- Food Ingredients & Additives

- Canola Lecithin Market

Canola Lecithin Market Size, Share, and Growth Forecast, 2026 - 2033

Canola Lecithin Market by Product Type (Liquid, Powder, Granules), Application (Food & Beverages, Pharmaceutical, Cosmetics), Distribution Channel (Supermarket, Online Stores), and Regional Analysis for 2026-2033

Canola Lecithin Market Share and Trends Analysis

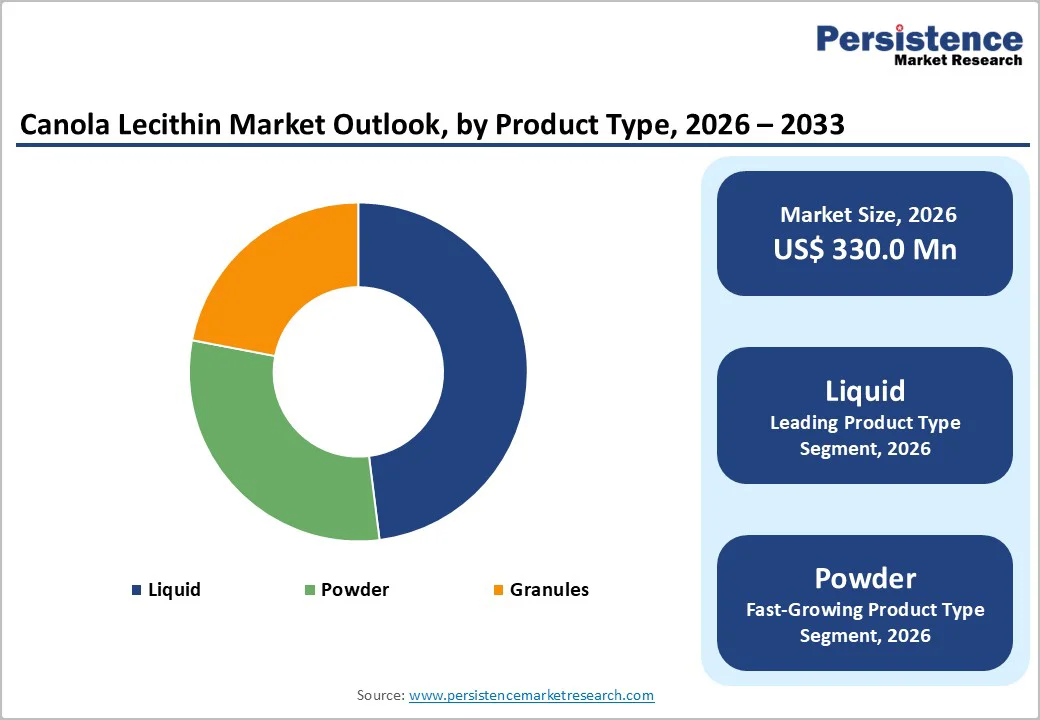

The global canola lecithin market size is likely to be valued at US$ 330.0 million in 2026, and is estimated to reach US$ 420.0 million by 2033, growing at a CAGR of 3.5% during the forecast period 2026−2033. Primary growth factors for the market are the high nutritional value and functionality of the ingredient. Canola lecithin is gaining popularity as a natural emulsifier, which is essential in the food & beverage industry for improving texture and shelf life of products. The increasing consumer inclination towards plant-based and allergen-free ingredients has further fueled its demand. Moreover, its lower cholesterol content and beneficial health attributes such as supporting heart health and liver function, make it a preferred choice among health-conscious consumers

Key Industry Highlights

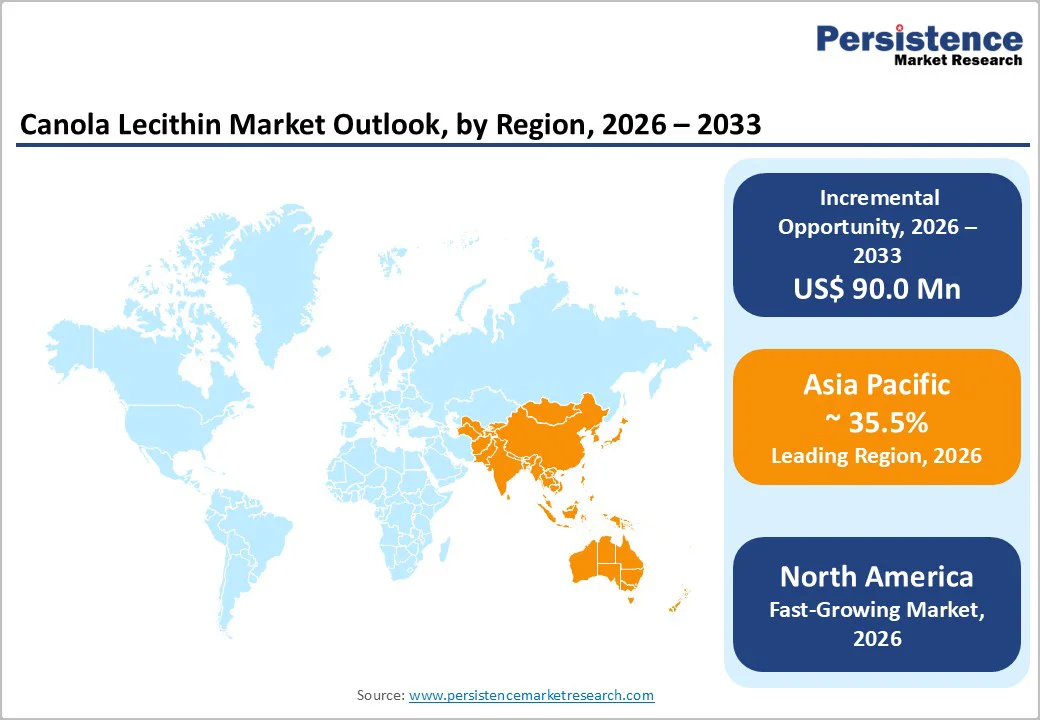

- Dominant Region: Asia Pacific is expected to command about 35.5% market share in 2026, supported by its growing population and steadily rising disposable incomes.

- Fastest-growing Regional Market: North America is set to be the fastest-growing regional market through 2033 due to its well-developed food and beverage, nutraceutical, and personal care industries.

- Leading & Fastest-growing Product Types: The liquid segment is projected to lead with an approximate 48% revenue share in 2026, with the powder segment growing the fastest during the 2026-2033 forecast period.

- Leading & Fastest-growing Applications: Food & beverages is slated to be dominant with an estimated 46% revenue share in 2026, while pharmaceutical is expected to be the fastest-growing application between 2026 and 2033.

- Major Driver: Canola lecithin use in pharmaceuticals is expanding as formulators increasingly leverage its phospholipid structure to improve the solubility, stability, and bioavailability of poorly water-soluble drugs.

- Key Opportunity: The growing demand for natural and plant-based ingredients, driven by health-conscious, vegan, and flexitarian consumers, presents prime business opportunities.

|

Key Insights |

Details |

|

Canola Lecithin Market Size (2026E) |

US$ 330.0 Mn |

|

Market Value Forecast (2033F) |

US$ 420.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

3.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Application of Canola Lecithin in the Pharmaceutical Industry

Lecithin plays a critical role in pharmaceutical formulations because it can form stable lipid systems that improve the solubility, absorption, and overall bioavailability of active pharmaceutical ingredients (APIs), especially those that are poorly water?soluble. In many oral, injectable, and topical drugs, lecithin helps disperse APIs more evenly, protects them from degradation, and supports controlled or targeted release, which enhances therapeutic effectiveness and shelf stability. As the global pharmaceutical industry expands, particularly in emerging economies where investment in generics, biosimilars, and complex formulations is accelerating, drug manufacturers are placing greater emphasis on high?quality, and well?characterized excipients such as canola?derived lecithin to meet regulatory and performance requirements.

Advances in oilseed processing, fractionation, and purification technologies have made it easier to extract and refine canola lecithin into specialized, high-purity grades, reducing production costs and improving functional performance. These technological improvements support a more reliable supply, tighter quality control, and tailored specifications, which in turn encourage wider adoption of canola lecithin as a preferred excipient in modern drug development and large-scale pharmaceutical manufacturing.

Price Volatility and Dependency on Canola Oilseed Supply

Price volatility is a major structural challenge to the canola lecithin market growth because its production is tightly linked to the economics and availability of canola oilseeds. Canola lecithin is a by?product of canola oil processing, so any change in canola seed prices, crushing margins, or overall canola oil demand feeds directly into lecithin costs. When harvests in key producing regions such as Canada, the EU, and parts of Asia are affected by droughts, floods, or other weather extremes, the resulting drop in seed supply can raise raw material prices and limit the volume available for processing.

For formulators in food and confectionery who work with low margins and have limited flexibility to pass on higher costs, this price and supply instability makes it harder to commit to long?term contracts and discourage broader adoption of canola lecithin. In cost?sensitive applications such as mainstream bakery or low?priced confectionery, buyers often revert to cheaper or more stable alternatives like soy or sunflower lecithin.

Increasing Demand for Natural and Plant-Based Ingredients

Growth opportunities in the canola lecithin market are mainly driven by the shift toward natural, plant?based, and clean?label ingredients across food, nutrition, and personal care categories. As consumers become more aware of the potential health benefits of canola lecithin such as its role in supporting healthy lipid metabolism and its use in better formulations, brands have stronger incentives to replace synthetic or animal?derived emulsifiers with canola?based alternatives.

A clear scope for value creation through product innovation and portfolio diversification is also emerging in the market. By supplying canola lecithin in multiple forms liquid for standard food processing, powder for dry blends and instant products, and granules for easier handling and precise dosing producers can better serve the varied needs of bakery, confectionery, beverages, dietary supplements, and functional foods. These expanding applications, combined with the broader plant-based and clean-label movement, offer substantial market expansion for suppliers that invest in technical support, application development, and tailored canola lecithin grades.

Category-wise Analysis

Product Type Insights

Liquid is likely to be the leading segment with an approximate 48% of the canola lecithin market revenue share in 2026, as it is simple to use, highly functional, and well?suited to large?scale processing. In liquid form, the ingredient disperses quickly into fats, oils, and aqueous phases, which makes it easy for manufacturers to pump, meter, and blend directly into production lines without extra dissolution steps. This reduces handling time, lowers processing complexity, and supports consistent product quality across high?volume operations. Demand is also supported by its use in pharmaceutical and cosmetic formulations, where liquid canola lecithin functions as both an emulsifier and stabilizer.

The powder segment is expected to register the highest CAGR during the 2026-2033 forecast period, since it meets the needs of the dietary supplement and functional food sectors. In dry form, it offers a longer shelf life than many liquid systems and is easier to store, transport, and handle in standard powder?processing facilities, which is important for contract manufacturers and brand owners operating multiple production sites. The powder form also enables accurate dosing and homogeneous blending into tablets, capsules, drink mixes, bars, and fortified foods, helping formulators control nutrient levels and meet label claim targets consistently.

Application Insights

Food & beverage applications are slated to be dominant with an estimated 46% of the canola lecithin market revenues in 2026, owing to the ability of the ingredient to deliver multiple functional benefits in a single, label?friendly package. As an emulsifier, stabilizer, and dispersing agent, it helps oil and water mix uniformly, keeps ingredients evenly distributed, and maintains product structure over shelf life. This makes it highly valuable in complex formulations such as bakery mixes, confectionery fillings, spreads, and ready?to?eat or ready?to?drink products, where texture, appearance, and stability are critical to consumer acceptance.

Pharmaceutical applications are expected to be the fastest-growing between 2026 and 2033. Canola lecithin plays a direct functional role in modern drug delivery systems. Its phospholipid structure allows it to act as a solubilizing and wetting agent, helping poorly water?soluble active pharmaceutical ingredients disperse more uniformly and dissolve more readily in biological fluids. This improves the bioavailability and absorption of many drugs, which is critical in oral tablets and capsules where limited solubility is a key formulation challenge.

Distribution Channel Insights

The supermarket channel is poised to capture around 65% of the market revenue share in 2026. Supermarkets are traditional and well-established distribution channels for canola lecithin. These large retail stores offer a wide variety of food and non-food products, including dietary supplements and health products containing canola lecithin. The ability to physically examine products, coupled with the convenience of one-stop shopping, makes supermarkets and hypermarkets a popular choice among consumers. The increasing number of supermarkets and hypermarkets, especially in urban areas, is expected to boost the sales of canola lecithin through this channel.

Online stores are anticipated to be the fastest-growing during the 2026-2033 forecast period. Online ordering and delivery platforms have rapidly become an important route for distributing canola lecithin, supported by the extensive proliferation of e?commerce and an astronomical rise in digital buying behavior. Consumers increasingly prefer purchasing canola lecithin based products online because they can compare multiple brands, formats, and price points in one place and order at any time with home delivery.

Regional Insights

Asia Pacific Canola Lecithin Market Trends

Asia Pacific is set to command approximately 35.5% of the canola lecithin market share in 2026.The region's large and growing population, rising disposable incomes, is fueling higher consumption of processed foods, functional beverages, and dietary supplements, all of which use lecithin as a key emulsifier and stabilizer. At the same time, awareness of health and wellness is increasing, encouraging consumers in countries such as China, India, and Japan to seek products positioned as natural, clean-label.

China, India, and Japan stand out as key demand centers as each of them combines a large, growing food processing sector with significant pharmaceutical and cosmetic manufacturing capacity. These factors can create broad application opportunities for canola lecithin across foods, nutraceutical, topical products, and advanced drug delivery systems. In China, for example, increase in processed food output and a strong, export-oriented nutraceutical industry are driving higher lecithin use. Meanwhile in India, rapid growth in fortified and convenience foods is generating a massive demand for novel ingredients. Japan’s focus on premium, high-quality processed foods and dietary supplements further supports the adoption of lecithin in sophisticated, value-added formulations.

Europe Canola Lecithin Market Trends

Europe is a key market for canola lecithin, with Germany, France, and the United Kingdom being the largest contributors. The region’s strong food and beverage and cosmetics industries rely heavily on natural emulsifiers and stabilizers, creating sustained demand for canola lecithin in bakery, confectionery, dairy alternatives, spreads, personal care, and skincare formulations. Manufacturers value canola lecithin because it supports both functional performance and consumer-facing claims around natural origin and plant-based ingredients.

In Europe, canola lecithin falls under the broader category of lecithin (E 322) and is regulated both as a food additive and as a feed additive. As a food additive, its use is governed mainly by Regulation (EC) No 1333/2008, which sets out where E 322 can be used, under what conditions, and with what purity and labeling requirements. Within this framework, lecithin is generally considered safe and can be added to many food categories as an emulsifier or stabilizer.

North America Canola Lecithin Market Trends

North America is anticipated to emerge as the fastest-growing market for canola lecithin from 2026 to 2033. The region boasts well-developed food and beverage, nutraceutical, and personal care industries that routinely use lecithin as an emulsifier, stabilizer, and dispersing agent in bakery, confectionery, beverages, dietary supplements, and cosmetic formulations. Within North America, the U.S. and Canada are the main markets. The U.S. drives demand through its very large packaged food and supplement sectors, while Canada plays a critical role on the supply side with extensive canola cultivation and oilseed processing capacity that supports lecithin production for the wider region.

Market growth is reinforced by consumer and regulatory shifts toward clean label, non?GMO, and plant?based products. Retailers and brand owners are increasingly reformulating to reduce artificial additives and major allergens, which supports the use of canola?derived lecithin in place of synthetic or animal?derived emulsifiers. Rising health and wellness awareness especially around natural ingredients, reduced allergies, and sustainable sourcing, further encourages manufacturers to position canola lecithin as a label-friendly functional ingredient in new product development, helping to drive steady demand growth across North America.

Competitive Landscape

The global canola lecithin market structure displays moderate fragmentation. Leading companies such as Cargill, Incorporated, Archer Daniels Midland Company (ADM), Bunge Limited, and Bioriginal Food & Science Corp. control around 43% of the market share. These firms compete primarily on superior product quality, competitive pricing, and versatility across diverse applications. End users in food processing, nutraceuticals, pharmaceuticals, and personal care demand lecithin that achieves high purity levels, reliable functionality, and full regulatory adherence while aligning with tight budget constraints.

Buyers prioritize suppliers who deliver consistent emulsification performance, oxidative stability, and clean-label compatibility to streamline formulations. Market leaders differentiate through vertically integrated supply chains that ensure traceability from seed to final product. To strengthen positioning, companies should invest in non-genetically modified organism [non-GMO] certifications, customized viscosity profiles for specific uses, and sustainability metrics that appeal to premium segments. This approach not only secures loyalty from quality-focused clients but also opens doors to high-margin opportunities in clean-label foods and organic cosmetics.

Key Industry Developments

- In September 2025, Louis Dreyfus Company (LDC) inaugurated a new laboratory in Luohe, Henan Province, China, in partnership with Zhongyuan Food Laboratory to advance food innovation and research capabilities. The facility strengthens local R&D for ingredients such as lecithin in the Asia Pacific market.

- In August 2025, Bunge agreed to acquire International Flavors & Fragrances' (IFF) soy and lecithin business for US$ 1.8 billion, enhancing its position in plant-based ingredients and expanding lecithin production capacity. The deal targets growth in food emulsifiers and nutraceutical applications.

- In March 2025, LDC launched a plant-based vitamin E product line at Food Ingredients China 2025, targeting food and nutraceutical applications with sustainable sourcing. The initiative expands LDC's portfolio in clean-label antioxidants and emulsifiers, including lecithin, for the Asia Pacific market.

Companies Covered in Canola Lecithin Market

- Cargill, Incorporated

- Archer Daniels Midland Company

- Bunge Limited

- DuPont de Nemours, Inc.

- Stern-Wywiol Gruppe GmbH & Co. KG

- American Lecithin Company

- Lipoid GmbH

- Wilmar International Limited

- Soya International Ltd.

- Avanti Polar Lipids, Inc.

- Lasenor Emul, S.L.

- Sime Darby Unimills B.V.

- VAV Life Sciences Pvt. Ltd.

Frequently Asked Questions

The global canola lecithin market is projected to reach US$ 330.0 million in 2026.

Rising demand for natural, plant‑based and non‑GMO emulsifiers in food, beverage, nutraceutical and personal care applications, supported by clean‑label and health‑focused consumer trends, is driving the market.

The market is poised to witness a CAGR of 3.5% from 2026 to 2033.

Widening consumer awareness about the health benefits of canola lecithin and the movement towards clean label products are key factors creating opportunities for market expansion.

Cargill, Archer Daniels Midland Company, Bunge Limited, and Bioriginal Food & Science Corp are some of the key players in the market.