- Medical Devices

- Bone Mineral Densitometry (BMD) Market

Bone Mineral Densitometry (BMD) Market Size, Share, and Growth Forecast 2026 - 2033

Bone Mineral Densitometry (BMD) Market by Product Type (Axial Bone Densitometers, Peripheral Bone Densitometers), by Technology (DXA / DEXA, Peripheral DXA (pDXA), Quantitative Ultrasound (QUS), Quantitative CT (QCT)), by Application (Osteoporosis Diagnosis, Fracture Risk Assessment, Bone Health Screening, Monitoring Treatment, Others), by End User (Hospitals, Diagnostic & Imaging Centers, Specialty Clinics, Research Institutions, Home Care / Portable Services), by Regional Analysis, 2026-2033

Bone Mineral Densitometry (BMD) Market Outlook (2023-2033)

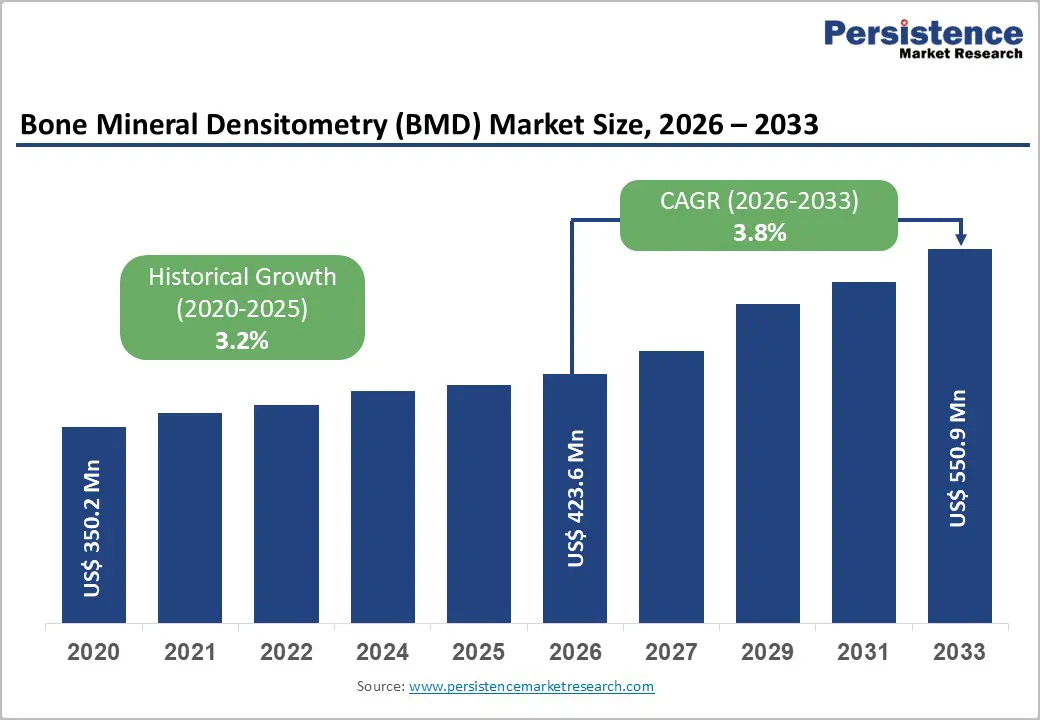

The global Bone Mineral Densitometry (BMD) market size is expected to be valued at US$ 423.6 million in 2026 and projected to reach US$ 550.9 million by 2033, growing at a CAGR of 3.8% between 2026 and 2033. Rising prevalence of osteoporosis drives this growth, as over 1.5 million fragility fractures occur annually in the U.S. alone, necessitating widespread BMD screening. An aging global population and increasing adoption of preventive healthcare further accelerate demand, supported by endorsements from organizations like the World Health Organization (WHO) for DXA as the gold standard.

Key Market highlights

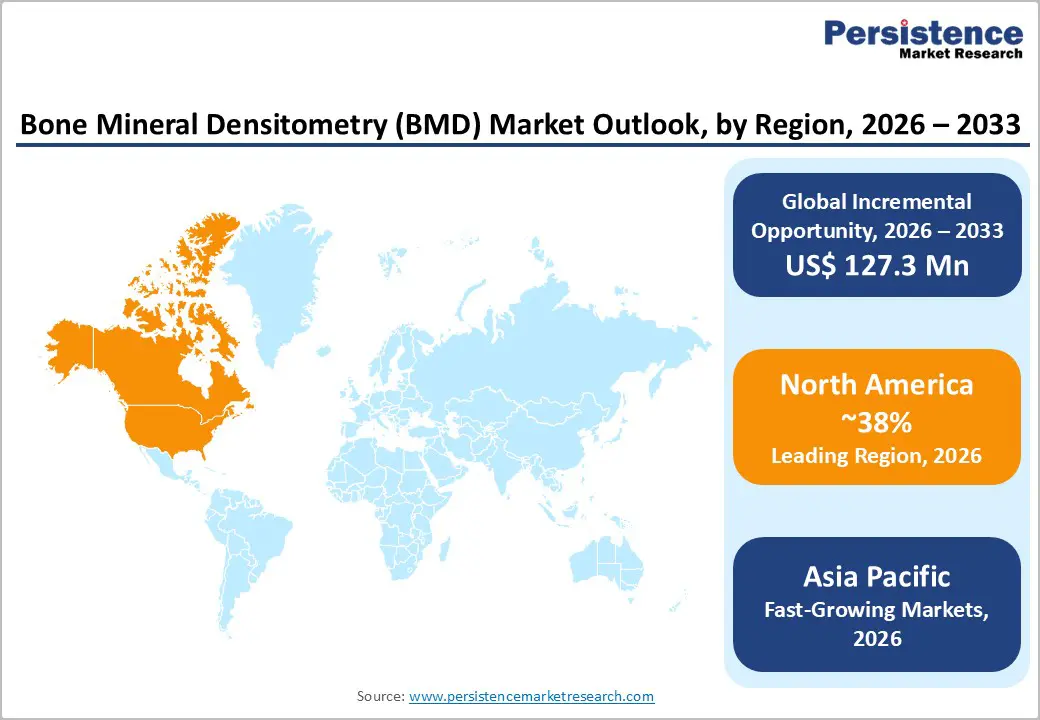

- North America dominates Bone Mineral Densitometry (BMD) with 38% share in 2025, driven by U.S. screening and FDA innovations.

- Asia Pacific fastest-growing region at a high CAGR (2025-2032), fueled by China/India demographics and subsidies.

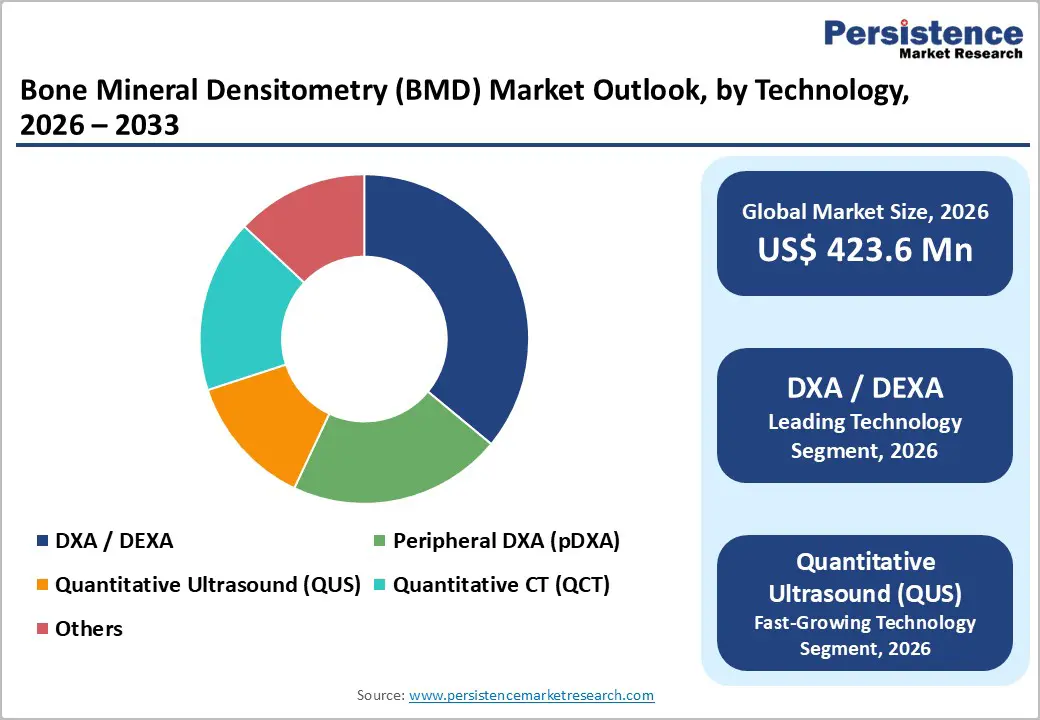

- DXA / DEXA leads technology with 36% 2025 share as the WHO gold standard for precise osteoporosis diagnosis.

- Quantitative Ultrasound (QUS) fastest-growing segment, offering portable, radiation-free screening for emerging markets.

- Key opportunity in portable QUS for home care, tapping underserved regions with validated fracture risk assessment.

| Key Insights | Details |

|---|---|

| Bone Mineral Densitometry (BMD) Market Size (2026E) | US$ 423.6 Mn |

| Market Value Forecast (2033F) | US$ 550.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 3.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.2% |

Market Dynamics

Rising Osteoporosis Prevalence

The global rise in osteoporosis prevalence is a major driver of the Bone Mineral Densitometry (BMD) market, largely due to rapidly aging populations and longer life expectancy. Osteoporosis is often asymptomatic until a fracture occurs, making early diagnosis essential for reducing morbidity, mortality, and long-term healthcare costs. In the U.S. alone, over 1.5 million osteoporotic fractures occur annually, significantly increasing hospitalizations, rehabilitation needs, and economic burden. Similar trends are observed across Europe and Asia, where expanding elderly populations and postmenopausal women represent high-risk groups. Elderly men are also increasingly recognized as vulnerable, further widening the screening base. Healthcare systems are therefore emphasizing preventive care and routine bone health assessments. DXA-based BMD testing, endorsed by WHO diagnostic criteria using T-scores, remains the gold standard for confirming osteoporosis and guiding treatment decisions. Early identification through BMD enables timely pharmacological and lifestyle interventions, reducing fracture incidence and associated complications. As awareness improves among physicians and patients, demand for BMD testing continues to rise, driving sustained installations of densitometry systems across hospitals, diagnostic centers, and specialty clinics worldwide.

Advancements in Portable Technologies

Advancements in portable and low-radiation technologies are significantly accelerating growth in the Bone Mineral Densitometry (BMD) market by improving accessibility and affordability of bone health screening. Traditional DXA systems, while highly accurate, are expensive, bulky, and limited to hospital-based settings, restricting their reach in rural and resource-limited regions. In contrast, portable technologies particularly Quantitative Ultrasound (QUS) offer compact, lightweight solutions, often weighing less than 1 kg, enabling easy deployment in community health camps, primary care clinics, and mobile screening units. QUS devices assess bone properties at peripheral sites, such as the heel, without exposing patients to ionizing radiation, thereby enhancing safety and patient acceptance. Clinical studies have demonstrated a strong correlation between QUS measurements and DXA results for fracture risk prediction, supporting its use as an effective screening tool. These innovations reduce infrastructure requirements, lower operational costs, and expand screening coverage in developing markets. As governments and healthcare providers prioritize early diagnosis and preventive care, adoption of portable BMD technologies is expected to rise steadily, strengthening overall market penetration and growth.?

Market Restrains

High Equipment Costs and Reimbursement Issues

High capital investment requirements remain a key restraint for the Bone Mineral Densitometry (BMD) market, particularly for advanced axial DXA systems, which typically cost between US$100,000 and US$300,000. For small and mid-sized hospitals, diagnostic centers, and specialty clinics, especially in cost-sensitive and rural markets, such upfront expenditure is difficult to justify given limited patient volumes and slow return on investment. In addition to purchase costs, facilities must account for ongoing expenses related to installation, calibration, software upgrades, service contracts, and trained personnel, further increasing total ownership costs. Reimbursement challenges compound this issue, as insurance coverage for routine osteoporosis screening remains inconsistent across regions. In many developing and emerging markets, BMD tests are either partially reimbursed or paid out-of-pocket, discouraging patients from preventive screening. Even in developed healthcare systems, reimbursement rates may not fully offset operational expenses, reducing provider incentives to expand BMD services. These financial constraints disproportionately affect rural and standalone clinics, slowing adoption of high-end densitometry systems and limiting market expansion despite growing clinical need.

Radiation Exposure Concerns

Concerns related to radiation exposure continue to restrain the adoption of traditional Bone Mineral Densitometry (BMD) technologies, particularly DXA and Quantitative CT (QCT), despite their relatively low radiation doses. While DXA typically delivers minimal exposure compared to standard radiographic procedures, patient and clinician apprehension persists, especially in populations requiring frequent monitoring such as postmenopausal women, elderly patients, pediatric cases, and individuals with chronic bone disorders. Cumulative radiation exposure over repeated scans raises long-term safety considerations, prompting some healthcare providers to limit test frequency or delay follow-up assessments. These concerns are more pronounced with QCT, which involves higher radiation doses than DXA, restricting its use mainly to specialized or research settings. Regulatory oversight and strict radiation safety guidelines further add to compliance costs and operational complexity for healthcare facilities. As awareness of radiation risks increases, preference is gradually shifting toward non-ionizing alternatives such as Quantitative Ultrasound. While this trend supports safer screening options, it simultaneously slows upgrades and investments in conventional radiation-based densitometry systems, constraining overall market growth.?

Market Opportunity

Portable and Home Care Innovations

Portable and home-care-focused innovations present a significant growth opportunity for the Bone Mineral Densitometry (BMD) market, particularly through the rising adoption of Quantitative Ultrasound (QUS). As the fastest-growing BMD technology during 2025–2032, QUS benefits from its radiation-free operation, compact design, and ease of use, making it well suited for decentralized care models. Lightweight, portable QUS devices enable bone health assessments in home care settings, outpatient clinics, community health camps, and long-term care facilities, overcoming accessibility limitations associated with conventional DXA systems. Clinical validation studies demonstrating strong correlation between QUS measurements and DXA-based fracture risk assessment have increased physician confidence in its screening utility. Regulatory acceptance of low-dose and non-ionizing diagnostic alternatives further strengthens adoption momentum. These advantages are particularly relevant in underserved and aging populations where early osteoporosis detection remains limited. For manufacturers, targeting specialty clinics, geriatric centers, and primary care providers with affordable, portable solutions offers attractive returns through higher unit volumes and repeat usage. As healthcare systems shift toward preventive and home-based care, portable BMD technologies are expected to play a pivotal role in market expansion.

Category-wise Insights

Product Type Analysis

Axial bone densitometers dominate the Bone Mineral Densitometry (BMD) market, accounting for approximately 69% market share in 2025, primarily due to their superior diagnostic accuracy and clinical relevance. These systems are specifically designed to measure bone mineral density at central skeletal sites such as the spine and hip, which are the most predictive locations for osteoporotic fractures. Clinical guidelines globally recognize axial measurements as essential for definitive osteoporosis diagnosis and fracture risk assessment, giving these devices a clear advantage over peripheral alternatives. Endorsement by organizations such as the World Health Organization further reinforces their role as the diagnostic gold standard. Hospitals and large diagnostic centers prefer axial densitometers because they provide highly reproducible, precise data that supports long-term patient monitoring and treatment evaluation. Although axial systems involve higher capital investment, their ability to deliver comprehensive, clinically actionable results ensures sustained demand. As osteoporosis screening programs expand and emphasis on accurate diagnosis increases, axial bone densitometers continue to lead the product type segment.

Technology Analysis

DXA/DEXA technology holds a dominant position in the BMD market, capturing around 36% market share in 2025, driven by its strong clinical validation and widespread acceptance. DXA is considered the gold standard for assessing bone mineral density of the axial skeleton, particularly the hip and spine, which are critical sites for osteoporosis diagnosis. Its use of low-dose X-ray radiation significantly lower than conventional imaging addresses safety concerns while maintaining high precision and reproducibility. International organizations, including WHO, as well as national screening programs, recommend DXA-derived T-scores as the benchmark for diagnosing osteoporosis and monitoring disease progression. Physicians rely on DXA for its ability to detect subtle changes in bone density, enabling early intervention and treatment optimization. Additionally, its integration with advanced software for fracture risk assessment enhances clinical decision-making. These factors collectively sustain DXA’s technological leadership despite the emergence of alternative, lower-cost modalities.

End User Analysis

Hospitals account for roughly 55% of the Bone Mineral Densitometry market share in 2025, reflecting their central role in advanced diagnostic care. Hospitals are well equipped with the infrastructure required to install and operate high-end axial DXA systems, including radiation-controlled environments and trained radiology professionals. High patient inflow, particularly elderly and high-risk populations, supports consistent utilization of BMD services. Favorable reimbursement structures in many healthcare systems further encourage hospital-based screening and follow-up assessments. In addition, hospitals often serve as referral centers for osteoporosis management, integrating BMD testing with orthopedic, rheumatology, and endocrinology services. They also participate in clinical trials and post-market evaluations of new densitometry technologies, reinforcing early adoption. While diagnostic centers and clinics are growing in importance, hospitals remain the primary end users due to their comprehensive care capabilities, clinical credibility, and ability to manage complex osteoporosis cases.

Regional Insights

North America Bone Mineral Densitometry (BMD) Market Trends

North America remains the leading region in the Bone Mineral Densitometry (BMD) market, driven by a high osteoporosis burden, strong healthcare infrastructure, and early adoption of advanced diagnostic technologies. The region benefits from a large aging population, particularly postmenopausal women and elderly men, who are at elevated risk of bone loss and fractures. Well-established clinical guidelines strongly recommend routine BMD screening, supporting consistent demand for DXA-based systems. High awareness among physicians and patients regarding preventive bone health further accelerates testing volumes. Favorable reimbursement policies in the United States and Canada encourage hospitals and diagnostic centers to invest in advanced axial densitometers. In addition, the presence of leading medical imaging manufacturers and continuous product innovation, including software upgrades and low-dose technologies, strengthens regional leadership. Growing emphasis on early diagnosis, fracture prevention, and value-based care models ensures sustained utilization of BMD testing. Together, these factors position North America as the most mature and revenue-generating market for bone mineral densitometry.

Asia Pacific Bone Mineral Densitometry (BMD) Market Trends

Asia Pacific is emerging as a high-growth region in the Bone Mineral Densitometry (BMD) market, supported by rapidly aging populations, rising osteoporosis awareness, and expanding healthcare access. Countries such as China, India, Japan, and South Korea are experiencing a sharp increase in elderly populations, driving higher incidence of osteoporosis and fracture risk. Historically low screening rates are improving as governments and healthcare organizations promote early diagnosis and preventive care. Expanding hospital networks, growth of private diagnostic centers, and increasing investments in medical imaging infrastructure are accelerating adoption of BMD systems. Cost sensitivity across the region is also encouraging demand for portable and lower-cost technologies such as Quantitative Ultrasound, especially in rural and semi-urban areas. Additionally, rising disposable incomes and improving insurance coverage are making diagnostic services more accessible. International manufacturers are increasingly targeting Asia Pacific through local partnerships and manufacturing, further strengthening market penetration. These factors collectively position Asia Pacific as the fastest-growing and strategically important BMD market globally.

Competitive Landscape

Market Structure Analysis

The Bone Mineral Densitometry (BMD) market competitive landscape is moderately consolidated, characterized by the presence of established global players and a growing number of regional manufacturers. Competition is driven by technological innovation, diagnostic accuracy, and compliance with clinical guidelines. Market participants focus on enhancing system precision, reducing radiation exposure, and integrating advanced software for fracture risk assessment and workflow efficiency. Product differentiation increasingly centers on portability, ease of use, and cost-effectiveness to address emerging and underserved markets. Strategic initiatives such as technology upgrades, regulatory approvals, geographic expansion, and partnerships with healthcare providers strengthen competitive positioning.

Key Market Developments

- In December 2025, the Foundation for the National Institutes of Health (FNIH) announced that the Food and Drug Administration (FDA) had qualified treatment-related changes in hip bone mineral density (BMD) as a surrogate endpoint for bone fractures in clinical trials of anti-osteoporosis drugs in post-menopausal women at risk of osteoporotic fractures.

Companies Covered in Bone Mineral Densitometry (BMD) Market

- GE Healthcare

- Hologic, Inc.

- Beammed, Ltd.

- Swissray International, Inc.

- Osteosys Co. Ltd.

- Diagnostic Medical System SA

- Medonica Co. Ltd.

- Osteometer Meditech, Inc.

- Hitachi Ltd

- CooperSurgical, Inc. (Cooper Companies)

- Dentsply Sirona Inc.

- Lone Oak Medical Technology LLC

- Scanflex Int. AB

- CompuMed, Inc.

Frequently Asked Questions

The global Bone Mineral Densitometry (BMD) market is expected to reach US$ 423.6 million in 2026.

Rising osteoporosis prevalence, with 1.5 million annual U.S. fractures, drives demand for screening.

North America leads with 38% share in 2025, supported by U.S. infrastructure.

Portable QUS for Asia Pacific and home care, leveraging growth in emerging markets.

Leading players include GE Healthcare, Hologic, Inc., and OsteoSys Corporation