- Automotive Components & Materials

- Automotive Active Health Monitoring Systems Market

Automotive Active Health Monitoring Systems Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Active Health Monitoring Systems Market by System Location (Driver’s Seat and Dashboard), by Component (Sensors, Software and Hardware), Application Outlook (Pulse Rate, Blood Sugar Level, Blood Pressure and Misc.), End-user (Passenger Car, LCV and HCV) and Regional Analysis for 2025 - 2032

Automotive Active Health Monitoring Systems Market Size and Trends Analysis

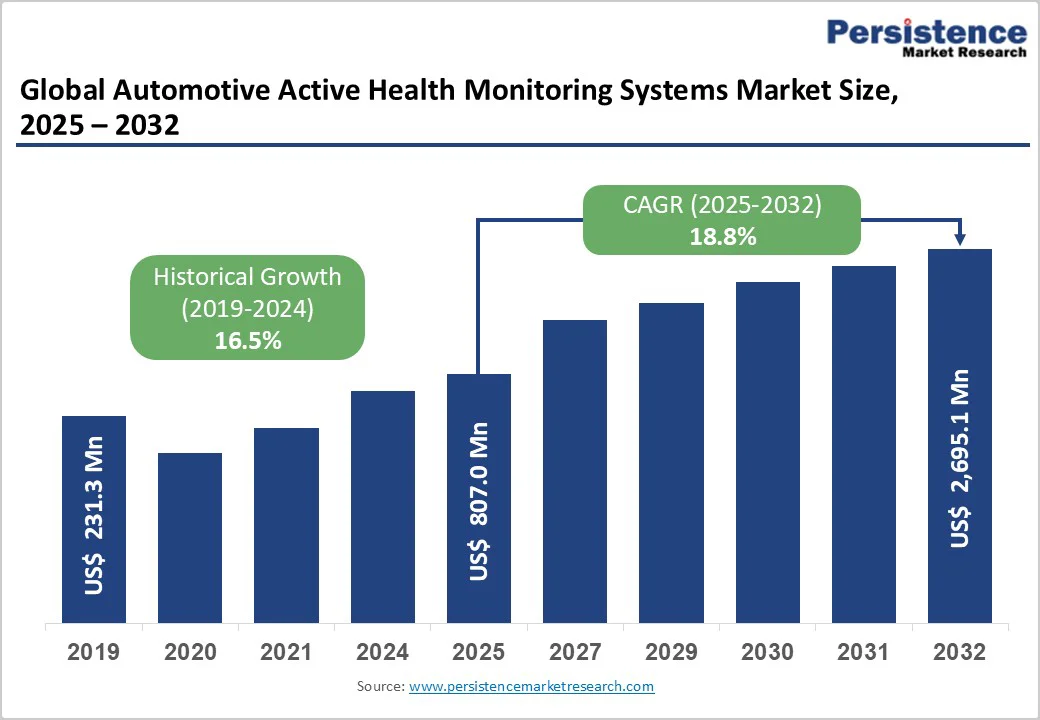

The global automotive active health monitoring systems market size was valued at US$807.0 million in 2025 and is projected to reach US$2,695.1 million by 2032, growing at a CAGR of 18.8% between 2025 and 2032.

This exceptional expansion reflects growing safety regulations mandating driver-monitoring technologies, technological convergence enabling biometric sensors integrated into steering wheels and seats, achieving 95% detection accuracy, and strategic automotive-industry investment in AI-driven wellness ecosystems supporting the autonomous-vehicle transition.

Key Industry Highlights:

- Location Segment Leadership: Dashboard-mounted driver monitoring systems dominate with 63.2% market share, driven by cost-efficient camera integration and wide OEM adoption. The driver’s seat segment is the fastest-growing, with a 22% CAGR, supported by superior biometric signal accuracy and the rise of smart seating platforms incorporating wellness, posture, and fatigue-detection technologies.

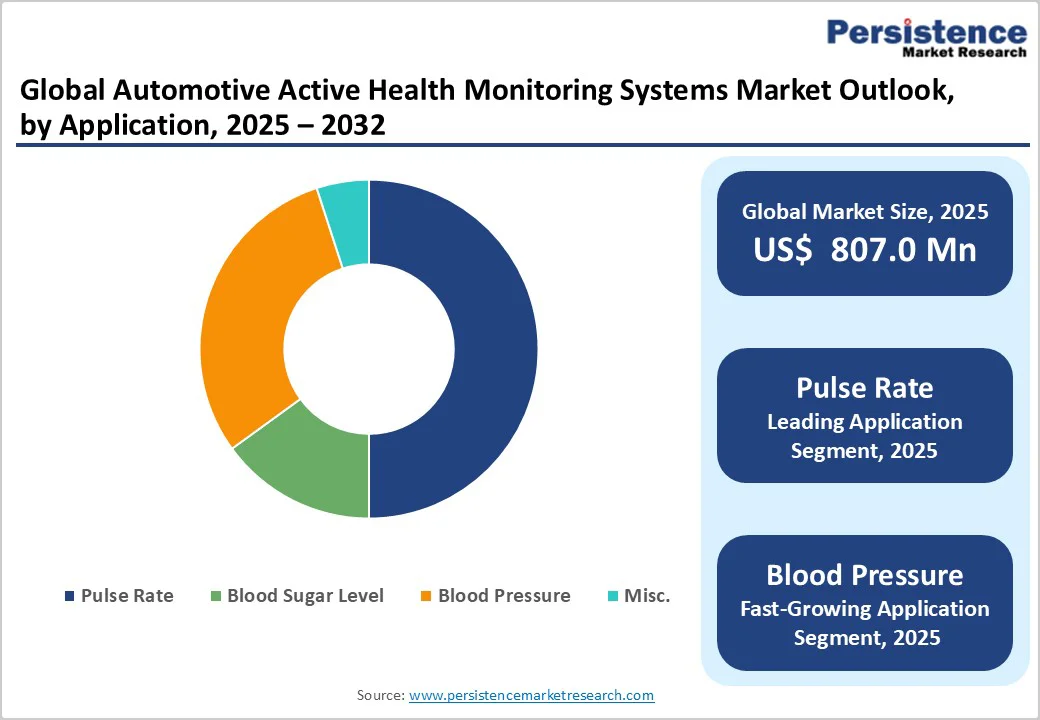

- Application Dynamics: Pulse-rate monitoring leads with 48.6% share, reflecting its critical role as the primary vital-sign indicator and long-established clinical relevance. Blood-pressure monitoring is the fastest-growing application at 30% CAGR, propelled by increasing hypertension prevalence exceeding 1.3 billion individuals globally and OEM focus on preventive health features.

- Vehicle Category Trends: Passenger cars command a 64.3% share, underpinned by high global production and rapid integration of advanced interior sensing in luxury vehicles. Light commercial vehicles (LCVs) represent the fastest-growing category at 20% CAGR, driven by fleet-safety investments and e-commerce delivery expansion.

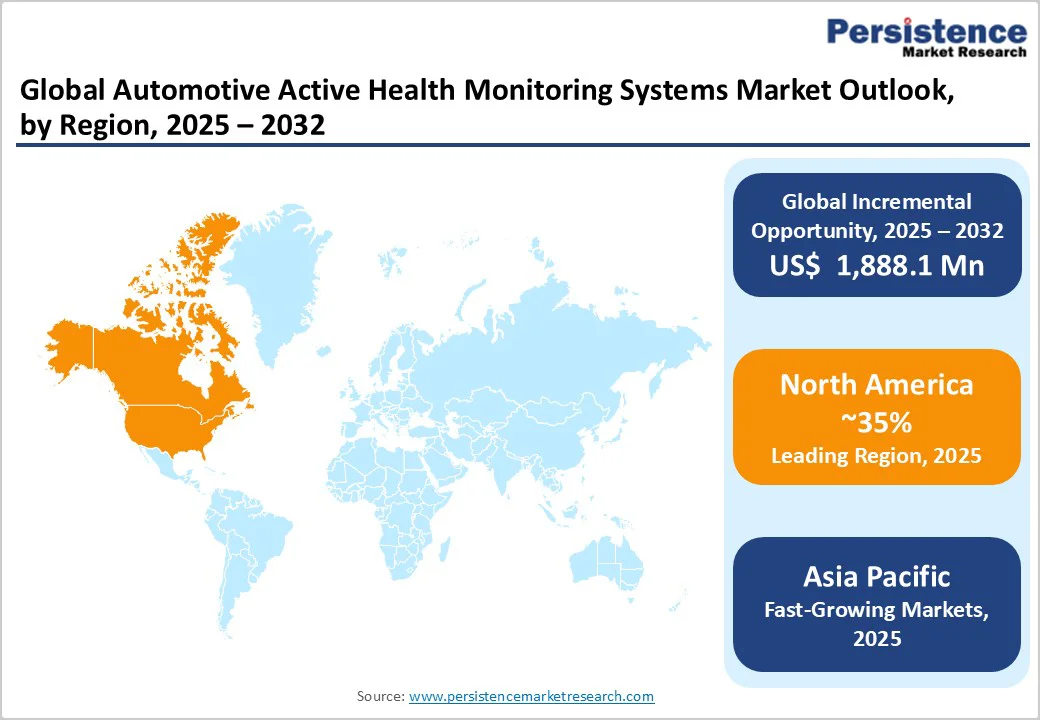

- Regional Growth Patterns: North America dominates with 35% share, expanding at 16.5% CAGR through deployments from Ford, GM, and Tesla. Asia Pacific is the fastest-growing region at 21.5% CAGR, fueled by Hyundai’s Smart Cabin program and China’s national smart-vehicle initiatives.

- Strategic Market Developments: Bosch leads with 12% market share, supported by strong interior-sensing portfolios. Continental, Harman, and DENSO maintain competitive positions. Commercial fleet adoption represents a substantial US$800M–$1.2B opportunity by 2032, driven by measurable ROI in safety compliance and driver-risk reduction.

| Key Insights | Details |

|---|---|

|

Market Size (2025E) |

US$ 807.0 Mn |

|

Market Value Forecast (2032F) |

US$ 2,695.1 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

18.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

16.5% |

Market Dynamics

Growth Drivers

Rising Road Safety Concerns and Regulatory Mandates Addressing Driver Health-Related Accidents

Global road safety crisis, with over 20% of automotive accidents attributed to driver health issues, including heart attacks, fatigue, stress, and drowsiness, creates compelling regulatory and commercial imperative for active health monitoring systems, preventing medical emergencies while driving. Driver health detection systems monitoring vital signs including heart rate (HR) and respiration rate (RR) enable early detection of conditions like sleep apnea, heart disease, and stress providing real-time alerts and emergency service communication during medical events. Advanced

Driver Assistance Systems (ADAS) market growth is driven by regulatory requirements for driver monitoring, with Euro NCAP and NHTSA increasingly mandating driver state detection technologies as a prerequisite for five-star safety ratings, supporting system adoption across vehicle segments. Driver Monitoring Systems (DMS) track driver behavior through cameras and sensors, monitoring eye movement, head positioning, and facial expressions, detecting fatigue, distraction, or impairment with real-time alerts prompting driver focus restoration, reducing accident likelihood by 15%.

Technological Advancement in Biometric Sensors and AI-Driven Health Analytics

Revolutionary improvements in biometric sensor accuracy, miniaturization, and integration capabilities enable seamless vehicle incorporation of health monitoring achieving 95%+ detection accuracy through advanced computer vision algorithms and multi-sensor fusion delivering comprehensive wellness assessment. Sensor fusion techniques combining infrared cameras, ultrasonic sensors, millimeter-wave radar, and seat-embedded pressure sensors create 360-degree driver and occupant monitoring, overcoming individual sensor limitations, including extreme lighting conditions or rapid vehicle movements.

Steering wheel-integrated ECG sensors, seat-embedded pulse monitors utilizing radio wave sensors, and dashboard-mounted cameras enable non-intrusive continuous vital sign tracking without requiring wearable devices addressing consumer adoption concerns regarding additional equipment requirements. Hyundai Smart Cabin, unveiled in June 2022, incorporates four sensors that track heart rate, posture, and brainwaves via an ear-set sensor, an ECG steering wheel sensor, a 3D position camera, and HVAC cabin condition monitoring. This demonstrates the automotive industry's capability to deliver medical-grade monitoring and recommend an autonomous driving mode when elevated stress is detected.

Market Restraints

Privacy Concerns and Data Security Challenges in Health Information Management

Automotive health monitoring systems that collect sensitive biometric data, including heart rate, blood pressure, stress levels, and medical conditions, raise substantial privacy concerns about data ownership, data storage security, and potential misuse, constraining consumer adoption, particularly in privacy-conscious markets. Health data sensitivity exceeding typical vehicle telemetry, creating regulatory compliance obligations under HIPAA, GDPR, and emerging health information protection legislation, requires comprehensive data governance frameworks, including encryption, access controls, and consent management, elevating system complexity and operational costs.

Consumer skepticism regarding automotive manufacturers' and technology companies' trustworthiness in handling medical information limits adoption willingness, with surveys indicating 40-55% of consumers expressing reluctance to share health data with automotive brands despite potential safety benefits. Insurance industry interest in accessing driver health data for premium calculation creates consumer concerns regarding discrimination and coverage denial based on monitored health conditions, requiring careful regulatory frameworks balancing safety objectives with individual privacy rights.

High System Cost and Integration Complexity Constraining Mass Market Adoption

Advanced health monitoring systems incorporating medical-grade sensors, AI processing capabilities, and cloud connectivity command substantial price premiums of $1,500-$3,500 per vehicle, constraining adoption to premium segments and limiting mass-market penetration, particularly in price-sensitive emerging markets. Retrofit market complexity requiring electrical system integration, sensor installation across steering wheels and seats, and software integration with existing vehicle architectures creates installation costs exceeding $2,000-$5,000 deterring aftermarket adoption among existing vehicle owners. Sensor calibration requirements and individual physiological variation necessitating personalized baselines create user experience complexity potentially generating false positives undermining system credibility and user trust, with current systems experiencing 5-10% false alarm rates requiring continuous algorithm refinement.

Market Opportunities

Commercial Fleet Management and Driver Wellness Program Integration

The commercial transportation sector, including trucking, logistics, and ride-sharing services, managing hundreds of thousands of drivers, presents a substantial market opportunity for health monitoring, supporting operational safety, regulatory compliance, and driver retention through comprehensive wellness programs. Commercial vehicle operators facing substantial liability exposure from driver health-related accidents are willing to invest in preventive monitoring technology, with fleet health monitoring delivering measurable ROI through accident reduction, insurance premium decreases, and reduced driver turnover.

The heavy commercial vehicle (HCV) segment is growing faster than passenger cars at a 20% CAGR, reflecting commercial operators prioritization of safety technology and regulatory compliance requirements increasingly mandating driver health monitoring for long-haul operations. Integration with fleet management systems, enabling centralized health analytics, driver coaching, and wellness program administration, creates comprehensive driver management platforms supporting operational excellence and regulatory compliance.

Emerging Market Vehicle Electrification and Smart Cockpit Development

Rapidly expanding automotive markets across Asia Pacific, Latin America, and the Middle East, experiencing electric vehicle adoption and smart cockpit technology proliferation, create greenfield opportunities for health monitoring system integration without legacy vehicle retrofit constraints. China and India's electric vehicle markets are projected to reach 20+ million annual EV sales by 2030, creating a substantial addressable market for health monitoring systems integrated as standard features supporting differentiation and premium positioning. Smart cockpit architecture development enabling integrated sensor arrays, AI processing capabilities, and connectivity infrastructure reduces incremental cost for health monitoring integration from $3,500 standalone systems to $800-$1,200 when factory-integrated supporting mass-market viability.

Government initiatives supporting automotive technology development, including India's automotive mission and China's intelligent vehicle standards, create regulatory support and potential subsidies, thereby accelerating the adoption of health monitoring. Market opportunity for emerging market health monitoring is estimated at $600-900 million by 2032 as EV penetration accelerates.

Segmentation Analysis

System Location Analysis

Dashboard-mounted health monitoring systems dominate 63.2% market share due to optimal sensor placement, non-intrusive design, and cost-effective integration that supports large-scale OEM adoption. Forward-facing cameras on the dashboard track facial expressions, eye movement, and head position to detect fatigue and distraction, while infrared technology ensures reliable monitoring in low-light and night conditions. Seamless integration with vehicle displays enables real-time alerts and wellness dashboards, enhancing driver awareness and safety.

Driver’s seat-embedded systems are the fastest-growing segment (22% CAGR), driven by superior biometric accuracy and continuous contact-based monitoring. Advanced smart seats equipped with pulse sensors, posture analysis, and wellness features such as temperature regulation and massage offer enhanced comfort, premium differentiation, and support holistic driver well-being.

Component Analysis

Sensor components hold a dominant 40% share of the automotive active health monitoring systems market, serving as the core data-acquisition layer that enables all downstream analysis and alerts. Biometric sensors such as ECG electrodes in steering wheels, PPG pulse sensors, and seat-embedded temperature sensors provide accurate measurements of vital signs. RGB and infrared cameras enhance driver monitoring through facial analysis, eye-tracking, and head-position detection, while emerging mmWave radar and ultrasonic sensors enable contactless monitoring of heart and respiratory rates.

Software and AI analytics form the fastest-growing segment (28% CAGR), driven by advances in machine learning, sensor-fusion techniques, and cloud-based analytics. These systems integrate multi-sensor data to generate precise driver-state evaluations, reduce false alarms, personalize health baselines, and support predictive wellness insights that extend beyond basic safety functions.

Application Analysis

Pulse rate monitoring holds 48.6% market share as it provides a fundamental and clinically validated indicator of stress, fatigue, and cardiovascular irregularities. Non-invasive heart rate sensing through steering wheels, seats, and ear-set devices enables continuous tracking without disrupting driving, allowing real-time alerts when abnormal patterns or arrhythmias appear. Integration with wearables such as Apple Watch and Fitbit further enhances cardiovascular monitoring beyond the vehicle.

Blood pressure monitoring is the fastest-growing application, expanding at 30% CAGR due to its importance in hypertension management for over 1.3 billion affected adults globally. Advanced algorithms that analyze pulse waveforms enable continuous, cuffless measurement, improving convenience and adoption. Connectivity with healthcare platforms supports remote monitoring, medication optimization, and preventive care value.

End-Use Analysis

Passenger cars account for 64.3% of the market share, supported by high production volumes, rising consumer focus on safety, and strong adoption of advanced health-monitoring technologies in premium vehicles. Luxury brands such as Mercedes-Benz, BMW, Volvo, and Tesla are pioneering features like Energizing Comfort Control, Healthcare Cockpit, and integrated biometric systems, setting benchmarks that are gradually expanding into the mass-market segment.

Growing consumer willingness to pay $1,500–$3,500 for comprehensive health and wellness packages underscores the commercial viability of these systems. Additionally, the progression toward autonomous driving increases the need for continuous driver state monitoring to ensure takeover readiness, creating sustained demand irrespective of voluntary consumer adoption.

Regional Market Insights

North America

North America generates approximately US$272 million market value in 2025 representing 35% global market share growing at 16.5% CAGR through 2032, driven by established automotive technology leadership, strong regulatory framework supporting safety innovation, and consumer receptiveness to premium vehicle technology. The United States dominates regional market with 78% North American share through automotive OEM leadership including Ford, General Motors, and Tesla deploying health monitoring systems, established tier-1 supplier base including Bosch and Continental developing integrated solutions, and Silicon Valley technology innovation supporting AI and sensor advancement.

Ford Driver Alert System utilizing facial recognition and steering feedback detecting drowsiness demonstrates OEM commitment to health monitoring deployment across mainstream vehicle segments. Regulatory environment through NHTSA safety standards and emerging federal requirements for advanced driver monitoring create supportive policy framework accelerating adoption.

Europe

Europe represents approximately US$225 million market in 2025 capturing 25% global market share growing at 17.2% CAGR through 2032, characterized by premium automotive leadership, stringent safety regulations, and privacy-conscious regulatory framework requiring careful data governance. Germany leads European market with 32% regional share through automotive manufacturing excellence including Mercedes-Benz Energizing Comfort Control monitoring stress and recommending relaxation programs, BMW wellness integration, and Volkswagen Group technology development.

Euro NCAP safety rating requirements increasingly incorporating driver monitoring mandates create regulatory drivers supporting widespread adoption across European vehicle production regardless of market segment. United Kingdom contributing 14-18% European share maintains automotive technology development through tier suppliers, while France and Italy demonstrate steady growth through Renault-Nissan-Mitsubishi alliance and Stellantis technology deployment.

Asia Pacific

Asia Pacific represents fastest-growing region at approximately 21.5% CAGR through 2032, with estimated market value reaching US$890 million by 2032 comprising 30% global market share by 2032, driven by automotive manufacturing leadership, smart cockpit technology proliferation, and electric vehicle adoption acceleration. China dominates Asia Pacific with 36% regional share through automotive production leadership, government smart vehicle initiatives supporting connected car development, and domestic technology companies including Huawei and Baidu advancing AI and sensor technologies supporting health monitoring implementation.

Japan representing 18% regional share maintains technology leadership through automotive electronics expertise, Toyota and Honda health monitoring development, and medical device integration supporting automotive-healthcare convergence. India emerging as high-growth market at 26% CAGR through expanding automotive production, consumer safety awareness, and government technology adoption initiatives supporting smart vehicle proliferation.

Automotive Active Health Monitoring Systems Market Competitive Landscape

The automotive active health monitoring systems market exhibits moderate-to-high fragmentation with leading players commanding approximately 35% combined market share, while automotive tier-1 suppliers and specialized health technology companies capture growing segments through integrated solutions and application expertise.

Robert Bosch GmbH emerges as market leader with estimated 12% market share through comprehensive automotive sensor portfolio, interior sensing solutions detecting driver distraction and drowsiness, and established OEM relationships across global automotive industry.

Key Industry Developments

- In December 2024, Roadzen Inc. partnered with Bosch, to implement Bosch's Mobility Solutions segment into Roadzen's drivebuddy AI ADAS platform. The purpose of this integration is to improve driver monitoring and assistance capabilities to ensure better road safety.

- In December 2024, DENSO Corporation and Onsemi extended their partnership with the vision of developing technologies focused on self-driving and ADAS. For more than ten years, Onsemi has partnered with DENSO in supplying intelligent automotive sensors that enhance ADAS and self-driving performance. Such semiconductors are key in making vehicles smarter and more connected, which helps lessen the number of traffic casualties.

Companies Covered in Automotive Active Health Monitoring Systems Market

- Bosch

- Affectiva

- VitalConnect

- Smart Eye AB

- Continental AG

- Faurecia

- Jabil Inc.

- OxStren

- Tata Elxsi

- Vayyar Imaging

- Others Key Players

Frequently Asked Questions

The Automotive Active Health Monitoring Systems market is estimated to be valued at US$ 807.0 Mn in 2025.

The key demand driver for the Automotive Active Health Monitoring Systems market is the growing focus on driver and passenger safety through real-time health assessment.

In 2025, the North America region will dominate the market with an exceeding 35% revenue share in the global Automotive Active Health Monitoring Systems market.

Among the Product Type, Pulse Rate holds the highest preference, capturing beyond 48.6% of the market revenue share in 2025, surpassing other Application type.

The key players in Automotive Active Health Monitoring Systems are Bosch, Affectiva, VitalConnect and Smart Eye AB.