- Medical Devices

- Breast Lesion Localization Methods Market

Breast Lesion Localization Methods Market Size, Share, and Growth Forecast, 2026 - 2033

Breast Lesion Localization Methods Market by Localization Method (Wire, Radioisotope, Magnetic Tracers, Others), End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Others), Lesion Type (Non-Palpable, Palpable), and Regional Analysis for 2026-2033

Breast Lesion Localization Methods Market Share and Trends Analysis

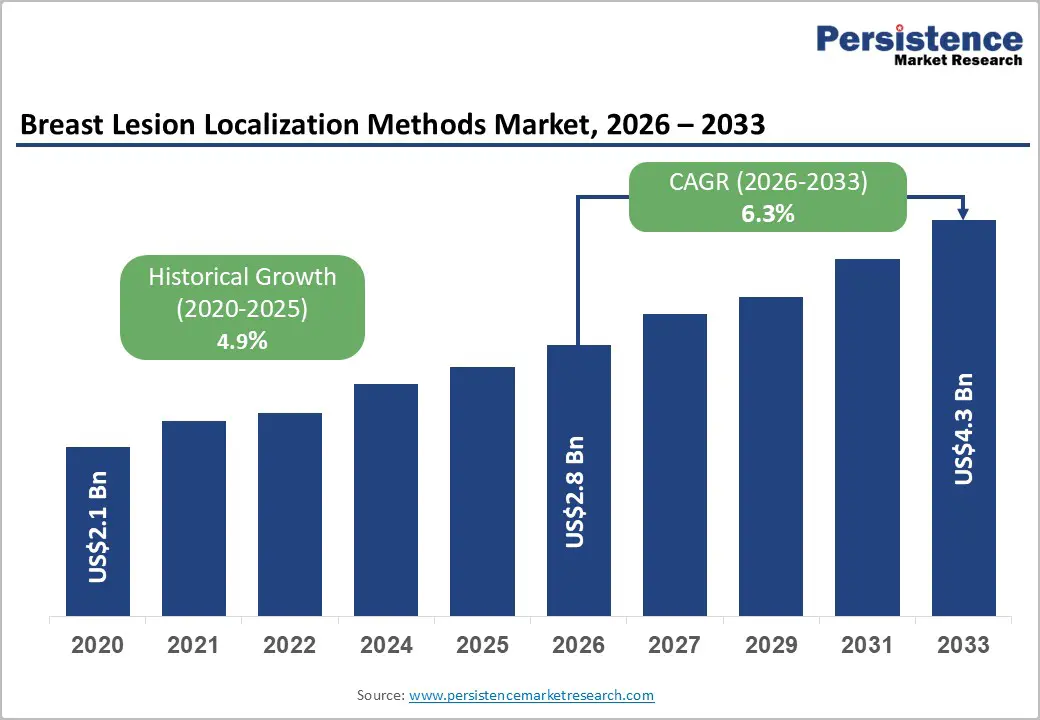

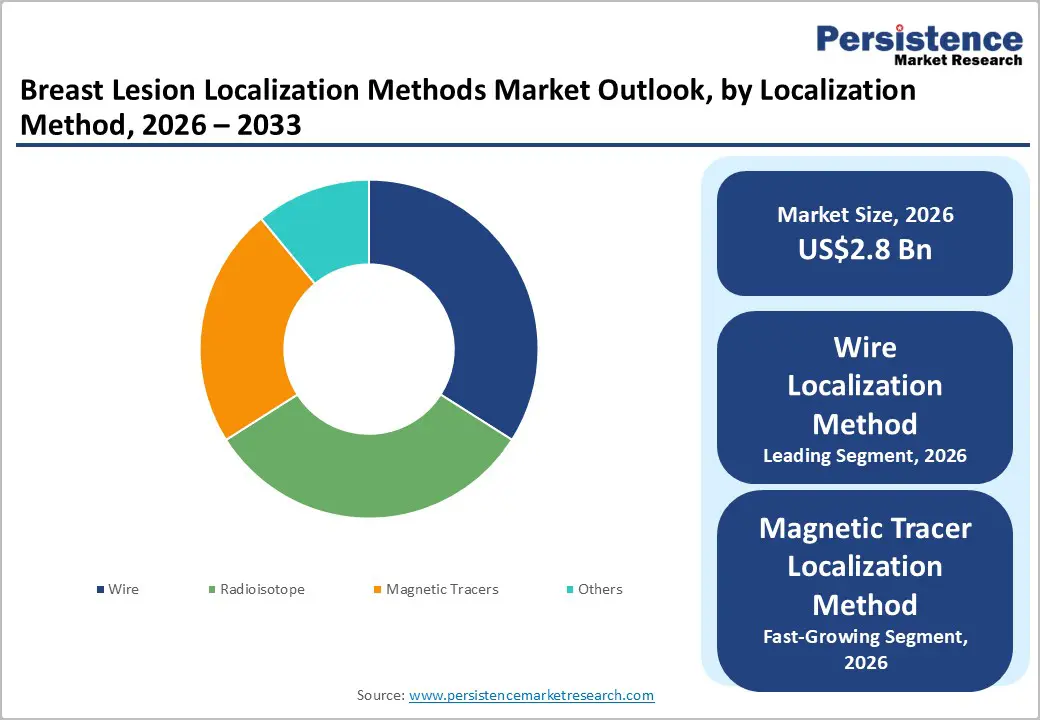

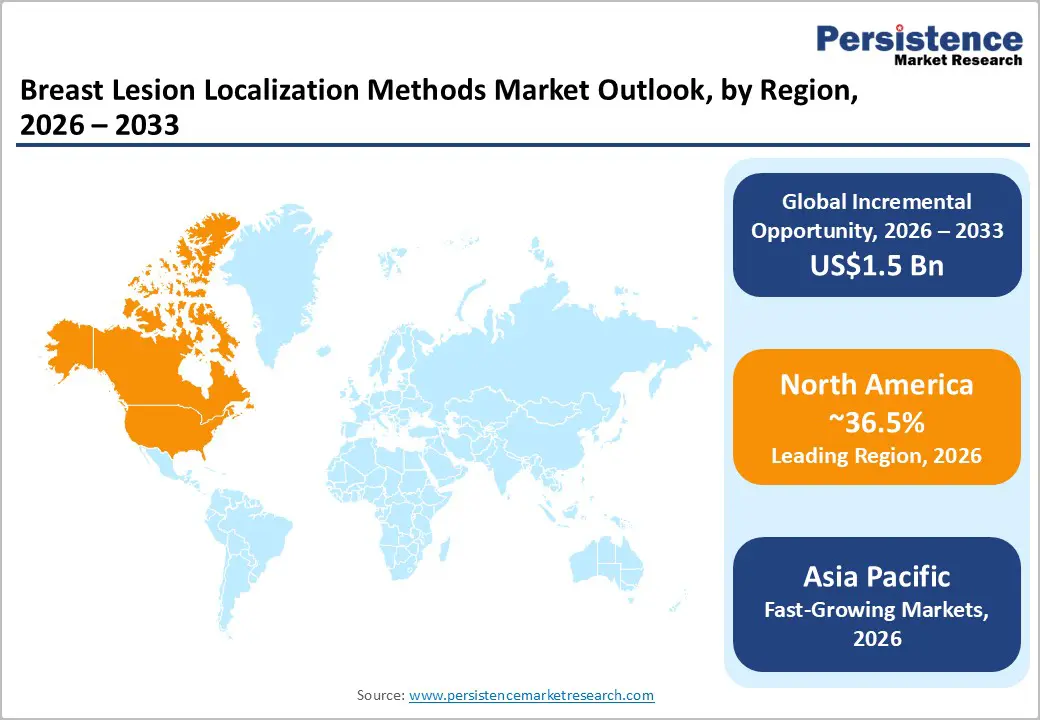

The global breast lesion localization methods market size is likely to be valued at US$ 2.8 billion in 2026, and is projected to reach US$ 4.3 billion by 2033, growing at a CAGR of 6.3% during the forecast period 2026−2033.

The market's sustained expansion reflects a convergence of rising global breast cancer incidence, rapid adoption of minimally invasive surgical techniques, and the increasing integration of image-guided localization technologies in clinical workflows. Furthermore, favorable reimbursement frameworks in developed economies, growing awareness campaigns, and infrastructure investments in oncology centers across emerging economies are collectively accelerating market penetration during the forecast period.

Key Industry Highlights

- Dominant Region: North America is set to dominate with nearly 36.5% market share in 2026, fueled by its robust healthcare infrastructure, high awareness levels, and favorable reimbursement policies.

- Fastest-growing Market: Asia Pacific is poised to be the fastest-growing market through 2033, due to rising awareness about breast cancer and widening adoption of advanced medical technologies.

- Leading & Fastest-growing Product Type: Wire localization is expected to command approximately 34.5% revenue share, while magnetic tracer is likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing End-User: Hospitals are slated to capture roughly 61.4% revenue share in 2026, whereas ambulatory surgical centers (ASCs) are expected to grow the fastest over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

|

Breast Lesion Localization Methods Market Size (2026E) |

US$ 2.8 Bn |

|

Market Value Forecast (2033F) |

US$ 4.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Global Breast Cancer Burden and Screening Expansion

Governments across North America, Europe, and Asia Pacific are expanding national breast screening programs to detect smaller and non-palpable lesions at earlier stages. Healthcare providers are relying on accurate localization methods to guide breast conserving surgeries and improve clinical outcomes. The World Health Organization (WHO) reports that about 2.3 million women were diagnosed with breast cancer in 2022, with global incidence rising by nearly 14% over the past decade. This increase reflects improved detection, stronger reporting systems, and persistent risk factors, which is reinforcing the need for effective screening and early intervention strategies.

For stakeholders, these trends are signaling sustained demand for precise and scalable localization technologies.

Rising screening volumes are driving adoption of advanced localization methods, including wireless and magnetic systems that enhance patient comfort and surgical accuracy. Device developers are focusing on innovation to improve usability, reduce procedural complexity, and support higher throughput in clinical settings. Hospitals and diagnostic centers are integrating these technologies to manage increasing caseloads more efficiently. Policymakers are supporting adoption through reimbursement expansion and targeted training programs for clinicians.

Companies that align product development with screening infrastructure and public health priorities are strengthening their market position and unlocking long term growth opportunities.

Increasing Government and Institutional Healthcare Investment in Oncology Infrastructure

Public sector investment is accelerating adoption of advanced localization systems by strengthening cancer diagnosis and treatment infrastructure. In the United States, the National Cancer Institute (NCI) is funding research and development for surgical oncology tools, while hospitals are procuring these technologies to improve procedural precision. In Europe, the European Union (EU) is implementing Europe’s Beating Cancer Plan to enhance early detection and care delivery through 2027.

Across Asia Pacific, governments such as China are expanding screening networks and oncology centers. These efforts are equipping healthcare systems with modern equipment and trained personnel, which is enabling wider use of localization methods.

These investments are driving hospital procurement and opening growth opportunities in emerging markets. Healthcare facilities are integrating localization technologies into routine workflows to improve surgical accuracy and support breast conserving procedures. Developers are collaborating with public institutions to tailor solutions for high volume environments and resource constrained settings. Regions such as India, Southeast Asia, and Latin America are building new hospitals, which is increasing procedural capacity. Companies that align product design with public health priorities and scalable deployment models are strengthening market access and long term growth potential.

High Cost of Advanced Localization Technologies and Budget Constraints

Wire free localization systems are facing adoption barriers due to high device and per procedure costs, particularly in lower middle income regions. Public hospitals across Asia Pacific, Latin America, and Sub-Saharan Africa are operating under constrained budgets and are prioritizing lower cost alternatives such as wire guided methods. Premium pricing for technologies such as magnetic seed systems is limiting uptake, as healthcare providers focus on essential tools to manage expenses. This dynamic is slowing the transition to advanced localization techniques despite their clinical advantages.

Weak reimbursement structures are further restricting access, as many emerging economies lack funding mechanisms to support advanced procedures. Governments are limiting subsidies for imported devices, which is increasing out of pocket costs for patients and delaying adoption by providers. Manufacturers are exploring tiered pricing and local partnerships to improve affordability, but progress is dependent on supportive policy frameworks. Companies that invest in cost efficient designs and regional production strategies are better positioned to expand in high demand markets while addressing access gaps.

Stringent Regulatory Requirements and Approval Timelines

Regulatory authorities classify breast localization devices as Class II or Class III medical devices and enforce rigorous approval pathways across major markets. Agencies such as the United States Food and Drug Administration (FDA), the European Medicines Agency (EMA), and the Pharmaceuticals and Medical Devices Agency (PMDA) in Japan are requiring detailed submissions for 510(k) clearance or Premarket Approval (PMA). Manufacturers are conducting extensive testing, clinical studies, and risk assessments to demonstrate safety and efficacy. These requirements are ensuring patient protection and product reliability, but they are extending development timelines and increasing compliance costs. For companies, early regulatory alignment is improving approval success and reducing delays.

Ongoing compliance obligations are creating challenges, particularly for smaller innovators. The EU Medical Device Regulation (MDR) is raising expectations for quality systems, traceability, and post market surveillance. Firms are facing higher validation expenses, which is limiting the ability of new entrants to compete with established players. While some regulatory harmonization is taking shape, regional complexities remain significant. Larger companies are managing these demands through scale and resources, while startups are pursuing partnerships to navigate approval pathways.

Organizations that invest in robust regulatory strategies and adaptive compliance systems are strengthening market access while mitigating operational risk.

Integration of Artificial Intelligence and Imaging Technologies

Artificial intelligence (AI)-driven imaging analysis is integrating with breast localization workflows and creating a strong commercial opportunity. Developers are embedding AI into mammography and ultrasound platforms from providers such as iCAD, Hologic, and GE HealthCare to improve lesion detection and guide precise marker placement. These systems are enhancing visualization for surgical planning, which is improving accuracy and procedural efficiency. Healthcare providers are adopting integrated solutions to optimize clinical outcomes and streamline workflows. Companies that lead in this convergence are differentiating their offerings through data driven capabilities and advanced decision support.

Early adopters are securing premium positioning by delivering faster procedures and higher rates of clear surgical margins. Hospitals and diagnostic centers are prioritizing these systems for long term cost efficiency and improved patient outcomes. Vendors are tailoring platforms to suit varied clinical environments, from large urban hospitals to regional facilities. Strategic partnerships and software enhancements are accelerating deployment and adoption across markets. Organizations that invest in AI enabled ecosystems are strengthening competitiveness and unlocking sustained growth opportunities in oncology care.

Rising Adoption of Outpatient and ASCs

Healthcare systems are shifting toward value based care and cost control, which is accelerating the movement of breast localization procedures from hospital operating rooms to ambulatory surgical centers and outpatient facilities. These settings are offering lower operational costs and faster patient throughput, making them attractive for routine breast surgeries. ASCs are prioritizing tools that support quick setup and efficient workflows, and wire free localization devices are aligning well with these needs due to flexible scheduling and minimal infrastructure requirements.

Manufacturers are designing portable and easy to use systems that fit decentralized care models. For stakeholders, this shift is signaling a structural change in care delivery that favors compact and efficient technologies.

Growth in ASCs is creating targeted opportunities for companies that adapt product and go to market strategies. Developers are supporting adoption through focused training programs and tailored device designs that improve usability in high volume settings. Surgeons are benefiting from simplified logistics, while facilities are reducing costs without compromising clinical outcomes. Partnerships with ASC networks are enabling customization and strengthening long term relationships.

Reimbursement policies are also encouraging outpatient care, which is reinforcing this transition. Companies that align with these evolving care pathways are improving market penetration and positioning for sustained growth.

Category-wise Analysis

Localization Method Insights

Wire localization is set to be the leading segment, accounting for about 34.5% of the total market revenue share due to its reliability and cost efficiency. Surgeons are inserting a thin wire to mark lesion location before surgery, which supports accurate excision across varied clinical settings. This method is delivering consistent outcomes and remains widely used in facilities with limited access to advanced technologies. Patients may experience discomfort and occasional wire displacement, yet providers are favoring this approach because it is simple and affordable. For several healthcare systems, wire localization remains a practical standard where budget constraints shape technology adoption.

Magnetic tracer and radioisotope-based methods are likely to emerge as the fastest-growing segment from 2026 to 2033, driven by demand for minimally invasive and precise solutions. These techniques allow surgeons to localize lesions without external wires, which improves scheduling flexibility and patient comfort. Radioisotope approaches are enhancing accuracy and reducing reoperation rates, particularly for non-palpable lesions, while supporting better cosmetic outcomes.

Adoption is requiring specialized equipment, trained personnel, and adherence to radiation safety protocols, which can limit uptake in some settings. Advances in low dose isotopes and simplified workflows are improving feasibility, positioning these technologies for broader use in advanced care environments.

End-User Insights

Hospitals are poised to be the top end-users in 2026, accounting for about 61.4% of the breast lesion localization methods market revenue share, owing to high patient volumes and advanced clinical infrastructure. These facilities are serving as primary centers for cancer diagnosis and treatment, where precise localization is essential for achieving clear surgical margins. Multidisciplinary teams, including radiologists and oncologic surgeons, are using imaging systems and techniques such as wire guided and magnetic seed localization to improve outcomes.

Hospitals are investing in training and workflow optimization to enhance efficiency and reduce complications. For manufacturers, this segment is offering stable demand driven by institutional procurement and complex care requirements.

Ambulatory surgical centers are anticipated record the fastest 2026-2033 growth, backed by a robust demand for cost-efficient and patient-focused care. These centers are delivering outpatient procedures with shorter recovery times and lower treatment costs compared to hospitals. ASCs are adopting advanced localization tools such as wireless seeds and portable imaging systems to enable precise interventions in streamlined settings. Healthcare networks are expanding ASC presence to improve access and operational efficiency in breast cancer management.

Companies that tailor solutions for outpatient environments are strengthening their position as care models shift toward decentralized and value driven delivery.

Regional Insights

North America Breast Lesion Localization Methods Market Trends

North America is projected to hold approximately 36.5% of the breast lesion localization methods market share in 2026, supported by advanced healthcare infrastructure and strong screening awareness. Providers are operating integrated facilities that combine imaging and surgical technologies to enable precise interventions. Education programs are encouraging early detection, while clinicians are adopting proactive care pathways that improve outcomes. Reimbursement frameworks are supporting the use of advanced devices across healthcare networks, which is accelerating adoption.

The United States is leading regional progress through collaboration between research institutions and hospitals to refine techniques such as magnetic seed and radar based localization. This environment is enabling faster validation and deployment of new solutions.

A focus on early diagnosis and personalized treatment is sustaining regional leadership over the forecast period. Policymakers are supporting multidisciplinary care models that integrate radiology, surgery, and pathology to enhance clinical precision. Healthcare institutions are investing in training to manage complex workflows and reduce repeat procedures. The region is also serving as a launchpad for next generation localization technologies, supported by strong innovation ecosystems.

Stakeholders are prioritizing patient-centered approaches, including outpatient care models, to improve accessibility and efficiency. Companies that align with these trends are strengthening their competitive position in a mature but innovation driven market.

Europe Breast Lesion Localization Methods Market Trends

Europe is expected to occupy a strong position in the market for breast lesion localization methods, owing to the region’s established healthcare systems and structured cancer screening programs. Providers are delivering coordinated care through national networks that enable timely diagnosis and treatment. Countries such as Germany, the United Kingdom, and France are adopting advanced localization technologies, supported by clinical research and standardized treatment pathways.

Regulatory alignment under the EMA is simplifying approvals and facilitating cross border adoption. Hospitals are integrating localization methods into routine breast conserving procedures through multidisciplinary clinics that emphasize precision and consistency.

Government initiatives are strengthening cancer care by expanding screening programs and improving access to advanced devices. Early detection campaigns are increasing identification of non-palpable lesions, which is raising demand for accurate localization techniques. Clinicians are using shared data platforms to refine protocols, improve outcomes, and reduce repeat surgeries. Europe is also advancing as an innovation hub, where collaborations between industry and academic institutions are driving development of next generation solutions. Companies that align with policy priorities and clinical standards are strengthening their presence in a region that is shaping global oncology practices.

Asia Pacific Breast Lesion Localization Methods Market Trends

Asia Pacific is poised to become the fastest-growing market for breast lesion localization methods through 2033, driven by rising healthcare investment and stronger awareness of breast cancer screening. Governments are upgrading hospitals with advanced imaging and surgical capabilities while training clinicians to perform complex procedures. China and India are prioritizing oncology networks, which is attracting global companies to establish regional operations.

Urban centers are adopting wireless markers and AI-guided systems, while public programs are extending basic diagnostic tools to wider populations. This combination is improving access to timely diagnosis and supporting sustained market expansion.

Policy support is accelerating adoption through expanded screening initiatives and improved treatment access. Regulators are facilitating approvals for cost effective imports and domestic manufacturing, which is enabling faster deployment of localization technologies. Healthcare providers are collaborating with manufacturers to tailor solutions for high volume settings and reduce dependence on external suppliers. Infrastructure expansion is increasing procedural capacity, while tiered product strategies are addressing varied income levels across the region.

Companies that align with these dynamics are strengthening market penetration and contributing to a more balanced global landscape in cancer care.

Competitive Landscape

The global breast lesion localization methods market structure is moderately consolidated, headlined by Hologic, Endomagnetics, Merit Medical Systems, Savi Medical, and C. R. Bard, accounting for about 55% to 60% of total revenue. These firms are driving competition through product innovation, portfolio expansion, and strategic collaborations. Companies are advancing wireless and magnetic localization systems, integrating AI capabilities, and strengthening global distribution networks to enhance market reach. Their scale and regulatory expertise are enabling faster commercialization and broader adoption across healthcare systems.

Market dynamics are being governed by a mix of established players and emerging entrants offering specialized solutions. Larger firms are leveraging resources to accelerate deployment, while smaller companies are targeting niche applications to differentiate offerings. Investments in research and development (R&D) are improving surgical precision, workflow efficiency, and patient comfort. At the same time, cost considerations are influencing product design and adoption strategies. Organizations that balance innovation with affordability and clinical value are strengthening their competitive position and capturing long term growth opportunities.

Key Industry Developments

- In January 2026, Mercy Medical Center became the first in Iowa to perform breast surgery using SCOUT MD, a radar-based, wire-free breast localization system that improves surgical precision, enables real time tumor mapping, and enhances patient comfort. The technology supports accurate margin assessment and reduces repeat surgeries, marking a shift toward more advanced, and minimally-invasive breast cancer procedures in clinical practice.

- In May 2025, Sirius Medical announced that real world data from the iBRA NET study validated its Pintuition system as a safe and effective surgical marker navigation solution, demonstrating non inferiority to traditional wire localization in breast conserving procedures. The platform enhances precision through real time audio visual guidance and improves workflow efficiency, supporting better surgical outcomes and patient experience.

- In April 2025, GE Healthcare highlighted its latest breast imaging advances, including Pristina Recon DL, an AI powered 3D mammography reconstruction technology that improves image quality and diagnostic confidence without increasing radiation dose. The company is also expanding workflow enhancing tools such as patient assisted compression, automated workflows, and AI driven applications within its Senographe Pristina and broader breast care portfolio.

Companies Covered in Breast Lesion Localization Methods Market

- Hologic, Inc.

- BD (Becton, Dickinson) / Cianna Medical

- Endomagnetics Ltd.

- Merit Medical Systems, Inc.

- Savi Medical, Inc.

- C. R. Bard, Inc.

- Mammotome

- IZI Medical Products

- Argon Medical Devices

- Invacare Corporation

- GE HealthCare Technologies, Inc.

- Siemens Healthineers AG

- Philips Healthcare

- iCAD, Inc.

- IsoAid LLC

Frequently Asked Questions

The global breast lesion localization methods market is projected to reach US$ 2.8 billion in 2026.

The market is driven by rising breast cancer incidence and expanded screening programs that are stoking the demand for precise, minimally invasive techniques.

The market is poised to witness a CAGR of 6.3% from 2026 to 2033.

Major opportunities lie in AI integration with localization workflows to enhance accuracy and efficiency in outpatient settings.

Hologic, Inc., Endomagnetics Ltd., Merit Medical Systems, Inc., Savi Medical, Inc., and C. R. Bard, Inc. are some of the key players in the market.