinning high penetration across diverse food and beverage applications.

In 2025, the Univar Solutions–Ingredion partnership expansion into the Benelux region (Belgium, Netherlands, and Luxembourg) enhanced ingredient distribution and availability, supporting growth in plant-based and clean-label applications across Europe. Regulatory harmonization and strict food additive standards encourage the adoption of certified natural hydrocolloids and premium carrageenan grades. Manufacturers increasingly emphasize sustainable sourcing, R&D, and product innovation to meet compliance and consumer expectations. These combined factors solidify Europe’s leading market status and support ongoing expansion across dairy, bakery, and beverage segments

Asia Pacific Carrageenan Market Trends

Asia Pacific is projected to be the fastest-growing regional market for carrageenan, with an estimated CAGR of 4.6% during the 2026-2033 forecast period, supported by rapid expansion of food processing, rising disposable incomes, and extensive seaweed cultivation. The region supplies a substantial share of the world’s red seaweed raw material, which underpins carrageenan production and competitive pricing in both domestic and export markets. In December 2025, Indonesia spotlighted its seaweed industry at Food Ingredients Europe (FIE) 2025 in Paris, featuring six exporters of processed seaweed products, including carrageenan, attracting interest from global buyers and reinforcing Asia Pacific’s supply significance.

Government support for seaweed aquaculture is strengthening output and supply reliability, encouraging wider carrageenan adoption in food applications such as dairy alternatives, convenience meals, and beverages. For example, Indonesia’s Ministry of Marine Affairs and Fisheries reported US$264.6 million in seaweed exports in 2025, with dried seaweed and carrageenan as major contributors, highlighting export momentum to key markets such as China and the EU.

Regulatory alignment with international safety standards enhances Asia Pacific’s export potential, while local producers leverage raw material proximity to attract investment in processing infrastructure and partnerships, further solidifying the region’s role as a manufacturing and supply hub for carrageenan.

Competitive Landscape

The global carrageenan market structure is moderately consolidated, with leading players such as CP Kelco, Cargill, DuPont, Ingredion, and FCF Co. together accounting for over 50% of the total revenue share. These companies leverage established relationships with food and beverage manufacturers, regulatory expertise, and vertically integrated supply chains to maintain leadership. Heavy investment in R&D and innovation allows them to develop specialized carrageenan grades, optimize extraction technologies, and meet growing demand for clean-label and plant-based applications.

Regional and niche competitors, including Gelymar, Seasol, and Qingdao Haiyang Seaweed, focus on specific geographic markets or application segments such as dairy alternatives, beverages, and confectionery. Barriers such as stringent food safety regulations, raw material supply variability, and high capital requirements for processing facilities limit new entrants. However, the trend toward clean-label, organic, and functional ingredients is opening opportunities for smaller players and ingredient startups to collaborate through co-manufacturing agreements, joint R&D, and strategic partnerships. Market consolidation is expected to gradually increase as global leaders expand through acquisitions, geographic expansion, and innovation-driven differentiation.

Key Industry Developments

- In January 2026, the European Commission (EC) adopted Delegated Regulation (EU) 2026/196 amending Regulation (EC) No 1333/2008, updating usage conditions and specifications for carrageenan (E 407) and several other hydrocolloids, while introducing transitional periods to allow food businesses to comply with stricter standards without immediate market disruption.

- In December 2025, Indonesian seaweed processors, led by ASTRULI and supported by the Ministry of Marine Affairs and Fisheries, exhibited refined and semi-refined carrageenan, agar, and seaweed powders at Fi Europe 2025 in Paris, targeting US$ 8 million in direct exports.

- In May 2025, Roquette completed the acquisition of IFF’s Pharma Solutions unit, including seaweed-derived polymers such as carrageenan and alginate, expanding its footprint in pharmaceutical and nutraceutical applications.

Companies Covered in Carrageenan Market

- DuPont de Nemours Inc.

- Ingredion Incorporated

- Cargill, Incorporated

- CP Kelco U.S. Inc.

- Ashland Global Holdings

- CEAMSA

- Gelymar S.A.

- MCPI Corporation

- TBK Manufacturing Corporation

- LAUTA Ltd.

- ACCEL Carrageenan Corporation

Frequently Asked Questions

The global carrageenan market is projected to reach US$ 1.2 billion in 2026.

Rising demand for natural food additives, expansion of plant-based beverages and dairy alternatives, and multifunctional use in processed foods are driving the market.

The market is poised to witness a CAGR of 3.2% from 2026 to 2033.

Emerging plant-based food markets, functional beverage formulations, and innovation in organic and clean-label products represent major growth opportunities.

CP Kelco, Cargill, DuPont, Ingredion, and FCF Co. are some of the leading players.