- Medical Devices

- Orthopedic Bone Cement Market

Orthopedic Bone Cement Market Size, Share, and Growth Forecast, 2026 – 2033

Orthopedic Bone Cement Market by Product Type (Low Viscosity Cements, Medium Viscosity Cements, High Viscosity Cements, Others), Material (Polymethyl Methacrylate (PMMA), Calcium phosphate, Others), and Regional Analysis for 2026 – 2033

Orthopedic Bone Cement Market Size and Trends Analysis

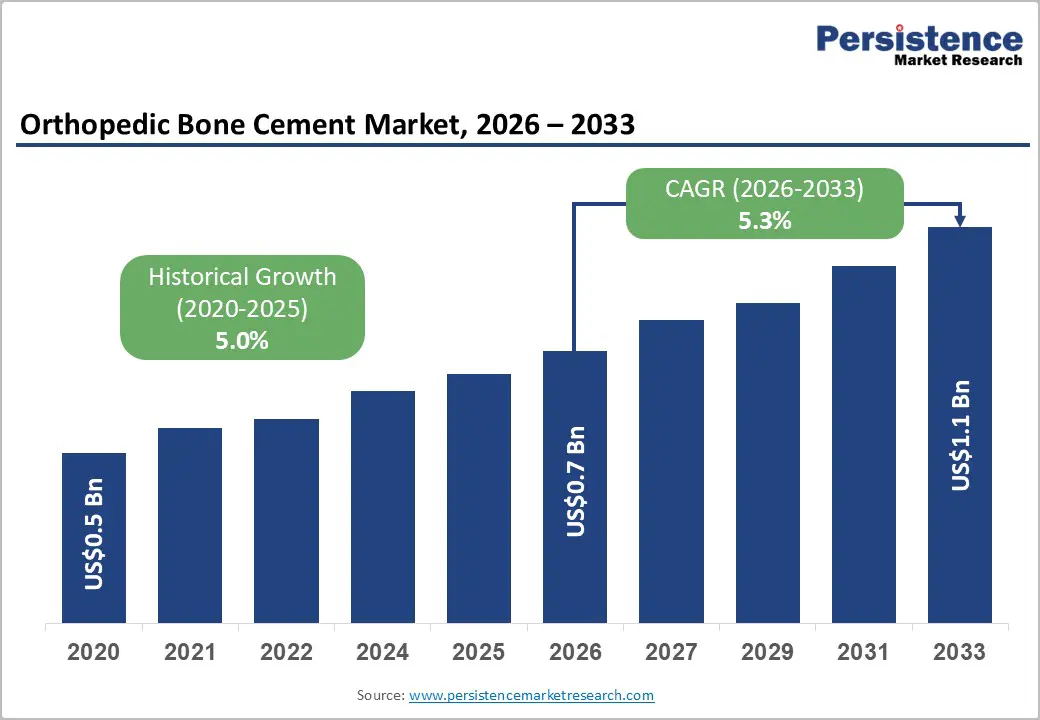

The global orthopedic bone cement market size is likely to be valued at US$0.7 billion in 2026 and is expected to reach US$1.1 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by the increasing demand for joint replacement procedures such as hip and knee arthroplasty, fueled by the rising prevalence of musculoskeletal disorders and an aging population worldwide.

According to the World Health Organization, the global population aged 85 years or more will increase by 351% in the following 40 years. Osteoporosis International Journal estimated that 158 million people aged 50 years or above are highly prone to developing bone fractures. The growing incidence of osteoporosis, fractures, and orthopedic trauma necessitates effective bone stabilization and implant fixation. Healthcare infrastructure improvements, increasing surgical volumes in both hospital and outpatient settings, and rising awareness among patients and clinicians about advanced orthopedic solutions are further driving demand.

Key Industry Highlights:

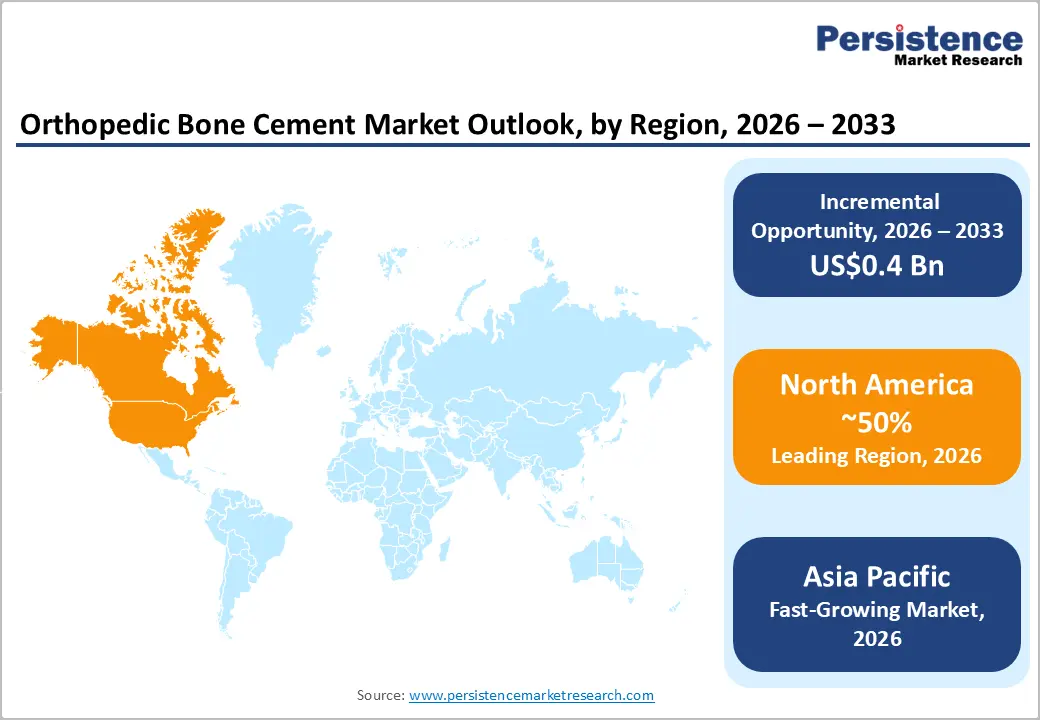

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 50% in 2026, driven by high procedure volumes, advanced healthcare infrastructure, and an aging population.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by large patient populations, rising healthcare expenditure, and expanding orthopedic procedure access.

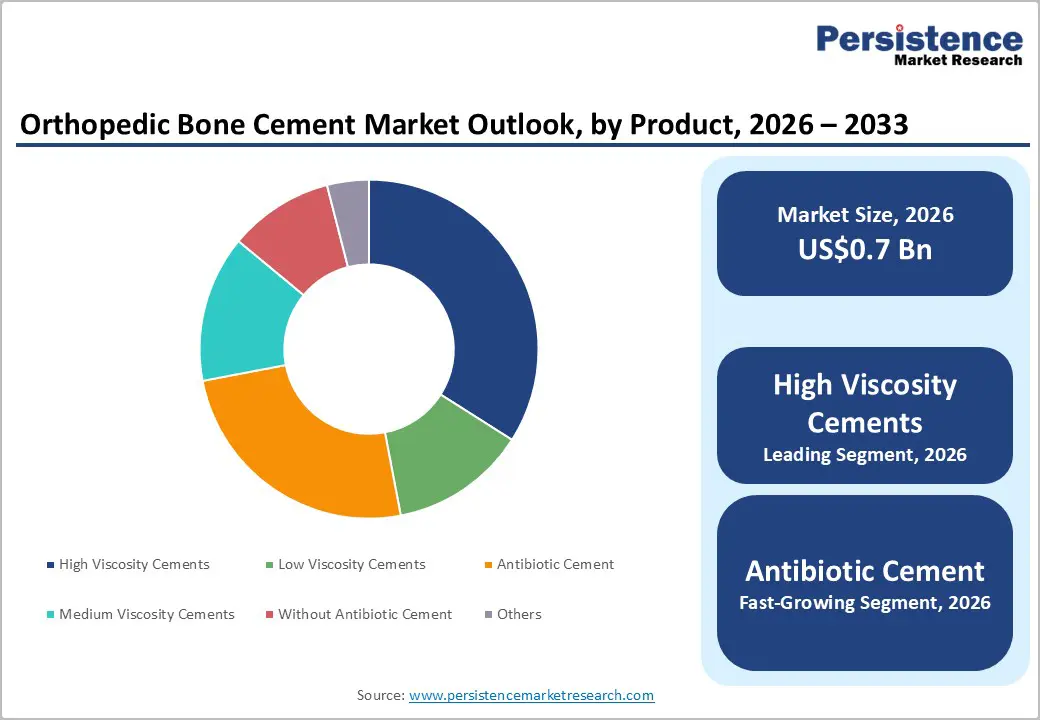

- Leading Product Type: High viscosity cements are projected to represent the leading product type in 2026, accounting for 45% of the revenue share, driven by superior handling characteristics and strong preference in complex arthroplasties.

- Leading Material: Polymethyl methacrylate (PMMA) is anticipated to be the leading material, accounting for over 60% of the revenue share in 2026, supported by its proven reliability, ease of use, and long clinical track record in cemented fixations.

| Key Insights | Details |

|---|---|

| Orthopedic Bone Cement Market Size (2026E) | US$0.7 Bn |

| Market Value Forecast (2033F) | US$1.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis- Rising Prevalence of Orthopedic Conditions and Surgical Volumes

The rise in musculoskeletal disorders, including osteoarthritis, fractures, and osteoporosis, has significantly increased the demand for orthopedic interventions. Aging populations in developed regions, along with lifestyle-related factors in emerging markets, have contributed to higher incidences of joint degeneration and trauma. The number of hip and knee replacement surgeries has grown steadily, driving orthopedic bone cement demand. Hospitals and surgical centers are performing more cemented procedures due to proven fixation reliability. This trend is reinforced by the expansion of healthcare infrastructure, greater patient awareness, and rising surgical volumes, positioning bone cement as a critical material in modern orthopedic practices.

The rising incidence of orthopedic trauma resulting from accidents and injuries further supports market growth. Patients with fractures or spinal compression frequently require stabilization using bone cement, particularly in procedures such as vertebroplasty and kyphoplasty. National healthcare programs and insurance coverage expansions in several countries are improving access to these surgical procedures, increasing demand for cement-based solutions. The increasing preference for joint replacement surgeries over non-surgical management of chronic conditions drives consistent procedural volumes.

Surgeons’ reliance on cemented fixation for predictable outcomes ensures sustained consumption of orthopedic bone cement across hospitals, outpatient centers, and specialized orthopedic clinics.

Advancements in Cement Formulations and Infection Control

Technological innovations in orthopedic bone cement, including high-viscosity, antibiotic-loaded, and bioactive formulations, are enhancing surgical outcomes and patient safety. Improved handling characteristics, reduced leakage risk, and controlled curing times make advanced cements increasingly preferred in complex arthroplasty procedures. Antibiotic-loaded cements help prevent post-operative infections, a major concern in joint replacement surgeries, thereby improving recovery rates.

Clinical studies demonstrating efficacy in reducing periprosthetic joint infections reinforce adoption. Continuous R&D efforts by key market players, combined with regulatory approvals for new formulations, are driving the replacement of traditional cements and fostering trust among surgeons.

Bioactive and dual-antibiotic cements are expanding the application spectrum of orthopedic bone cement, enabling integration with surrounding bone and tissue. These innovations also address rising concerns about infection and implant loosening, which are critical for long-term surgical success. Rapid-curing and customizable cement formulations allow surgeons to tailor procedures based on patient-specific needs, particularly in high-risk or revision surgeries. Advancements in cement delivery systems and compatibility with minimally invasive procedures contribute to efficiency and improved outcomes.

Barrier Analysis - Risk of Complications and Clinical Concerns

Despite the benefits, orthopedic bone cement use carries inherent risks, including cement leakage, thermal necrosis, and potential adverse reactions. Improper handling or excessive cement volumes during procedures can lead to post-operative complications such as embolism or implant failure. Clinical concerns also include variability in outcomes across different patient demographics, particularly elderly or osteoporotic individuals. Surgeons must follow strict protocols to mitigate these risks, which increases procedural complexity. These safety concerns can limit adoption in certain markets and discourage widespread use among smaller clinics or low-resource hospitals.

Concerns about long-term implant stability and potential interactions between cement and bone can impact surgeon preference. Rare but serious complications, such as allergic reactions or systemic toxicity, necessitate careful patient selection and monitoring. Liability considerations and heightened regulatory scrutiny in major markets, including the U.S. and Europe, create additional barriers to market expansion. Revision surgeries resulting from cement-related complications can incur higher costs and limit repeat adoption, particularly in cost-sensitive healthcare systems. These clinical and procedural risks act as a restraint, requiring ongoing training, improved formulations, and robust post-market surveillance to maintain confidence in orthopedic bone cement applications.

Competition from Alternative Fixation Technologies

Orthopedic bone cement faces competition from alternative fixation methods, including cementless implants, bioresorbable screws, and advanced internal fixation devices. Cementless prostheses, which rely on bone ingrowth for stability, are gaining popularity due to perceived lower complication rates and long-term durability. Minimally invasive internal fixation techniques and metal-based implants also provide alternatives in fracture and spinal applications. These substitutes appeal to surgeons seeking faster recovery, reduced procedural complexity, or lower infection risks. As awareness of alternative technologies grows, demand for traditional bone cement can be moderated, particularly in regions with advanced surgical infrastructure or high adoption of cementless techniques.

Emerging technologies such as 3D-printed implants, porous coatings, and hybrid fixation systems intensify competitive pressure on the bone cement market. Healthcare providers are increasingly evaluating cost-benefit ratios between cemented and cementless options, influencing procurement decisions. The perception that alternative methods may reduce revision rates or post-operative complications encourages adoption in high-income regions. Regulatory approvals and clinical guidelines favoring specific cementless systems can accelerate this trend.

Orthopedic bone cement manufacturers must innovate formulations, enhance performance characteristics, and differentiate through infection-control and bioactive solutions to maintain relevance against evolving fixation technologies.

Opportunity Analysis - Technological Convergence with Antibiotic and Bioactive Cements

The integration of antibiotic and bioactive agents into orthopedic bone cement presents significant growth opportunities. Combining infection control with enhanced bone integration addresses critical clinical challenges in joint replacement and trauma surgeries. Dual-function cements enable targeted delivery of antibiotics while supporting osteoconduction and reducing implant loosening. The convergence of technologies facilitates more predictable surgical outcomes and broadens application potential across complex arthroplasties and revision procedures. Ongoing R&D, regulatory approvals, and favorable clinical evidence drive adoption.

Antibiotic and bioactive cement innovations align with global healthcare priorities focused on reducing post-operative infections and improving recovery rates. Integration with delivery systems optimized for minimally invasive procedures enhances efficiency and safety, appealing to both surgeons and healthcare providers. These cements also support personalized approaches, enabling tailored antibiotic dosages and controlled release profiles to suit patient-specific risk factors. Technological convergence represents a significant opportunity for orthopedic bone cement manufacturers to innovate, expand adoption, and strengthen competitive positioning worldwide.

Minimally Invasive and Spine Applications

Techniques such as vertebroplasty and kyphoplasty leverage cement’s stabilization properties to treat vertebral compression fractures effectively. Minimally invasive approaches reduce hospital stays, enhance patient recovery, and lower overall procedural risk, driving higher adoption of bone cement in these interventions. The increasing prevalence of osteoporosis-related spinal fractures, particularly among the aging population, supports sustained demand. Advancements in delivery systems and imaging-guided procedures enable precise cement placement, improving clinical outcomes and expanding applications beyond traditional joint arthroplasty to broader orthopedic and trauma care.

Spinal applications and minimally invasive orthopedic procedures are gaining traction, particularly in regions investing in healthcare infrastructure and advanced surgical capabilities. Surgeons increasingly prefer cement-based stabilization in complex spine and trauma cases, where rapid structural support is critical. The rise in outpatient procedures and shorter hospitalization trends emphasizes the need for reliable, fast-setting bone cements. Technological improvements in injectable delivery devices and cement formulations tailored for vertebral and spinal applications enhance safety and effectiveness, creating new market opportunities.

Category-wise Analysis

Product Type Insights

High viscosity cements are expected to lead the orthopedic bone cement market, accounting for approximately 45% of revenue in 2026, driven by superior handling characteristics, which allow surgeons to precisely control placement and reduce the risk of cement leakage during complex arthroplasty procedures such as total hip and knee replacements. The predictable viscosity ensures stable fixation of implants, enhancing surgical outcomes and reducing post-operative complications.

For example, in total knee arthroplasty procedures, surgeons often prefer high-viscosity PMMA-based cements due to their consistent working time and strong mechanical interlock with bone surfaces, which supports long-term implant stability.

Antibiotic-loaded bone cements are likely to represent the fastest-growing segment, supported by rising awareness of infection risks associated with joint replacement and revision surgeries. These cements are designed to deliver targeted antibiotics locally, reducing the incidence of periprosthetic joint infections, which are among the most serious complications in orthopedic surgery. For example, gentamicin-loaded cements are widely used in hip and knee revisions to prevent infections in high-risk patients, demonstrating measurable reductions in post-operative infection rates.

Clinical studies and hospital protocols increasingly recommend antibiotic cement for both primary and revision procedures, particularly in regions with high surgical volumes.

Material Insights

Polymethyl methacrylate (PMMA) is projected to lead the market, capturing around 60% of the revenue share in 2026, supported by its long-standing clinical track record and proven reliability in cemented fixations. PMMA offers ease of use, predictable mechanical properties, and strong implant bonding, which makes it the material of choice for total hip and knee arthroplasty procedures. For example, PMMA is extensively used in cemented hip replacements, providing stable fixation and reducing the risk of implant loosening over long-term follow-up periods. Its ability to accommodate antibiotic additives for infection control further enhances its clinical value.

Calcium phosphate is likely to be the fastest-growing material, driven by its bioresorbable and osteoconductive properties that support bone integration. Unlike traditional acrylics, calcium phosphate cements gradually resorb and are replaced by natural bone tissue, reducing long-term complications and improving patient outcomes, particularly in trauma and spinal procedures. For example, in vertebroplasty procedures for osteoporotic vertebral compression fractures, calcium phosphate cement is preferred because it provides structural support while promoting bone regeneration and reducing the risk of cement-related complications.

Regional Insights

North America Orthopedic Bone Cement Market Trends

North America is anticipated to be the leading region, accounting for a market share of 50% in 2026, driven by a combination of strong healthcare infrastructure, high procedural volumes, and favorable reimbursement frameworks. The region’s aging population is a primary trend driver, as the incidence of osteoarthritis, fractures, and other musculoskeletal disorders rises with age, resulting in increased demand for hip and knee arthroplasty procedures where cemented fixation is preferred. Surgeon preference for high viscosity and antibiotic loaded cement formulations supports both clinical outcomes and market adoption.

The strategic emphasis is on collaborating with key orthopedic device manufacturers to integrate advanced bone cement solutions into comprehensive surgical offerings. For example, Zimmer Biomet has expanded its portfolio with high performance bone cement products and delivery systems that align with surgeon preferences for improved handling and reduced complication rates. Their initiatives include educational programs for surgeons that emphasize optimal cement handling techniques and outcomes data, contributing to increased product utilization in complex joint replacements.

Europe Orthopedic Bone Cement Market Trends

Europe is likely to be a significant market for orthopedic bone cement, due to advanced healthcare systems, aging populations, and high volumes of joint replacement and trauma procedures. Countries such as Germany, the U.K., and France consistently lead regional adoption due to well established healthcare infrastructure and high surgical rates, particularly for hip and knee arthroplasty. Public healthcare programs and universal coverage further support accessibility to orthopedic surgeries, expanding clinical demand for bone cement solutions.

The region also exhibits a strong interest in bioactive, antibiotic loaded, and resorbable cement formulations that improve clinical outcomes and address infection control needs.

Europe orthopedic bone cement market trends also include a notable shift toward minimally invasive procedures and tailored solutions for complex cases such as vertebral augmentation and spine stabilization. Strategic initiatives by manufacturers further illustrate evolving dynamics. For example, Heraeus Medical GmbH continues to invest in antimicrobial and advanced PMMA based cement formulations that meet European clinical and regulatory standards, reinforcing its position in key markets such as Germany and the UK. Such company-level efforts underscore how product differentiation, clinical support, and regional healthcare priorities are shaping orthopedic bone cement adoption and competitive landscapes across Europe.

Asia Pacific Orthopedic Bone Cement Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by rising healthcare infrastructure investments, increasing procedural volumes, and greater access to advanced orthopedic care across key countries such as China, India, Japan, and Southeast Asian nations. Aging populations in these countries are contributing to a surge in joint replacement and trauma related surgeries, which directly boosts demand for bone cement products used in implant fixation and vertebral procedures. There is also a growing preference for minimally invasive techniques such as vertebroplasty and kyphoplasty, which require specialized cement formulations to support rapid curing and effective stabilization.

Demand for cost effective and antibiotic loaded bone cement is increasing as clinicians focus on infection control and enhanced clinical outcomes in high volume surgical settings. For example, Johnson & Johnson MedTech (DePuy Synthes) continues to expand its portfolio of orthopedic solutions tailored for Asia Pacific surgical needs. Through product offerings that cater specifically to joint replacement and revision surgery requirements, DePuy Synthes strengthens its regional presence by addressing both standard and complex clinical demands. Their initiatives often include partnerships with local healthcare providers to enhance the adoption of advanced bone cement formulations and delivery systems, improving patient outcomes in high growth Asian markets.

Competitive Landscape

The global orthopedic bone cement market exhibits a moderately fragmented structure, driven by the presence of multiple established multinational companies alongside specialized regional players, each offering a range of PMMA, antibiotic loaded, high viscosity, and bioactive cement formulations across joint replacement, trauma, and spine procedures. Leading manufacturers such as Stryker have leveraged extensive product portfolios and strong distribution networks to maintain significant market positions, often integrating advanced cement delivery systems that improve handling and clinical outcomes.

With key leaders including Zimmer Biomet, DePuy Synthes (Johnson & Johnson), Smith & Nephew, Heraeus Medical GmbH, DJO Global Inc., Tecres S.p.A., and Cardinal Health, the competitive landscape reflects both global reach and specialized niche strategies. These players compete through sustained product innovation, strategic mergers and acquisitions, expanded geographic penetration, and robust post market clinical support to address evolving surgeon needs and procedural trends.

Key Industry Developments:

- In February 2026, Biocomposites announced the launch of its SYNICEM™ bone cement in the U.K. ahead of schedule to help address a supply shortage affecting orthopedic surgeries such as hip and knee replacements. The company also expanded production capacity to support hospital demand and ensure the continued availability of bone cement for orthopedic procedures.

- In March 2026, orthopedic biomaterials company Biocomposites expanded the availability of its SYNICEM™ bone cement in the U.K. market to support hospitals facing shortages of orthopedic bone cement used in joint replacement surgeries. The initiative aimed to stabilize supply for procedures such as hip and knee arthroplasty and help healthcare providers maintain continuity of orthopedic care during the ongoing supply disruption.

- In March 2025, Zimmer Biomet launched TEKCEM® 1G and TEKCEM® 3G antibiotic bone cements in India to enhance implant fixation in arthroplasty and joint reconstruction procedures. The products incorporate gentamicin for improved infection control and are designed to reduce monomer release and toxicity while improving implant stability in orthopedic surgeries.

Companies Covered in Orthopedic Bone Cement Market

- Stryker

- Zimmer Biomet

- Smith & Nephew

- DJO Global Inc. (Enovis)

- Arthrex Inc.

- Tecres S.p.A. (Demetra Holding S.p.A.)

- Heraeus Medical GmbH

- Cardinal Health

- Johnson & Johnson (Depuy Synthes)\

- SCANOS

Frequently Asked Questions

The global orthopedic bone cement market is projected to reach US$0.7 billion in 2026.

The orthopedic bone cement market is driven by the rising number of joint replacement surgeries and the increasing prevalence of musculoskeletal disorders among the aging population.

The orthopedic bone cement market is expected to grow at a CAGR of 5.3% from 2026 to 2033.

Key market opportunities include the development of antibiotic-loaded and bioactive bone cements, expanding applications in minimally invasive spine procedures, and increasing demand for advanced orthopedic solutions in emerging healthcare markets.

Stryker, Zimmer Biomet, DePuy Synthes, Smith & Nephew, and Arthrex Inc. are the leading players.