- Medical Devices

- Breast Tissue Markers Market

Breast Tissue Markers Market Size, Share, and Growth Forecast 2026 – 2033

Breast Tissue Markers Market by Product Type (Coil markers, Ribbon markers, Butterfly/wing markers, Others), by Material (Non-absorbable markers, Bioabsorbable markers), by Imaging Modality (Mammography-compatible, Ultrasound-visible, MRI-compatible, Multi-modality), by End User (Hospitals, Ambulatory Surgical Centers, Cancer Research Centers, Diagnostic Centers), by Regional Analysis, 2026-2033

Breast Tissue Markers Market Size, Share, and Growth Forecast, 2026 - 2033

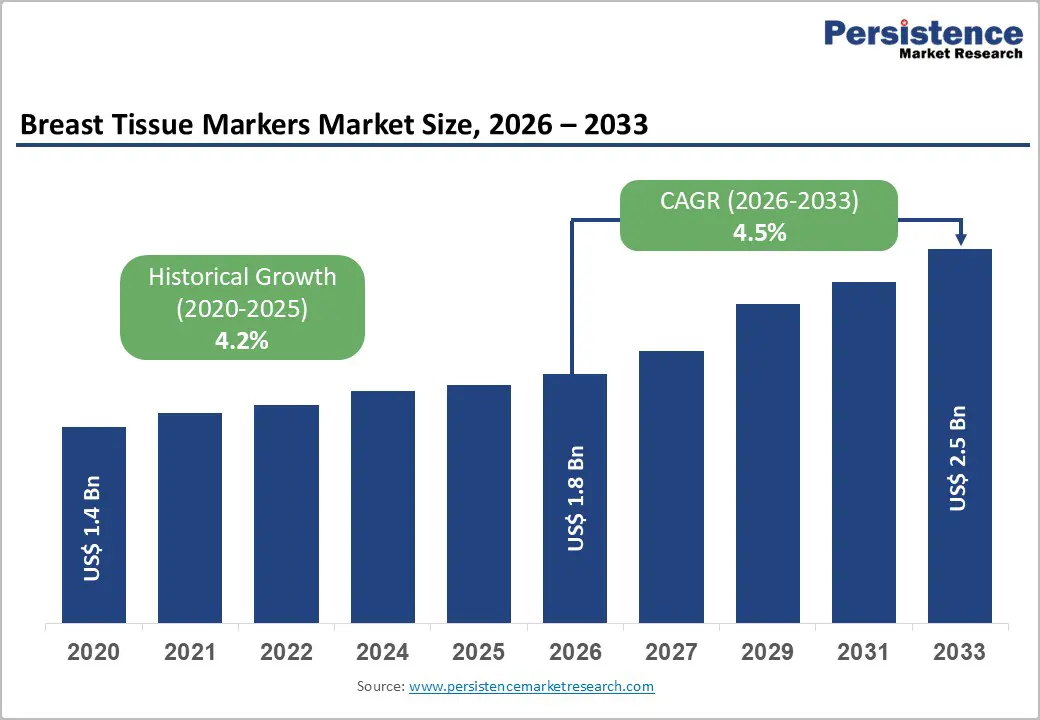

The global breast tissue markers market size is expected to be valued at US$ 1.8 billion in 2026 and projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

Rising breast cancer incidence, expanding screening programs, and the shift to image-guided, minimally invasive breast procedures are accelerating the adoption of clip and seed-based localization solutions in both developed and emerging markets. Coil markers currently lead usage due to strong visibility and anchoring in mammography- and ultrasound-guided biopsies, while newer bioabsorbable and multi-modality designs support better MRI compatibility and post-treatment imaging. Growing investments in comprehensive breast centers and quality accreditation programs across North America, Europe, and the Asia Pacific further reinforce steady procedure volumes and recurring demand for marker systems.

Key Market highlights

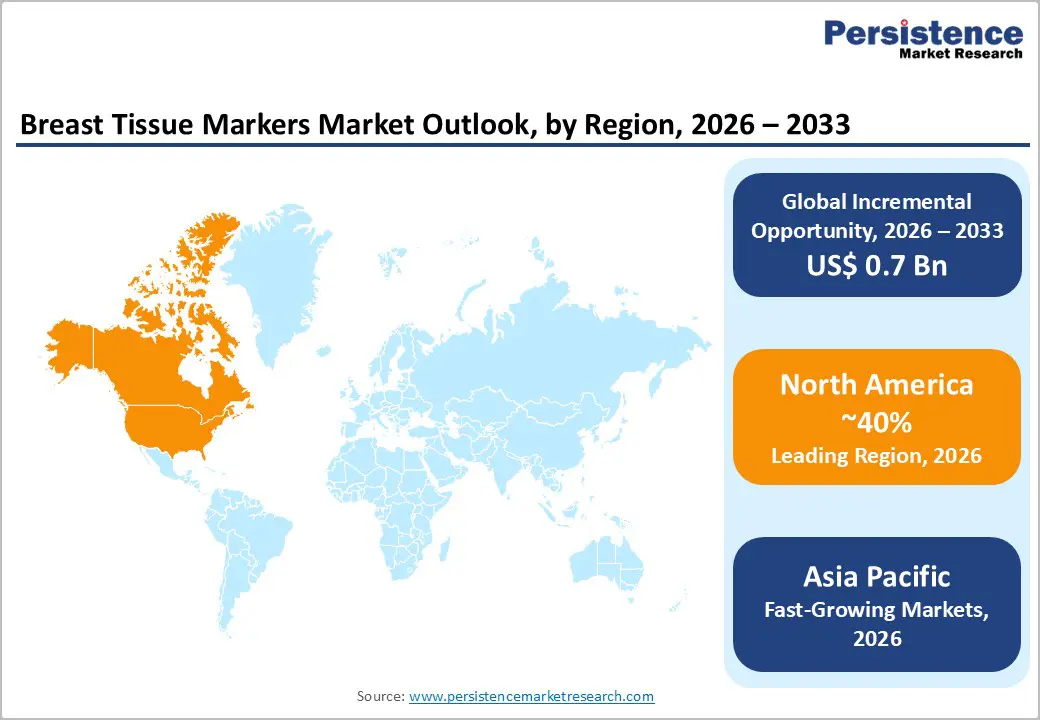

- North America remains the leading region in the breast tissue markers market, supported by high screening coverage, strong FDA regulatory oversight, and early adoption of wireless localization platforms in U.S. breast centers, sustaining significant marker demand across hospitals and ASCs.

- Asia Pacific is the fastest-growing region, as expanding mammography infrastructure, rising breast cancer incidence, and investments in cancer centers across China, India, Japan, and ASEAN are rapidly increasing procedure volumes and driving demand for cost-effective, multi-modality-compatible breast tissue markers.

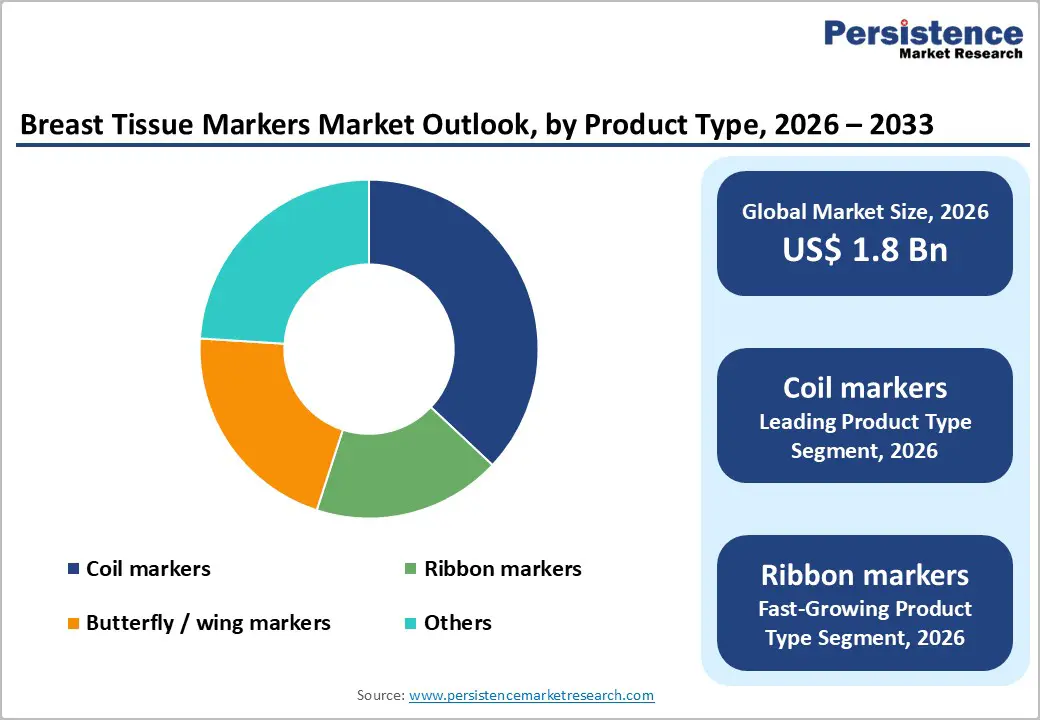

- Coil markers form the dominant product segment with about 37% share in 2025, combining secure anchoring and excellent mammography and ultrasound visibility, and are widely adopted by hospitals and diagnostic centers for image-guided biopsy and localization workflows.

- Ribbon markers are among the fastest-growing product segments from 2025–2032, as their flat, elongated shape supports ease of placement, reduced tissue disruption, and favorable imaging characteristics, aligning with evolving preferences for minimally invasive, cosmetically sensitive breast procedures.

- A key market opportunity lies in bioabsorbable and MRI-friendly markers integrated into wireless localization ecosystems, enabling reduced imaging artifacts, improved patient comfort, and seamless use across mammography, ultrasound, and MRI in advanced breast cancer programs worldwide.

| Key Insights | Details |

|---|---|

|

Breast Tissue Markers Market Size (2026E) |

US$ 1.8 billion |

|

Market Value Forecast (2033F) |

US$ 2.5 billion |

|

Projected Growth CAGR (2026-2033) |

4.5% |

|

Historical Market Growth (2020-2025) |

4.2% |

Market Dynamics

Market Growth Drivers

Rising global breast cancer burden and screening expansion

The growing incidence of breast cancer is the most critical demand driver for the breast tissue markers market, as early detection mandates accurate lesion localization and long-term site tracking. The World Health Organization (WHO) reports that female breast cancer has become the most commonly diagnosed cancer worldwide, with more than 2.3 million new cases annually, driving large volumes of mammography and image-guided biopsies. National programs, such as organized population-based screening in Europe and North America, increasingly rely on stereotactic and ultrasound-guided biopsies, in which tissue markers are routinely placed to guide surgery and subsequent imaging. This structural dependence on imaging and minimally invasive biopsy pathways underpins sustained consumption of markers per procedure, supporting stable growth in hospitals, cancer centers, and diagnostic facilities.

Shift toward minimally invasive, image-guided and wireless localization

Broader adoption of minimally invasive breast-conserving surgery and image-guided interventions is reinforcing demand for precise, multi-modality-compatible breast tissue markers. Surgeons and radiologists are increasingly replacing traditional wire localization with clip- or seed-based solutions that can be placed days before surgery, improving scheduling flexibility and patient comfort. Emerging “wireless localization” ecosystems, including magnetic and RFID-guided marker systems integrated with navigation platforms, enable real-time intraoperative targeting while maintaining clear visibility on mammography, ultrasound, and MRI. These trends align closely with advances seen in the broader breast lesion localization methods market, where wireless and image-guided techniques are experiencing double-digit growth and are rapidly becoming the standard of care in high-volume breast centers.

Market Restraints

Risk of marker migration, imaging artifacts, and re-intervention

Despite their benefits, traditional metallic markers can migrate from the original placement site, complicating subsequent localization and potentially necessitating additional imaging or repeat procedures. Clinical reports highlight cases in which metallic clips of approximately 3 mm shift after biopsy, leading to discrepancies between the biopsy site and the surgical target. Metallic markers may also induce artifacts on MRI, especially in high-field systems, reducing image quality and making assessment of treatment response more challenging. These factors contribute to clinician hesitancy in specific patient groups, particularly where MRI plays a central role in treatment planning, thereby restraining broader adoption of legacy marker designs.

Cost pressures, reimbursement complexity, and procedural variability

Cost constraints and heterogeneous reimbursement policies can limit the uptake of advanced marker technologies, especially in low- and middle-income settings and smaller outpatient centers. While some payers, such as the U.S. Centers for Medicare & Medicaid Services (CMS), have introduced dedicated reimbursement codes for certain magnetic localization solutions, coverage remains uneven across regions and product types. Hospitals and ambulatory surgical centers must also balance marker costs against bundled payments for breast procedures, leading to variability in adoption between premium wireless systems and basic clips. Furthermore, differences in surgeon preference and institutional protocols slow standardization, hindering the rapid scaling of innovative marker platforms.

Market Opportunities

Bioabsorbable and MRI-friendly marker innovations

The growing clinical emphasis on MRI-guided biopsy and surveillance, particularly in high-risk or dense-breast populations, creates a strong opportunity for bioabsorbable and low-artifact breast tissue markers. Demand is increasing for markers that maintain visibility on mammography and ultrasound while minimizing MRI susceptibility artifacts and the long-term presence of foreign bodies. Manufacturers are developing partially or fully bioabsorbable designs, polymer-embedded markers, and shape-encoded clips that preserve accurate localization yet integrate better with advanced imaging. As oncology protocols increasingly rely on multi-modality assessments, mammography, contrast-enhanced mammography, ultrasound, MRI, and even molecular breast imaging, multi-modality and bioabsorbable markers are positioned as a high-value growth pocket for premium pricing and differentiation.

Integration with wireless localization and digital surgery ecosystems

A major opportunity lies at the intersection of breast tissue markers and the rapidly growing wireless localization and digital surgery ecosystem. Companies are pairing markers with magnetic, radiofrequency, or radar-based localization platforms that provide intraoperative guidance and integrate with operating room imaging and navigation systems. For example, wireless seed systems and magnetic localization platforms are increasingly adopted in leading breast centers in the U.S. and Europe, enabling surgeons to localize tumors without same-day wire placement and reducing workflow bottlenecks. As hospitals invest in comprehensive breast health service lines, vendors that bundle markers, localization probes, and planning software can capture a larger share of procedural revenues, positioning the Breast Tissue Markers market to benefit from broader growth in breast lesion localization technologies.

Category-wise Insights

Product Type Analysis

Coil markers constitute the leading product type, accounting for about 37% market share in 2025, supported by strong clinical preference for their anchoring performance and multi-modality visibility. Their helical design provides secure placement within breast tissue, reducing the risk of migration during the interval between biopsy and surgery. Coil markers demonstrate excellent visibility under both mammography and ultrasound and are increasingly engineered to be compatible with MRI, widening their clinical utility across pre-operative planning and post-treatment surveillance. The combination of procedural reliability, imaging versatility, and broad availability across major manufacturers such as Hologic, Inc., Becton, Dickinson and Company (BD), and others cements coil markers as the dominant product category in routine breast biopsy and localization workflows.

Imaging Modality Analysis

By imaging modality, mammography-compatible markers currently represent the leading segment, with an estimated market share of around 40% in 2025, reflecting the central role of mammography in global breast screening and diagnostic algorithms. Most breast biopsies stereotactic or tomosynthesis-guided are performed under mammographic guidance, and consistent radiographic visibility is crucial for both radiologists and surgeons. At the same time, multi-modality markers (visible on mammography, ultrasound, and increasingly MRI) are emerging as the fastest-growing segment, driven by adoption in high-risk screening centers and comprehensive cancer hospitals that routinely use multi-modality imaging. This mirrors broader trends observed in the breast lesion localization methods market, where the ability to seamlessly localize lesions across imaging platforms is becoming a key purchasing criterion for advanced breast units.

End User Analysis

Among end users, Hospitals are the leading segment, capturing approximately 50% or more of the market share in 2025, supported by high procedure volumes and integrated surgical, imaging, and oncology services. Large tertiary care hospitals and academic medical centers conduct a substantial share of breast biopsies, lumpectomies, and mastectomies and are early adopters of new localization technologies, including wireless seed systems and advanced markers. Ambulatory Surgical Centers (ASCs) represent the fastest-growing end-user segment due to ongoing migration of breast-conserving surgery and day-case biopsies to outpatient settings, especially in the U.S. and select European markets. As payers and providers favor cost-efficient, minimally invasive care pathways, ASCs increasingly invest in breast imaging and marker capabilities, creating attractive opportunities for manufacturers with tailored product and service offerings.

Regional Insights

North America Breast Tissue Markers Market Trends

North America is the leading regional market, with around 40% share in 2025, supported by high breast cancer incidence, mature screening programs, and early adoption of advanced imaging and localization technologies. The U.S. benefits from well-established mammography infrastructure, widespread use of core needle biopsy, and strong integration between radiology and breast surgery teams, all of which drive routine placement of breast tissue markers after biopsy. Regulatory oversight by the U.S. Food and Drug Administration (FDA) ensures robust safety and performance standards for markers, while payers such as CMS have introduced specific codes for certain magnetic and localization solutions, reinforcing their clinical and economic viability.

Asia Pacific Breast Tissue Markers Market Trends

Asia Pacific is projected to be the fastest-growing regional market for Breast Tissue Markers between 2025–2032, driven by rapid improvements in healthcare infrastructure and rising breast cancer awareness in China, Japan, India, and ASEAN economies. As mammography capacity expands and more women undergo organized or opportunistic screening, detection of early-stage and non-palpable lesions increases, prompting higher utilization of image-guided biopsy and marker placement. Several countries are investing in national cancer control plans and rolling out screening pilot programs, which, over time, enhance procedure volumes and marker consumption in tertiary hospitals and regional cancer centers.

Manufacturing and cost advantages in countries such as China and India are enabling local and regional firms to develop competitively priced market solutions, often in partnership with global device companies or distributors. This supports broader access in price-sensitive markets and accelerates the shift from basic surgical approaches to image-guided, minimally invasive care. As the broader breast lesion localization methods market in Asia Pacific is forecast to grow at a higher-than-global CAGR, markers that offer multi-modality visibility and compatibility with emerging wireless localization systems are well positioned to capture incremental demand from expanding breast surgery and oncology networks.

Competitive Landscape

The Breast Tissue Markers Market is highly competitive and characterized by continuous innovation in design, material, and imaging compatibility. Companies focus on developing markers that are more visible across multiple imaging modalities, easier to deploy, and patient-friendly, including bioabsorbable and multi-shape options. Competition is driven by technological advancements, strategic collaborations, and increasing adoption in minimally invasive biopsy and surgical procedures.

Key Market Developments

- In May 2025, the FDA granted breakthrough device designation to the EnVisio X1 In-Body Spatial Intelligence System a next-generation localization platform for the real-time, non-imaging detection, localization, and surgical navigation of the SmartClip soft tissue marker, tracked surgical instruments, and other compatible tools used for the surgical excision of soft tissue in patients with cancer and other diseases.

Companies Covered in Breast Tissue Markers Market

- Hologic, Inc.

- Becton, Dickinson and Company (BD)

- Merit Medical Systems, Inc.

- Argon Medical Devices, Inc.

- Carbon Medical Technologies, Inc.

- Mammotome (Devicor Medical Products / Danaher)

- SOMATEX Medical Technologies GmbH

- Endomag / Endomagnetics Ltd.

- Scion Medical Technologies, LLC

- Mermaid Medical A/S

- Cook Medical Incorporated

- Medtronic plc

Frequently Asked Questions

The global Breast Tissue Markers market is expected to reach about US$ 1.8 billion in 2026, supported by rising breast cancer screening participation and growing adoption of image-guided biopsy and localization procedures worldwide.

A major demand driver is the increasing global burden of breast cancer, with more than 2.3 million new cases annually, which necessitates large volumes of mammography, image-guided biopsies, and marker placement for accurate lesion localization and follow-up.

North America leads the Breast Tissue Markers market with around 40% share in 2025, driven by robust screening infrastructure, advanced breast imaging, supportive FDA regulation, and rapid uptake of wireless localization platforms in the U.S. and Canada.

A prominent opportunity lies in developing bioabsorbable, MRI-friendly, and multi-modality markers integrated with wireless magnetic or RFID localization systems, enabling artifact-reduced imaging, improved patient comfort, and streamlined digital surgery workflows in advanced breast centers.

Hologic, Inc.., Becton, Dickinson and Company (BD), Merit Medical Systems, Inc., Argon Medical Devices, Inc., etc.