- Automotive Components & Materials

- Automotive Grade Inductor Market

Automotive Grade Inductor Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Grade Inductor Market by Product Type (SMD Power Inductors, Plug-in Power Inductors), Application (Transmission Control Units, LED Drivers, HID Lighting), and Regional Analysis for 2026 - 2033

Automotive Grade Inductor Market Size and Trends Analysis

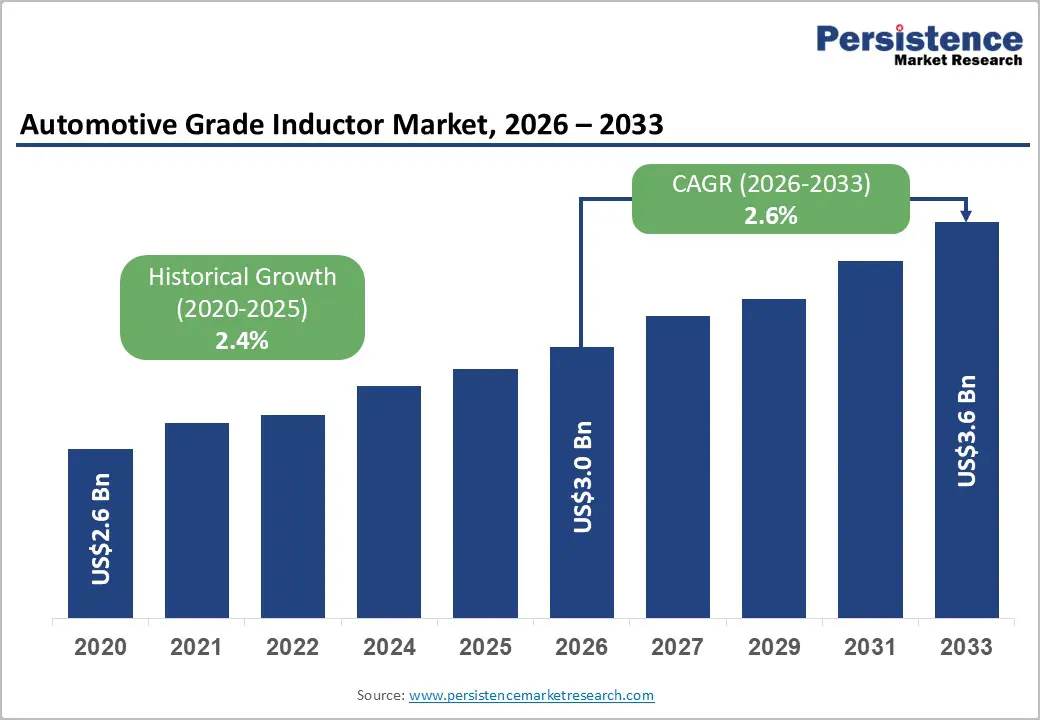

The global automotive grade inductor market size is likely to be valued at US$3.0 billion in 2026 and is expected to reach US$3.6 billion by 2033, growing at a CAGR of 2.6% during the forecast period from 2026 to 2033, driven by the increasing complexity and electrification of modern vehicles. As automotive architectures evolve, incorporating electric and hybrid powertrains, advanced driver assistance systems (ADAS), and connected vehicle technologies, the demand for high-performance inductors has intensified.

These components play a critical role in power management, signal filtering, EMI suppression, and energy storage across applications such as transmission control units, LED and HID lighting systems, and infotainment modules. Surface-mount (SMD) power inductors are gaining prominence due to their compact form factor and compatibility with high-density electronic circuits, while plug-in inductors continue to serve high-power applications.

Key Industry Highlights:

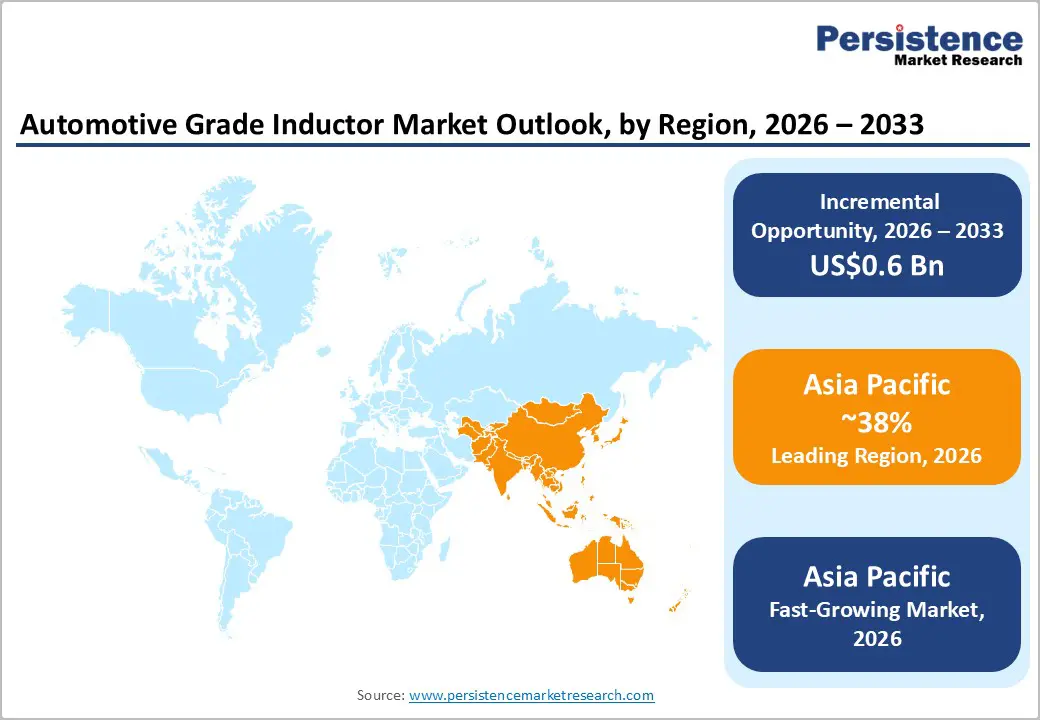

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by high EV adoption, supportive government regulations, and strong local manufacturing and supply chain capabilities.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by increasing EV adoption, favorable government policies, and robust local manufacturing and supply chain infrastructure.

- Leading Product Type: SMD power inductors are projected to represent the leading product type in 2026, accounting for 62% of the revenue share, driven by their compatibility with automated PCB assembly and compact form factors essential for modern ECUs.

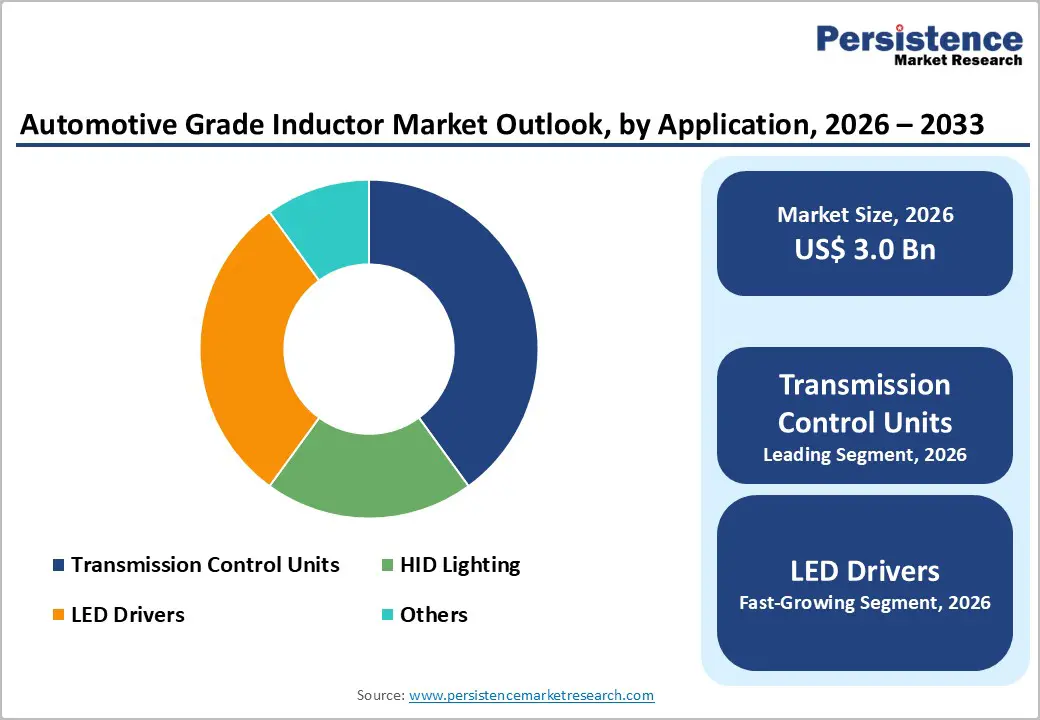

- Leading Application: Transmission control units are anticipated to be the leading application type, accounting for over 38% of the revenue share in 2026, supported by the growing adoption of automatic transmissions and the complexity of EV powertrain systems.

| Key Insights | Details |

|---|---|

|

Automotive Grade Inductor Market Size (2026E) |

US$3.0 Bn |

|

Market Value Forecast (2033F) |

US$3.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

2.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis- Accelerated Electrification of Vehicle Powertrains

The shift toward electric and hybrid vehicles is accelerating the demand for automotive-grade inductors. These components play a crucial role in DC-DC converters, battery management systems, and onboard chargers, ensuring efficient power delivery and signal integrity. As traditional internal combustion engines transition to electrified powertrains, OEMs require the high-reliability inductors that can operate under high currents and varying thermal conditions. The integration of 48V architectures and high-voltage systems in mild-hybrid and fully electric vehicles is driving the need for miniaturized, high-performance SMD and plug-in inductors, which are becoming essential enablers of next-generation EV power electronics.

Electrification also increases system complexity, requiring inductors capable of managing voltage fluctuations and EMI suppression in compact spaces. Powertrain controllers, inverter modules, and regenerative braking systems rely on high-current inductors to maintain efficiency and safety. Regional policies promoting EV adoption, particularly in Asia Pacific and Europe, intensify the demand for automotive-grade inductors. Manufacturers are investing in innovative magnetic materials and designs to support higher current densities and thermal stability, ensuring reliable performance across diverse operating environments.

Growth in Energy-Efficient Lighting Systems

The automotive lighting segment is rapidly evolving with the adoption of LED, matrix LED, and adaptive lighting technologies. These systems require precise current regulation and EMI suppression, roles effectively fulfilled by automotive-grade inductors. As consumers demand brighter, energy-efficient, and customizable lighting solutions, manufacturers increasingly rely on SMD and plug-in inductors to manage current flow in compact LED driver circuits. Government regulations and incentives for energy-efficient vehicle components accelerate this trend, making inductors indispensable for modern lighting architectures.

LED and HID systems in both passenger and commercial vehicles are increasingly integrated with ADAS and automated signaling functions, increasing electronic content. Inductors stabilize voltage, reduce ripple, and protect circuits from electromagnetic interference, supporting system reliability. With vehicles incorporating multiple LED modules for headlamps, taillights, and interior lighting, the aggregate requirement for high-performance inductors rises.

Barrier Analysis - Supply Chain Vulnerabilities in Critical Materials

The automotive grade inductor market faces potential constraints due to the reliance on critical raw materials such as ferrite, copper, and high-grade magnetic alloys. Fluctuations in material availability, geopolitical tensions, or trade restrictions can lead to production delays and increased costs. Many inductors require high-purity ferrites or specialized alloys to achieve desired inductance and thermal stability, and disruptions in supply chains can affect both SMD and plug-in production, delaying OEM delivery schedules.

Semiconductor shortages indirectly impact inductor manufacturing as these components are integrated with power electronics. Long lead times and concentration of suppliers in specific regions exacerbate vulnerability. Companies are exploring localized sourcing, multi-supplier strategies, and recycling approaches to mitigate risks. However, the dependence on specialized raw materials remains a significant challenge that slows market expansion despite growing demand for automotive-grade inductors in EVs, ADAS, and energy-efficient lighting applications.

Technological Complexity in High Voltage Architectures

These inductors must withstand elevated currents, thermal stress, and electromagnetic interference while maintaining high efficiency. Designing compact SMD inductors capable of operating reliably in high voltage inverters and DC-DC converters presents significant engineering challenges. Integration with battery management systems and powertrain electronics requires tight tolerance and precise magnetic characteristics, increasing design and testing efforts. Rising adoption of EVs and 48V mild-hybrid systems intensifies the demand for inductors that can handle high switching frequencies without performance degradation.

Thermal management and insulation are critical, as overheating can compromise performance and safety. OEMs and Tier-1 suppliers face challenges in ensuring inductors meet AEC-Q200 standards while supporting miniaturized layouts for space-constrained ECUs. The need for high voltage compatibility, low losses, and EMI suppression in a single package adds manufacturing complexity. Market players are increasingly investing in advanced magnetic materials and multi-layer winding techniques to optimize efficiency and reliability.

Opportunity Analysis - Technological Convergence with Wide Bandgap Semiconductors

The integration of wide-bandgap (WBG) semiconductors, such as silicon carbide (SiC) and gallium nitride (GaN), in automotive power electronics creates new opportunities for inductors. WBG devices operate at higher voltages, frequencies, and temperatures, requiring inductors with superior thermal stability and low-loss characteristics. Automotive grade inductors designed for WBG integration enable smaller, more efficient converters and inverters in EVs, enhancing system performance while reducing overall vehicle weight.

High-frequency operation enabled by WBG semiconductors allows for miniaturized inductors with increased power density. OEMs can leverage this convergence to optimize powertrain efficiency and extend battery range. The use of advanced magnetic materials and innovative winding techniques creates avenues for product differentiation. Companies investing in R&D to produce inductors compatible with high-speed, high-voltage WBG architectures can capture growing demand across EVs, hybrid vehicles, and next-generation power electronics, making this convergence a major market opportunity.

Sustainability and Low- Aftermarket and Retrofit Demand

As vehicle fleets age, there is increasing demand for upgrading lighting systems, powertrain modules, and ADAS features. Inductors are critical components in retrofitted LED lighting, inverter upgrades, and energy-efficient auxiliary systems, allowing older vehicles to meet modern efficiency and safety standards. This aftermarket demand extends the life cycle of inductors and creates additional revenue streams for manufacturers. Increasing availability of cost-optimized SMD inductors and plug-in variants enables easier integration into legacy vehicles, while OEM-certified aftermarket kits ensure reliability and compliance with automotive standards.

Retrofitting EV conversion kits and performance upgrades in regions with rising EV adoption drives demand. Tier-2 and aftermarket suppliers can offer compact, high-performance SMD inductors tailored for these applications. The combination of cost-effective solutions, increasing consumer awareness of energy efficiency, and regulatory encouragement for modernization enhances growth prospects. Collaborations between inductor manufacturers and aftermarket suppliers are expanding product availability and technical support for end-users.

Category-wise Analysis

Product Type Insights

SMD power inductors are expected to lead the automotive grade inductor market, accounting for approximately 62% of revenue in 2026, driven by their compatibility with automated PCB assembly lines and compact form factors, which are essential for modern, space-constrained ECUs in vehicles. For example, in EV powertrain modules, SMD power inductors are used in DC-DC converters to efficiently manage high currents in a small footprint, ensuring a stable voltage supply for battery management systems. Their reduced DC resistance in newer generations allows higher current ratings without increasing size, supporting advanced powertrain and infotainment electronics.

SMD power inductors are likely to represent the fastest-growing segment, supported by OEMs prioritizing surface-mount designs to achieve higher production efficiency and lower assembly costs. For example, modern adaptive cruise control modules incorporate compact SMD power inductors to filter noise and maintain precise signal integrity, supporting safety-critical features in connected vehicles. Their ability to operate reliably under high switching frequencies and thermal stress makes them ideal for increasingly electrified powertrains. As vehicles integrate multiple electronic systems such as infotainment, navigation, and LED lighting, the demand for high-density, compact inductors continues to rise.

Application Insights

Transmission control units (TCUs) are projected to lead the market, capturing around 38% of the revenue share in 2026, supported by high power inductors to manage torque converter and shift control electronics, particularly in vehicles with automatic transmissions and dual clutch EV systems. For example, in modern dual clutch transmissions, automotive grade inductors regulate current flow in the solenoids and control circuits, ensuring precise gear engagement and smooth shifting under variable load conditions. The growth of automatic transmission penetration in new vehicles enhances the demand for reliable inductors capable of withstanding thermal and electrical stress.

LED drivers are likely to be the fastest-growing application, driven by the rapid adoption of energy-efficient and adaptive lighting systems in modern vehicles. Growth is fueled by consumer demand for premium illumination and regulatory pushes for energy-efficient lighting solutions. For example, matrix LED headlights in high-end EVs incorporate automotive grade inductors to regulate current precisely, reduce electromagnetic interference, and ensure consistent brightness across multiple light modules. Inductors in LED drivers also contribute to the miniaturization of lighting control circuits, enabling compact headlamp designs that fit within aerodynamic vehicle profiles.

Regional Insights

North America Automotive Grade Inductor Market Trends

North America is likely to be a significant market for automotive grade inductor in 2026, driven by increasing adoption of electric vehicles, hybrid powertrains, and advanced driver assistance systems (ADAS). Rising consumer demand for energy-efficient vehicles and regulatory mandates for reduced emissions are encouraging OEMs to integrate high-performance inductors in power electronics and lighting systems. For example, Coilcraft, Inc., a leading North American manufacturer, has developed high-current SMD inductors for EV inverters and powertrain modules that meet stringent AEC-Q200 automotive standards.

Another major trend shaping the North America market is the increasing deployment of advanced lighting systems, including LED and adaptive matrix lighting, in both passenger and commercial vehicles. Automotive-grade inductors are integral to these systems, regulating current, suppressing noise, and enabling compact driver circuits. The rise of 48 V mild-hybrid systems and electrified auxiliary components also contributes to higher electronic content per vehicle, boosting inductor demand. Regional supply chain advantages, such as local manufacturing capabilities and proximity to Tier-1 suppliers, allow faster product development and customization for OEM requirements.

Europe Automotive Grade Inductor Market Trends

Europe is likely to be a significant market for automotive grade inductor in 2026, due to stringent environmental regulations, increasing electrification of vehicles, and the growing adoption of advanced driver assistance systems (ADAS). The rise of electric vehicles (EVs) and hybrid models across Europe has elevated demand for high-performance inductors in powertrain systems, DC-DC converters, battery management systems, and onboard chargers. For example, TDK Corporation has supplied automotive-grade SMD and power inductors for European EV inverters, supporting compact designs with high current capacity and low DC resistance while meeting AEC-Q200 standards.

Another notable trend in Europe is the adoption of 48 V mild-hybrid systems and electrified auxiliary modules, which significantly increase the inductor content per vehicle. Inductors are integral in regulating current in LED drivers, powertrain electronics, and high-voltage inverters, ensuring efficiency and reliability under thermal and electrical stress. The market benefits from well-established manufacturing ecosystems, proximity to Tier-1 automotive suppliers, and a strong focus on research and development in advanced magnetic materials. The increasing prevalence of adaptive lighting, autonomous driving technologies, and connected vehicle systems also fuels demand for inductors capable of high-frequency operation and EMI suppression in compact footprints.

Asia Pacific Automotive Grade Inductor Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by the rapid adoption of electric vehicles (EVs), hybrid powertrains, and advanced driver assistance systems (ADAS) across China, Japan, India, and ASEAN countries. The region’s dominance is supported by favorable government policies, subsidies for EV adoption, and regulatory mandates for energy efficiency and emissions reduction. For example, Murata Manufacturing Co., Ltd. has developed high-performance SMD inductors for EV powertrain modules in China and Japan, providing compact designs with low DC resistance and high thermal endurance, which are essential for densely packed ECUs.

A key trend in Asia Pacific is the growth of 48 V mild-hybrid systems and high-voltage architectures, which increase inductor content per vehicle while demanding higher performance standards. Compact, high-frequency inductors are increasingly required to manage power efficiently in battery management systems, inverters, and auxiliary electronics. Countries such as China and India are investing heavily in local semiconductor and passive component manufacturing, enabling rapid development and supply of automotive-grade inductors.

Competitive Landscape

The global automotive grade inductor market exhibits a moderately fragmented structure, driven by the presence of established multinational component manufacturers alongside specialized niche players competing to serve evolving automotive electronics needs. Leading firms leverage long-standing relationships with OEMs and Tier-1 suppliers, investing heavily in R&D to deliver compact, high-efficiency inductors that meet stringent automotive quality standards such as AEC-Q200.

With key leaders including TDK Corporation, Murata Manufacturing Co., Ltd., and Vishay Intertechnology, Inc., the competitive landscape is shaped by technological differentiation and strategic initiatives. These players compete through continuous product innovation, expansion of production capacity, and strategic partnerships with automakers to integrate inductive components into next-generation vehicle platforms.

Key Industry Developments:

- In August 2025, Vishay Intertechnology launched two automotive-grade inductors, the IHDM-1107BBEV-2A and IHDM-1107BBEV-3A, for high-current automotive power applications. These edge-wound, through-hole inductors feature powdered iron alloy cores for stable inductance, low power loss, and superior heat dissipation (-40°C to +180°C). They deliver up to 30% higher rated and saturation current at +125°C compared to ferrite-based solutions.

- In April 2025, Bourns introduced three automotive-grade chip inductor series, CWF1610A, CWF1612A, and CWF2012A, designed for high current and inductance in compact sizes. These AEC-Q200-compliant inductors use wirewound ferrite cores to minimize resistance, filter noise, and handle high frequencies. They are ideal for RF signal processing, resonant circuits, decoupling, and low-current DC power lines in automotive, power, audio, and mobile applications.

Companies Covered in Automotive Grade Inductor Market

- TDK Corporation

- Murata Manufacturing Co., Ltd.

- Vishay Intertechnology, Inc.

- Taiyo Yuden Co., Ltd.

- Panasonic Corporation

- Coilcraft, Inc.

- Bourns, Inc.

- Sumida Corporation

- Eaton Corporation plc

- KEMET Corporation

Frequently Asked Questions

The global automotive grade inductor market is projected to reach US$3.0 billion in 2026.

The automotive-grade inductor market is driven by increasing vehicle electrification, rising adoption of EVs and hybrid powertrains, and growing demand for advanced electronic systems such as ADAS and energy-efficient lighting.

The automotive grade inductor market is expected to grow at a CAGR of 2.6% from 2026 to 2033.

Key market opportunities lie in the growing demand for electric and hybrid vehicles, advanced driver assistance systems, energy-efficient lighting, and aftermarket/retrofit upgrades.

TDK Corporation, Murata Manufacturing Co., Ltd., Vishay Intertechnology, Inc., and Taiyo Yuden Co., Ltd are the leading players.