- Transportation & Logistics

- Automated Fare Collection System Market

Automated Fare Collection System Market Size, Share, and Growth Forecast 2026 – 2033

Automated Fare Collection System Market by Component Type (Hardware and Software), by Application (Railways & Transportation, Parking, Entertainment and Others (Government, Retail), by Media (Smart Cards, Mobile Ticketing and Wearables) and by Technology (Smart Card, Magnetic Stripe, Near-field communication (NFC) and Optical Character Recognition (OCR), and Regional Analysis for 2026-2033

Automated Fare Collection System Market Share and Trends Analysis

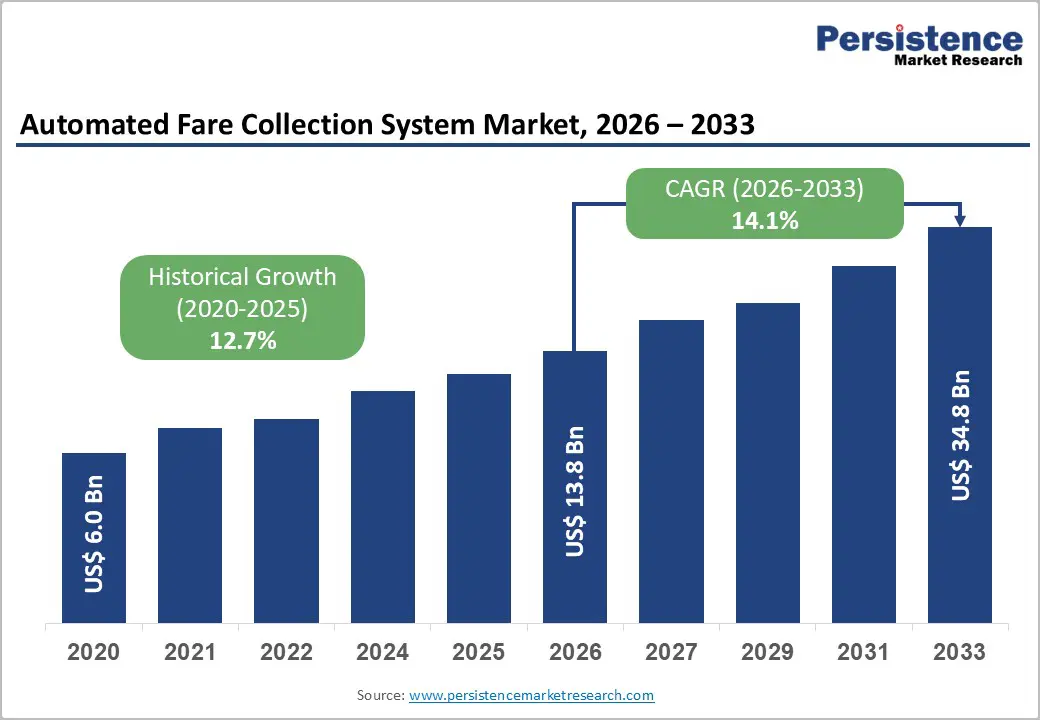

The global Automated Fare Collection System Market size is likely to be valued at US$ 13.8 Billion in 2026 and is projected to reach US$ 34.8 Billion by 2033, growing at a CAGR of 14.1% between 2026 and 2033. The automated fare collection market is experiencing substantial expansion driven primarily by accelerating urbanization, increasing commuter volumes, widespread adoption of contactless payment technologies addressing post-pandemic health and safety concerns, and government investments in smart city initiatives and public transportation modernization.

Key Industry Highlights:

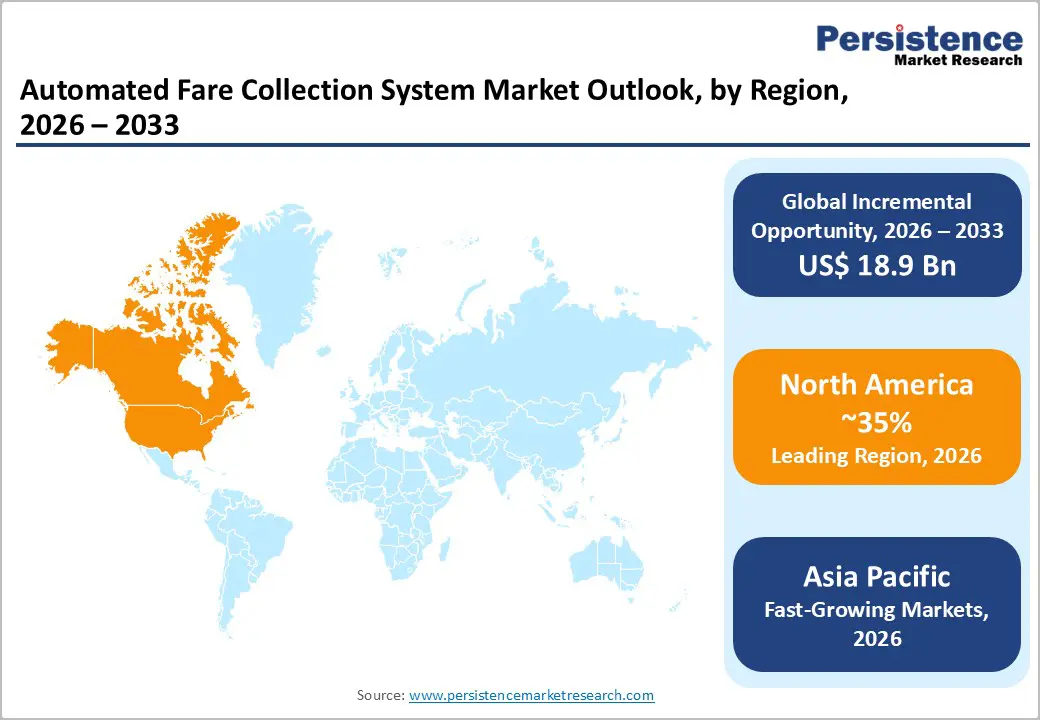

- Leading Region: North America maintains a dominant AFC market position, commanding approximately 35% global market share through early technology adoption, substantial public transportation infrastructure investment, and a high concentration of AFC solution vendors, including Cubic Transportation Systems.

- Fastest Growing Region: Asia Pacific represents the fastest-growing AFC market region, expanding at 18.7% CAGR, driven by rapid urbanization in China, Japan, India, and Southeast Asia, government smart city initiatives, and unprecedented public transportation infrastructure development.

- Dominant Segment: Software solutions command 56% component market share, reflecting transportation authorities' recognition that software capabilities determine AFC system differentiation, operational efficiency, analytics capabilities, and future scalability.

- Fastest Growing Segment: Mobile Ticketing represents the fastest-growing media segment, expanding at 18.5% CAGR, driven by smartphone proliferation reaching 80% globally and transit agencies' recognition that mobile payment integration is strategically essential for modern transit systems.

- Key Market Opportunity: Emerging market AFC expansion in Asia, Latin America, and Africa represents the highest-potential opportunity, with government smart city initiatives, urbanization growth, and public-private partnership financing mechanisms catalyzing substantial AFC investment in capital-constrained developing nations.

| Key Insights | Details |

|---|---|

| Automated Fare Collection System Size (2026E) | US$ 13.8 Bn |

| Market Value Forecast (2033F) | US$ 34.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.1% |

| Historical Market Growth (CAGR 2020 to 2024) | 12.7% |

Market Dynamics

Drivers - Exponential Growth in Urbanization and Rising Public Transportation Demand

Global urbanization continues to accelerate with urban populations projected to reach 68% of the world's population by 2050, creating unprecedented demands on public transportation infrastructure and necessitating efficient automated ticketing solutions. Major metropolitan areas worldwide are experiencing rapid transit ridership growth, with cities including New York, London, Seoul, and Shanghai demonstrating substantial AFC system adoption driving market expansion.

Rising commuter populations in developing nations, particularly in India, China, and Southeast Asia, are compelling transportation authorities to modernize legacy fare collection systems with automated fare collection solutions enabling high-volume, efficient passenger processing. Public transit agencies face mounting pressure to reduce operational costs while improving service quality, and AFC systems deliver compelling economic benefits through reduced manual ticketing expenses, lower cash handling costs, and accelerated transaction processing.

Contactless Payment Technology Adoption and Post-Pandemic Health Imperatives

Contactless payment adoption has accelerated dramatically post-pandemic, with consumers and transit authorities recognizing substantial hygiene and convenience benefits compared to cash transactions. UK contactless payment adoption reached 94.6% of eligible transactions in 2024, representing unprecedented consumer acceptance of contactless technologies and demonstrating market readiness for contactless AFC systems. NFC technology deployments in major transit networks including New York's OMNY system and London's evolving contactless infrastructure have demonstrated operational viability and passenger satisfaction, encouraging additional adoption.

Mobile ticketing applications have gained substantial traction, with commuters preferring smartphone-based payment methods offering convenience and real-time balance management. Travel-related contactless payments demonstrated 6.3% growth overall, with public transport and AFC systems driving increased transaction volumes. The shift away from cash transactions, accelerated by pandemic-related health concerns and consumer preference for touchless interactions, has created existential imperatives for AFC system implementation in transit networks worldwide.

Restraints - High Capital Investment Requirements and Implementation Complexity

The prohibitive capital costs associated with AFC system procurement, installation, integration, and staff training represent significant barriers limiting adoption, particularly in developing nations and smaller transit agencies with constrained budgets. Initial AFC system investments require substantial expenditure encompassing ticket vending machines, fare gates, readers, back-office software, and integration with existing transit infrastructure, with comprehensive systems frequently costing millions of dollars depending on system scope and network complexity. Maintenance and ongoing operational costs for AFC systems require specialized technical expertise and spare parts inventory, consuming significant operational budgets over system lifespans.

Data Security and Privacy Compliance Challenges

AFC systems handling substantial passenger personal information and payment data face mounting cybersecurity threats and regulatory compliance requirements creating operational challenges and increasing implementation costs. Increasingly sophisticated cyberattacks targeting transportation infrastructure necessitate continuous investment in security upgrades, encryption technologies, and compliance monitoring consuming significant operational resources. Regulatory frameworks including GDPR, PCI-DSS, and emerging data protection regulations impose stringent requirements for passenger data protection, breach notification, and audit capabilities that complicate AFC system design and operations. Payment card industry standards require continuous security certification, software updates, and infrastructure hardening that strains IT resources of many transit agencies.

Opportunity - Mobile Ticketing and Account-Based System Expansion

Mobile ticketing and account-based fare collection systems represent rapidly expanding market opportunities as smartphone penetration reaches unprecedented levels globally and transit agencies increasingly recognize mobile channels' strategic importance. Smartphone-based AFC applications enable convenient pre-purchase, balance management, and contactless validation, with platforms including Masabi's SaaS ticketing solutions and Cubic's Umo platform gaining substantial adoption across multiple transit agencies.

Account-based systems enabling post-payment fare collection are being deployed in leading transit networks including London, Washington DC, and emerging implementations in Asia, demonstrating market viability of dynamic pricing and personalized fare offerings. Regional fare harmonization initiatives including NEORide procurement in North America demonstrate transit agencies' recognition of mobile ticketing solutions' operational efficiency and revenue optimization potential. Integration of mobile ticketing with popular payment platforms including Apple Pay, Google Pay, and contactless debit cards dramatically expands accessibility, particularly among younger demographics and tech-savvy commuters.

Emerging Markets and Smart City Infrastructure Development

Rapidly developing nations in Asia, Latin America, and Africa are experiencing transformational investment in public transportation infrastructure modernization, creating substantial AFC system procurement opportunities as transit agencies transition from cash-based systems to modern digital infrastructure. India's government initiatives including Viability Gap Funding schemes covering up to 40% of AFC project costs are catalyzing significant private investment in transit modernization, with systems including NCRTC's QR code-based and smart card implementations demonstrating technology deployment at scale. China's extensive metro system expansion and urban transit growth are driving substantial AFC system procurement, with major cities implementing NFC and QR code-based systems addressing rapid ridership growth. Southeast Asian nations including Singapore, Bangkok, and Jakarta are modernizing transportation infrastructure incorporating state-of-the-art AFC technologies.

Category-wise Analysis

Component Insights

Software solutions command the dominant market position with approximately 56% market share, reflecting transportation authorities' recognition that software capabilities determine AFC system competitive differentiation, operational efficiency, and future scalability. Modern AFC software platforms provide real-time data analytics, dynamic pricing optimization, revenue management, and passenger behavior analysis capabilities that justify substantial software investment.

Back-office software managing fare calculation, revenue allocation, equipment management, and regulatory reporting represent mission-critical functionality essential for AFC operations. Integration capabilities with existing transit management systems, financial systems, and business intelligence platforms require sophisticated software architectures accommodating diverse technical environments. Continuous software updates addressing emerging cybersecurity threats, regulatory compliance requirements, and new functionality demands create recurring revenue opportunities for AFC vendors through subscription and maintenance models.

Technology Insights

Smart Card technology maintains market dominance with approximately 48% market share, reflecting these cards' proven reliability, consumer familiarity, and proven interoperability across diverse transit networks. Reusable smart cards with embedded NFC or RFID technology provide durability, consumer acceptance, and technical reliability that has established smart cards as proven foundation technology for AFC systems globally. Major transit networks including London's Oyster card, Seoul's T-Money Card, and Tokyo's Suica system have demonstrated smart card technology's operational viability across diverse geographic markets.

Near-Field Communication (NFC) technology represents the fastest-growing segment at CAGR of 16.2%, driven by smartphone penetration reaching 80% globally and consumer preference for integrated payment solutions. NFC enables tap-on/tap-off fare validation using smartphones, smartwatches, contactless bank cards, and wearable devices, dramatically expanding payment method accessibility.

Application Insights

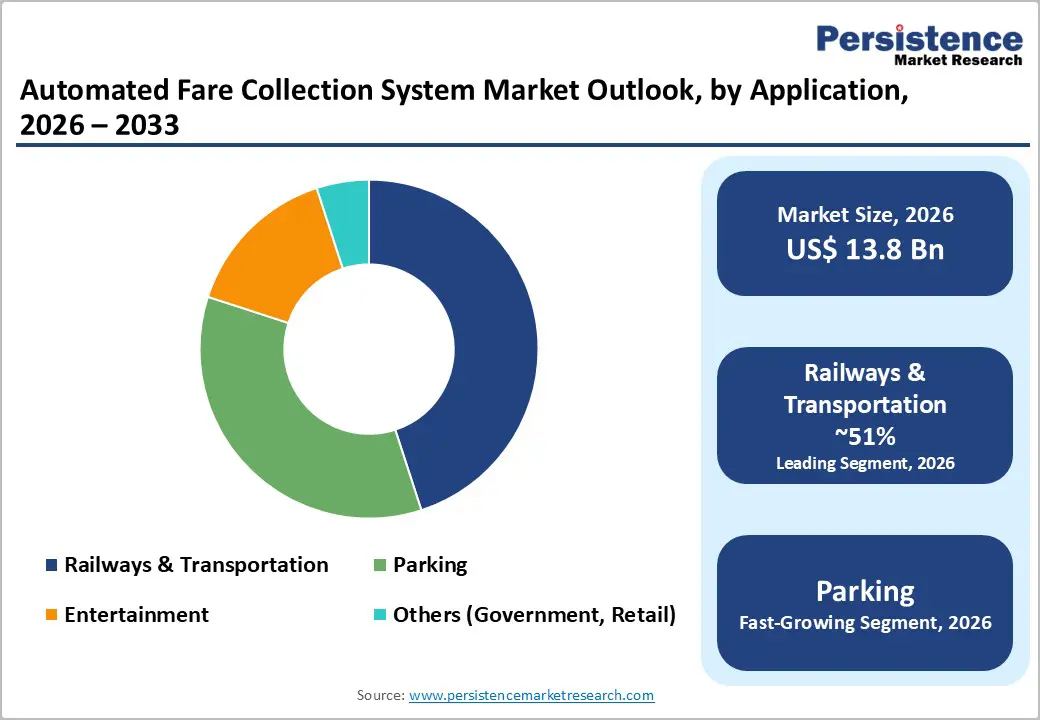

Railways and Transportation represent the dominant application segment commanding approximately 51% market share, reflecting these transportation modes' handling of the highest passenger volumes and greatest investment capacity among public transportation categories. Major rail networks including metro systems, commuter rail, and light rail transit have historically pioneered AFC technology adoption, with systems in New York, London, Paris, and Tokyo demonstrating operational viability and passenger acceptance. Bus rapid transit systems increasingly adopt AFC platforms designed for rail applications, with agencies recognizing comprehensive ticketing ecosystem benefits.

Parking management systems represent the fastest-growing application segment, expanding at CAGR of 17.8%, as municipalities recognize AFC technology's ability to optimize parking revenue management, reduce enforcement costs, and implement dynamic pricing strategies addressing urban congestion. Parking AFC systems enable cashless transactions, automated enforcement, and real-time availability management while generating valuable traffic pattern data.

Media Insights

Smart Cards maintain market leadership with approximately 52% market share, reflecting their proven reliability and widespread global deployment across transportation networks. Mobile Ticketing represents the fastest-growing segment at CAGR of 18.5%, driven by smartphone proliferation and consumer preference for integrated mobile payment experiences. Wearables including smartwatches and NFC-enabled devices are emerging as innovative payment media, with early implementations in major transit networks demonstrating viability and consumer interest in expanded contactless options.

Regional Insights

North America Automated Fare Collection Market Share and Trends

North America maintains dominant market position commanding approximately 35% of global AFC market share, driven by early technology adoption, substantial public transportation infrastructure, and high concentration of major AFC vendors. The United States represents the largest North American AFC market, with advanced public transportation infrastructure in major metropolitan areas including New York, Washington DC, Chicago, and San Francisco driving substantial AFC investment.

Cubic Transportation Systems, headquartered in San Diego, represents a dominant North American AFC vendor maintaining 400+ global transit deployments. December 2024 contract award to Cubic for Port Authority of New Jersey and New York fare system upgrade exemplifies ongoing substantial AFC investment in major North American transit networks. Masabi's EZfare platform serving NEORide consortium is expanding across multiple Midwestern transit agencies, with 2026 projections adding five to six additional agencies, demonstrating growing acceptance of cloud-based SaaS ticketing solutions.

Europe Automated Fare Collection Market Share and Trends

Europe represents the second-largest AFC market, driven by stringent regulatory frameworks prioritizing transportation electrification and digitalization, combined with early AFC adoption and mature public transportation infrastructure. Germany, United Kingdom, France, and Spain collectively represent substantial European AFC market demand, with nations implementing EU-harmonized standards and regulatory frameworks supporting AFC interoperability.

France's substantial investment in contactless payment infrastructure and Spain's growing AFC deployments demonstrate continuing European expansion. Post-pandemic prioritization of contactless payments addressing hygiene concerns has accelerated AFC adoption across European transit networks, with 35% of pandemic survivors reporting reduced cash usage and corresponding increase in digital payment preference. European regulatory emphasis on data protection, environmental sustainability, and accessibility is shaping AFC system specifications and vendor strategies, creating differentiated market dynamics compared to North American and Asia Pacific regions.

Asia Pacific Automated Fare Collection Market Share and Trends

Asia Pacific is emerging as the fastest-growing regional market, expanding at CAGR of 18.7%, with momentum in China, Japan, India, and Southeast Asian nations driven by rapid urbanization, government smart city initiatives, and unprecedented public transportation expansion. China's extensive metro system expansion and major city transportation modernization is driving substantial AFC procurement, with NFC and QR code-based systems being deployed at unprecedented scale across major cities.

India's government initiatives including Viability Gap Funding schemes supporting AFC implementation have catalyzed significant private investment in public transportation modernization. NCRTC's Delhi-Ghaziabad-Meerut Regional Rapid Transit System implementing QR code-based ticketing and smart card systems demonstrates Indian adoption of modern AFC technologies.

Competitive Landscape

The global AFC market exhibits a moderately consolidated competitive structure, with major vendors including Cubic Transportation Systems, Masabi, Thales Group, Siemens AG, and LECIP Holdings commanding substantial market share through comprehensive product portfolios and global distribution networks. Cubic Transportation Systems, headquartered in San Diego, maintains market leadership through 50 years of transportation technology expertise and 400 global transit deployments.

Masabi's SaaS-based ticketing platform has achieved rapid growth through cloud-native architecture and flexible deployment models addressing requirements of smaller transit agencies and emerging markets. Competitive differentiation increasingly centers on cloud-native architecture, mobile-first design, dynamic pricing capabilities, and integration with open payment ecosystems rather than proprietary hardware solutions.

Key Developments:

- In July 2025, Land Bank of the Philippines launched a pilot automated fare collection system for MRT-3, enabling EMV payments and serving as payment-gateway integrator for nationwide settlements.

- In July 2025, Philippine Department of Transportation completed nationwide open-loop EMV roll-out across rail lines with road-vehicle extension planned.

In May 2025, Ho Chi Minh City’s Bn Thành–Sui Tiên metro introduced an automated fare collection platform offering single-ride and multi-day passes.

Companies Covered in Automated Fare Collection System Market

- Advanced Card Systems Ltd.

- Atos SE

- Cubic Transportation Systems

- GMV

- Indra Sistemas SA

- LECIP Holdings Corporation

- LG Corporation

- Siemens AG

- Thales Group

- Omron Corporation

- Masabi Ltd.

- Others Key Players