- Medical Devices

- Breast Cancer Screening Tests Market

Breast Cancer Screening Tests Market Size, Share, and Growth Forecast, 2026 – 2033

Breast Cancer Screening Tests Market by Test Type (Imaging Tests, Genomic/Mol. Test, Others), Technology Type (Mammography, Others), Application (Screening, Staging and Prognosis, Others), and Regional Analysis 2026 – 2033

Breast Cancer Screening Tests Market Size and Trends Analysis

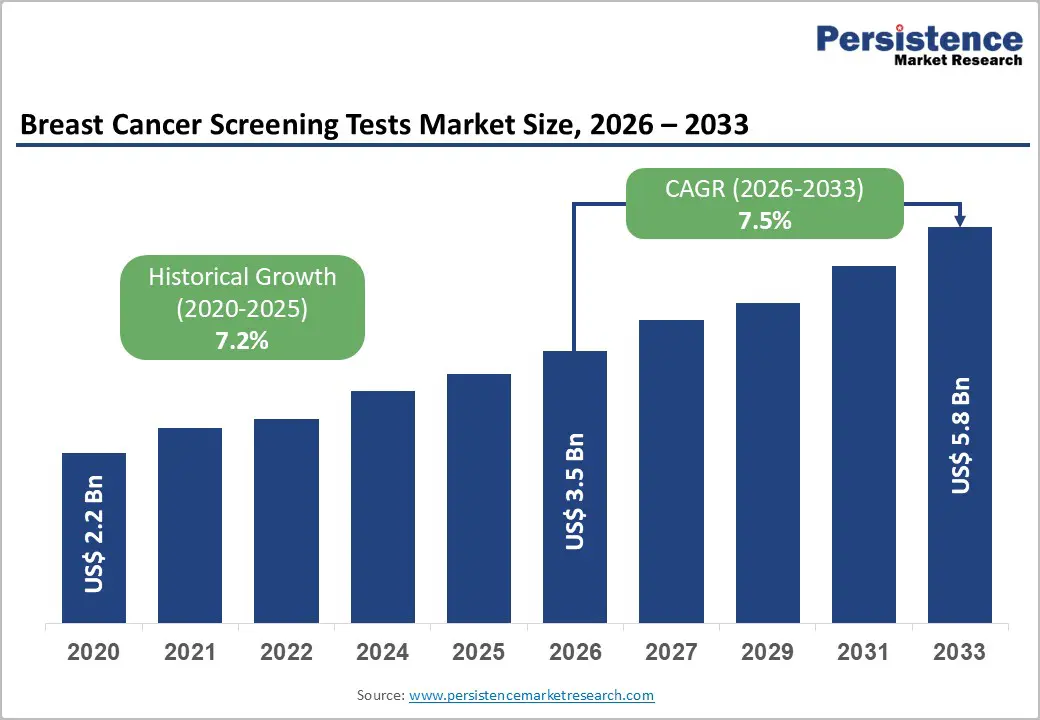

The global breast cancer screening tests market size is likely to be valued at US$ 3.5 billion in 2026 and is expected to reach US$ 5.8 billion by 2033, growing at a CAGR of 7.5% during the forecast period from 2026 to 2033, driven by the fact that breast cancer primarily affects middle-aged and older women, with the median age at diagnosis being 62. This means that half of the women diagnosed with breast cancer are 62 years old or younger, while only a small percentage of cases occur in women under 45.

According to the American Cancer Society's January 2026 report, breast cancer is the most common cancer among women in the U.S., accounting for approximately 30% (or one in three) of all new female cancer diagnoses each year. In 2026, the American Cancer Society estimates that about 321,910 new cases of invasive breast cancer will be diagnosed in women, along with 60,730 new cases of ductal carcinoma in situ (DCIS). About 42,140 women are expected to die from breast cancer in the same year.

Key Industry Highlights:

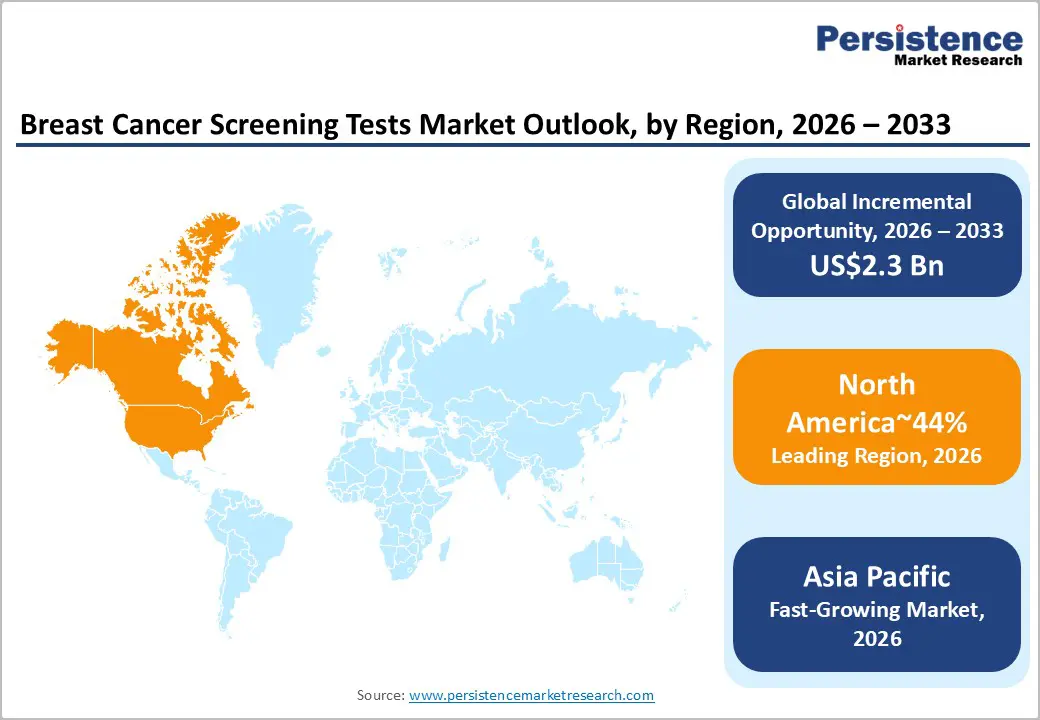

- Leading Region: North America is expected to remain the leading region in the breast cancer screening tests market, accounting for approximately 44% of global revenue.

- Fastest-growing Region: Asia Pacific, driven by a large, underserved population and gradual improvements in diagnostic access across key economies.

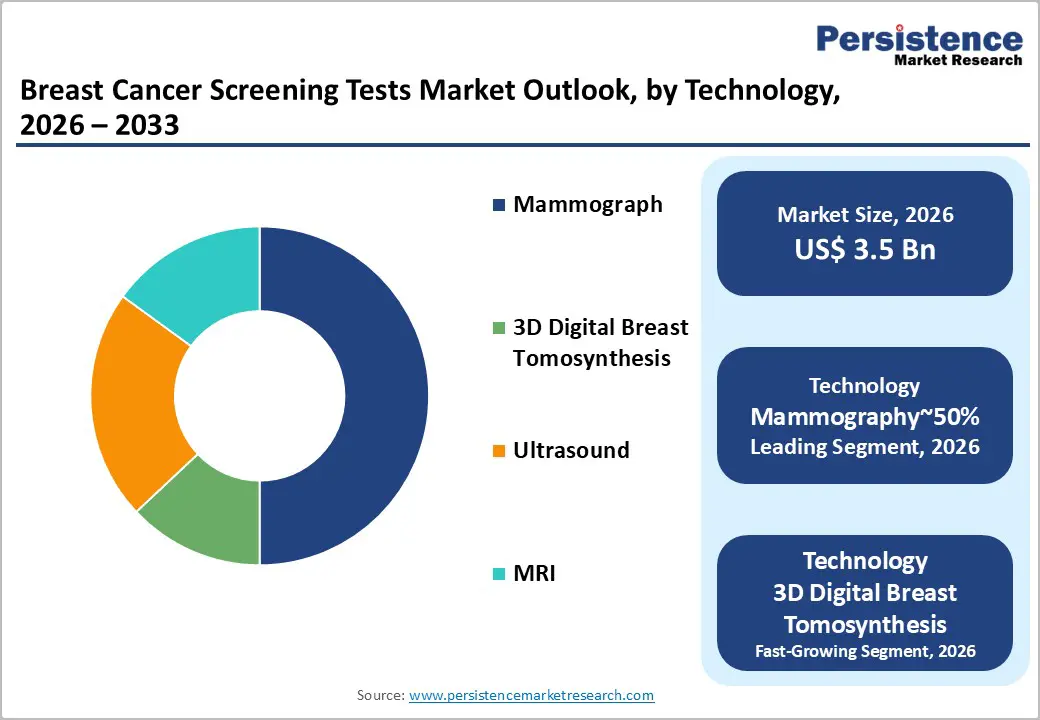

- Leading Test Type: Imaging tests are expected to remain the leading segment with roughly 75% share, driven by digital breast tomosynthesis adoption and integrated multi-modality workflows.

- Leading Technology: Mammography is anticipated to remain the dominant technology, accounting for around 60% utilization, supported by its role in national screening programs and routine diagnostics.

| Report Attribute | Details |

|---|---|

|

Breast Cancer Screening Tests Market Size (2026E) |

US$3.5 Bn |

|

Market Value Forecast (2033F) |

US$5.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Breast Imaging

Technological advancements in breast imaging, particularly the adoption of 3D mammography, have become a core driver of growth in the breast cancer screening market. Unlike conventional 2D imaging, 3D systems provide layered visualization that reduces tissue overlap and improves lesion conspicuity, especially in dense breast tissue. This directly addresses long-standing diagnostic blind spots that previously led to missed or ambiguous findings. The clinical value of clearer anatomical separation has shifted provider preference toward advanced imaging platforms in routine screening workflows. Hospitals and diagnostic centers increasingly view these systems as a standard-of-care upgrade rather than an optional enhancement. This transition is reinforced by the need for higher diagnostic confidence and more consistent screening outcomes across large patient populations.

Advancements in breast imaging, particularly with the adoption of 3D mammography, are driving growth in the breast cancer screening market. Unlike 2D imaging, 3D imaging provides layered visualization, improving lesion visibility and addressing diagnostic blind spots, particularly in dense breast tissue. This has shifted provider preferences, making advanced systems a standard in screening workflows rather than an optional upgrade.

These innovations not only enhance clinical performance but also improve operational efficiency. Clearer images reduce callbacks, lowering costs and patient anxiety, while software tools support radiologists in managing increasing volumes with greater accuracy. This cycle of improved detection and streamlined workflows strengthens the case for technological upgrades. In May 2025, Hologic introduced the Genius AI Detection PRO mammography solution, which reduces reading time by 24%, improves specificity, and aids early cancer detection, leading to better patient outcomes.

Risk of Overdiagnosis and False Positives

Overdiagnosis and false positives remain key challenges in breast cancer screening, as highly sensitive tests may detect slow-growing lesions that don't require intervention. This creates ethical dilemmas and clinical inertia, as providers balance the risks of overtreatment against the benefits of early detection. False positives also increase patient anxiety, reduce adherence to screening, and strain trust in programs.

At the system level, overdiagnosis complicates reimbursement and delays regulatory approval, especially for innovations in genomics and liquid biopsy. Payers prioritize clinical significance, raising the bar for new tools to demonstrate meaningful outcomes. Divergent screening guidelines and value-based care models further fragment demand and slow adoption of high-sensitivity technologies, lengthening procurement cycles and elevating costs for manufacturers.

Personalized Screening Models Powered by AI Risk Stratification

AI-driven personalized risk stratification is reshaping breast cancer screening by shifting practice away from uniform, age-based protocols toward precision prevention grounded in individualized risk profiles. Image-based AI models extract latent radiomic patterns from routine mammograms, enabling earlier and more accurate identification of women who carry disproportionate clinical risk. This transition supports differentiated screening intervals and modality selection, improving pathway efficiency while preserving clinical safety. By triaging low-risk cohorts and prioritizing higher-risk patients, providers can rebalance radiology workloads and improve throughput without compromising detection quality. The model aligns with population health objectives by concentrating resources where marginal clinical benefit is highest. It also creates a scalable software-led growth avenue for imaging vendors and digital health platforms embedded in routine screening workflows.

Momentum is growing around platforms that combine image-based risk scores with patient density, clinical history, and broader context to guide care pathways. These systems streamline risk stratification, imaging selection, and care navigation, reducing unnecessary procedures and improving outcomes for high-risk patients. Integration with EHRs and reporting systems enhances clinical adoption by minimizing workflow friction and fostering shared decision-making among radiologists, clinicians, and patients.

In resource-constrained areas, portable AI-enhanced ultrasound and low-infrastructure imaging expand access to screening. The convergence of AI risk engines and multimodal data supports personalized screening, driving growth in both mature and emerging healthcare markets. In June 2025, Clairity, Inc. received FDA De Novo authorization for CLAIRITY BREAST, an AI platform that predicts 5-year breast cancer risk from routine mammograms, enabling tailored, earlier intervention for diverse populations.

Category–wise Analysis

Test Type Insights

Imaging is expected to dominate, accounting for around 75% of revenue in 2026, driven by its role in organized screening programs and hospital radiology workflows. Digital breast tomosynthesis is set to replace conventional 2D mammography, offering better lesion visibility, fewer recalls, and faster throughput in high-volume centers. Contrast-enhanced mammography is gaining traction as an alternative for high-risk triage and staging, particularly in integrated radiology suites. Hardware-integrated decision support is transitioning from adjunct software to embedded tools, improving accuracy and efficiency for radiologists. Multi-modality pathways, combining mammography, targeted ultrasound, and advanced imaging, are becoming standard in large diagnostic centers, reducing the time from screening to diagnosis. Decentralized screening, including portable ultrasound, is expanding access in underserved populations.

Blood markers and liquid biopsies are expected to grow rapidly due to demand for non-invasive monitoring, early detection, and therapy matching. Companion diagnostics, using blood-based genomic profiling, will increasingly guide treatment selection and track response. Multi-cancer early detection platforms that use methylation signatures are advancing from trials to clinical use, thereby improving specificity. Circulating tumor DNA for recurrence surveillance is becoming integral to post-treatment care, enabling earlier interventions. Faster hospital-based processing and streamlined workflows will enhance physician adoption and patient adherence in high-risk groups.

Technology Insights

Mammography is expected to dominate, comprising about 60% of modality-level utilization due to its key role in national screening programs and diagnostic workflows. The technology will evolve from conventional 2D setups to integrated 3D platforms, featuring synthetic 2D reconstruction, faster acquisition times, and embedded decision support to sustain throughput in high-volume centers. Cloud-enabled reading environments will expand the workforce by enabling distributed reporting, while prioritization tools will improve case triage and reading efficiency in resource-constrained settings. Patient-centric design, such as adaptive compression and ergonomic improvements, will boost adherence in repeat screenings. Service-based deployment models and lifecycle upgrades will support ongoing replacement cycles, cementing mammography’s position as the primary tool for early detection.

3D digital breast tomosynthesis is projected to be the fastest-growing imaging technology, driven by its superior lesion visibility in dense tissue and its ability to reduce false positives due to tissue overlap. Health systems will prioritize tomosynthesis to enhance diagnostic confidence and reduce downstream diagnostic burdens, especially in high-density populations. Integrated reconstruction engines that generate 2D views from 3D data will streamline workflows and preserve low-dose protocols. Tomosynthesis-guided interventions will improve targeting accuracy, and edge-based processing combined with cloud analytics will enable real-time triage and performance monitoring, positioning tomosynthesis as the next standard in organized screening and diagnostic pathways.

Regional Insights

North America Breast Cancer Screening Tests Market Trends

North America is expected to remain the leading region, supported by a highly developed screening ecosystem, early adoption of AI-enabled diagnostics, and strong payer coverage across preventive care pathways, accounting for 44% of the global market share in 2026. The region benefits from dense networks of accredited imaging centers, large-scale population screening programs, and rapid clinical uptake of advanced modalities such as digital breast tomosynthesis, automated breast ultrasound, and MRI for high-risk cohorts. Regulatory direction is likely to continue shaping demand, as patient notification requirements around breast density and expanded eligibility for routine screening increase diagnostic volumes and downstream use of supplemental imaging. Technology vendors are prioritizing workflow automation, decision support, and interoperability with hospital IT systems to address radiologist shortages and throughput constraints.

The U.S. is expected to anchor regional performance due to the scale of its screening infrastructure, payer-driven preventive coverage, and accelerated FDA pathways for AI-based risk stratification tools. Canada is anticipated to expand organized screening programs with greater standardization across provinces, supporting wider adoption of adjunct imaging for dense breast populations. Mexico is likely to see gradual capacity expansion through public–private partnerships aimed at improving access to mammography and diagnostic follow-up in urban centers. Across the region, market momentum is expected to be reinforced by continued clinical validation of predictive imaging, integration of non-invasive adjunct tests, and health system investments in digital screening pathways.

Europe Breast Cancer Screening Tests Market Trends

Europe’s breast cancer screening market is expected to remain mature but steadily grow, driven by centralized public healthcare systems and coordinated policies in key economies such as the U.K., Germany, and France. Regional demand will be shaped by regulatory harmonization under the European Commission’s Breast Cancer Initiative, aligning screening protocols with higher-sensitivity technologies. The shift toward digital breast tomosynthesis over standard mammography will reshape procurement priorities, favoring higher-capex platforms that offer better diagnostic yield. Cost-effectiveness thresholds set by national health technology assessment bodies will continue to moderate rollout, emphasizing solutions with strong evidence on recall reduction and workflow efficiency. Market competition remains concentrated among a few established med-tech suppliers with strong public-sector ties.

Germany is expected to lead in hardware upgrades, supported by its large-scale screening programs and hospital capital expenditure capacity. The U.K. will continue as a testbed for AI deployment in NHS screening, influencing reimbursement for algorithm-assisted reading. France will focus on digital workflow modernization and quality assurance across regional centers. Nordic countries will maintain high participation through mobile units and standardized recall pathways, while Eastern Europe will expand access as infrastructure improves. Overall, the market growth will be driven by evolving guidelines, radiologist capacity constraints, and selective reimbursement of AI-supported screening models.

Asia Pacific Breast Cancer Screening Tests Market Trends

Asia-Pacific is expected to be the fastest-growing region in the breast cancer screening market, driven by a large, underserved population and gradual improvements in diagnostic access across key economies. Demand is likely to be driven by the rapid expansion of healthcare infrastructure, with public-sector programs in China anticipated to strengthen tiered oncology networks and extend organized screening to lower-tier cities and semi-urban regions. Japan is expected to function as a regional technology anchor, with domestic manufacturers advancing high-resolution mammography and ultrasound platforms that set performance benchmarks for the wider market.

Manufacturing depth across China and Southeast Asia is likely to sustain the availability of cost-efficient imaging systems, supporting broader penetration of ultrasound-based screening in populations with higher breast density. In India, private hospital networks are expected to continue bundling screening services with preventive health packages, thereby reinforcing demand for self-pay and employer-sponsored health check programs.

China is anticipated to drive screening volumes through mobile and community-based deployment models, with AI-supported triage improving throughput in radiologist-constrained settings. India is likely to remain the primary access-expansion frontier, where portable, lower-cost imaging systems support decentralized screening in district hospitals and outreach camps. Japan and South Korea are expected to lead the adoption of advanced ultrasound and tomosynthesis within structured screening pathways, reflecting higher technology readiness and reimbursement maturity. Southeast Asian markets are likely to see accelerated uptake through private-sector hospital chains and medical tourism-led diagnostics, positioning the region as a priority growth corridor for global imaging and AI vendors.

Competitive Landscape

The breast cancer screening market exhibits a medium level of concentration, with the top four players, Hologic, GE HealthCare, Siemens Healthineers, and Fujifilm, capturing approximately 60–65% of imaging hardware revenue. These established multinationals leverage comprehensive product portfolios, global distribution networks, and robust R&D investments, covering mammography, 3D tomosynthesis, ultrasound, MRI, and biopsy solutions. Hologic leads in 3D mammography and localization, GE HealthCare in Automated Breast Ultrasound (ABUS) and contrast-enhanced biopsy, Siemens in MRI/CT integration, and Fujifilm in high-resolution digital mammography, particularly across Asia Pacific.

The remaining market is fragmented, dominated by specialized biotech and diagnostic software firms targeting liquid biopsy, genomic testing, and AI-driven risk assessment. Key innovators include Myriad Genetics, Exact Sciences, Natera, Guardant Health, Volpara Health, and Lunit, while startups such as Niramai, Delphinus Medical Technologies, Gabbi, and Koning Corporation address niche gaps such as non-invasive, radiation-free, or rapid 3D imaging solutions. Market positioning increasingly relies on ecosystem strategies, where major hardware players integrate AI and molecular diagnostics, generating higher switching costs and reinforcing end-to-end hospital adoption.

Key Industry Developments:

- In December 2025, Lunit presented new AI evidence for cancer screening and breast density-driven risk modeling at RSNA 2025. The showcased data support advanced risk prediction models, contributing to precision medicine approaches that refine screening strategies and improve outcomes.

- In December 2025, DeepHealth launched the Breast Suite, a modular AI-powered platform integrating detection, density assessment, risk stratification, and workflow tools. It increases detection rates by 21% (including in dense breasts and diverse groups), elevates generalist performance, and enables earlier stage shifting through prioritized alerts and safeguards.

- In December 2025, Astrin Biosciences launched Certitude Breast, the first non-imaging, blood-based test for early breast cancer detection using deep proteomics and AI. Offering 92% sensitivity and >99.9% negative predictive value, it provides a non-invasive complement to mammography, particularly beneficial for dense breasts and reducing unnecessary procedures.

Companies Covered in Breast Cancer Screening Tests Market

- Hologic, Inc.

- GE HealthCare

- Siemens Healthineers

- Philips Healthcare

- Fujifilm Holdings

- Canon Medical

- Roche Diagnostics

- Guardant Health

- Exact Sciences

- Illumina Inc.

- Hitachi Medical

- Lunit

- iCAD, Inc.

- RadNet / DeepHealth

- Natera Inc.

Frequently Asked Questions

The global breast cancer screening tests market is projected to be valued at US$3.5 billion in 2026 and is expected to reach US$5.8 billion by 2033, driven by technological advancements in imaging and the expansion of organized screening programs.

Growth is fundamentally driven by the clinical adoption of advanced imaging technologies such as 3D mammography (digital breast tomosynthesis), which provide superior lesion detection, reduce false positives, and improve workflow efficiency, thereby strengthening the standard of care in routine screening.

The global breast cancer screening tests market is forecast to grow at a CAGR of 7.5% from 2026 to 2033, reflecting sustained demand from aging populations and improved access to screening.

North America is the leading regional market, accounting for approximately 44% of the global revenue, supported by a highly developed screening ecosystem, early adoption of AI-enabled diagnostics, strong payer coverage, and dense networks of accredited imaging centers.

The key players include Hologic, Inc., GE HealthCare, Siemens Healthineers, Fujifilm Holdings, and Roche Diagnostics.