- Medical Devices

- Breast and Prostate Cancer Diagnostics Market

Breast and Prostate Cancer Diagnostics Market Size, Share, and Growth Forecast, 2026 - 2033

Breast and Prostate Cancer Diagnostics Market by Technology Type (Imaging, Biopsy, Genomic Testing), Test Type (Laboratory Tests, Imaging Tests, PCT Tests), Application (Screening, Diagnostic & Staging, Monitoring), and Regional Analysis 2026 - 2033

Breast and Prostate Cancer Diagnostics Market Size and Trends Analysis

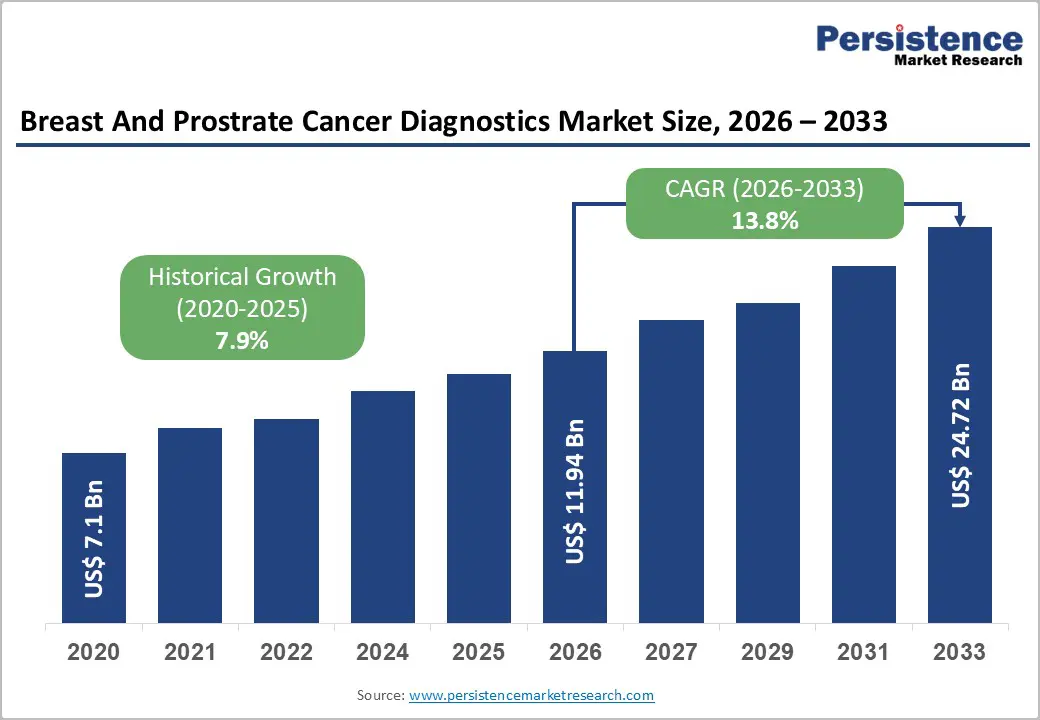

The global breast and prostate cancer diagnostics market size is likely to be valued at US$11.94 billion in 2026 and is expected to reach US$ 24.7 billion by 2033, growing at a CAGR of 13.8% during the forecast period from 2026 to 2033, driven by an accelerating global incidence of oncology cases and a fundamental shift toward precision medicine and early-intervention strategies.

Current market dynamics reflect the integration of artificial intelligence (AI) in diagnostic imaging and the rising adoption of liquid biopsy for non-invasive monitoring. Technological shifts toward genomic testing and liquid biopsies accelerate adoption, while aging populations in key regions amplify volume.

Key Industry Highlights:

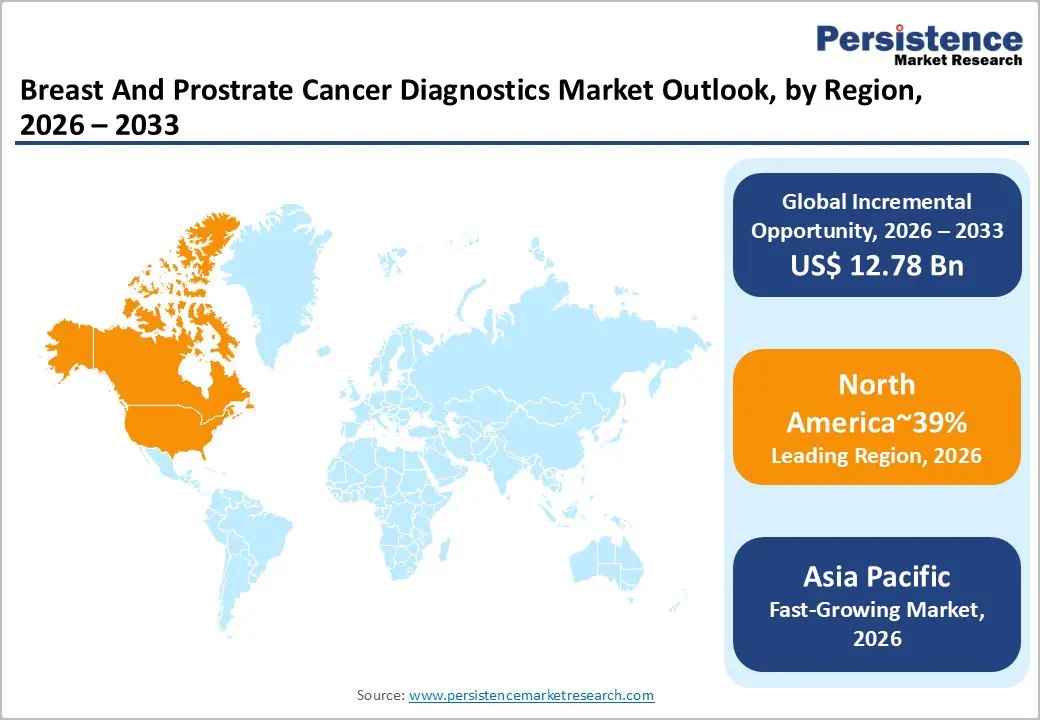

- Leading Region: North America is projected to lead due to high healthcare expenditure accounting for 39% in 2026, advanced cancer screening infrastructure, and widespread adoption of early-detection technologies.

- Fastest-Growing Region: Asia Pacific is anticipated to grow the fastest due to expanding healthcare infrastructure, rising cancer awareness, and government-led screening initiatives.

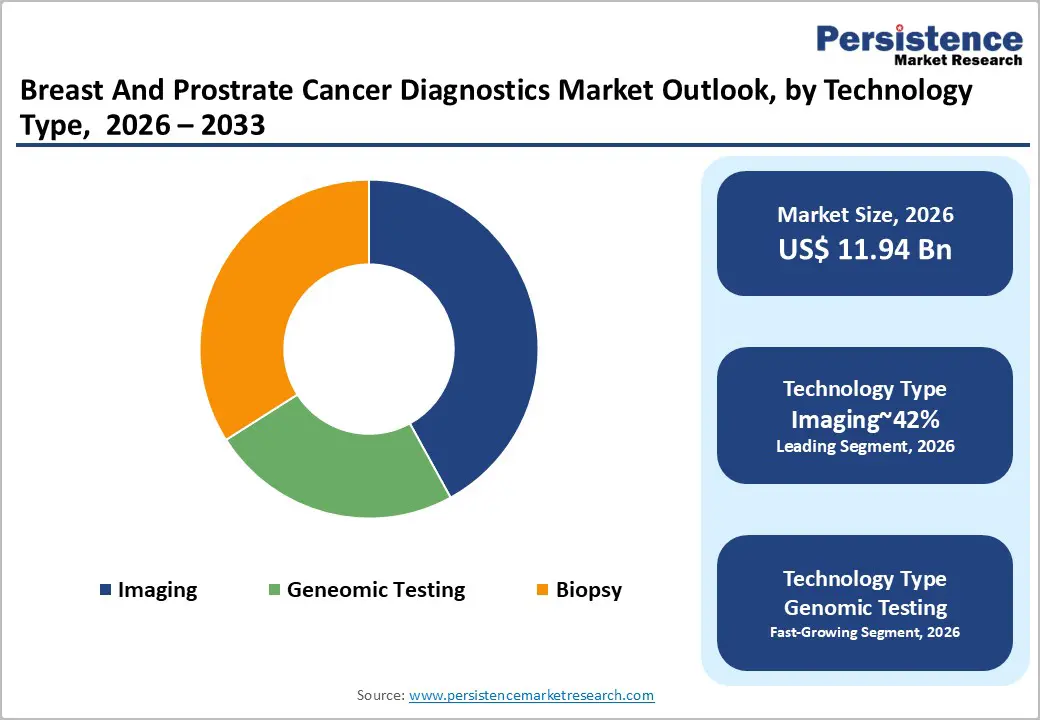

- Leading Technology Type: Imaging technology is expected to lead through high-volume screening programs, strong clinical integration with a share of 42% in 2026, and established reimbursement frameworks across developed markets.

- Leading Test Type: Laboratory tests are projected to dominate for simplicity, accounting for 48% share in 2026, cost-effectiveness, standardized blood-based screening (e.g., PSA testing), and broad functional use across primary and secondary care settings.

| Key Insights | Details |

|---|---|

| Breast and Prostate Cancer Diagnostics Market Size (2026E) | US$11.94 Bn |

| Market Value Forecast (2033F) | US$24.72 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Global Incidence and Epidemiological Shifts

Escalating global cancer incidence is structurally expanding diagnostic service demand. Breast and prostate malignancies dominate global oncological case volumes. Epidemiological transition toward aging populations intensifies screening requirements. Higher life expectancy expands the at-risk demographic cohort. Healthcare systems consequently prioritize early detection infrastructure expansion. Screening protocols increasingly embed routine mammography and PSA assessments. Earlier diagnosis frameworks shift patient flow toward outpatient diagnostics. This dynamic sustains recurring demand across imaging and laboratory platforms.

Rising diagnostic volumes reshape procurement patterns across the value chain. Laboratory networks scale assay capacity and automation capabilities. Imaging centers upgrade to digital mammography ecosystems. Regulatory agencies reinforce population-based screening compliance standards. Reimbursement structures increasingly align with preventive oncology pathways. Biopsy services experience parallel growth in confirmatory testing demand. Equipment manufacturers benefit from recurring consumables utilization. Collectively, demographic pressure embeds durable throughput expansion within oncology diagnostics markets.

Advancements in Precision Oncology and Genomic Testing

Advancements in precision oncology and genomic testing are structurally redefining therapeutic decision frameworks across breast and prostate cancer markets. The diffusion of next-generation sequencing and advanced molecular diagnostics has displaced empiric treatment models with mutation-guided stratification pathways embedded within clinical protocols. Regulatory authorities increasingly formalize companion diagnostics as prerequisites for targeted therapy eligibility, integrating genomic validation directly into drug approval architectures. Biomarker identification, including alterations in tumor suppressor and DNA repair pathways, now governs access to high-value targeted agents and reshapes prescribing algorithms. This regulatory and clinical convergence elevates diagnostic testing from an optional adjunct to a mandatory gatekeeper within oncology care delivery systems.

The integration of multiple cancer early detection platforms further expands the diagnostic value chain by consolidating signal identification into minimally invasive blood-based workflows. These technologies compress diagnostic timelines, redistribute testing toward centralized high complexity laboratories, and intensify data analytics requirements across molecular interpretation platforms. Capital allocation shifts toward sequencing infrastructure, bioinformatics capacity, and compliance-aligned laboratory accreditation systems. Reimbursement models increasingly reflect outcome-linked precision pathways, reinforcing sustained demand for genomic assays while restructuring cost distribution toward advanced diagnostics within oncology treatment budgets.

Barrier Analysis - Socio-Cultural & Gender Sensitivity

Socio-cultural norms and gender sensitivities create structural barriers to oncology screening adherence across multiple markets. Patient reluctance toward male clinicians, particularly for breast examinations and prostate digital rectal assessments, reduces uptake of routine diagnostic protocols. Social stigma associated with cancer testing discourages timely participation in preventive care programs. Cultural perceptions of invasive procedures further limit consent for biopsies and confirmatory diagnostics. Health systems in affected regions face persistent challenges in designing culturally aligned outreach initiatives. Geographic and demographic disparities exacerbate inequitable access to diagnostic services. Collectively, these factors suppress overall screening volumes despite rising epidemiological demand.

The impact extends across both imaging and biopsy workflows, constraining throughput and operational efficiency within oncology care pathways. Limited patient participation affects laboratory utilization rates and imaging equipment deployment planning. Training and staffing requirements must accommodate culturally sensitive care delivery models, influencing human resource allocation. Outreach campaigns often require additional investment in community engagement, education, and gender-matched staffing. These constraints increase per-patient diagnostic costs while limiting value chain efficiency. Structural socio-cultural factors thus embed persistent market friction, reducing overall penetration and delaying timely intervention in breast and prostate cancer detection programs.

Skilled Workforce Shortage

Persistent shortages in skilled radiology professionals are structurally limiting diagnostic throughput across breast and prostate cancer markets. The imbalance between complex imaging demand and the available workforce constrains the timely interpretation of high-resolution mammography and multiparametric MRI scans. Training pipelines fail to match accelerating case volumes, creating systemic bottlenecks in patient flow. Workforce burnout further exacerbates attrition, reducing effective capacity within specialized imaging centers. Recruitment and retention pressures elevate labor cost structures, impacting operational budgets across hospital networks. Tele-radiology and remote interpretation partially mitigate geographic gaps but remain insufficient to resolve aggregate workload imbalances. Regulatory credentialing and certification requirements impose additional temporal constraints on workforce scalability, sustaining structural strain within oncology imaging services.

The shortage also affects advanced in vivo diagnostic modalities, including PET-CT and molecular imaging applications integrated into precision oncology pathways. Limited availability of trained personnel restricts the adoption of multi-modality imaging protocols essential for early detection and therapy monitoring. Operational inefficiencies increase cycle times for complex genomic and imaging integrated workflows. Capital investment in automated image analysis and AI augmentation becomes essential to offset human resource gaps. These constraints embed persistent cost and margin pressures across the diagnostic value chain. Geographic disparities widen as high-demand regions absorb disproportionate professional capacity.

Opportunity Analysis - The Surge of Liquid Biopsy and Non-Invasive Monitoring

The emergence of liquid biopsy and non-invasive monitoring is structurally transforming oncology diagnostic pathways, creating high-value opportunities within breast and prostate cancer care. Analysis of circulating tumor DNA and circulating tumor cells enables earlier detection of disease recurrence and real-time monitoring of treatment response. This capability compresses diagnostic timelines compared with conventional imaging, reshaping clinical decision frameworks and care sequencing. Repeat testing without invasive procedures reduces patient burden and aligns with value-based care models emphasizing longitudinal management. Laboratories and diagnostic networks benefit from scalable testing volumes and recurring service demand, embedding durable growth within high-complexity molecular diagnostics infrastructure.

Adoption of liquid biopsy further restructures the diagnostic value chain by centralizing analytical workflows in high-capacity molecular laboratories. Data interpretation and bioinformatics integration become essential for actionable insights, increasing reliance on automated analytics and skilled personnel. Cost structures shift toward recurring consumables, sequencing reagents, and assay validation, while enabling precision-guided treatment optimization. The approach strengthens alignment with personalized oncology pathways, particularly for metastatic patient management requiring continuous monitoring. Non-invasive monitoring expands market addressable size, enhances throughput efficiency, and accelerates integration of precision diagnostics across regulated oncology care systems.

AI-Integrated Imaging Convergence

The convergence of artificial intelligence with advanced imaging modalities is structurally reshaping diagnostic workflows in breast and prostate oncology. AI algorithms enhance the interpretation of mammography, multiparametric MRI, and PET-CT scans, increasing detection sensitivity while reducing inter-reader variability. Integration within radiology information systems and picture archiving networks streamlines case triage, prioritizes high-risk findings, and accelerates reporting timelines. Hospitals and diagnostic networks leverage AI to optimize operational efficiency, balancing technician workload with throughput demands. The convergence also drives demand for interoperable imaging platforms and standardized data annotation protocols. Investment in AI-capable hardware and software elevates capital intensity but delivers downstream margin improvements through reduced repeat imaging and enhanced diagnostic accuracy. Overall, AI integration is restructuring both clinical and economic dimensions of oncology imaging markets.

Beyond workflow efficiency, AI-enabled imaging convergence supports predictive analytics and longitudinal patient monitoring across therapeutic pathways. Deep learning models correlate imaging phenotypes with genomic profiles, enhancing precision oncology decision-making. Automated lesion segmentation, volumetric assessment, and risk scoring reduce dependency on scarce radiology expertise. Integration of AI outputs into electronic health records facilitates multidisciplinary care coordination and evidence-based treatment planning. Value chains increasingly emphasize data management, algorithm validation, and cybersecurity compliance as critical operational components. Adoption also accelerates innovation in hybrid imaging modalities, including PET-MRI and functional MRI, enhancing early detection capabilities. AI convergence elevates diagnostic quality, optimizes resource allocation, and embeds sustainable scalability within breast and prostate cancer imaging ecosystems.

Category-wise Analysis

Technology Type Insights

Imaging is expected to lead, accounting for approximately 42% share in 2026, underpinned by its entrenched role as the primary frontline screening tool across hospitals, diagnostic centers, and high-volume outpatient facilities. Adoption remains anchored by the non-invasive, high-throughput nature of mammography, ultrasound, and MRI, with providers prioritizing workflow integration, reproducibility, and rapid patient turnaround. Ongoing platform evolution, including AI-enabled image interpretation, cloud connectivity, and automated reporting, continues to reinforce replacement cycles and utilization intensity. Key players such as GE Healthcare, Siemens Healthineers, and Hologic, with their imaging systems and service ecosystems, lock in enterprise workflows and ensure predictable recurring demand.

Genomic testing is expected to be the fastest-growing segment, driven by emerging unmet needs in precision oncology and workflow gaps in therapy selection. Growth is being catalyzed by next-generation sequencing, liquid biopsy platforms, and validated biomarker assays, which materially improve diagnostic personalization, early detection, and monitoring of treatment response. Accelerating adoption is supported by AI-driven analytics, automated sample processing, and interoperability with electronic health records, lowering operational friction for first-time adopters. Brands such as Illumina, Thermo Fisher Scientific, and QIAGEN are expanding platforms and assay portfolios to capture early-cycle demand and embed switching costs. As clinical validation, reimbursement pathways, and laboratory workforce familiarity improve, the segment is expected to outpace overall market growth over the forecast period.

Test Type Insights

Laboratory tests are expected to dominate, accounting for approximately 48% share, underpinned by their entrenched role within routine physical exams and centralized diagnostic laboratory networks. Adoption remains anchored by the cost-efficient, high-throughput nature of blood work and PSA testing, with providers prioritizing scalability, workflow integration, and consistent patient coverage across geriatric and general populations. Ongoing platform evolution, including automated analyzers, digital reporting, and sample tracking systems, continues to reinforce recurring utilization and service contracts. Key players such as Roche Diagnostics, Abbott Laboratories, and Siemens Healthineers, with their laboratory assay portfolios and service ecosystems, lock in enterprise workflows and sustain predictable demand.

Genetic/PCR tests are expected to be the fastest-growing segment in the oncology diagnostics market, driven by emerging demand for high-specificity testing and the increasing adoption of companion diagnostics in precision oncology. Growth is being catalyzed by next-generation sequencing, BRCA and HER2 panels, and point-of-care molecular assays, which materially enhance diagnostic accuracy, treatment selection, and clinical decision timelines. Accelerating adoption is supported by AI-driven interpretation, automated workflow integration, and interoperability with electronic health records, reducing operational friction for new users. Brands such as Illumina, Thermo Fisher Scientific, and QIAGEN are expanding platforms and assay lines to capture early-cycle demand and embed switching costs. As validation, reimbursement, and clinician familiarity improve, this segment is expected to outpace overall market growth.

Regional Insights

North America Breast and Prostate Cancer Diagnostics Market Trends

North America is expected to maintain its position as the leading regional market, accounting for approximately 39% of global revenue in 2026, supported by deep enterprise penetration, advanced healthcare infrastructure, and a robust innovation ecosystem. Adoption is anchored in high-throughput diagnostic workflows, including centralized laboratory automation, AI-integrated imaging, and digital pathology, with providers prioritizing operational efficiency, standardized protocols, and integration across hospital networks. Commercial alignment approaches such as Roche, Abbott, GE Healthcare, Siemens Healthineers, and Hologic lock in enterprise workflows through imaging and laboratory platform portfolios. Platform evolution, including AI-enabled mammography, real-time analytics, and cloud-based data management, continues to intensify utilization and embed long-term replacement cycles, consolidating North America’s leading market position.

The U.S. anchors North America’s oncology diagnostics momentum, accounting for the majority of regional revenue and shaping adoption trajectories through policy, funding, and technology deployment. Regulatory acceleration of breakthrough devices via FDA pathways, combined with substantial National Cancer Institute funding, drives high adoption of AI-assisted imaging and genomic assays. U.S. hospital networks are investing in centralized laboratory platforms, automated workflows, and liquid biopsy integration, reinforcing scale efficiencies and interoperability across diagnostic pathways. As reimbursement alignment and digital adoption expand, the U.S. is set to sustain North America’s market dominance while advancing early adoption of next-generation oncology diagnostics, including precision molecular testing and AI-enabled imaging.

Asia Pacific Breast and Prostate Cancer Diagnostics Market Trends

Asia Pacific is expected to register the fastest growth trajectory, driven by rapid economic development, expanding private healthcare access, and industrial-scale manufacturing capabilities. Adoption is anchored in high-volume screening programs, centralized and decentralized laboratory networks, and integration of molecular and imaging diagnostics across urban and semi-urban centers. Structural growth is reinforced by government initiatives, digital health integration, and platform evolution, including AI-assisted imaging, point-of-care molecular testing, and liquid biopsy deployment. Leading industry players such as Thermo Fisher Scientific, Illumina, and QIAGEN are expanding local laboratory networks, platform offerings, and reagent production, embedding enterprise workflows and enabling early-cycle adoption. Regional scale efficiencies, combined with rising middle-class demand and growing healthcare awareness, are expected to accelerate platform utilization and establish Asia Pacific as a high-growth, investment-driven market for oncology diagnostics.

China anchors Asia Pacific’s growth, accounting for a substantial portion of regional revenue through government-led initiatives, urban hospital expansion, and nationwide cancer screening programs under “Healthy China 2030.” Regulatory approvals from the NMPA for next-generation sequencing and companion diagnostics facilitate rapid adoption of precision oncology workflows, while investments in centralized laboratories, liquid biopsy trials, and AI-enabled imaging platforms strengthen operational throughput and diagnostic reliability. Vendor strategies focus on local partnerships, infrastructure expansion, and workflow integration to support high patient volumes and multi-modality diagnostics. As China continues to prioritize early detection, technology standardization, and scalable laboratory networks, it is expected to sustain Asia Pacific’s leading growth momentum while enabling the regional diffusion of advanced molecular and imaging diagnostics across emerging markets.

Europe Breast and Prostate Cancer Diagnostics Market Trends

Europe is expected to remain a structurally important market in oncology diagnostics, accounting for approximately 30% of global revenue, supported by harmonized public health screening programs, advanced imaging infrastructure, and coordinated regulatory frameworks. Adoption is anchored in AI-enhanced multiparametric MRI, digital pathology integration, and centralized laboratory workflows, with providers prioritizing throughput, clinical reliability, and standardized patient pathways across hospitals and diagnostic centers. Pan-European initiatives, including the Beating Cancer Plan and alignment with IVDR standards, reinforce quality and consistency, while platform evolution, such as AI-assisted imaging analytics, integrated electronic health records, and liquid biopsy pilots, continues to drive utilization intensity. Leading Supplier operating models, including Roche, Abbott, and Siemens Healthineers, consolidate enterprise workflows through imaging and genomic platforms, sustaining predictable demand. Regional harmonization of clinical guidelines and diagnostic protocols further strengthens Europe’s position as a reference market for high-quality, multi-modality oncology diagnostics.

Germany anchors Europe’s market momentum, accounting for a substantial portion of regional revenue through advanced manufacturing, R&D, and clinical program deployment. The Deutsche Krebsgesellschaft (DKG) liquid biopsy pilots and AI-enabled MRI initiatives set benchmarks for early detection and recurrence monitoring, shaping adoption across neighboring countries. Investments through Horizon Europe and targeted public health funding enhance technology diffusion, enabling integration of genomic assays and imaging analytics into standardized workflows. Competitive positioning framework strategies focus on high-value platform portfolios, interoperability, and operational scale, facilitating consistent deployment across hospitals and regional laboratories. As reimbursement frameworks evolve and EMA approvals for next-generation sequencing expand, Germany is projected to sustain Europe’s growth trajectory while advancing the adoption of precision diagnostics.

Competitive Landscape

The global breast and prostate cancer diagnostics market is moderately consolidated, with leadership concentrated among global suppliers such as Roche, Abbott, Thermo Fisher Scientific, and Illumina. These leaders matter due to their extensive functional influence across laboratory testing, imaging, and molecular diagnostics, enabling standardized workflows and interoperability across hospital networks and diagnostic centers. Their technological footprint encompasses AI-enabled imaging platforms, next-generation sequencing, and integrated liquid biopsy solutions, which shape procurement priorities and set performance benchmarks for competitors. Competitive positioning varies across horizontal integration of multi-modality diagnostics, vertical specialization in genomic assays or imaging systems, and niche adoption of emerging technologies such as point-of-care molecular testing. Industry dynamics reflect ongoing platform evolution, consolidation through strategic acquisitions, and expansion of service-led models that reinforce recurring revenue streams and workflow entrenchment. Forward-looking investment is directed toward enhancing automation, digital integration, and multi-site laboratory networks, sustaining structural market leadership while enabling incremental adoption across emerging regional markets.

Key Industry Developments:

- In January 2026, Clairity (US) received FDA De Novo authorization for CLAIRITY BREAST, an image-based platform predicting five-year breast cancer risk from standard mammograms, transforming diagnostics into predictive care.

- In December 2025, Hologic unveiled AI-powered mammography data, showing a one-third reduction in missed cases. Retrospective analysis demonstrated that AI-flagged cancers initially interpreted as negative, enhancing screening sensitivity.

- In September 2025, Stratipath & Visiopharm formed a strategic partnership for AI precision oncology, integrating prognostic AI solutions with advanced biomarker scoring for more accurate early-stage breast cancer analysis.

Companies Covered in Breast and Prostate Cancer Diagnostics Market

- F. Hoffmann-La Roche Ltd

- Abbott Laboratories

- Thermo Fisher Scientific

- Hologic, Inc.

- GE HealthCare Technologies

- Siemens Healthineers

- Illumina, Inc.

- Myriad Genetics

- Philips Healthcare

- Danaher Corp

- QIAGEN N.V.

- Becton, Dickinson and Company (BD)

- Agilent Technologies

- bioMérieux

- Fujifilm Holdings

- MDxHealth

Frequently Asked Questions

The global breast and prostate cancer diagnostics market is projected to be valued at US$11.94 billion in 2026 and is expected to reach US$24.7 billion by 2033, driven by rising cancer incidence, adoption of AI-enabled imaging, and expansion of molecular and liquid biopsy diagnostics across hospital and laboratory networks.

The transition to precision oncology underpins growth by embedding genomic testing, biomarker-guided therapy selection, and companion diagnostics within clinical protocols. Early detection and treatment personalization increase recurring diagnostic demand, integrate AI and molecular platforms into workflows, and incentivize investment in laboratory automation, sequencing infrastructure, and imaging convergence, reinforcing operational throughput across hospitals and diagnostic networks.

The breast and prostate cancer diagnostics market is forecast to grow at a CAGR of 13.8% from 2026 to 2033, reflecting sustained adoption of advanced imaging, genomic assays, liquid biopsy technologies, and workflow automation in both developed and emerging healthcare systems.

Asia Pacific is anticipated to be the fastest-growing regional market, driven by healthcare infrastructure expansion, government-led screening initiatives, rising cancer awareness, and increasing adoption of AI-assisted imaging, point-of-care molecular tests, and centralized laboratory platforms across urban and semi-urban centers.

The breast and prostate cancer diagnostics market is moderately consolidated, with leading players including F. Hoffmann-La Roche Ltd, Abbott Laboratories, Thermo Fisher Scientific, Hologic, Inc., GE HealthCare Technologies, Siemens Healthineers, Illumina, Inc., Myriad Genetics, Philips Healthcare, Danaher Corp, QIAGEN N.V., Becton, Dickinson and Company (BD), Agilent Technologies, bioMérieux, Fujifilm Holdings, and MDxHealth. These companies compete through platform integration, enterprise workflow dominance, and high-complexity diagnostic capabilities.