- Medical Devices

- Automated Endoscope Reprocessor Market

Automated Endoscope Reprocessor Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Automated Endoscope Reprocessor Market by Product (Single Basin Automated Endoscopic Reprocessors, Dual Basin Automated Endoscopic Reprocessors), Modality (Stand-alone Automated Endoscopic Reprocessors, Table/Bench Top Automated Endoscopic Reprocessors), End User and Regional Analysis from 2025 to 2032

Automated Endoscope Reprocessor Market Share and Trends Analysis

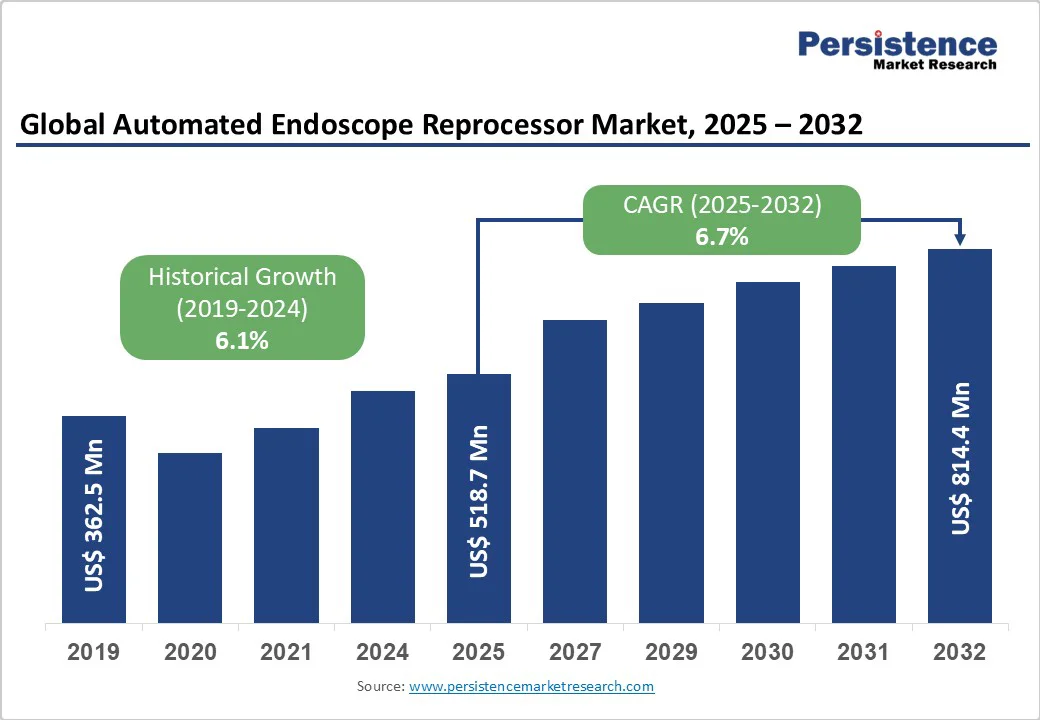

The global automated endoscope reprocessor market size is likely to be valued at US$518.7 million in 2025 and is projected to reach US$814.4 million by 2032, growing at a CAGR of 6.7% between 2025 and 2032.

Automated endoscope reprocessors (AERs) are essential for ensuring patient and staff safety by providing consistent, high-level disinfection or sterilization of complex, reusable endoscopes between procedures.

These systems use liquid chemical sterilization (LCS) or high-level disinfection (HLD) to eliminate microorganisms, including spores such as C. difficile, thereby preventing cross-contamination.

Key Industry Highlights:

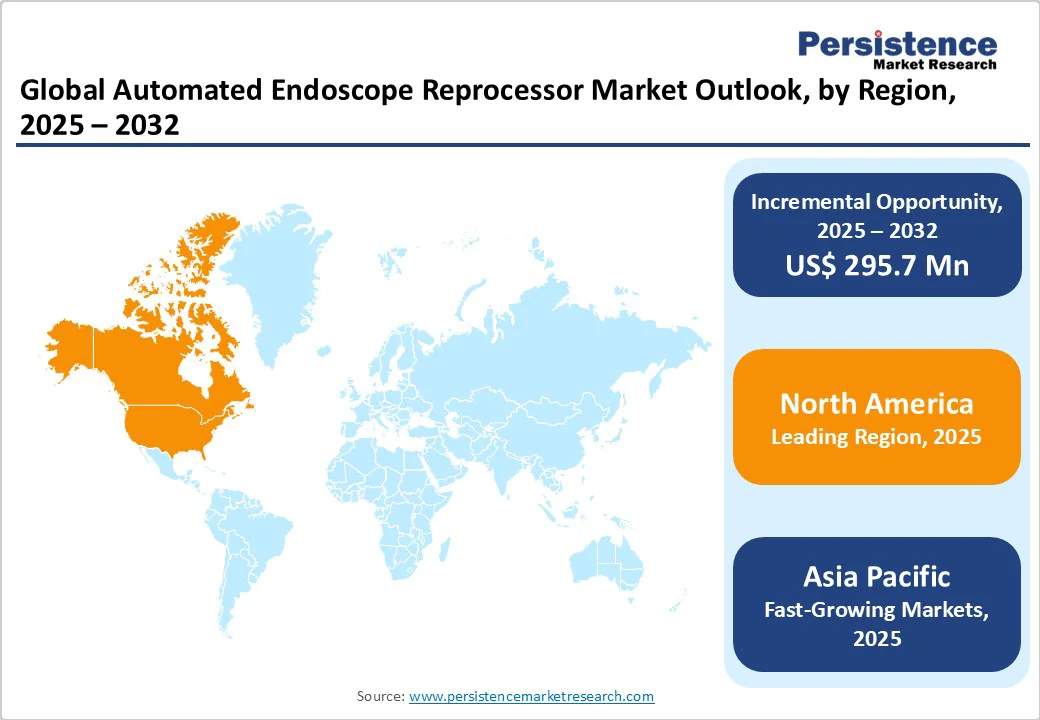

- Leading Region: North America is poised to dominate, driven by strong regulatory compliance frameworks, high procedural volumes, and consistent technology upgrades across healthcare facilities.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market, driven by expanding hospital infrastructure, rising endoscopy volumes, and increasing investments in infection-prevention technologies.

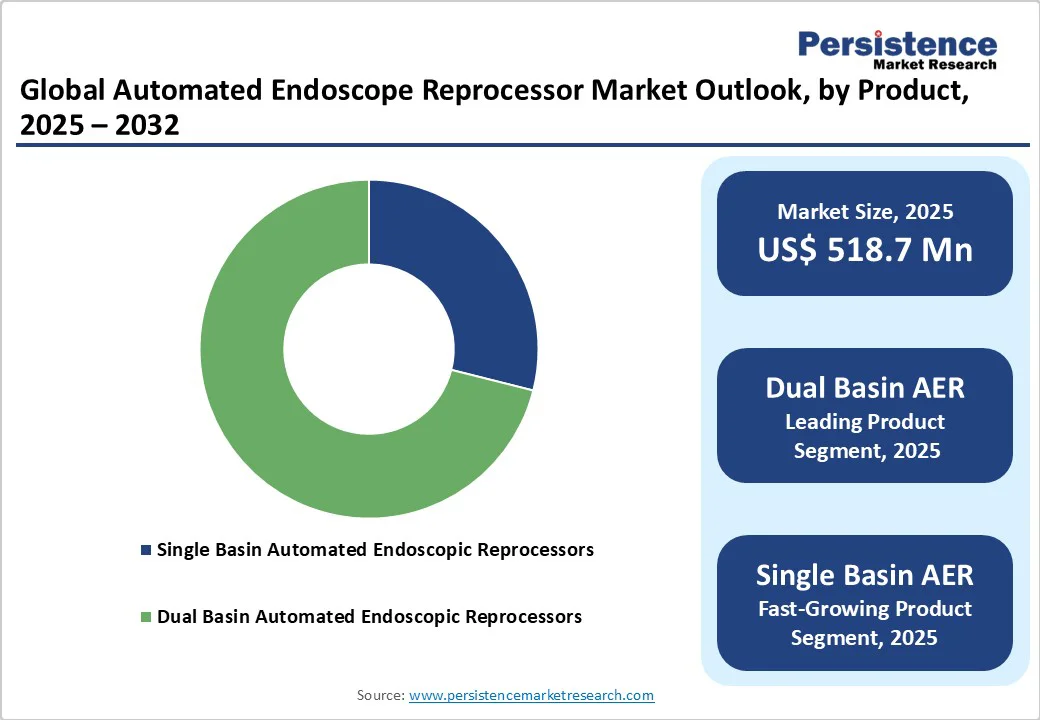

- Leading Product Segment: Dual Basin AERs hold the dominant share (75.8% in 2025), owing to their ability to independently monitor each endoscope channel independently, ensuring superior disinfection and operational efficiency.

- Leading Modality: Standalone AERs lead the market due to their ease of installation, compact design, and suitability for high-throughput healthcare environments with growing patient volumes.

- Increasing adoption of digital traceability systems and automated compliance reporting is expected to redefine infection prevention and quality assurance in endoscope reprocessing.

- Development of eco-efficient AERs with reduced chemical and water consumption to align with sustainability goals.

- Rising incidence of hospital-acquired infections (HAIs) and global emphasis on infection control are accelerating AER adoption.

| Key Insights | Details |

|---|---|

| Global Automated Endoscope Reprocessor Market Size (2025E) | US$518.7 Mn |

| Market Value Forecast (2032F) | US$814.4 Mn |

| Projected Growth (CAGR 2025 to 2032) | 6.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.1% |

Market Dynamics

Driver - Rising Procedure Volume and Regulatory Pressure Driving Automated Endoscope Reprocessor Adoption

The growing complexity and volume of endoscopic procedures are major drivers of the automated endoscope reprocessor (AER) market. Over 250 million endoscopies are performed globally each year, making thorough cleaning, high-level disinfection, and drying critical to patient safety. Flexible endoscopes, with multiple lumens and narrow channels, are difficult to reprocess manually, which is time-consuming, labor-intensive, and prone to variability.

A study across Russia, China, and India found that manual endoscope turnaround times often exceeded procedure durations, while switching to AERs increased efficiency — e.g., a Russian facility added 3.9 procedures per day. Manual handling also contributes to 18% of endoscope damage, which AERs reduce by 34%, lowering repair and replacement costs. In addition to cost benefits, regulatory pressure further reinforces AER adoption.

A 2019 study revealed that over 65% of institutions were noncompliant with reprocessing guidelines, prompting the FDA to recommend stronger, standardized reprocessing methods or the use of disposable endoscopes.

In March 2022, AAMI released the updated ANSI/AAMI ST91:2021 standard, establishing comprehensive requirements for the processing of flexible and semi-rigid endoscopes. By automating cleaning, disinfection, drying, and documentation, AERs ensure compliance, enhance staff accountability, reduce infection risk, and improve patient safety-factors that collectively drive robust market growth.

Restraints - High Costs, Complex Protocols, and Compliance Challenges Restrain Automated Endoscope Reprocessor Adoption

Automated endoscope reprocessors (AERs), while critical for patient safety, face adoption restraints due to operational, financial, and procedural challenges. Effective AER use depends heavily on well-trained staff, proper pre-cleaning, correct detergent and disinfectant selection, and routine system maintenance.

Improper pre-cleaning, misconnection of endoscope channels, or failure to detect damaged scopes can compromise disinfection, despite automation. Small cracks, wear, or distal-end defects in duodenoscopes often harbor debris and pathogens, including multidrug-resistant organisms, making outbreaks possible even with standard protocols.

The FDA has reported evidence of pathogenic microorganisms, including Salmonella spp., K. pneumoniae, P. aeruginosa, and multidrug-resistant Enterobacteriaceae, surviving even multistep reprocessing, highlighting the need for standardized, automated methods. A study found that nearly 24% of bacterial cultures from endoscope channels exceeded 100,000 colonies post-disinfection, underscoring infection risks.

Regulatory compliance also adds significant complexity to AER adoption. The ANSI/AAMI ST91:2021 standard (March 2022) updated flexible and semi-rigid endoscope processing requirements, and a study comparing it with ST91:2015 estimated an increase of ~24 minutes and $52-68 per procedure, excluding capital costs.

In practice, additional steps, staff training, documentation, and resource constraints raise costs to $216 per procedure. Moreover, between 2019 and 2021, MAUDE (Manufacturer and User Facility Device Experience) reports for reusable endoscopes rose by 125%, while infection-related readmission and complication rates reached 7.7% and 2.8%, respectively. These procedural, operational, and financial challenges collectively restrain AER adoption, despite its critical role in patient safety.

Opportunity - Innovation, Automation, and AI Integration Create Growth Opportunities in the Global Market

High-income economies, including the U.K. and U.S., are creating a favorable environment for innovative AER technologies, driven by a growing focus on patient safety and the prevention of cross-contamination. Advances in AER design, such as automated pass-through reprocessing, are transforming traditional cleaning workflows, reducing reliance on manual soaking and minimizing infection risks, as highlighted by the World Gastroenterology Organization.

Emerging trends in the field present significant opportunities for market growth. These include integrating artificial intelligence for process optimization and early fault detection, enhancing connectivity with hospital information systems, implementing advanced documentation for real-time compliance monitoring, and developing single-use disposable components to reduce infection risks further.

Sustainability and operational efficiency are also gaining attention, with next-generation AERs designed to lower chemical and water consumption while incorporating comprehensive tracking and verification features to meet stringent regulatory requirements.

A notable example is the AquaTYPHOON™ automated pre-cleaning device by PENTAX Medical (CE-marked in March 2023), which reduces channel pre-cleaning time to 2-7 minutes, automates validation, ensures full protocol compliance, and offers traceability with network connectivity. By lowering staff workload, enhancing safety, and improving productivity, such innovations are poised to drive the adoption and expansion of the AER market globally.

Category-wise Analysis

By Product: Dual Basin Leads Due to Higher Efficiency, Safety, and Channel Monitoring Accuracy

Dual-basin automated endoscope reprocessors are projected to maintain a 75.8% market share in 2025, driven by their superior design and operational safety. These systems allow simultaneous or sequential reprocessing of multiple endoscopes, reducing turnaround time and improving workflow efficiency in high-volume healthcare settings.

Their ability to individually monitor each endoscope channel for blockages ensures complete high-level disinfection and minimizes infection risks. Furthermore, integrating automated leak testing, traceability features, and chemical monitoring systems enhances compliance with stringent infection-control standards, making dual-basin AERs the preferred choice for hospitals and advanced endoscopy centers worldwide.

By Modality: Standalone AERs Lead Owing to Portability, Flexibility, and Ease of Integration

Standalone automated endoscope reprocessors are expected to remain the dominant modality segment in 2025, accounting for nearly one-third of the global market share. Their compact and mobile design makes them ideal for smaller hospitals, ambulatory surgical centers, and facilities with space constraints. These systems offer plug-and-play operation, simplified installation, and reduced infrastructure requirements compared to plumbed systems, leading to wider adoption.

The surge in infectious disease prevalence and heightened demand for cost-effective, user-friendly disinfection solutions further support their growth. With rising preference for decentralized reprocessing setups and flexible workflow integration, standalone AERs continue to play a crucial role in expanding safe endoscopy access.

Regional Insights

North America Automated Endoscope Reprocessor Market Trends

The North American market continues to grow steadily. It is projected to hold around 37.1% of the global market share by 2025, supported by a mature healthcare ecosystem, stringent infection-control regulations, and rising procedural volumes.

The U.S. automated endoscope reprocessor market, being one of the most prominent and competitive, benefits from long production runs and advanced manufacturing efficiency, which helps reduce per-unit costs. The FDA’s continued emphasis on strict adherence to reprocessing protocols, device maintenance, and adverse event reporting serves as a key regulatory driver shaping AER innovation and compliance frameworks.

Every year, approximately 20 million gastrointestinal (GI) endoscopic procedures are performed in the U.S. Although reported infection transmission is rare (1 in 1.8 million procedures), underreporting and asymptomatic cases suggest the actual rate to be higher, underscoring the importance of standardized, automated reprocessing.

In February 2025, Germitec raised $30 million to accelerate its U.S. expansion and advance UV-C high-level disinfection (HLD) technologies, reflecting strong investor confidence in next-generation AER systems. Together, these advancements and regulatory reinforcements continue to position North America as a global leader in endoscope reprocessing innovation and patient safety.

Europe Automated Endoscope Reprocessor Market Trends

Europe remains one of the most significant regions in the global market, projected to capture around 29.4% of the worldwide market share by 2025. The region’s mature healthcare systems, strong regulatory oversight, and rising focus on infection prevention are driving consistent adoption of AER.

Germany, in particular, stands out due to its universal healthcare coverage, advanced hospital infrastructure, and well-trained workforce-factors that encourage large-scale implementation of automated disinfection technologies to ensure patient safety and compliance with EU hygiene directives.

In March 2025, Wassenburg Medical announced major investments in the UK, expanding its Sheffield facility from 8,000 sq ft to 10,500 sq ft to meet the rising demand for its decontamination solutions. The company’s growth across the UK and Europe reflects increasing institutional prioritization of full-cycle reprocessing, from pre-cleaning to drying and traceable documentation.

Furthermore, the European Union’s Medical Device Regulation (MDR) continues to push manufacturers toward higher safety standards and more transparent validation processes. As healthcare facilities modernize and infection-control requirements intensify, European markets are expected to accelerate adoption of next-generation AER systems featuring automation, traceability, and integrated quality assurance, solidifying the region’s position as a global leader in reprocessing innovation.

Asia Pacific Automated Endoscope Reprocessor Market Trends

Asia Pacific is experiencing strong momentum, with a CAGR of 9.5% projected for the forecast period. This growth is driven by rapid healthcare modernization, rising awareness of infection control, and increased adoption of endoscopic procedures across major economies, including China, Japan, South Korea, and India.

China, in particular, has emerged as a lucrative market, supported by robust economic expansion and large-scale hospital infrastructure upgrades. The country’s focus on improving diagnostic capacity has led to a sharp rise in endoscopic procedures.

According to a recent national study, the average annual endoscopy volume in China increased from 12,445 to 16,206 in tertiary hospitals and from 2,938 to 4,255 in secondary hospitals. The establishment of the National Digestive Endoscopy Improvement System (NDEIS) further standardized practices through nationwide surveys and the implementation of quality indicators aligned with international protocols.

Additionally, the Japanese market continues to prioritize automation and precision technologies, while India and Southeast Asian nations are investing in affordable, high-throughput reprocessing systems to address infection risks and staffing challenges.

The region’s growing hospital base, improving reimbursement environment, and local manufacturing initiatives-such as China’s medical device localization drive-are expected to strengthen long-term AER adoption. Together, these developments position Asia Pacific as the fastest-growing regional market for automated endoscope reprocessors worldwide.

Competitive Landscape

With several manufacturers of automated endoscope reprocessors that have patented products, the overall market is highly consolidated. To meet consumer demand and expand their customer base, these companies are resorting to mergers and acquisitions, approvals and certifications and new product launches.

Key Industry Developments:

- In March 2025, Nanosonics received FDA De Novo clearance for its CORIS automated endoscope cleaning system, offering advanced internal channel cleaning, reducing infection risk, initially approved for colonoscopes with broader expansion planned.

- In November 2023, Steelco Group and Belimed formed a joint venture to combine expertise and deliver innovative, high-quality cleaning, disinfection, and sterilization solutions globally.

- In June 2023, Olympus launched its ETD endoscope washer-disinfector n two versions, ETD Basic and ETD Premium, introducing an innovative solution for automated cleaning, disinfection, and workflow efficiency in endoscope reprocessing.

Companies Covered in Automated Endoscope Reprocessor Market

- Steelco S.p.A.

- ASP India Private Ltd.

- STERIS

- Getinge

- Olympus America

- ECOLAB

- MMM Group

- SBSystem

- Belimed

- Cantel Medical Group of Companies

- Device Technologies Asia (Wassenburg Medical)

- HOYA Group (PENTAX Medical)

- OLIVE HEALTH CARE

- ARC Group of Companies Inc.

- Censis

- Hubei CFULL Medical Technology Co., Ltd.

- Medonica Co. LTD

- Detrox

- Huons Meditech

- MİXTA MEDİKAL

- SUN TECHNOLOGY JSC. (SUNTECH)

- JIAJING MEDICAL

- Nanosonics

Frequently Asked Questions

The global automated endoscope reprocessor market is projected to be valued at US$ 518.7 Mn in 2025.

Growing endoscopy volumes, rising infection control awareness, and stricter reprocessing regulations drive the global AER market.

The global automated endoscope reprocessor market is poised to witness a CAGR of 6.7% between 2025 and 2032.

Integration of AI, IoT, and eco-efficient designs offers major growth opportunities in next-generation AER systems.

Major players in the global automated endoscope reprocessor market include are STERIS, Getinge, Olympus America, ECOLAB and others.