- Medical Devices

- Bone Densitometer Devices Market

Bone Densitometer Devices Market Size, Share, and Growth Forecast 2026 - 2033

Bone Densitometer Devices Market by Product Type (Axial Bone Densitometers, Peripheral Bone Densitometers), Technology (Dual-Energy X-ray Absorptiometry (DEXA/DXA), Quantitative Ultrasound (QUS), Quantitative Computed Tomography (QCT), Radiographic Absorptiometry (RA)), Application (Osteoporosis Diagnosis, Osteopenia Diagnosis, Body Composition Measurement), End-user (Hospitals, Diagnostic Centers, Specialty Clinics, Research Institutes), and Regional Analysis, 2026 - 2033

Bone Densitometer Devices Market Share and Trends Analysis

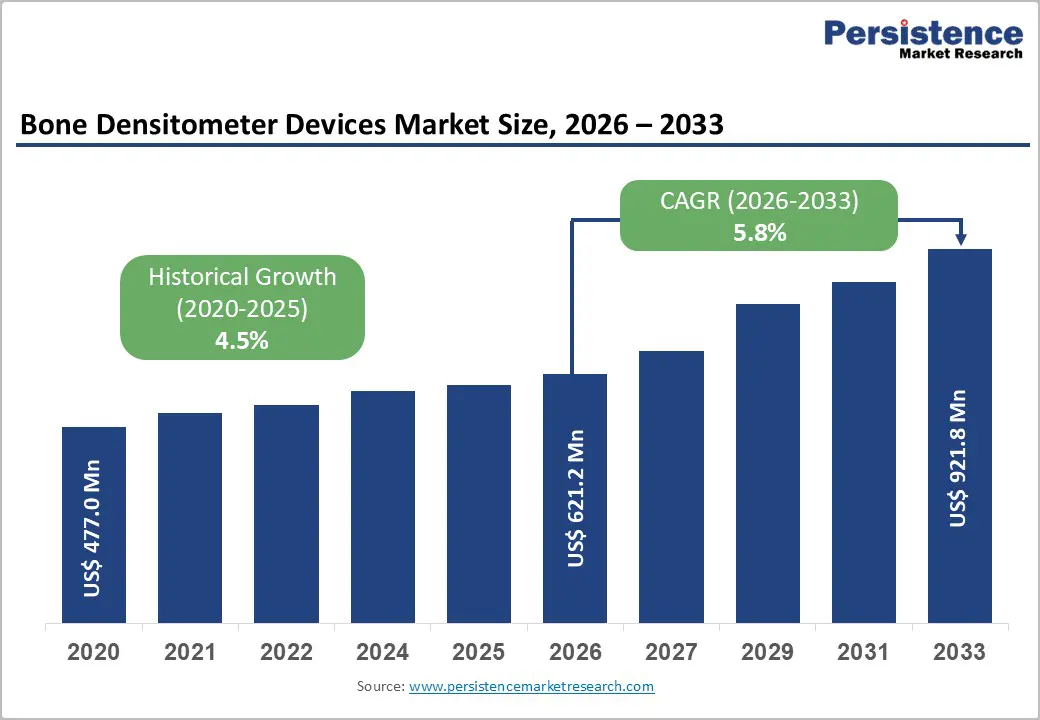

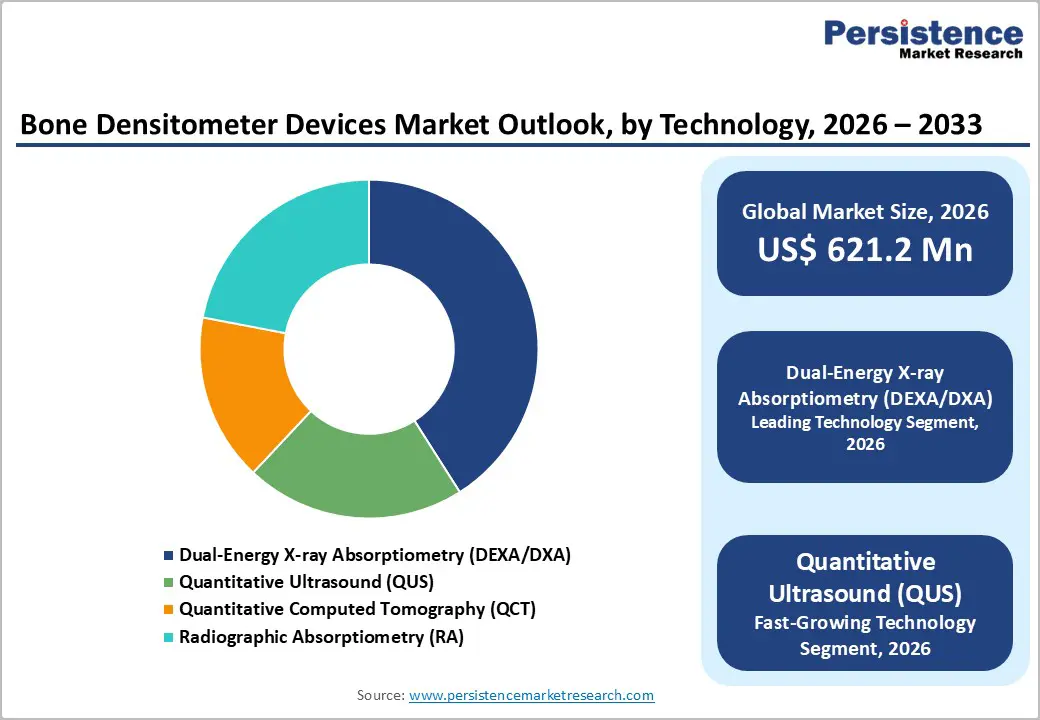

The global Bone Densitometer Devices market size is expected to be US$ 621.2 million in 2026 and to reach US$ 921.8 million by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

Robust demand is underpinned by the rising global burden of osteoporosis and fragility fractures, the rapid ageing of populations, and the expansion of evidence-based screening guidelines that prioritize bone mineral density assessment using central DEXA/DXA systems. These devices are increasingly complemented by portable and radiation-free modalities such as QUS and advanced ultrasound-based methods, expanding access to diagnosis in primary care, community, and rural settings while supporting long-term monitoring of bone health.

Key Industry Highlights:

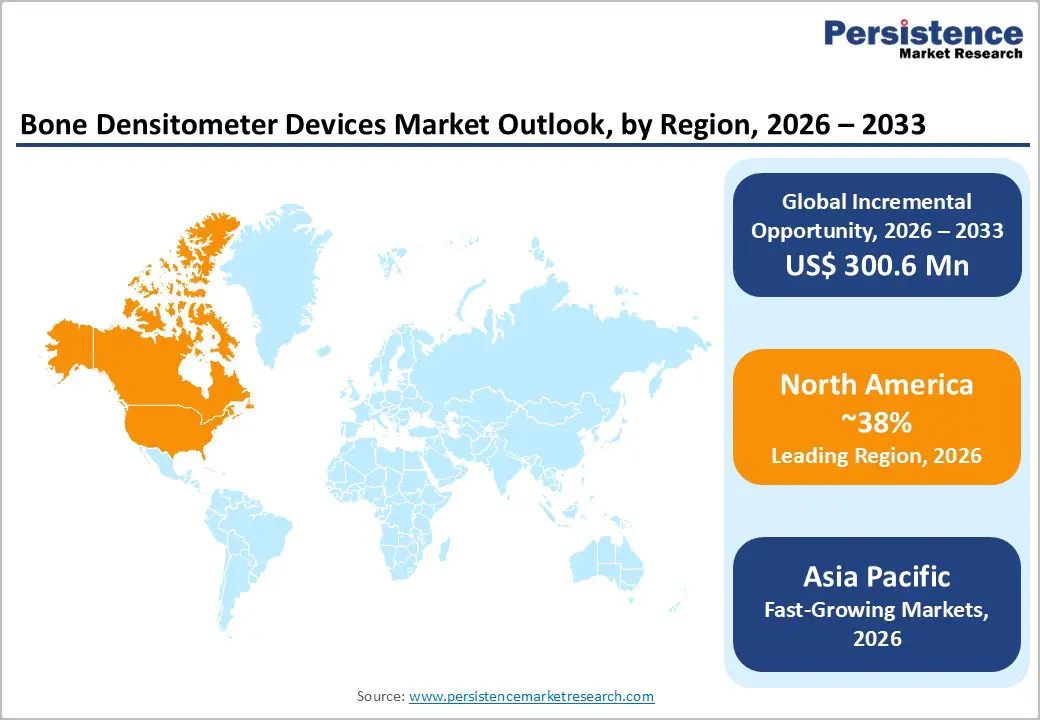

- Regional Leadership: North America is the leading regional market for bone densitometer devices, capturing around 38% share in 2025 due to high osteoporosis prevalence, strong screening guidelines, advanced imaging infrastructure, and the presence of major manufacturers offering state-of-the-art DXA platforms.

- Fast-growing Regional Market: The Asia Pacific bone densitometer devices market is the fastest-growing, supported by rapid population ageing, projections that more than 50% of global osteoporotic hip fractures will occur in Asia by 2050, and significant underdiagnosis, driving demand for both DXA and portable QUS devices.

- Leading Product: Axial Bone Densitometers and DEXA/DXA systems dominate installed bases, with DEXA/DXA accounting for about 41% of market share in 2025 owing to its gold-standard status for osteoporosis diagnosis, guideline endorsement, and ability to integrate advanced fracture risk tools.

- Fast-growing Technologies: Among emerging technologies, Quantitative Ultrasound (QUS) and axial ultrasound methods such as REMS represent the fastest-growing segments, leveraging radiation-free, portable designs that enable large-scale screening and rural outreach, particularly in resource-constrained regions across the Asia Pacific and other emerging markets.

| Key Insights | Details |

|---|---|

|

Bone Densitometer Devices Market Size (2026E) |

US$ 621.2 million |

|

Market Value Forecast (2033F) |

US$ 921.8 million |

|

Projected Growth CAGR (2026–2033) |

5.8% |

|

Historical Market Growth (2020–2025) |

4.5% CAGR |

Market Dynamics

Drivers - Rising Global Burden of Osteoporosis and Fragility Fractures

The primary growth driver for bone densitometer devices is the escalating prevalence of osteoporosis and associated fragility fractures in ageing populations worldwide. The International Osteoporosis Foundation (IOF) estimates that up to 37 million fragility fractures occur annually in individuals over 55 years, equivalent to roughly 70 fractures per minute, with around 1 in 3 women and 1 in 5 men over 50 expected to experience an osteoporotic fracture in their remaining lifetime. Meta-analytic data indicate a global osteoporosis prevalence of about 18.3%, with higher rates in women and in Asian and African populations, translating to approximately 500 million affected men and women over 50. This clinical and economic burden is driving healthcare systems to invest in earlier diagnosis and fracture prevention, directly increasing demand for central DEXA/DXA scanners and complementary devices used for baseline assessment and periodic bone mineral density (BMD) monitoring.

Expansion of Screening Guidelines and Preventive Care Programs

A second major growth driver is the strengthening of osteoporosis screening recommendations and preventive care initiatives, particularly in high-income regions. The U.S. Preventive Services Task Force (USPSTF) updated its clinical summary in 2025, recommending routine osteoporosis screening with DXA BMD for all women aged 65+ and for postmenopausal women under 65 with one or more risk factors, explicitly noting DXA as the core modality for fracture prevention strategies. Similar guidance from professional bodies in Europe and other regions reinforces DXA as the gold-standard technique for non-invasive diagnosis of osteoporosis and fracture risk assessment. As payers and governments increasingly recognize the cost savings associated with preventing hip and vertebral fracture events that double mortality risk and frequently lead to loss of independence, reimbursement, and quality metrics are aligning to support broader BMD testing, driving steady procedure volume growth for bone densitometer installations in hospitals, diagnostic centers, and specialty clinics.

Restraints - High Equipment Cost and Limited Access in Low-Resource Settings

Despite its clinical value, adoption of central DXA and advanced bone densitometry remains constrained by capital and operating costs, especially in low- and middle-income countries. The IOF and Asia-focused audits highlight that osteoporosis is significantly underdiagnosed and undertreated in many Asian nations, where large rural populations have limited access to specialized imaging centers and fracture liaison services. In such settings, the scarcity of trained technicians, the need for radiation-shielded facilities, and competition for imaging budgets with modalities such as CT and MRI slow the deployment and utilization of densitometers. This access gap dampens market penetration even where fracture risk is rising fastest.

Radiation Concerns and Low Awareness of Bone Health

A second restraint is persistent public and clinician under-appreciation of osteoporosis risk and concerns around radiation exposure, even though DXA employs very low-dose X-rays comparable to background radiation. Surveys cited by the IOF show that many postmenopausal women underestimate their personal fracture risk and do not proactively discuss osteoporosis with their physicians, leading to delayed or absent screening. In markets without organized fracture-prevention programs, this results in low referral rates for bone density testing, underutilization of installed densitometers, and slower equipment replacement or expansion cycles.

Opportunity - Growth of Portable, Radiation-Free Ultrasound and Novel Imaging Technologies

A key opportunity lies in the rapid uptake of portable and radiation-free technologies, particularly Quantitative Ultrasound (QUS) and novel ultrasound-based methods such as REMS (Radiofrequency Echographic Multi Spectrometry) for axial sites. Clinical literature shows that QUS devices, often applied to the heel or peripheral bones, are safe, easy to use, radiation-free, and highly portable, making them ideal for large-scale screening, pediatric assessment, and use in community or primary care settings. Recent studies from tertiary centers in Asia indicate that calcaneal QUS can efficiently detect osteopenia and osteoporosis in adults over 40, supporting its role as an accessible alternative or triage tool when central DEXA is unavailable. In 2024, Echolight S.p.A. announced a multi-year agreement allowing Siemens Healthineers to resell its REMS-based bone densitometers, which measure bone density and microarchitecture at the spine and femur via ultrasound without ionizing radiation, significantly broadening access to axial assessments and creating a strong growth runway for ultrasound-centric densitometry platforms.

Asia Pacific’s Rapidly Ageing Population and Large Diagnostic Care Gap

The Asia-Pacific region offers the most attractive long-term demand opportunity for bone densitometer vendors due to its demographic profile and substantial diagnostic gap. The IOF projects that more than 50% of all osteoporotic hip fractures worldwide will occur in Asia by 2050, driven by rapidly ageing populations and lifestyle changes. The APCO–IOF Asia Pacific Regional Audit 2025 highlights that in countries such as China, Japan, the Republic of Korea, Singapore, and Thailand, individuals aged 50+ will represent over 50% of the population by 2075, dramatically increasing the pool at risk for osteoporosis and fragility fractures. At the same time, osteoporosis remains markedly underdiagnosed and undertreated across the region, particularly in rural communities with limited access to central DXA. These dynamics create a compelling opportunity for both high-throughput hospital-based DXA systems and more affordable, portable QUS and ultrasound-based devices tailored to primary care and screening programs.

Category-wise Insights

By Product

By product type, Axial Bone Densitometers are expected to account for an estimated 65% share of the global market in 2025, outpacing Peripheral Bone Densitometers. This leadership is underpinned by clinical guidelines that prioritize central DXA measurements at the hip and lumbar spine as the reference standard for diagnosing osteoporosis and assessing fracture risk. Central systems enable comprehensive evaluation of critical skeletal sites, integration with tools such as FRAX, and precise follow-up of patients receiving anti-osteoporotic therapies. Axial densitometers are also more commonly installed in hospitals and large diagnostic centers, where they can support both skeletal health and full-body composition analysis, reinforcing their share advantage and making them the anchor modality in most osteoporosis management pathways.

By Technology

In technology terms, Dual-Energy X-ray Absorptiometry (DEXA/DXA) is the leading segment, accounting for approximately 41% of the bone densitometer devices market in 2025. DEXA/DXA remains the globally accepted gold-standard technique for non-invasive osteoporosis diagnosis and for quantifying BMD, with strong consensus among regulatory bodies and professional societies. It offers high accuracy, rapid scan times, and very low radiation dose, and is the modality explicitly recommended in osteoporosis screening guidelines such as those from the USPSTF and American and European clinical societies. While QUS is the fastest-growing technology segment due to its radiation-free, portable profile and suitability for mass screening and rural outreach, DEXA/DXA systems from players such as GE HealthCare and Hologic, Inc. continue to dominate installed bases in acute-care and specialist settings and increasingly incorporate body composition, trabecular bone score, and fracture risk analytics.

By End-user

Among end users, Hospitals are projected to hold the largest share of around 45% in 2025, ahead of Diagnostic Centers, Specialty Clinics, and Research Institutes. Hospitals are typically the first point of care for hip and vertebral fractures, which are associated with substantial morbidity, functional decline, and up to a twofold increase in mortality within the first year. As a result, many institutions integrate bone densitometry into fracture liaison services, orthopedic workflows, and geriatric assessment units, relying on central DEXA platforms to stratify fracture risk and guide pharmacologic therapy. Hospitals also benefit from the broader clinical utility of advanced systems such as Lunar iDXA and Horizon DXA, which support body composition, metabolic health, and research applications. While independent diagnostic centers are expanding rapidly in some regions, particularly North America and the Asia Pacific, the hospital segment remains the dominant buyer and user of high-throughput axial densitometers.

Regional Insights

North America Bone Densitometer Devices Market Trends and Insights

North America leads the Bone Densitometer Devices Market due to the high prevalence of osteoporosis, advanced healthcare infrastructure, and strong awareness regarding early diagnosis of bone-related disorders. The region has a rapidly aging population, which significantly increases the demand for bone mineral density testing and screening programs. Healthcare providers widely adopt advanced diagnostic technologies such as dual-energy X-ray absorptiometry systems because of their accuracy and clinical reliability in osteoporosis detection.

In addition, favorable reimbursement policies and the presence of well-established diagnostic centers and hospitals support the widespread use of bone densitometry devices across the region. Continuous technological advancements, including portable and low-radiation bone density scanners, are further improving diagnostic accessibility and efficiency. Research institutions and healthcare organizations also focus on preventive screening initiatives and clinical studies related to bone health, which strengthens market growth. Moreover, strong regulatory frameworks and the presence of major medical device manufacturers encourage product innovation and new device approvals. Increasing awareness about fracture risk assessment and bone health management among patients and physicians continues to reinforce North America’s leadership in the global bone densitometer devices market.

Asia Pacific Bone Densitometer Devices Market Trends and Insights

Asia Pacific is emerging as a significant growth region in the Bone Densitometer Devices Market, driven by the rising prevalence of osteoporosis and increasing awareness about bone health among aging populations. Countries such as China, Japan, India, and South Korea are witnessing a steady increase in the elderly population, which elevates the demand for early diagnosis of bone density disorders. Improving healthcare infrastructure, expanding diagnostic facilities, and growing investments in medical technologies are further supporting market expansion across the region. Governments and healthcare organizations are also promoting preventive healthcare programs and screening initiatives to address the burden of osteoporosis and related fractures. In addition, the adoption of cost-effective and portable bone densitometry technologies is increasing in hospitals and diagnostic centers, particularly in developing economies. The growing presence of local medical device manufacturers and rising healthcare expenditure are also contributing to market development. As awareness of bone mineral density testing improves and access to advanced diagnostic equipment expands, the Asia-Pacific region is expected to experience steady growth in the bone densitometer market.

Competitive Landscape

The Bone Densitometer Devices Market is characterized by a moderately consolidated competitive landscape with a mix of established global medical imaging manufacturers and emerging regional players. Leading participants maintain strong market positions through advanced product portfolios, extensive distribution networks, and continuous investments in research and development. Competition is primarily driven by technological innovation, including improvements in imaging accuracy, low-radiation scanning, AI-enabled analysis, and portable bone densitometry systems that enhance diagnostic efficiency. Companies also focus on strategic collaborations, partnerships, and geographic expansion to strengthen their presence in both developed and emerging healthcare markets. The growing demand for osteoporosis screening and preventive healthcare has intensified competition among manufacturers to introduce user-friendly and cost-effective solutions.

Key Developments:

- In June 2025, Echolight Medical LLC launched its novel Radiofrequency Echographic Multi Spectrometry (REMS), a radiation-free and portable bone densitometer designed to provide detailed profiling of patients’ bone health scores.

Companies Covered in Bone Densitometer Devices Market

- GE HealthCare, Hologic Inc.

- DMS Imaging, Swissray International, Inc.

- OSTEOSYS Co., Ltd.

- BeamMed Ltd.

- Scanflex Healthcare AB

- Echolight S.p.A.

- Trivitron Healthcare

- Medonica Co. Ltd.

- Shenzhen XRAY Electric Co., Ltd.

- Furuno Electric Co., Ltd.

- Eurotec Systems S.r.l

- AMPall Co., Ltd.

- OsCare Medical Oy

- Nanoomtech Co., Ltd.

- Xianyang Kanrota Digital Ultrasound System Co., Ltd.

- Nanjing Kejin Industrial Co., Ltd.

Frequently Asked Questions

The global Bone Densitometer Devices market size is expected to reach approximately US$ 621.2 million in 2026, supported by continued expansion of osteoporosis screening programs, ageing populations, and sustained investments in central DEXA/DXA and complementary peripheral and ultrasound-based systems.

Key demand drivers include the rising prevalence of osteoporosis and fragility fractures affecting an estimated 18.3% of the global population and up to 500 million men and women, as well as ageing demographics and guidelines recommending DXA-based screening to prevent disabling fractures.

North America leads the market, accounting for around 38% of global revenues in 2025, driven by high disease awareness, strong reimbursement frameworks, updated USPSTF guidelines favoring DXA screening, and the presence of leading manufacturers offering advanced DXA platforms.

The most significant opportunity lies in closing the osteoporosis care gap in Asia Pacific, where more than 50% of global osteoporotic hip fractures are projected to occur by 2050, through scaling hospital-based DXA, portable QUS, and ultrasound-based axial devices integrated into national screening and fracture prevention programs.

Leading players include GE HealthCare, Hologic, Inc., DMS Imaging, Swissray International, Inc., OSTEOSYS Co., Ltd., BeamMed Ltd., Scanflex Healthcare AB, Echolight S.p.A., Trivitron Healthcare, Medonica Co. Ltd., Shenzhen XRAY Electric Co., Ltd., and Furuno Electric Co., Ltd., which collectively offer a broad portfolio of DXA, QUS, and innovative ultrasound-based solutions.