- Home Appliances

- Can Opener Market

Can Opener Market Size, Share, and Growth Forecast, 2026 – 2033

Can Opener Market by Product Type (Manual Can Openers, Specialty Can Openers, Electric Can Openers), Material (Stainless Steel, Plastic, Aluminum, Mixed Materials), Application (Residential, Commercial, Industrial), and Regional Analysis for 2026-2033

Can Opener Market Share and Trends Analysis

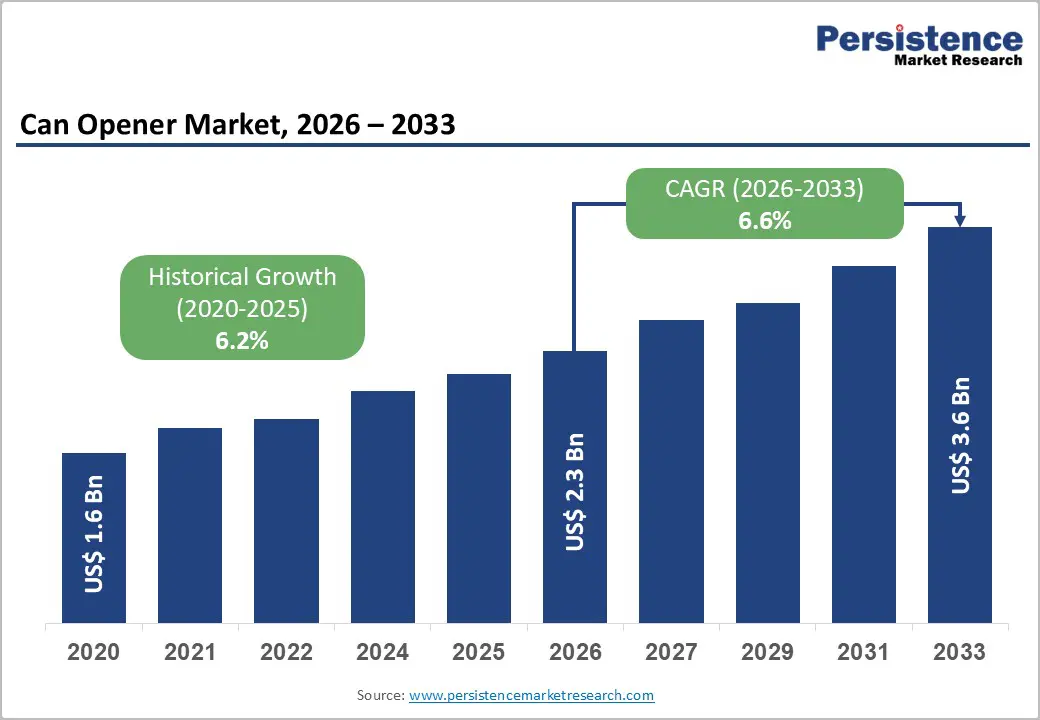

The global can opener market size is likely to be valued at US$ 2.3 billion in 2026, and is projected to reach US$ 3.6 billion by 2033, growing at a CAGR of 6.6% during the forecast period 2026−2033. The market demonstrates sustained expansion potential, supported by evolving household consumption patterns, rising demand for packaged food, and steady growth in food service infrastructure. Market momentum reflects a direct cause–effect relationship between urbanization, increased workforce participation, and higher reliance on canned and preserved food products.

Expansion of organized retail and electronic commerce platforms has improved product accessibility across both developed and emerging economies, strengthening baseline demand. Product innovation focused on ergonomic design, safety features, and automation has enhanced consumer acceptance across diverse demographic groups, including aging populations and individuals with limited hand strength. Commercial kitchens and institutional food service operators increasingly prioritize durable and time-efficient food preparation tools, reinforcing demand from non-residential segments.

Key Industry Highlights

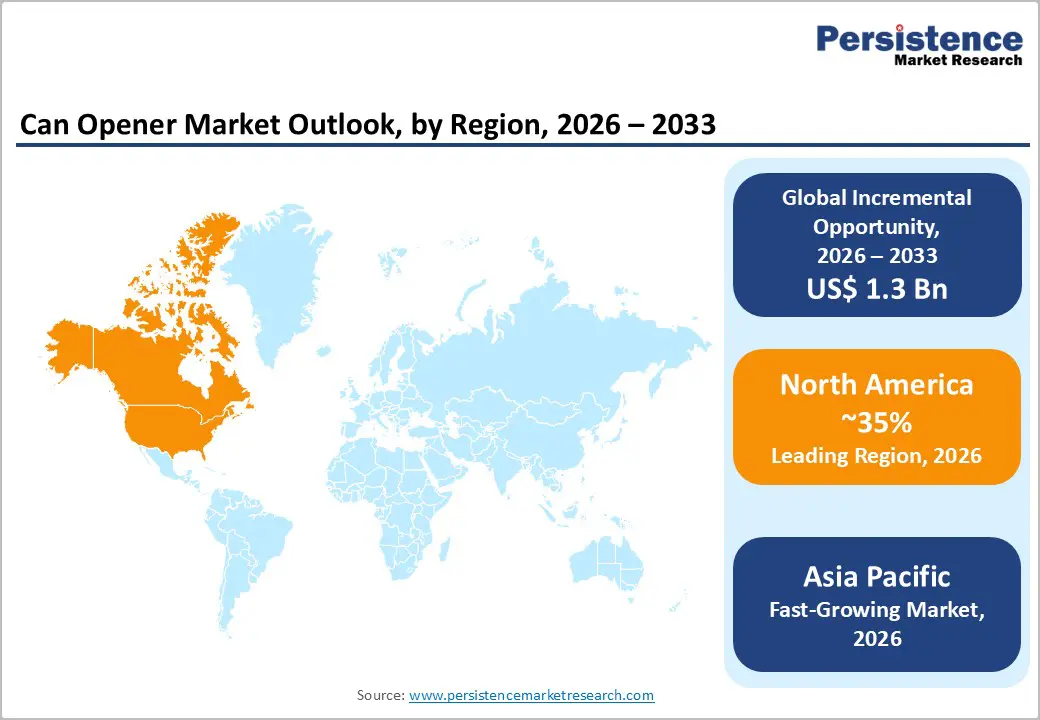

- Dominant Region: North America is set to lead with an estimated 35% share in 2026, driven by high packaged food consumption and mature cold-chain distribution.

- Fastest-growing Market: Asia Pacific is poised to be the fastest-growing market through 2033, supported by increasing adoption of shelf-stable foods and expansion of organized retail and digital grocery platforms.

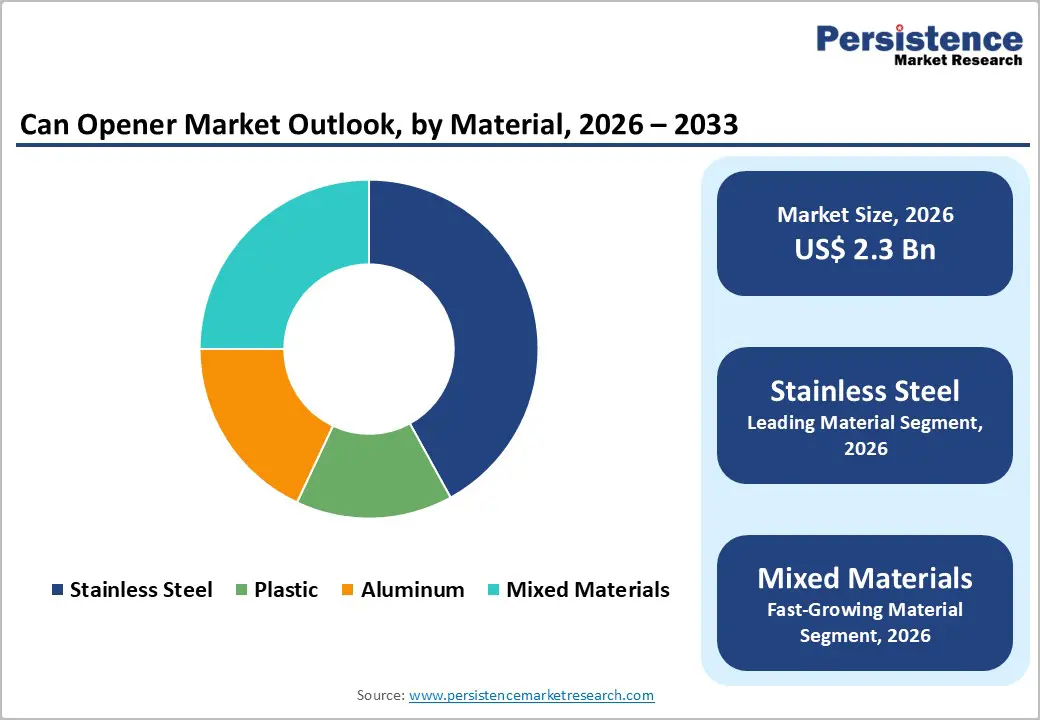

- Leading Material: Stainless steel is projected to hold a revenue share of about 42% in 2026, owing to its superior structural integrity, corrosion resistance, and stable performance in intensive kitchen environments.

- Fastest-growing Material: Mixed materials are slated to register the fastest growth during 2026–2033, enabled by hybrid designs that balance strength and comfort and deliver ergonomic and visual differentiation.

| Key Insights | Details |

|---|---|

| Can Opener Market Size (2026E) | US$ 2.3 Bn |

| Market Value Forecast (2033F) | US$ 3.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth in Packaged and Preserved Food Consumption

Consumption of packaged and preserved foods has fundamentally shifted dietary patterns and purchasing behavior, creating a larger base of users for products that facilitate access to such foods. Official data shows that about 55% of total calories consumed by Americans age one and older now come from ultra-processed foods, a category that includes many packaged and long-shelf-life items such as ready meals, snacks, and sweetened beverages. This statistic reflects a structural change in food demand where convenience and prolonged shelf stability are central to household food choices. Ultra-processed foods are typically sold in sealed metal cans or other durable packaging formats that protect product quality over time and distance. As consumption of these food formats rises, household and food service environments increasingly require reliable tools to handle and open these packaged goods efficiently and safely.

From a supply chain and consumer behavior perspective, packaged and preserved foods often dominate retail assortments and shelf space, meeting the needs of busy lifestyles and urban populations with limited time for food preparation. They are designed for extended storage and frequent usage, which increases the incidence of packaging formats requiring auxiliary tools for access. Growing reliance on processed and convenience food categories documented by national dietary surveys signals that a large proportion of daily food intake involves packaged formats. This trend drives consistent demand for implements that complement those formats, enabling smoother operation in both residential and commercial kitchens.

Ergonomic Design and Product Innovation Adoption

Changing consumption patterns and daily kitchen usage expectations place strong emphasis on tools that align with natural hand movement and reduce physical strain. Increased time pressure in urban households and higher awareness of musculoskeletal comfort influence evaluation of basic food preparation equipment. Products that support neutral wrist posture, stable grip, and controlled cutting action respond directly to user discomfort experienced with conventional designs. Senior consumers and users with reduced hand strength show clear preference for solutions that require lower torque and fewer repetitive motions.

Continuous product innovation transforms ergonomic principles into measurable performance advantages that support long-term adoption. Engineering refinements such as precision-cut blades, assisted rotation systems, reinforced cutting wheels, and soft-touch composite handles enhance durability and consistency during repeated use. Innovation cycles focused on user experience encourage replacement demand as consumers recognize efficiency gains and reduced effort. Brand positioning strengthens when design evolution is supported by testing, material optimization, and visual refinement that signals quality. Retail channels favor differentiated designs that reduce return rates and generate positive user feedback.

Saturation in Mature Markets and Price Sensitivity

High ownership levels across developed economies constrain demand expansion for everyday kitchen tools. Household penetration reached a point where first-time purchases are rare, and demand is driven mainly by replacement rather than adoption. Product durability extends replacement cycles, reducing transaction frequency and limiting volume growth. Retail shelves show minimal differentiation across models, reinforcing consumer perception of standardization and lowering motivation to upgrade. Competitive intensity rises in this environment, placing pressure on margins and reducing incentives for aggressive capacity expansion. Distribution channels also favor established low-cost suppliers, restricting entry opportunities for premium or innovation-led offerings.

Price sensitivity strengthens this restraint as household spending priorities remain tightly managed. Official data from the Government of India reports consumer price index (CPI) inflation at 1.33% in December 2025, indicating continued focus on value and cost control in daily purchases. In such conditions, buyers emphasize functional adequacy over design enhancements or branding, narrowing acceptance of higher-priced variants. Promotional pricing and private-label alternatives gain traction, intensifying downward pressure on average selling prices. Procurement decisions by retailers prioritize turnover and price competitiveness, reinforcing commoditization. Revenue growth therefore depends largely on cost efficiency and scale rather than premiumization.

Durability-Driven Replacement Cycles

Extended product lifespans fundamentally alter purchase behavior across household tools, creating a structural constraint on volume growth. High material quality, simple mechanical design, and limited exposure to technological obsolescence result in tools that remain functional for many years. Purchase decisions are infrequent and largely replacement driven rather than aspiration driven. Consumers perceive limited incremental value in upgrading, as core functionality remains unchanged across generations. Retail sales cycles therefore stretch over long intervals, suppressing repeat demand. Price sensitivity reinforces this pattern, with buyers favoring one time investments over frequent purchases. Distribution channels experience slower inventory turnover, reducing incentives for aggressive promotion or portfolio expansion.

Replacement demand is further constrained by low failure rates and limited maintenance requirements. Products typically endure routine household use without performance degradation, reducing urgency for substitution. Innovation cycles focus on minor ergonomic or aesthetic changes, which rarely justify replacement decisions at scale. Commercial food service adoption remains selective, as bulk opening solutions often rely on automated equipment rather than manual tools. Secondary usage such as gifting or seasonal cooking fails to generate sustained uplift. From an investment perspective, extended durability shifts competition toward pricing and distribution efficiency rather than volume acceleration. Revenue growth therefore depends heavily on population growth and first time buyers, while mature regions face saturation dynamics.

Technological Convergence with Smart Kitchen Ecosystems

Technological convergence with smart kitchen ecosystems emerges as a pivotal opportunity as household equipment purchasing shifts toward integrated, digitally enabled environments. Smart kitchens emphasize interoperability, data-driven convenience, and seamless user interaction across appliances. Manual tools that align with connected platforms gain renewed relevance through sensor integration, usage tracking, and compatibility with voice-assisted or application-based workflows. This convergence elevates a traditionally low-involvement product into a value-added component of a broader kitchen system, supporting premium positioning and higher replacement cycles. As urban households adopt modular kitchens and connected appliances, demand increases for accessories that match aesthetic, functional, and digital standards defined by smart environments.

Underlying this opportunity is a structural change in consumer evaluation criteria, where utility extends beyond basic functionality toward efficiency, safety, and experiential consistency. Smart kitchen ecosystems prioritize ergonomic design, energy awareness, and assisted operation, creating scope for automation features such as torque control, lid detection, and safety lock mechanisms. Integration with digital assistants enables guided usage, maintenance alerts, and accessibility support for elderly or mobility-restricted users. These attributes resonate with wellness-focused and aging demographics, reinforcing long-term demand stability. From a supplier perspective, convergence supports differentiation through software-enabled upgrades rather than material changes alone, improving margin resilience.

Expansion into Emerging Economies

Rising urbanization and steady income progression across Asia Pacific, Latin America, Middle East, and Africa are reshaping household consumption patterns toward packaged and preserved food formats. Growth in nuclear families, higher participation of working populations, and time-constrained lifestyles support frequent use of canned food products across residential and commercial kitchens. Penetration of modern retail, e-commerce grocery platforms, and organized foodservice chains improves product visibility and access across tier-2 and tier-3 cities. Local manufacturing expansion and regional sourcing strategies reduce unit costs, enabling competitive pricing aligned with cost-sensitive consumer bases. Regulatory alignment with international food safety and packaging standards further supports adoption of sealed food products, indirectly strengthening demand for manual and electric opening solutions across diverse income segments.

Shifts in institutional consumption patterns strengthen long-term demand potential. Expansion of hospitality infrastructure, quick-service restaurants, catering services, and community kitchens increases reliance on bulk packaged ingredients that require efficient opening tools. Public food distribution programs, disaster relief operations, and defense procurement initiatives emphasize long shelf-life food formats, reinforcing recurring utility demand. Product localization strategies such as durable materials, simplified mechanisms, and low-maintenance designs improve suitability for varied climatic and usage conditions. Rising emphasis on food hygiene and waste minimization elevates preference for precision opening solutions that reduce spillage and contamination risk.

Category-wise Analysis

Material Insights

Stainless steel is likely to be the leading segment with a projected 42% of the can opener market revenue share in 2026, due to durability, corrosion resistance, and strong hygiene perception. The material supports consistent performance across humid, high-temperature, and high-contact environments common in domestic and professional food preparation settings. Resistance to staining, odor retention, and microbial buildup strengthens suitability for repeated food contact. Compatibility with sterilization processes improves acceptance across regulated foodservice operations. Long replacement cycles lower total cost of ownership, strengthening value perception among institutional buyers.

Mixed materials are expected to witness the fastest growth between 2026 and 2033, powered by design flexibility and cost optimization. Hybrid construction enables balance between structural strength and user comfort, addressing evolving consumer expectations around ease of use. Polymer integration allows textured grips, thermal insulation, and color variation, supporting both functional and aesthetic differentiation. Lighter weight improves handling efficiency for elderly users and high-frequency kitchen environments. Modular component sourcing improves cost control and accelerates product innovation cycles.

Application Insights

The residential segment is slated to hold a dominant position, with an anticipated 61% of the can opener market share in 2026, driven by high household penetration of canned food consumption and routine kitchen tool replacement. Changing dietary habits toward ready-to-use and preserved food items increase daily usage frequency within home kitchens. Rising disposable income levels support preference for durable and ergonomically designed tools. Smaller living spaces favor compact, multi-functional utensils with long service life. Promotional activity through mass retail chains and digital platforms improves brand visibility and purchase frequency. Cultural emphasis on food storage and convenience cooking strengthens sustained household demand, supporting stable volume consumption across both developed and developing urban markets.

Commercial end use is forecasted to be the fastest-growing segment between 2026 and 2033, boosted by expansion of food service establishments, institutional catering, and cloud kitchen operations. High meal throughput environments require tools capable of continuous use with minimal performance degradation. Adoption of standardized kitchen equipment improves workflow consistency and labor productivity. Rising focus on hygiene audits and regulatory inspections elevates demand for robust, easy-to-clean designs. Growth of franchised dining formats increases centralized procurement practices, improving supplier visibility and repeat orders. Technological integration within professional kitchens further supports uptake of advanced opening mechanisms aligned with speed and safety benchmarks.

Regional Insights

North America Can Opener Market Trends

North America is expected to dominate with an estimated 35% of the can opener market share in 2026, reflecting structural consumption patterns rooted in packaged food reliance and operational efficiency requirements. High per-capita consumption of canned vegetables, ready meals, pet food, and emergency rations sustains consistent daily usage across households and food service environments. A mature cold-chain and warehousing ecosystem supports large-scale distribution of shelf-stable foods, reinforcing long-term utility demand rather than episodic purchases. Product replacement cycles remain shorter due to high usage intensity and preference for performance consistency. Strong alignment between kitchen tool specifications and food safety enforcement norms elevates demand for corrosion-resistant, easy-to-sanitize materials, favoring premium and mid-range offerings with higher unit value. Pricing tolerance supports value-based purchasing decisions, strengthening revenue concentration beyond volume metrics.

Market leadership is further bolstered by institutional consumption dynamics and procurement sophistication. Large-scale restaurant chains, contract catering operators, healthcare facilities, and public food programs rely on standardized kitchen equipment to meet audit, hygiene, and operational benchmarks. Centralized procurement models enable bulk purchasing agreements, stabilizing recurring demand and supplier margins. High penetration of electric and semi-automated variants reflects labor optimization priorities and higher kitchen automation levels. Retail structure strength, including warehouse clubs and subscription-based e-commerce models, improves product turnover and brand loyalty. Innovation adoption rates remain elevated due to strong intellectual property enforcement and rapid commercialization cycles, supporting differentiated product offerings.

Europe Can Opener Market Trends

Europe demonstrates a stable and value-driven growth profile for can openers, shaped by strong regulatory alignment, sustainability priorities, and mature food consumption habits. High penetration of canned vegetables, seafood, ready meals, and specialty imports sustains consistent baseline demand across households and food service operations. Strict food safety and hygiene frameworks elevate preference for materials that support sanitation compliance, corrosion resistance, and long service life. Consumer purchasing behavior shows higher sensitivity to build quality, ergonomic design, and recyclability rather than price-led decision-making. Replacement demand is driven less by product failure and more by upgrading toward improved functionality and compliance with evolving safety standards, supporting steady revenue generation despite moderate volume growth.

Market structure further reflects sophistication in distribution and product positioning. Private-label dominance across supermarket chains increases standardization of kitchen tools, reinforcing demand for reliable, specification-driven designs. Premiumization trends remain visible through adoption of stainless steel and hybrid variants positioned around durability, safety assurance, and aesthetic consistency. Commercial demand is supported by catering services, hospitality operators, and institutional kitchens operating under strict audit regimes, which favor standardized equipment procurement and long-term supplier relationships. Circular economy policies and recycling mandates influence material selection and packaging decisions, encouraging innovation in low-waste and recyclable product designs. E-commerce penetration complements traditional retail by enabling wider access to specialized and ergonomic tools.

Asia Pacific Can Opener Market Trends

Asia Pacific is forecasted to be the fastest-growing market for can openers during the 2026-2033 forecast period, stimulated by structural shifts in food consumption and accelerated modernization of domestic kitchens. Rapid expansion of urban middle-income populations increases demand for shelf-stable food products aligned with convenience-oriented lifestyles. Migration toward smaller households and high-density housing supports preference for compact, easy-to-use kitchen tools with minimal storage requirements. Growth of organized retail, private-label packaged food brands, and digital grocery platforms expands exposure to canned formats across first-time buyers. Local manufacturing scalability and competitive labor economics enable rapid product availability at accessible price points, supporting volume-driven expansion rather than replacement-led demand.

Growth momentum is further reinforced by commercial food ecosystem expansion and institutional adoption. Proliferation of quick-service restaurants, cloud kitchens, and centralized food preparation units increases reliance on standardized food inputs requiring frequent opening operations. Procurement emphasis on cost efficiency and durability favors adoption of manual and semi-automated tools optimized for high-throughput environments. Rising regulatory focus on food hygiene and contamination control elevates demand for materials and designs compatible with sanitation protocols. Infrastructure investment in hospitality, healthcare catering, and public nutrition programs increases institutional demand consistency.

Competitive Landscape

The global can opener market demonstrates a moderately consolidated structure, shaped by the presence of established international brands alongside a broad base of regional and local manufacturers. Recognized participants such as OXO, Hamilton Beach Brands, Inc., Cuisinart, Zyliss, Kuhn Rikon, WMF, KitchenAid, and Brabantia Branding B.V. account for a meaningful but not dominant share of total revenue, creating a competitive balance rather than market concentration. Competitive strength among these brands is built on product reliability, safety-oriented design, material quality, and consistent performance under repeated use. Brand credibility, compliance with food safety expectations, and strong shelf presence across organized retail and digital channels reinforce their positioning within mid-to-premium price tiers.

Competition remains intense due to the sustained presence of cost-focused manufacturers supplying unbranded and private-label products. These participants compete primarily on pricing efficiency and localized distribution, particularly in value-oriented retail formats. Entry barriers remain moderate, as manufacturing processes are standardized and raw material access remains stable. Innovation strategies among leading brands emphasize ergonomic enhancements, electric variants, and sustainable material integration to defend margins and maintain relevance. Distribution reach and supplier relationships with large retail chains function as key competitive levers. Consolidation activity remains limited, as brand-driven differentiation and segmented demand support coexistence of multiple participants.

Key Industry Developments

- In August 2025, Morphy Richards’ 3-in-1 Electric Tin Can Opener, combining a can opener, knife sharpener, and bottle opener, witnessed strong demand as shoppers capitalize on stacked discounts that reduce the price to under £ 7. The hands-free appliance, featuring a magnetic lid holder and smooth geared mechanism, is gaining popularity for convenience and ease of use in everyday kitchens.

- In August 2025, Bonzerr introduced a bold, signature black version of its iconic Classic R can opener, combining durable construction with a refreshed aesthetic for enhanced kitchen appeal. The update aims to attract style-focused consumers while maintaining reliable performance and ergonomic design.

- In March 2025, Toyo Seikan Group’s subsidiary Nippon Closures won a Social Products Award 2025 in Japan for its Smartphone Ring + Cap Opener, a dual-function tool that combines a PET bottle cap opener with a smartphone grip, designed to help users open caps easily anywhere. The product was recognized for both its practical utility and its social value in assisting people with limited grip strength.

Companies Covered in Can Opener Market

- OXO

- Hamilton Beach Brands, Inc.

- Cuisinart.

- Zyliss

- Kuhn Rikon

- WMF

- KitchenAid

- Brabantia Branding B.V.

- Inter IKEA Systems B.V

- Atlantic Promotions Inc.

Frequently Asked Questions

The global can opener market is projected to reach US$ 2.3 billion in 2026.

Sustained growth in packaged and canned food consumption, expansion of food service operations, hygiene and safety compliance requirements, and recurring household replacement demand collectively drive the market.

The market is poised to witness a CAGR of 6.6% from 2026 to 2033.

Expanding packaged food adoption in emerging economies, growth of organized food service formats, rising demand for ergonomic and electric designs, and premium product positioning aligned with hygiene and sustainability expectations represent key market opportunities.

Some of the key market players include OXO, Hamilton Beach Brands, Inc., Cuisinart, Zyliss, Kuhn Rikon, WMF, KitchenAid, and Brabantia Branding B.V.