- Food Ingredients & Additives

- Cantaloupe Market

Cantaloupe Market Size, Share, and Growth Forecast, 2026 - 2033

Cantaloupe Market by Product Type (Fresh, Processed, Frozen, Dried), Application (Food & Beverages, Cosmetics & Personal Care, Dietary Supplements, Functional Foods), Nature (Organic, Conventional), and Regional Analysis for 2026 - 2033

Cantaloupe Market Share and Trends Analysis

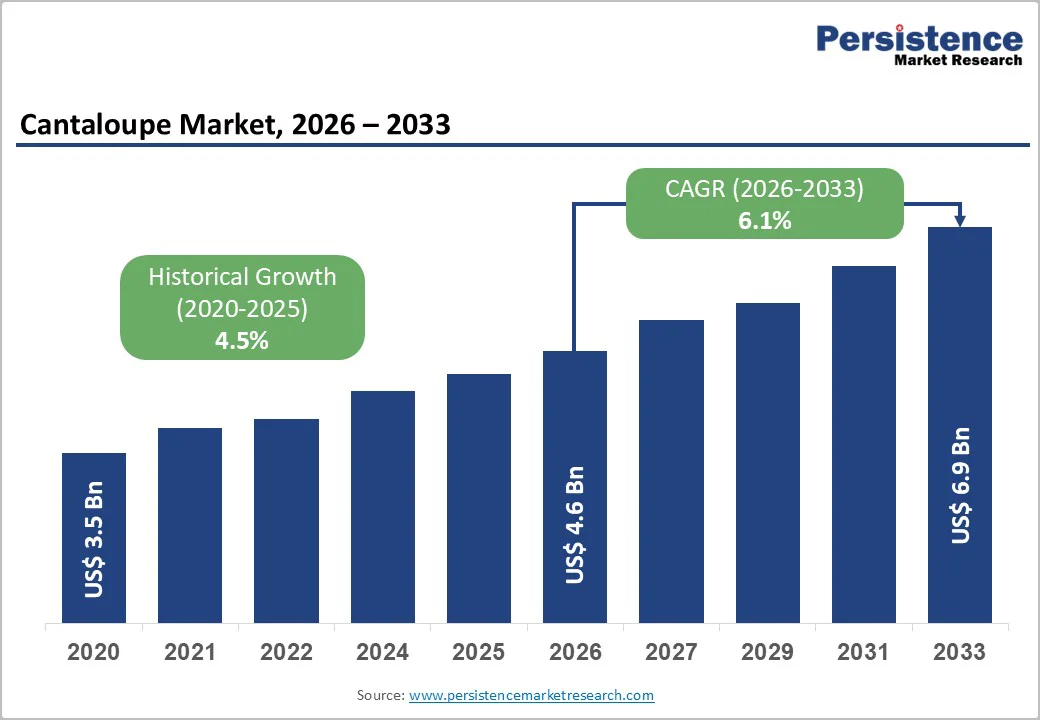

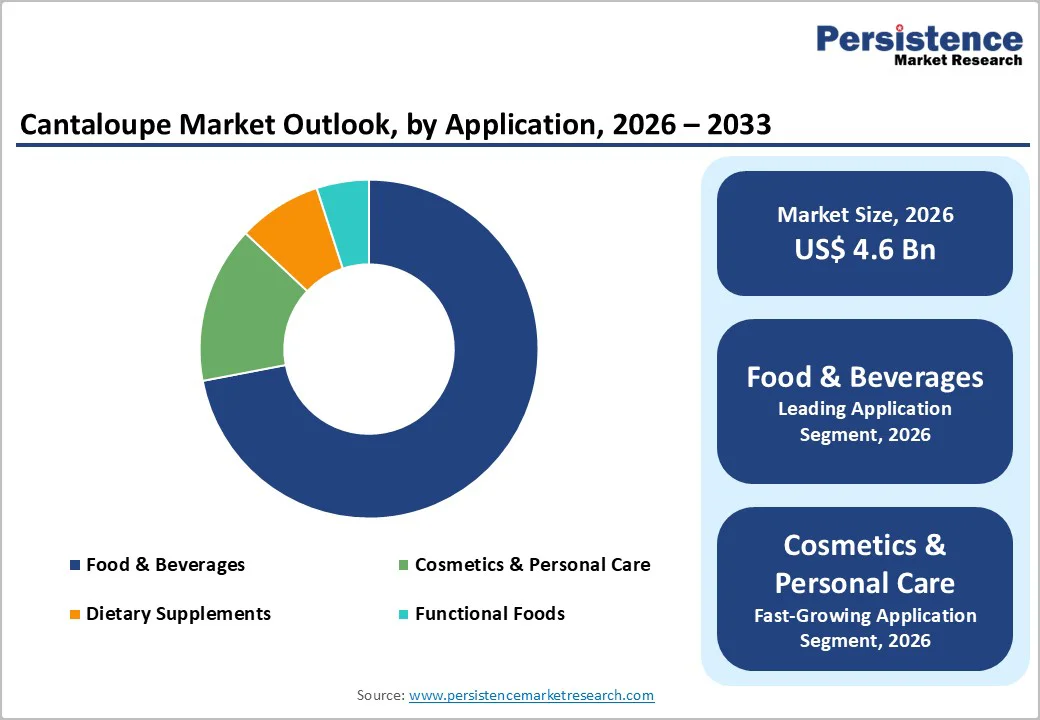

The global cantaloupe market size is likely to be valued at US$ 4.6 billion in 2026 and is projected to reach US$ 6.9 billion by 2033, growing at a CAGR of 6.1% during the forecast period 2026 - 2033.

This growth trajectory is primarily driven by increasing consumer awareness of the nutritional benefits of cantaloupe, which is rich in vitamin A, vitamin C, and potassium. Rising demand for fresh and organic produce across developed markets, coupled with expanding cultivation areas in emerging economies, continues to strengthen market fundamentals.

The integration of advanced agricultural technologies and improved cold chain infrastructure has enhanced product availability and reduced post-harvest losses, supporting sustained market expansion.

Key Industry Highlights

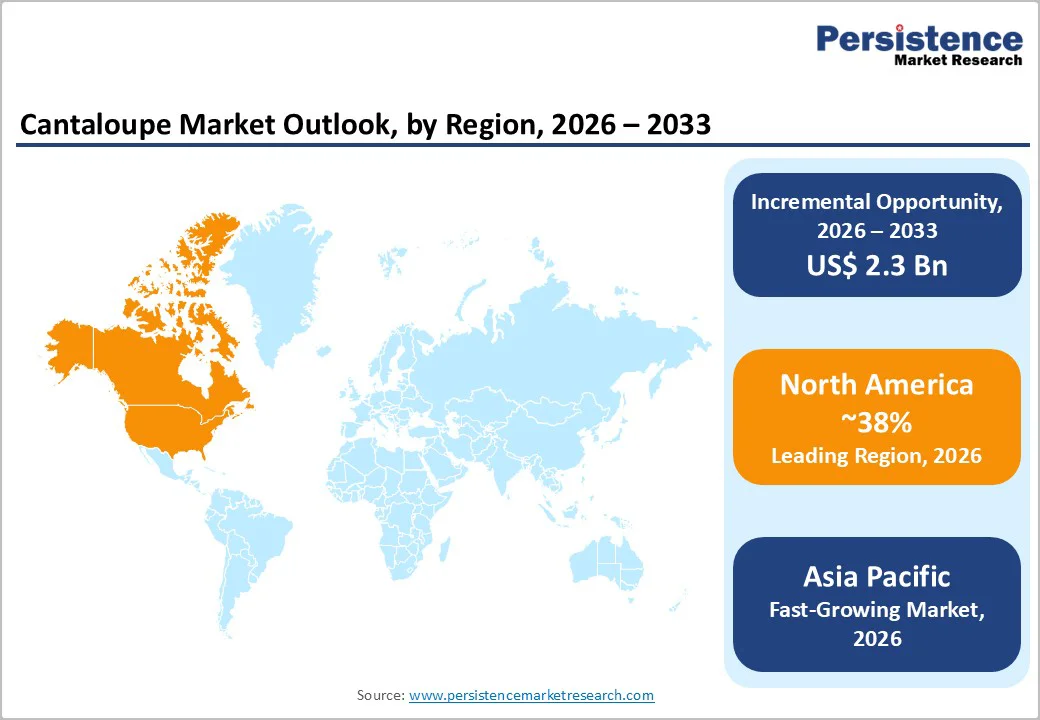

- Dominant Region: North America is expected to command around 38% market share in 2026, supported by well-established dietary incorporation of cantaloupes in breakfast routines.

- Fastest-growing Region: Asia Pacific is forecast to be the fastest-growing market through 2033, driven by strong supply networks and thriving export activity.

- Leading & Fastest-growing Product Types: Fresh cantaloupe is likely to account for about 78% of revenue share in 2026, while processed cantaloupe is expected to register the highest CAGR through 2033.

- Application Dominance: Food & beverages is slated to lead with an estimated 82% revenue share in 2026, while cosmetics & personal care is projected to grow the fastest during the 2026 - 2033 forecast period.

- Key Driver: Growing health consciousness and nutritional awareness have made fresh fruits a cornerstone of modern preventive healthcare, with consumers increasingly prioritizing natural, nutrient-dense foods in their daily diets.

- Major Opportunities: Shifting consumer preferences toward organic and sustainably produced food have created attractive premium segments that offer higher profitability for cantaloupe producers.

| Key Insights | Details |

|---|---|

| Cantaloupe Market Size (2026E) | US$ 4.6 Bn |

| Market Value Forecast (2033F) | US$ 6.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Health Consciousness and Nutritional Awareness

Growing health consciousness and nutritional awareness have made fresh fruits a cornerstone of modern preventive healthcare, with consumers increasingly prioritizing natural, nutrient-dense foods in their daily diets. Cantaloupes, with their refreshing taste and high water content, fit seamlessly into a wellness-oriented lifestyle, appealing to those seeking wholesome, low-calorie snacks.

Their natural sweetness and juicy texture make them a popular alternative to processed, sugary treats, especially among families and fitness-conscious individuals seeking balanced nutrition without sacrificing flavor or satisfaction.

Cantaloupes are increasingly valued not just as a fruit, but as a functional food that supports overall well-being. Their rich profile of vitamins and antioxidants aligns with consumer interest in foods that promote immune resilience, skin vitality, and heart health.

As people become more mindful of what they eat, cantaloupes stand out as a simple, accessible choice that complements smoothies, salads, and light meals, reinforcing their role in everyday healthy eating patterns across diverse age groups and lifestyles.

Perishability Challenges and Post-Harvest Losses

Cantaloupes are inherently perishable due to their high water content and thin rind, making them highly sensitive to temperature fluctuations, humidity, and physical handling. This limited shelf life creates substantial challenges across the entire supply chain, from farm to retail shelf.

Maintaining consistent, low temperatures from harvest through storage and transport is critical for preserving quality and extending freshness, but this requirement places a heavy burden on logistics and infrastructure. In many regions, especially where cold chain systems are underdeveloped, cantaloupes often degrade quickly, leading to softening, mold development, and loss of flavor and texture.

These quality issues not only reduce consumer appeal but also increase the risk of rejection by retailers and foodservice operators, putting pressure on producers and distributors to deliver near-perfect fruit within tight time windows.

The chemical instability of cantaloupes demands careful handling at every stage, from picking and packing to loading and unloading. Even minor impacts or rough handling can cause bruising or cracking, accelerating spoilage and increasing the risk of microbial contamination. As a result, specialized packaging and handling protocols are essential to minimize damage, but these measures add complexity and cost to operations.

The combination of a short shelf life, strict temperature requirements, and physical vulnerability limits producers in less developed markets' ability to access distant or high-value export markets. It also contributes to seasonal price swings, as oversupply during peak harvest periods cannot be easily stored or distributed over time, making the cantaloupe market particularly vulnerable to supply chain inefficiencies and infrastructure gaps.

Sustainable and Organic Production Systems

The marked shift in consumer preference for organic and sustainably produced food has created attractive premium segments that offer higher profitability for cantaloupe producers. Shoppers are increasingly willing to pay more for fruits grown without synthetic pesticides and fertilizers, viewing organic cantaloupes as healthier and more environmentally responsible choices.

This shift in demand has encouraged many growers to transition to organic production, supported by clear certification frameworks that help differentiate their products in the marketplace. Retailers and foodservice operators are also expanding their organic produce offerings, giving certified producers access to premium distribution channels and more stable, higher-margin contracts.

As a result, organic cantaloupes are no longer a niche product but a strategically important category that allows producers to build brand equity and long-term customer loyalty.

Beyond organic certification, broader sustainability practices are becoming essential for competitive positioning in the cantaloupe market. Producers are adopting water-efficient irrigation, integrated pest management, and regenerative soil practices to reduce environmental impact and improve long-term farm resilience.

These approaches not only meet consumer and regulatory expectations around sustainability but also lower input costs over time by reducing reliance on chemical inputs and improving soil health. By aligning with environmental, social, & governance (ESG) principles, cantaloupe producers can strengthen relationships with retailers, attract sustainability-focused investors, and access new markets that prioritize responsible sourcing.

Category-wise Analysis

Product Type Insights

The fresh segment is expected to account for around 78% of the cantaloupe market's revenue share in 2026. Direct consumption of fresh cantaloupe as a standalone fruit, in fruit salads, breakfast dishes, and desserts, remains the dominant segment globally.

Consumers strongly prefer the natural taste, juiciness, and aroma of fresh cantaloupe, valuing its nutritional benefits and sensory appeal that can be reduced by processing. In foodservice, demand is driven by breakfast buffets, salad bars, and fresh-cut fruit offerings in hotels, cafes, and restaurants, where cantaloupe is appreciated for its versatility, freshness, and visual appeal in plated and self-service formats.

Processed cantaloupe is likely to be the fastest-growing segment during the 2026-2033 forecast period. Manufacturers are increasingly developing innovative cantaloupe formats to meet convenience-oriented consumer preferences, driving growth beyond traditional fresh consumption.

Frozen cantaloupe products, such as chunks and purees, are gaining traction in smoothies, frozen desserts, and ready-to-blend beverages, appealing to time-pressed consumers seeking quick, nutritious options. Juice and concentrate applications are expanding in beverage formulations, with cantaloupe incorporated into multi-fruit blends and functional drinks targeting health-conscious audiences.

Dried cantaloupe snacks are also emerging as a popular choice, offering extended shelf life and portability. They are now widely available in convenience stores and online retail platforms, positioning cantaloupe as a versatile ingredient in the broader healthy snacking segment.

Application Insights

Food & beverage applications are slated to dominate with an estimated 82% revenue share in 2026. This segment encompasses fresh consumption as whole fruit, incorporation into fruit salads, breakfast preparations, desserts, and culinary applications across residential and foodservice channels.

The food and beverages segment's market leadership stems from cantaloupe's inherent appeal as a refreshing, naturally sweet fruit with versatile culinary applications spanning appetizers to desserts. Restaurant and hospitality establishments drive significant demand through breakfast buffets, salad bars, and beverage programs, while retail channels maintain consistent inventory to meet year-round consumer demand.

Cosmetics & personal care is estimated to be the fastest-growing application during the 2026 - 2033 forecast period. This accelerated growth reflects increasing utilization of cantaloupe extract and cantaloupe seed oil in skincare formulations, anti-aging products, moisturizers, serums, and hair care preparations.

Cantaloupe extract contains high concentrations of vitamin A, vitamin C, and beta-carotene, which provide antioxidant benefits that help protect skin from environmental stressors and premature aging. Beauty and personal care brands increasingly incorporate cantaloupe-derived ingredients into their natural and organic product lines, capitalizing on consumer preference for botanicals and clean beauty formulations.

Nature Insights

The conventional segment is set to lead, with a projected 85% share of market revenue in 2026. This segment’s leadership reflects mainstream consumer behavior, prioritizing affordability and consistent availability over production method. Conventional systems deliver reliable yields and consistent quality, which are critical for large retailers and foodservice operators that require a stable, year-round supply.

The lower cost structure of conventional production ensures more accessible price points, making cantaloupes widely available across different income groups. In several emerging markets, this cost advantage is especially important, as price sensitivity remains a key factor in purchasing decisions, reinforcing the continued dominance of conventionally grown cantaloupes.

The organic segment is expected to be the fastest-growing segment between 2026 and 2033, driven by evolving consumer values that emphasize environmental sustainability, health consciousness, and product transparency. Certified organic cantaloupes, produced without synthetic pesticides, chemical fertilizers, or genetically modified inputs, appeal to increasingly sophisticated consumer segments willing to pay premium prices for verified production standards.

Retailer commitments to expanding organic produce selections, supported by dedicated shelf space and prominent positioning strategies, further accelerate segment growth by enhancing consumer accessibility and purchase convenience.

Regional Insights

North America Cantaloupe Market Trends

North America is set to command a significant share of the cantaloupe market, approximately 38%, in 2026. The United States dominates regional consumption, driven by the well-established incorporation of cantaloupes into breakfast routines, salad preparations, and snacking.

California, Arizona, Texas, and Georgia constitute primary production regions, collectively supplying approximately 80% of domestic cantaloupe volume. The North American market benefits from advanced cold chain infrastructure, with temperature-controlled storage facilities and refrigerated transportation networks ensuring product quality maintenance throughout distribution channels.

Mexico serves as an important import source during off-season periods, providing year-round product availability essential for retail program continuity.

The regulatory framework in North America, especially under the Food Safety Modernization Act, has introduced strict food safety protocols that strengthen consumer confidence in cantaloupe quality and safety. These requirements mandate comprehensive traceability, sanitation, and risk-based preventive controls across the supply chain.

While this enhances market credibility and supports premium positioning, it also increases compliance costs and operational complexity, creating significant barriers for smaller and less-resourced producers. As a result, the market is witnessing greater consolidation, with larger players better positioned to absorb regulatory burdens and maintain a consistent, compliant supply.

Europe Cantaloupe Market Trends

Europe is a key regional hub in the cantaloupe market, supported by strong production capacity and diversified demand. Southern European countries, particularly those around the Mediterranean, serve as primary growing centers, benefiting from favorable climates and well-developed agricultural systems, including open-field and greenhouse cultivation.

Northern and Western Europe contribute significantly to the consumption side, where modern retail networks, expanding fresh produce assortments, and rising health awareness support steady growth in cantaloupe purchases. The cultural influence of fruit-rich dietary patterns further reinforces stable baseline demand across many European markets.

Regulatory harmonization across the European Union (EU) has created a unified framework that standardizes quality, safety, and labeling requirements for cantaloupes traded within the bloc. Maximum residue levels, traceability rules, and organic certification standards help ensure consistent product quality and support cross-border trade among member states.

Policy initiatives promoting sustainable agriculture and organic production encourage investment in protected cultivation technologies, such as greenhouses and advanced irrigation systems. Cooperative marketing organizations play an important role by aggregating supply from smaller growers, improving access to large retailers, and enhancing bargaining power.

Opportunities are also expanding in value-added formats and foodservice applications, especially in Northern Europe, where demand for convenient, healthy fruit options continues to rise.

Asia Pacific Cantaloupe Market Trends

Asia Pacific is projected to be the fastest-growing cantaloupe market globally through 2033, driven by strong demand growth across both established and emerging economies. China leads the regional market in terms of production and consumption, with large-scale cultivation concentrated in key agricultural provinces that supply the domestic market and support export activity.

Japan stands out for its high per capita consumption and premium positioning, where specialty cantaloupe varieties are marketed as luxury products in high-end retail and gifting channels. In India, the market is expanding rapidly, supported by a growing middle class, rising incomes, and the spread of organized retail in urban areas, which is increasing cantaloupe availability and consumer familiarity.

The regional market also benefits from well-set agricultural and manufacturing advantages, including abundant labor, favorable climates that allow multiple harvests each year, and government support for farming and infrastructure development. Regional initiatives are improving cold chain networks, helping to reduce post-harvest losses and enhance export potential.

Regulatory standards vary: more advanced markets enforce strict quality and safety requirements, while developing countries focus primarily on basic food safety compliance. Investment opportunities are concentrated in cold storage and logistics infrastructure, which are critical to meeting rising demand.

ASEAN countries, in particular, show strong growth potential as urbanization accelerates and younger consumers adopt more diverse, fruit-inclusive diets influenced by global trends.

Competitive Landscape

The global cantaloupe market structure is moderately fragmented, with leading companies such as Dole Food Company, Fresh Del Monte Produce, SunFed, and the Melon Consortium collectively holding 35-40% of the market share in 2026. This competitive landscape is shaped by several key factors, including product quality, pricing strategies, distribution network efficiency, and brand recognition.

Major players are actively expanding their product portfolios and investing in supply chain improvements to secure a stronger market position. Strategic moves such as partnerships, mergers, and acquisitions are frequently used to enhance geographic reach and consolidate market influence.

The competitive environment is highly dynamic, with companies continuously innovating to address changing consumer preferences and demands. These innovations include improved packaging, sustainable farming practices, and the introduction of new cantaloupe varieties.

The market’s structure encourages ongoing investment in research and development, as well as in logistics and marketing, to differentiate offerings and capture a larger share. As a result, the cantaloupe industry remains agile, with companies adapting quickly to new trends and opportunities in both domestic and international markets.

Key Industry Developments

- In October 2025, Martori Farms has acquired Fyffes' SOL Group melon business, combining farms in Honduras and Guatemala with distribution operations in Miami to create the world's largest year-round melon producer and the leading North American melon supplier. The acquisition enables Martori to offer continuous cantaloupe, watermelon, and honeydew supply across all 12 months.

- In October 2025, Mikiamo expanded its Italian spirit portfolio in India with the launch of Mikiamo Meloncello, a cantaloupe-infused liqueur crafted using traditional Italian methods. The product marks the brand's effort to diversify its offerings beyond traditional spirits and tap into the growing premiumization trend in the Indian alcohol market.

- In April 2025, Pacific Trellis Fruit, under its Dulcinea brand, launched Dulcinea Pure Perfection melons, a premium line focused on delivering superior sweetness, texture, and juiciness to elevate the eating experience.

Companies Covered in Cantaloupe Market

- Dole Food Company

- Fresh Del Monte Produce

- SunFed

- Southern Valley Fruit and Vegetable

- Melon Consortium

- Beijing Vegetable Research Center

- Honey Dew Farms

- Sakata Seed Corporation

- Nature's Pride

- California Giant Berry Farms

- Grupo Alta

Frequently Asked Questions

The global cantaloupe market is projected to reach US$ 4.6 billion in 2026.

Rising health consciousness, urbanization, and growing demand for fresh, convenient, and nutrient-dense fruits are driving the market.

The market is poised to witness a CAGR of 6.1% from 2026 to 2033.

Adoption of organic/sustainable production techniques, incorporation of value‑added formats (frozen, juice, dried), and expansion into foodservice and premium cosmetic applications are opening new market opportunities.

Dole Food Company, Fresh Del Monte Produce, SunFed and Melon Consortium are some of the key players in the market.