- Healthcare Services

- Facial Bone Contouring Market

Facial Bone Contouring Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Facial Bone Contouring Market by Product (Facial Implants, Fixation Devices, Consumables, and Others), Procedure (V Line Surgery, Angle Reduction Surgery, Cheek Bone Reduction Surgery, Cheek Fat Removal, Chin Narrowing Surgery, and Others) End-user (Hospitals, Aesthetic Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 to 2033

Facial Bone Contouring Market Share and Trends Analysis

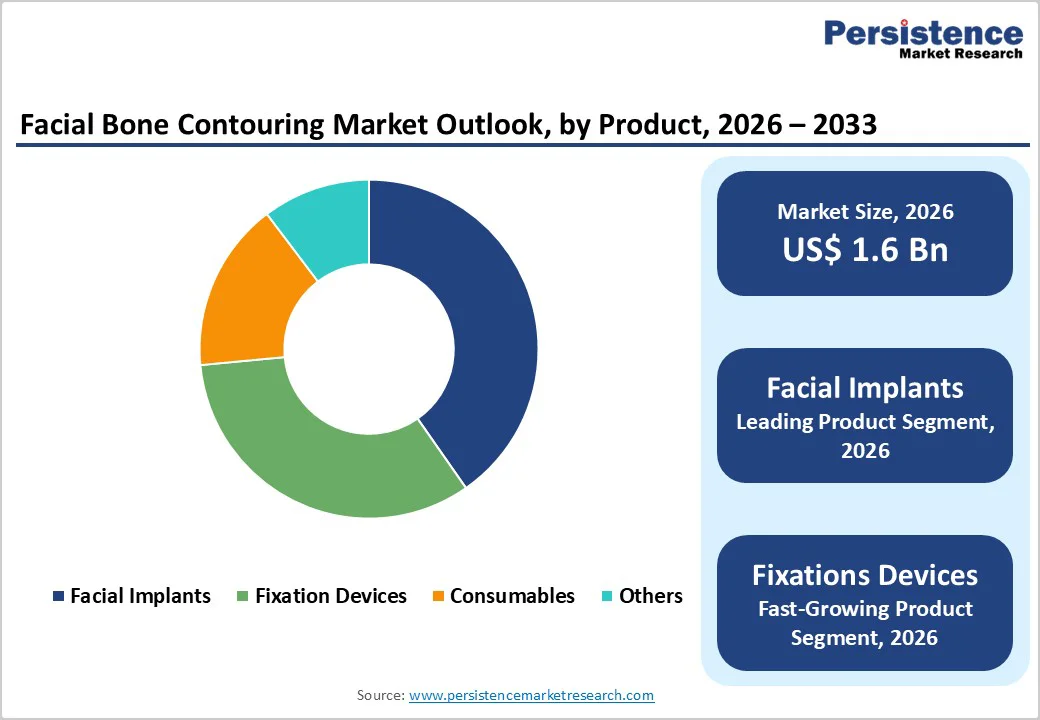

The global facial bone contouring market size is estimated to grow from US$ 1.6 Bn in 2026 to US$ 2.6 Bn by 2033. The market is projected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for facial bone contouring is rising rapidly, supported by increasing interest in aesthetic facial restructuring, growing awareness of facial symmetry and proportionality, and the adoption of advanced surgical planning and 3D-printed patient-specific implants. The expansion of specialized aesthetic clinics, rising disposable income, and growing medical tourism are accelerating market momentum. Continuous improvements in minimally invasive techniques, virtual surgical planning, and bio-compatible implant materials are enhancing surgical precision, reducing recovery time, and improving patient outcomes. Additionally, strong social media influence, celebrity-driven beauty trends, and increasing preference for permanent facial enhancements further drive market growth.

Key Industry Highlights

- Leading Region: North America holds the largest share at 47.2%, supported by a high concentration of board-certified maxillofacial and cosmetic surgeons, widespread adoption of advanced implants and fixation devices, and a mature healthcare infrastructure.

- Fastest-Growing Region: Asia Pacific is expanding at the quickest pace, driven by rising demand for jawline, chin, and cheekbone contouring, increasing medical tourism, and the presence of major OEMs enabling access to cost-effective and innovative surgical solutions.

- Leading Product Segment: Facial implants lead the category due to their strong adoption in chin, cheek, and jawline enhancement procedures, offering long-lasting results and customization options.

- Fastest-Growing Product Segment: Fixation devices are expanding fastest as clinics increasingly adopt advanced plates, screws, and patient-specific guides to improve precision and post-operative stability.

- Leading Procedure Segment: V-line surgery dominates the market owing to high demand for jawline slimming, chin narrowing, and overall facial contouring.

- Fastest-Growing Procedure Segment: Angle reduction surgery is scaling rapidly as patients increasingly seek mandibular angle and jawline reshaping, supported by advanced minimally invasive osteotomy techniques and personalized surgical planning.

| Key Insights | Details |

|---|---|

| Facial Bone Contouring Market Size (2026E) | US$ 1.6 Bn |

| Market Value Forecast (2033F) | US$ 2.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver - Rising Demand for Aesthetic Procedures and Technological Advancements

The global facial bone contouring market is witnessing strong growth driven by the rising demand for aesthetic procedures. Increasing awareness of facial aesthetics, fueled by social media, celebrity influence, and evolving beauty standards, is encouraging individuals to opt for facial contouring surgeries. Minimally invasive techniques, such as V-line surgery and cheekbone reduction, have become particularly popular in regions such as Asia Pacific, where cosmetic procedures are culturally embraced. Patients increasingly prefer procedures that offer noticeable results with reduced recovery time, lower risk of scarring, and enhanced safety, thereby driving market growth.

Technological advancements such as innovations in 3D imaging, patient-specific implants, and robotic-assisted surgical systems are enhancing surgical precision and improving clinical outcomes. These technologies allow surgeons to customize procedures according to individual facial structures, minimize errors, and optimize aesthetic results. Together, rising aesthetic consciousness and technological progress are propelling the facial bone contouring market.

Restraints - High Procedure Costs and Risk of Surgical Complications

The high cost of facial bone contouring procedures is a significant restraint on market growth. Advanced surgical techniques, including the use of patient-specific implants, robotic-assisted systems, and minimally invasive methods, come with substantial expenses. These costs often limit access in price-sensitive regions, particularly in emerging markets, where affordability remains a key concern. Even in developed countries, out-of-pocket expenses can deter potential patients, slowing adoption despite increasing awareness of aesthetic procedures. Additionally, the requirement for specialized equipment and highly skilled surgeons further elevates procedural costs, adding financial barriers to both patients and healthcare providers.

Moreover, the risk of surgical complications in facial bone contouring procedures carry potential risks such as infections, nerve damage, asymmetry, and implant rejection. Concerns about postoperative recovery, long-term outcomes, and revision surgeries can make patients hesitant. These risks, coupled with the high cost, reduce overall willingness to undergo procedures, impacting market growth despite rising demand and technological advancements.

Opportunity - Advancements in Scarless Techniques and Integration of AI & 3D Printing

The development of scarless and minimally invasive facial bone contouring techniques are creating significant growth opportunity in the market. Innovations such as endoscopic contouring, laser-assisted procedures, and other scarless approaches are attracting a broader patient base, particularly younger individuals and those seeking subtle yet effective facial enhancements. These techniques reduce recovery time, minimize visible scarring, and improve overall patient comfort, making aesthetic procedures more appealing. As patient awareness and demand for minimally invasive options increase, clinics and surgeons are increasingly adopting these advanced methods to differentiate their services and propel market growth.

Furthermore, the integration of AI and 3D printing technologies is transforming the facial contouring market with AI-powered surgical planning tools enable precise simulation of outcomes, while 3D-printed, patient-specific implants ensure an exact fit tailored to individual facial anatomy. This combination enhances surgical accuracy, reduces complications, and improves post-procedure satisfaction.

Category-wise Analysis

By Product, Facial Implants Dominate Globally Due to Rising Demand for Aesthetic Facial Reconstruction and Contouring Procedures

The facial implants segment is projected to dominate the global facial bone contouring market in 2026, accounting for a revenue share of 40.3%. The segment’s strong performance is primarily driven by the rising demand for long-lasting and highly customizable solutions for chin, cheek, and jawline enhancement. Facial implants offer superior structural definition compared to soft-tissue fillers, making them the preferred choice for patients seeking permanent aesthetic improvement and balanced facial proportions. Technological advancements such as 3D-printed patient-specific implants, hybrid titanium-PEEK materials, and CAD/CAM surgical planning have significantly improved precision, fit, and surgical outcomes, further boosting adoption. Growing popularity of celebrity-inspired facial aesthetics, increasing disposable income, and expanding availability of expert maxillofacial surgeons across developed and emerging markets are accelerating procedural uptake. Additionally, the rising acceptance of minimally invasive implantation techniques with shorter recovery periods is attracting a broader patient base. As clinics and surgical centers continue to integrate advanced imaging and virtual planning systems, the facial implants segment is expected to maintain its leadership in the global market.

By Procedure, V Line Surgery Leads the Market Globally Due to Growing Popularity of Minimally Invasive Facial Contouring and Youthful Aesthetics

The V line surgery segment is projected to dominate the global facial bone contouring market in 2026, accounting for a revenue share of 36.4%. This is due to rising demand for slimmer, more refined jawlines, especially among younger consumers influenced by East Asian beauty standards and social media aesthetics. V-line surgery offers a highly transformative outcome by combining mandibular angle reduction, chin narrowing, and jawline reshaping, making it one of the most sought-after procedures in both aesthetic and reconstructive practices. The technique has gained strong traction in countries such as South Korea, China, Japan, and increasingly in Western markets as awareness grows. Advancements in virtual surgical planning, intraoperative navigation, and 3D-printed patient-specific guides have significantly enhanced accuracy and outcomes, further elevating its appeal. Improved safety, reduced recovery time, and the availability of minimally invasive variations have also expanded patient adoption. Additionally, growing medical tourism in Asia, celebrity-driven trends, and higher disposable incomes continue to support the dominance of V-line surgery in the facial bone contouring market.

By End-user, Aesthetic Clinics Dominate Globally Due to High Adoption of Advanced Facial Contouring and Cosmetic Procedures

The aesthetic clinics segment is projected to dominate the global facial bone contouring market in 2026, accounting for a revenue share 52.8%. This is driven by the growing popularity of elective facial reshaping procedures such as V-line contouring, chin augmentation, cheekbone reduction, and jawline refinement, which are increasingly performed in specialized aesthetic centers rather than hospital settings. Aesthetic clinics offer highly personalized treatment plans, advanced imaging and planning technologies, and shorter waiting times, making them the preferred choice for patients seeking precision-driven cosmetic enhancements. Rising consumer inclination toward minimally invasive and scarless contouring techniques, along with greater affordability of aesthetic packages, is further fueling demand. Additionally, increased marketing through social media, celebrity influence, and clinic-led digital engagement is expanding awareness and patient footfall. The availability of skilled cosmetic surgeons, bundled financing options, and high adoption of 3D-printed implants and CAD/CAM surgical planning within these clinics continues drive market growth.

Regional Insights

North America Facial Bone Contouring Market Trends

The North America market is expected to dominate globally with a value share of 47.2% in the 2026, with the U.S. leading the region due to strong adoption of technologically advanced facial implants, widespread use of 3D surgical planning, and the presence of a large base of board-certified plastic and maxillofacial surgeons. High patient willingness to invest in aesthetic enhancements, coupled with increasing popularity of jawline definition, chin augmentation, and combination osteoplasty procedures, continues to propel growth. The region also benefits from rapid integration of patient-specific 3D-printed implants, hybrid titanium-PEEK devices, and minimally invasive contouring tools that enhance precision and aesthetic outcomes.

Favorable reimbursement for certain reconstructive procedures, robust R&D capabilities of key manufacturers, and expanding clinical training programs further strengthen market penetration. Additionally, strong influence of social media aesthetic trends and rising demand among both younger and aging populations boosts market growth in the across North America region.

Europe Facial Bone Contouring Market Trends

The Europe market is expected to grow steadily, driven by increasing adoption of advanced facial skeletal reconstruction techniques, rising preference for minimally invasive and scarless contouring procedures, and strong integration of 3D planning and patient-specific implant technologies across aesthetic and reconstructive practices. Countries such as Germany, the U.K., France, Italy, and Spain are witnessing higher uptake of chin augmentation, jawline reshaping, and midface reconstruction due to growing aesthetic awareness and the availability of specialized maxillofacial surgeons. The region also benefits from well-established regulatory frameworks, high clinical standards, and rapid acceptance of next-generation materials such as PEEK and bioresorbable fixation systems.

Additionally, expanding medical tourism in Central and Eastern Europe, rising investments by leading device manufacturers, and increasing emphasis on natural-looking outcomes are further strengthening market demand. Europe’s aging population is also contributing to the rise in facial rejuvenation and structural contouring procedures, supporting consistent long-term market growth across the region.

Asia Pacific Facial Bone Contouring Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 7.8% between 2026 and 2033, driven by rising demand for aesthetic facial reshaping procedures among younger demographics, strong cultural preference for V-line and jawline refinement, and rapid adoption of minimally invasive surgical techniques. Countries such as South Korea, Japan, China, and India are emerging as global hubs for cosmetic and maxillofacial surgery, supported by advanced clinical infrastructure and expanding medical tourism. Increasing availability of 3D-printed patient-specific implants, CAD/CAM surgical planning, and improved fixation systems is further elevating the quality and precision of facial bone contouring outcomes across the region.

Growing disposable income, strong influence of beauty standards shaped by K-beauty and social media culture, and shorter recovery time offered by new technologies are boosting patient acceptance. In addition, rising investments from global device manufacturers, surgeon training programs, and multi-specialty aesthetic centers are accelerating market growth throughout the Asia Pacific.

Competitive Landscape

The global facial bone contouring market is highly competitive, with major players including Stryker, Johnson & Johnson, Zimmer Biomet, Acumed LLC, and Medtronic. These companies leverage extensive surgical portfolios, strong surgeon networks, and continuous innovation in fixation systems, facial implants, and 3D-printed patient-specific solutions. Competition is intensifying as manufacturers focus on advanced biomaterials, virtual surgical planning, and CAD/CAM-based customized implants.

The manufacturers are increasingly investing in next-generation technologies such as 3D facial modeling, AI-driven planning software, and precision-guided osteotomy systems to enhance surgical outcomes. Strategic priorities include expanding product ranges, accelerating penetration in high-growth markets across Asia Pacific, and strengthening collaborations with maxillofacial and aesthetic surgeons. The growing shift toward minimally invasive contouring techniques and personalized implants continues to drive market growth.

Key Industry Developments:

- In June 2025, Aestiva Plastic Surgery, an aesthetic and reconstructive clinic, introduced an advanced scarless facial contouring technique, marking a first-of-its-kind advancement for individuals seeking facial sculpting without visible marks. This innovation enhances surgical precision while significantly improving aesthetic outcomes and postoperative recovery for patients.

Companies Covered in Facial Bone Contouring Market

- Stryker

- Johnson & Johnson

- Zimmer Biomet

- Acumed LLC

- Medtronic

- Smith + Nephew

- Wright Medical Group N.V

- NuVasive Inc

- Baxter International Inc

- KLS Martin Group

- CADskills

- Others

Frequently Asked Questions

The global facial bone contouring market is projected to be valued at US$ 1.6 Bn in 2026.

Growing demand for aesthetic facial restructuring procedures, supported by advances in 3D printing, imaging, and minimally invasive surgical techniques are driving the global facial bone contouring market.

The global facial bone contouring market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Rising adoption of 3D-printed patient-specific implants and virtual surgical planning systems are creating opportunities in the market.

Stryker, Johnson & Johnson, Zimmer Biomet, Acumed LLC, and Medtronic are some key players in the facial bone contouring market.