- Medical Devices

- Breast Tissue Expander Market

Breast Tissue Expander Market Size, Share, and Growth Forecast 2026 - 2033

Breast Tissue Expander Market by Product Type (Saline-filled, Silicone-filled, Air-filled), by Application (Breast Reconstruction, Cosmetic, Others), End-user (Hospitals, Ambulatory Surgical Centers, Specialty & Cosmetic Clinics), by Regional Analysis, 2026 - 2033

Breast Tissue Expander Market Share and Trends Analysis

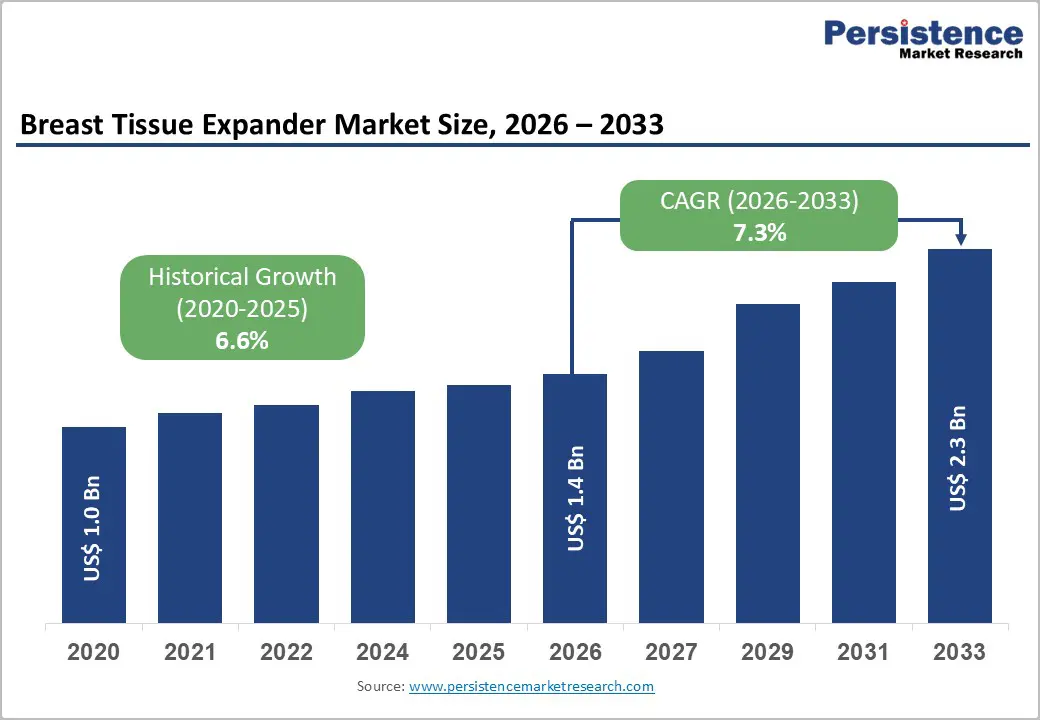

The global breast tissue expander market size is expected to be valued at US$ 1.4 billion in 2026 and projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033. Growth is primarily driven by rising breast cancer incidence and the increasing uptake of post-mastectomy breast reconstruction procedures, supported by improving reimbursement and growing awareness of survivorship quality of life.

Clinical guidelines and advocacy groups increasingly emphasize reconstructive options, while technological advances such as anatomically shaped expanders, integrated ports, and more biocompatible shells enhance clinical outcomes and patient satisfaction. Simultaneously, expanding access to reconstructive and cosmetic surgery in emerging markets is broadening the addressable patient pool, sustaining demand across both hospital and specialty clinic settings.

Key Industry Highlights:

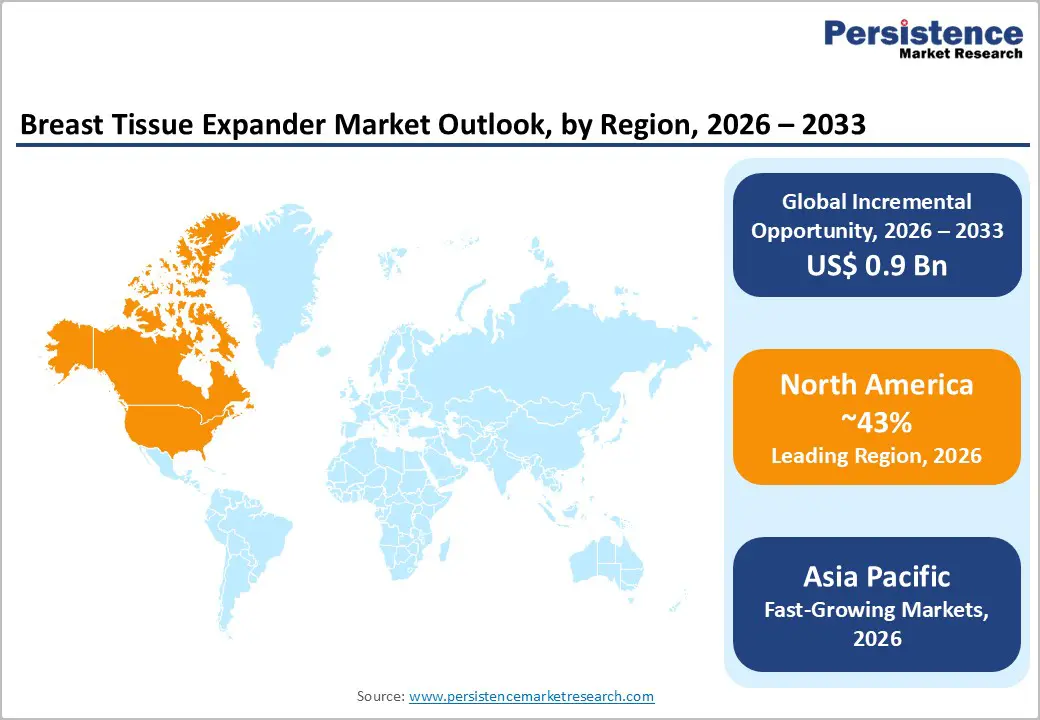

- North America leads the breast tissue expander market with about 43% share in 2025, driven by high breast cancer incidence, strong reimbursement for reconstruction under mandates such as WHCRA, and the presence of major implant manufacturers and comprehensive breast care centers.

- Asia Pacific is the fastest-growing region, benefiting from rising cancer awareness, expanding oncology and plastic surgery capacity in China, Japan, India, and ASEAN, improving health insurance coverage, and the emergence of regional manufacturers offering cost-effective expander solutions.

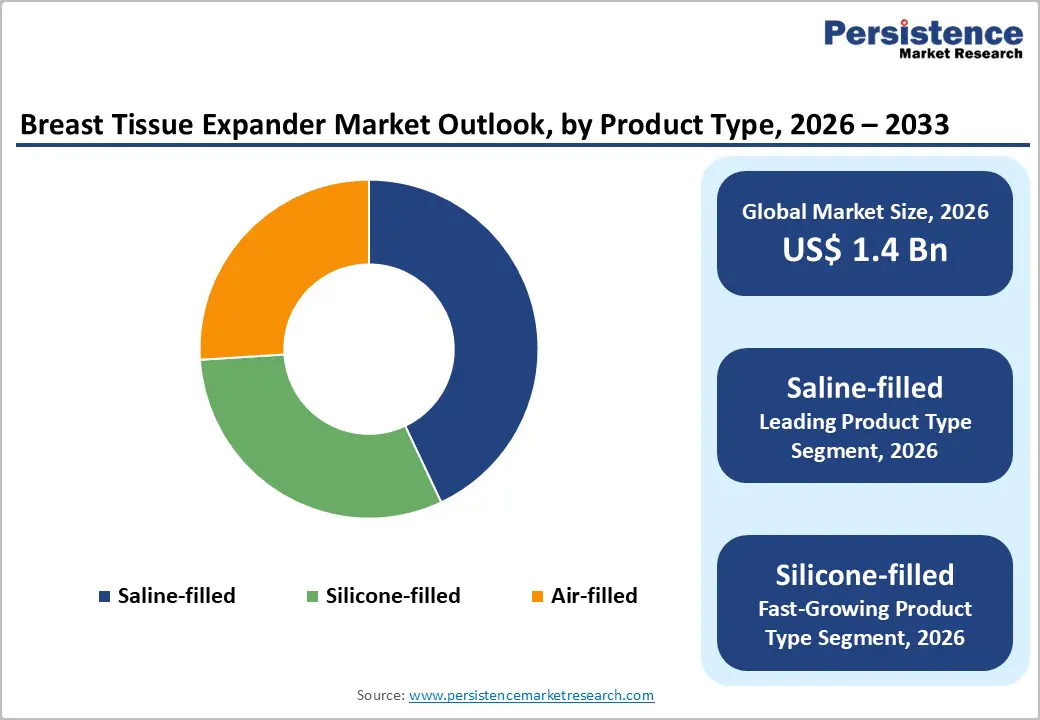

- Within product type, saline-filled expanders dominate with around 43% share in 2025, reflecting their long-standing clinical use, flexibility in expansion, and broad availability across hospitals and cancer centers worldwide.

- Silicone-filled expanders are the fastest-growing product segment, supported by efforts to more closely mimic the final implant’s feel and weight, enhance patient comfort, and improve aesthetic outcomes, particularly in immediate and prepectoral reconstructions.

| Key Insights | Details |

|---|---|

| Breast Tissue Expander Market Size (2026E) | US$ 1.4 billion |

| Market Value Forecast (2033F) | US$ 2.3 billion |

| Projected Growth CAGR (2026 - 2033) | 7.3% |

| Historical Market Growth (2020 - 2025) | 6.6% |

Market Dynamics

Drivers - Rising Breast Cancer Incidence and Increasing Reconstruction Rates

A key growth driver for the breast tissue expander market is the growing global burden of breast cancer, coupled with rising reconstruction rates after mastectomy. Breast cancer remains the most commonly diagnosed cancer among women worldwide, with more than 2 million new cases annually according to major cancer registries, and incidence is still increasing in many high and middle-income countries. Early detection programs and advances in systemic therapy have improved survival, shifting focus toward long-term quality of life, body image, and psychosocial recovery. Organizations such as the American Society of Plastic Surgeons (ASPS) report that more than 100,000 breast reconstruction procedures are performed each year in the United States, with a substantial proportion using tissue expander-implant techniques. Policy initiatives such as the Women’s Health and Cancer Rights Act (WHCRA) in the U.S., which mandates coverage of reconstruction after mastectomy, have also boosted procedural volumes. As more patients are informed of reconstructive options and multidisciplinary breast centers become the standard of care, tissue expanders are increasingly used to stage implant-based reconstruction in both unilateral and bilateral procedures.

Technological Advancements and Expanding Aesthetic & Reconstructive Indications

Technological innovation in breast tissue expanders is another strong driver of market growth. Contemporary devices from companies such as Allergan (AbbVie Inc.), Mentor Worldwide LLC (Johnson & Johnson), Sientra, Inc., GC Aesthetics, and Polytech Health & Aesthetics GmbH feature improved shell materials, integrated fill ports, and surface texturing designed to optimize expansion dynamics and soft-tissue integration. The adoption of anatomically shaped expanders and devices that more closely mimic natural breast contours has improved aesthetic outcomes, particularly in delayed reconstruction or after radiation therapy. At the same time, intraoperative and remotely adjustable expanders, including air-filled and magnetically controlled designs, are under development or in use in selected markets, aiming to reduce clinic visits and improve patient comfort. Beyond oncology, demand is rising in cosmetic and gender-affirming procedures, including prophylactic mastectomy with immediate reconstruction in high-risk women and top surgery in transgender patients. As surgical techniques such as prepectoral reconstruction gain traction, tissue expander designs are being refined to support these approaches, creating a pipeline of product upgrades that support premium pricing and higher adoption.

Market Restraints

Safety Concerns, Complications, and Regulatory Scrutiny

Safety concerns and device-related complications represent important restraints on the breast tissue expander market. Complications such as infection, seroma, capsular contracture, skin necrosis, and device exposure can lead to expander removal, delayed reconstruction, and increased healthcare costs. Historical issues related to textured breast implants and rare cases of Breast Implant Associated Anaplastic Large Cell Lymphoma (BIA ALCL) have led regulators such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) to intensify oversight of breast implantable devices, including expanders. Product recalls and safety communications involving certain textured implant and expander models have made both surgeons and patients more cautious, in some cases shifting preferences toward smooth-surface devices or autologous reconstruction. This heightened regulatory scrutiny and medico-legal environment may slow uptake of newer, more complex expander designs, increase compliance costs for manufacturers, and influence payer policies around certain products.

Cost Barriers and Access Disparities in Emerging Markets

Another key barrier is the cost of breast reconstruction and limited access to specialized surgical services in low and middle-income countries. While high-income regions increasingly consider breast reconstruction part of standard cancer care, reconstruction rates remain low in many emerging markets due to out-of-pocket costs, lack of reimbursement, and limited availability of trained plastic and reconstructive surgeons. Even when mastectomy is covered, tissue expanders and implants may not be fully funded, making patients bear the cost of devices and staged procedures. Hospital procurement budgets can also restrict the adoption of newer, higher-priced expanders with advanced features. In rural areas or smaller hospitals, limited operating room capacity, follow-up infrastructure, and patient transportation challenges reduce the feasibility of multi-stage expander protocols. These economic and structural factors constrain market penetration outside major urban centers in Asia, Latin America, and parts of the Middle East & Africa, slowing global growth despite rising breast cancer incidence.

Market Opportunities

Growth in Immediate and Bilateral Reconstruction, Including Risk-Reducing Surgery

One of the strongest opportunities in the breast tissue expander market lies in the global trend toward immediate reconstruction and bilateral procedures. Increasing numbers of patients, particularly in North America and Europe, opt for immediate reconstruction at the time of mastectomy, supported by evidence showing improved psychosocial outcomes and comparable oncologic safety in appropriately selected cases. The growing use of risk-reducing mastectomy in women carrying BRCA1/BRCA2 or other high-risk mutations, often performed bilaterally, also drives demand for expander-based reconstruction. As genetic testing and high-risk screening programs expand, more patients will be counseled on prophylactic surgery and reconstructive options, creating a steady pipeline of procedures. Tissue expanders are central in these staged reconstructions, enabling the gradual expansion of skin and muscle before definitive implant placement. Companies that provide comprehensive expanders and implant systems, along with planning tools and surgeon education on immediate and bilateral reconstruction techniques, are well-positioned to capitalize on this opportunity.

Emerging Markets Expansion and Adoption of Pre-Pectoral and Day Surgery Pathways

Emerging markets in Asia Pacific, Latin America, and parts of the Middle East & Africa present substantial future growth opportunities as awareness of reconstructive options increases and health systems strengthen oncology pathways. As tertiary care hospitals and cancer centers in countries such as China, India, Brazil, and Saudi Arabia expand breast surgery services, tissue expander-implant reconstruction is gradually being incorporated into standard offerings. The spread of prepectoral reconstruction techniques, which place the expander and subsequent implant above the pectoral muscle with acellular dermal matrix or mesh support, can reduce postoperative pain and recovery time, making these procedures more compatible with enhanced recovery and day surgery pathways. This can, in turn, improve operating room utilization and reduce length of stay, making adoption more attractive to hospitals facing resource constraints. Manufacturers that provide clinical evidence, training support, and cost-effective product lines tailored to local health system budgets can accelerate penetration in these high-potential regions.

Category-wise Analysis

Product Type Insights

Within the product type, saline-filled tissue expanders represent the leading segment, accounting for approximately 43% share in 2025. Saline-filled expanders have been widely used for decades, offering surgeons predictable intraoperative handling and post-operative adjustability via periodic saline injections through an integrated port. Their long clinical track record, relatively straightforward design, and flexibility in expansion schedules make them the default choice in many centers, particularly where budget constraints or regulatory considerations limit use of alternative filler types. Saline expanders are perceived as easier to monitor for leaks or ruptures and can be deflated or removed relatively simply if complications arise. At the same time, silicone-filled expanders are the fastest-growing product segment, supported by efforts to more closely simulate the weight and feel of the final implant and to improve patient comfort during the expansion period. Air-filled and innovative remote-adjustment designs remain niche but highlight the potential for future disrupters that further enhance patient experience and reduce clinic visits.

Application Insights

By application, breast reconstruction is the dominant segment, representing an estimated 72% share in 2025, while cosmetic indications and other uses account for the remainder. The majority of tissue expanders are used in post-mastectomy reconstruction for breast cancer patients or those undergoing risk-reducing mastectomy, reflecting the strong clinical rationale for staged reconstruction in these populations. Clinical data and guidelines from major oncology and plastic surgery societies emphasize the role of reconstruction in restoring body image and psychological well-being, thereby supporting broader adoption among eligible patients. Cosmetic uses-such as staged augmentation in complex chest wall deformities or in patients with thin soft-tissue envelopes-form a smaller but growing niche, particularly in regions with active private aesthetic markets. As awareness of reconstructive options and multidisciplinary breast care models spreads to emerging markets, the reconstruction segment will remain the primary growth engine, but cosmetic and gender-affirming indications are expected to grow faster from a smaller base, contributing to the diversification of demand.

End-user Insights

Among end users, hospitals constitute the leading segment, accounting for an estimated 58% share in 2025. Most mastectomy and immediate reconstruction procedures are performed in hospital settings, often within dedicated breast units or oncology departments that coordinate surgical, medical, and radiation treatments. Hospitals typically manage procurement of tissue expanders through centralized purchasing, favoring suppliers with strong clinical evidence, comprehensive product portfolios, and reliable logistics. Ambulatory surgical centers (ASCs) are the fastest-growing end-user segment, driven by the shift of selected reconstructive and cosmetic procedures into outpatient settings to improve efficiency and reduce costs. In markets such as the United States, reimbursement models increasingly support same-day surgery and enhanced recovery pathways, allowing some expander placements and exchange procedures to be performed in ASCs. Specialty and cosmetic clinics, particularly in regions with robust private aesthetic sectors, add incremental demand, focusing more on cosmetic and revision cases and often working closely with specific brands such as GC Aesthetics, Groupe SEBBIN SAS, or Eurosilicone S.A.S. to align with patient preferences.

Regional Insights

North America Breast Tissue Expander Market Trends and Insights

North America is the leading regional market for breast tissue expanders, holding around 43% share in 2025, underpinned by high breast cancer incidence, widespread screening programs, and strong integration of reconstruction into standard oncology care. The United States drives most of this demand, supported by the Women’s Health and Cancer Rights Act (WHCRA), which requires group health plans that cover mastectomy to also cover breast reconstruction, including procedures on the contralateral breast for symmetry. Data from the American Society of Plastic Surgeons (ASPS) show that breast reconstruction procedures in the U.S. have increased substantially over the past two decades, with implant-based reconstruction often staged using tissue expanders being the most common approach.

Asia Pacific Breast Tissue Expander Market Trends and Insights

Asia Pacific is the fastest-growing regional market for breast tissue expanders, supported by rising breast cancer incidence, improving healthcare infrastructure, and growing awareness of reconstructive and cosmetic breast surgery. China is experiencing rapid expansion of oncology services and plastic surgery capacity, particularly in major urban centers, with increasing numbers of women seeking reconstruction after mastectomy and a growing private aesthetic market. Domestic and international manufacturers are expanding their presence to serve both public hospitals and private clinics, and as national health insurance coverage broadens, more patients gain access to staged reconstruction pathways. Japan has a strong record in breast cancer screening and treatment, and while reconstruction rates historically lagged behind some Western countries, recent policy decisions to reimburse implant-based reconstruction and inclusion of certain products in the national insurance system have boosted adoption.

In India, rise in cancer awareness, urbanization, and the growth of private hospital networks and specialty cancer centers are gradually increasing demand for post-mastectomy reconstruction, although cost and cultural factors still limit penetration in some segments. Leading corporate hospital groups and metropolitan cancer centers are more likely to offer expander-based reconstruction, and as training in oncoplastic surgery expands, procedure volumes are expected to grow. In ASEAN markets such as Singapore, Malaysia, and Thailand, well-developed private healthcare and medical tourism industries support both reconstructive and cosmetic breast surgery, including expander implant techniques. Regional manufacturers such as Guangzhou Wanhe Plastic Materials Co., Ltd. contribute to local supply and cost-competitive options, while global firms provide premium brands. Overall, demographic trends, economic growth, and the gradual normalization of reconstruction within breast cancer care position Asia Pacific as a key engine of future market expansion.

Competitive Landscape

The global breast tissue expander market is moderately consolidated, with a limited number of established manufacturers holding significant market share due to strong clinical credibility, regulatory approvals, and long-standing surgeon relationships. Competition is driven by product reliability, safety profile, ease of expansion, and post-surgical aesthetic outcomes. Technological differentiation, such as remote-controlled expansion, improved shell durability, and enhanced biocompatible materials, plays a key role in market positioning. Pricing pressure remains high, especially in emerging markets, encouraging cost-effective product offerings. New entrants face high regulatory and clinical validation barriers, while innovation, surgeon training, and distribution reach remain critical factors shaping competitive dynamics.

Key Developments:

- In November 2025, Syantra, Inc., a biotechnology company focused on advancing cancer detection, and the Alamo Breast Cancer Foundation (ABCF), a nonprofit dedicated to breast cancer prevention, cure, and quality care for all women, formed a new partnership aimed at supporting innovative technologies and expanding access to breast cancer detection and treatment.

Companies Covered in Breast Tissue Expander Market

- Allergan (AbbVie Inc.)

- Mentor Worldwide LLC (Johnson & Johnson)

- Sientra, Inc.

- GC Aesthetics

- Polytech Health & Aesthetics GmbH

- Establishment Labs S.A.

- Silimed Industria de Implantes Ltd.

- Groupe SEBBIN SAS,

- Eurosilicone S.A.S.,

- Implantech Associates Inc.,

- PMT Corporation

- Guangzhou Wanhe Plastic Materials Co., Ltd.

- Sebbin Italia S.r.l., Nagor Ltd.

Frequently Asked Questions

The global breast tissue expander market is expected to reach approximately US$ 1.4 billion in 2026, and is projected to grow further to about US$ 2.3 billion by 2033, reflecting a forecast CAGR of around 7.3% between 2026 and 2033.

Demand is driven by rising breast cancer incidence, increasing rates of post‑mastectomy reconstruction, supportive reimbursement and legal frameworks, growing awareness of quality‑of‑life benefits, and technological advances in expander design that improve safety, comfort, and cosmetic outcomes.

North America is the leading region, supported by high procedure volumes in the United States and Canada, robust breast cancer screening and treatment programs, mandated coverage for reconstruction after mastectomy, and the strong presence of major implant and expander manufacturers.

A key opportunity lies in expanding immediate, bilateral, and prepectoral reconstruction, especially in emerging markets by combining advanced expander designs with surgeon training, patient education, and cost-effective product lines that align with day‑surgery and enhanced recovery pathways.

Major players include Allergan (AbbVie Inc.), Mentor Worldwide LLC (Johnson & Johnson), Sientra, Inc., GC Aesthetics, Polytech Health & Aesthetics GmbH, Establishment Labs S.A., Silimed Industria de Implantes Ltd., Groupe SEBBIN SAS, Eurosilicone S.A.S., Implantech Associates Inc., PMT Corporation, and Guangzhou Wanhe Plastic Materials Co., Ltd., among others.