- Semiconductor Materials & Components

- Automated Container Terminal Market

Automated Container Terminal Market Size, Share, and Growth Forecast 2026 - 2033

Automated Container Terminal Market by Degree (Semi-Automated Terminals, Fully Automated Terminals), Offering (Equipment, Software, Services), Project Type (Brownfield Projects, Greenfield Projects), End-user (Port Authorities/Government Terminals, Private Terminal Operators, Shipping Line-Owned Terminals, Logistics Companies), and Regional Analysis, 2026 - 2033

Automated Container Terminal Market Size and Trend Analysis

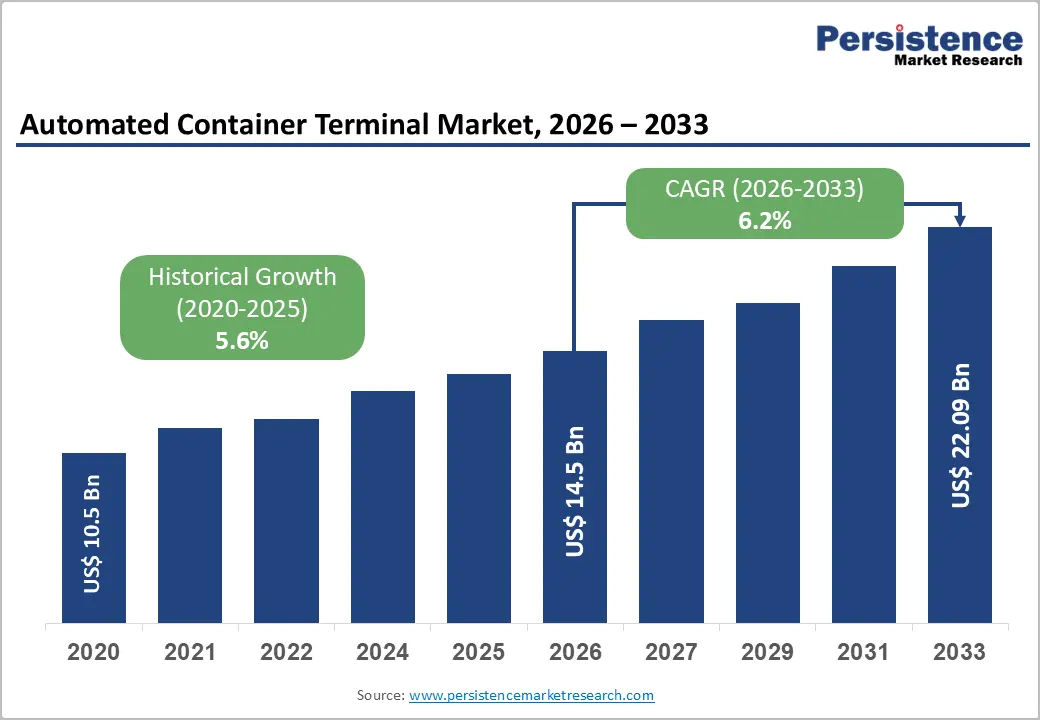

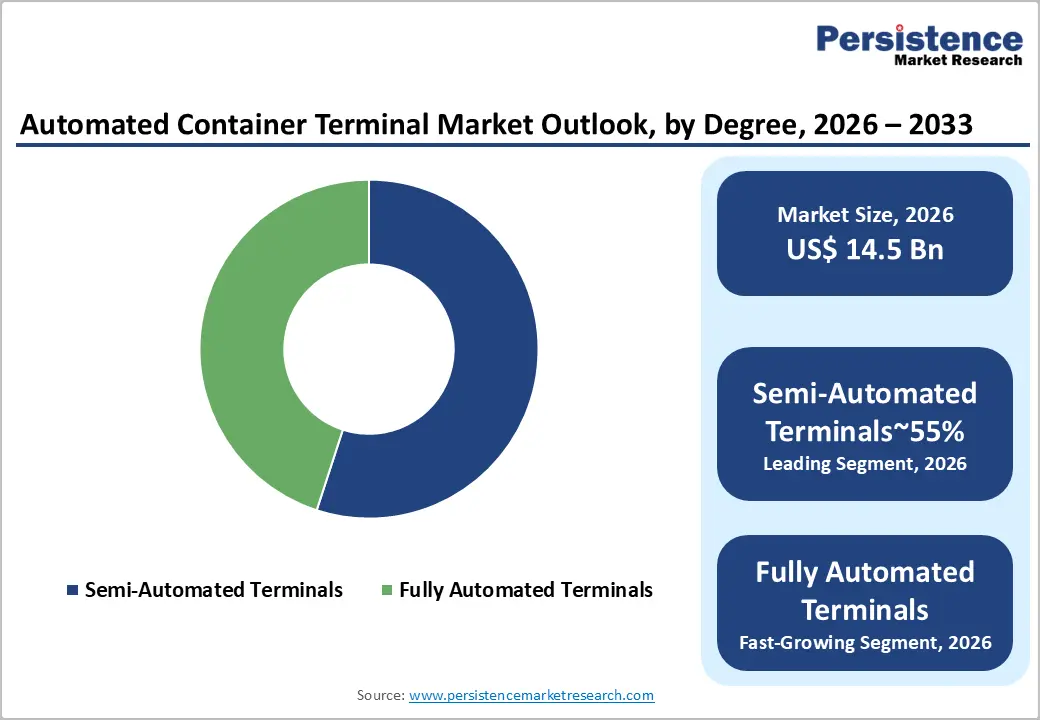

The global automated container terminal market size is expected to be valued at US$ 14.50 billion in 2026 and is projected to reach US$ 22.09 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

The global Automated Container Terminal Market is expanding at a structurally robust pace, driven by rising trade volumes, acute labour cost pressures, and the accelerating deployment of port automation technologies across major maritime economies.

Key Industry Highlights:

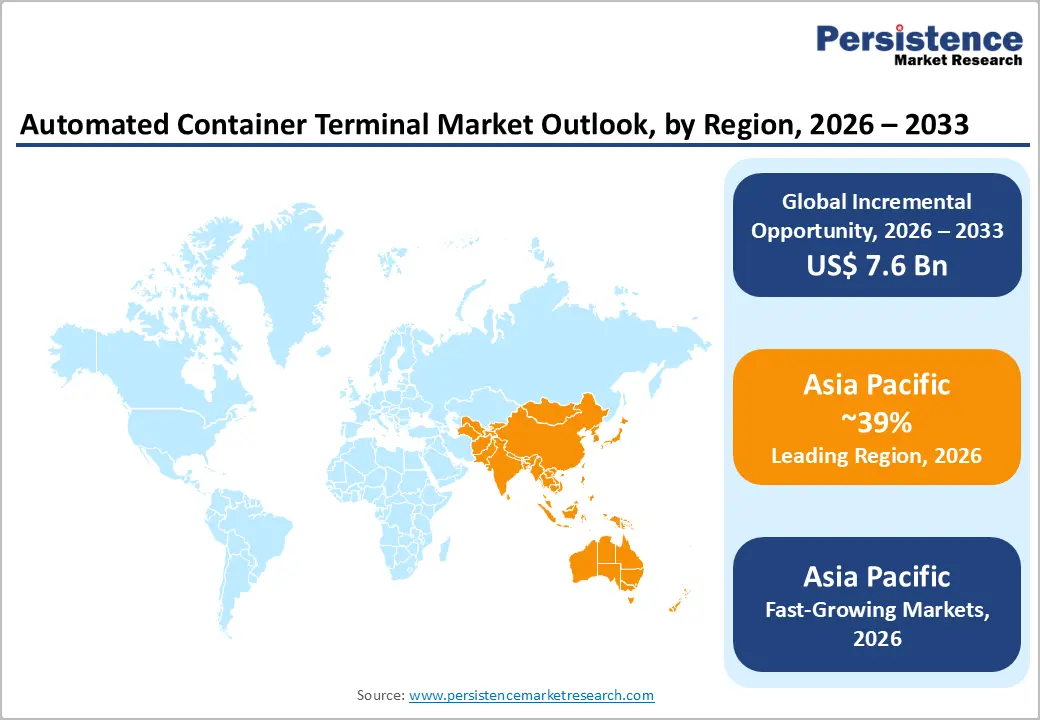

- Leading Region: Asia Pacific leads the Automated Container Terminal Market with a 39.0% share in 2026, underpinned by the world's highest concentration of mega-hub ports, state-directed smart ports investment programmes, and a competitive domestic automation technology manufacturing base centred on China and Japan that structurally advantages regional procurement.

- Fast-Growing Region: Asia Pacific is also the fastest growing regional market at a projected CAGR of 7.9% through 2033, driven by India's Sagarmala-linked terminal modernisation pipeline, China's 14th Five-Year Plan port infrastructure targets, and the broader Southeast Asian greenfield port development wave, collectively representing the most significant incremental revenue pool in the global automated container terminal market forecast period.

- Leading Segment: Semi-automated terminals dominate the degree segmentation with a 55.0% share in 2026, reflecting port operators' demonstrated preference for hybrid automation models that balance capital efficiency with operational risk management, a structural characteristic that is expected to persist throughout the near-to-mid forecast horizon as full automation prerequisites remain demanding.

- Fastest Growing Segment: Fully automated terminals represent the fastest growing degree segment, accelerating as technology costs decline, reference site performance data builds investor confidence, and green port initiatives in Europe and Asia Pacific favour zero-emission fully automated equipment configurations that are structurally easier to implement in purpose-built rather than hybrid operational environments.

Market Dynamics

Drivers - Surging Global Container Trade Volumes and Port Congestion Pressures Accelerating Automation Adoption

Port operators across the world are investing in full-stack automation because manual terminal operations can no longer absorb the throughput demands of next-generation mega-vessels, some carrying over 24,000 TEUs per voyage.

Automated container handling systems, including AGVs, ASCs, and AI-powered optimisation platforms, consistently deliver 15 to 25% improvements in berth utilisation compared with conventional operations. Terminal operators that have deployed fully automated stacking systems at major hub ports report measurable reductions in vessel turnaround time, directly translating to lower demurrage costs and higher asset utilization.

Escalating Labour Costs and Safety Mandates Compelling Operational Technology Upgrades

Rising labour costs and increasingly stringent occupational health and safety regulations are compelling terminal operators to replace human-intensive yard operations with robotics-driven alternatives. Labour accounts for up to 60 to 70% of total operating expenditure at conventional container terminals in developed markets, making automation a financially compelling proposition with payback periods frequently under eight years for large-scale deployments.

Regulatory bodies across the European Union and several Asia Pacific jurisdictions have introduced mandatory safety performance benchmarks that manual operations struggle to meet without significant workforce augmentation. This cost-and-compliance convergence is a durable structural driver that terminal operators, port authorities, and logistics companies cannot defer indefinitely.

Restraints - Exceptionally High Capital Expenditure and Long Investment Payback Periods Constraining Adoption in Emerging Markets

The capital intensity of full-scale automation deployments, where greenfield fully automated terminals require investments over US$ 1 Billion depending on berth count and specification of the equipment. Smaller port authorities and private terminal operators in Latin America, sub-Saharan Africa, and parts of South Asia lack the balance sheet capacity or long-term concession security needed to justify such expenditures.

Multilateral development bank financing can partially offset this barrier, but loan tenors and risk-sharing frameworks often remain misaligned with the commercial realities of emerging market port operators. Until financing instruments better accommodate lower-rated sovereign and private counterparties, capital constraints will continue to slow adoption in high-potential but under-capitalised regions.

Integration Complexity with Legacy Infrastructure and Workforce Transition Challenges Creating Project Delays

Brownfield automation projects, which represent the majority of active deployments in the automated container terminal market, face substantial integration risk when retrofitting modern terminal operating systems, digital twin technology, and IoT-enabled logistics platforms onto decades-old quayside infrastructure and legacy IT architectures.

System interoperability between new automated equipment and inherited cargo management platforms frequently extends project timelines by 12-24 months beyond initial estimates, according to project case studies in authenticated industry databases. Labour union resistance in major European and North American ports adds further friction, as workforce transition agreements and retraining commitments require careful negotiation that can delay or dilute automation rollout scopes. These execution risks elevate perceived project complexity and can deter first-time automation adopters from committing capital.

Opportunities - Expansion of AI-Powered Optimisation and Digital Twin Technology Across Existing Terminal Portfolios

Terminal operators that have already invested in basic automation hardware now have a strong opportunity to enhance performance by adding AI-powered optimisation, digital twin technology, and real-time data analytics to their existing systems. This should be viewed as a software-driven value strategy, allowing operators to unlock additional efficiency without the need for costly new infrastructure. For example, predictive maintenance tools applied to automated stacking cranes and AGV fleets can reduce unexpected equipment downtime by up to 30%, directly improving asset utilisation and return on investment.

AI-enabled yard and fleet management systems can intelligently re-sequence container movements, reducing crane cycles and lowering operational costs, especially in high-volume terminals. Vendors offering flexible, modular software solutions that integrate easily with different hardware systems are best positioned to capture this growing demand as semi-automated terminals continue to expand globally.

Smart Port Development Mandates and Green Port Initiatives Creating Demand in Underpenetrated Emerging Markets

Government-led port development programmes across Southeast Asia, the Middle East, and South Asia are increasingly combining smart port requirements with sustainability goals, creating strong demand for automated terminal solutions in emerging markets. Countries such as India, Saudi Arabia, and Vietnam have announced large-scale port modernisation plans that include automation, IoT-enabled logistics, and low-emission equipment as key requirements. These initiatives are transforming markets that were previously limited by cost constraints.

Vendors and system integrators that establish early projects in these regions gain a significant advantage, as proven local experience reduces risk perception in future tenders. Additionally, concession-backed financing models supported by global institutions are improving access to capital for such projects. Companies that invest in local engineering capabilities, strong after-sales support, and regulatory engagement are better positioned to convert these policy-driven opportunities into long-term contracts and sustainable revenue streams.

Category-wise Analysis

Degree Insights

Semi-automated terminals hold 55.0% of the global automated container terminal market in 2026, valued at US$ 7.97 billion, making them the leading segment in degree-based classification. This dominance is driven by their balanced approach, where operators gain efficiency through automation while maintaining human control over complex operations. Industry data shows that over 70% of current automation projects use hybrid models combining automated yard equipment with manually operated ship-to-shore cranes, highlighting the preference for gradual adoption.

Fully automated terminals are the fast-growing segment, supported by falling sensor costs, improved AGV navigation systems, and successful deployments in countries such as China, the Netherlands, and Singapore. While semi-automated terminals will continue to lead in the near term due to lower investment risk, the gap between the two models is expected to shrink. This trend encourages vendors to develop scalable systems that support a smooth transition toward full automation.

Offering Insights

Equipment accounts for 47.0% of the global market share in 2026, reaching US$ 6.82 billion, making it the largest offering segment. This is because physical infrastructure, such as automated stacking cranes, AGVs, ship-to-shore cranes, and gantry systems, is the foundation of any automation project. Without this hardware, software and services cannot be effectively deployed. Procurement data from major projects in the Asia Pacific and Europe shows that equipment typically represents 45% of total project investment, reinforcing its importance.

Software is the fastest growing segment, as operators increasingly invest in advanced solutions like terminal operating systems, yard management platforms, digital twins, and AI-based optimisation tools. Over time, the dominance of equipment is expected to decline slightly as recurring software and service revenues grow. Vendors must therefore focus on building flexible, integrated platforms to remain competitive and capture long-term value.

Project Type Insights

Brownfield projects represent 68.0% of the global Automated Container Terminal Market in 2026, valued at US$ 9.86 billion, making them the dominant project type. This reflects the fact that most automation opportunities involve upgrading existing terminals rather than building new ones. Major global ports such as Rotterdam, Singapore, Shanghai, Los Angeles, and Hamburg already have established infrastructure, high cargo volumes, and strong financial frameworks, making phased automation more practical than new construction.

Data shows that these large ports account for a significant share of annual automation investments, reinforcing the strength of brownfield projects. On the other hand, greenfield projects are the fast-growing segment, driven by new port developments in the Middle East, South and Southeast Asia, and East Africa. While brownfield projects will continue to dominate in mature markets, greenfield growth in emerging regions is creating new opportunities for automation providers worldwide.

End-user Insights

Port authorities and government-operated terminals account for 49.0% of the global Automated Container Terminal Market in 2026, totaling US$ 7.11 billion, making them the largest end-user group. Their dominance is due to their control over large-scale port infrastructure, high cargo volumes, and access to public funding, which supports long-term investments in automation. Government-backed programmes across the Asia Pacific and Europe have announced over US$ 25 billion in terminal modernisation investments between 2022 and 2024, highlighting the scale of public-sector involvement.

Private terminal operators are the fast-growing segment, driven by rising competition, pressure to improve margins, and the need to attract major shipping alliances. Companies such as PSA International, DP World, and APM Terminals are rapidly expanding automation across their global networks. As private operators grow in influence, vendors should focus on tailored solutions and financing models to effectively capture this expanding market segment.

Regional Insights

North America Automated Container Terminal Market Trends and Insights

North America holds 19.0% of the global automated container terminal market in 2026, valued at US$ 2.75 billion. Growth is driven by infrastructure investment, labour cost pressures, and federal funding like the Infrastructure Investment and Jobs Act. Rising cargo volumes and supply chain resilience priorities are accelerating automation adoption.

- United States Automated Container Terminal Market Size

The United States represents 78% of North America’s market, about US$ 2.15 billion in 2026. Investments at major ports like Los Angeles and Savannah drive growth. Federal funding and private competition support demand, while strong e-commerce import volumes push operators to expand automated handling capacity through 2033.

Europe Automated Container Terminal Market Trends and Insights

Europe holds 25.0% of the global market in 2026, valued at US$ 3.62 billion. Strong regulations promoting smart ports, decarbonisation, and digitalisation drive growth. Advanced automation in Northern Europe leads globally, while expansion into Southern and Eastern ports is broadening demand and sustaining steady market growth.

- Germany Automated Container Terminal Market Size

Germany accounts for 22% of Europe’s market, around US$ 796 million in 2026. Automation at Hamburg and Bremerhaven supports growth. Strong industrial automation capabilities and Industry 4.0 adoption drive advanced terminal technologies. Continued investment is expected as Hamburg expands capacity to compete with other North Sea ports.

- United Kingdom Automated Container Terminal Market Size

The UK holds 14% of Europe’s market, about US$ 507 million in 2026. Growth is driven by automation at Felixstowe, Southampton, and London Gateway. Post-Brexit trade shifts and national port policies support investment, while operators focus on automation to improve efficiency and offset rising costs and customs complexities.

- France Automated Container Terminal Market Size

France represents 11% of Europe’s market, about US$ 398 million in 2026. Automation is focused at Le Havre and Marseille-Fos, supported by reforms and EU funding. Easing labour constraints and productivity needs enable projects, while ambitions to regain transshipment traffic drive future investment in terminal automation.

Asia Pacific Automated Container Terminal Market Trends and Insights

Asia Pacific holds 39.0% of the global market in 2026, valued at US$ 5.66 billion, and is the fastest-growing region. Growth is driven by major ports, government programmes, and strong automation suppliers. Initiatives like Belt and Road and Sagarmala expand deployment, increasing regional market share through 2033.

- China Automated Container Terminal Market Size

China accounts for 47% of Asia Pacific’s market, about US$ 2.66 billion in 2026. Growth is driven by state investments, major ports, and companies like ZPMC. Government policies support smart ports and automation technologies, positioning China as both a leading market and global exporter of terminal automation solutions.

- Japan Automated Container Terminal Market Size

Japan represents 16% of Asia Pacific’s market, about US$ 905 million in 2026. Growth is supported by the Smart Port initiative and upgrades at key terminals. Strong robotics expertise enables advanced automation adoption, while ongoing infrastructure modernisation ensures steady growth and competitiveness within the regional port landscape.

- India Automated Container Terminal Market Size

India holds 10% of Asia Pacific’s market, about US$ 566 million in 2026. Growth is driven by Sagarmala and national port programmes. Rising trade volumes strain traditional capacity, encouraging automation. Both government and private operators are accelerating investments, making India a high-growth market for terminal automation through 2033.

Competitive Landscape

The automated container terminal competitive landscape is moderately consolidated at the equipment tier but fragmented across software and services segments, creating a structurally layered competitive environment. A small number of global OEMs, including ZPMC, Konecranes, Kalmar (Cargotec), Liebherr, and ABB, dominate capital equipment supply and leverage installed-base scale to defend market position. The software and TOS segment features greater fragmentation, with specialist vendors including Navis, CyberLogitec, and Tideworks competing on platform functionality, integration capability, and client switching costs.

The primary basis of competition at the equipment tier is engineering capability, delivery track record, and financing support capacity. In software, competitive differentiation pivots on AI-powered optimisation depth, real-time data analytics sophistication, and interoperability with multi-vendor hardware ecosystems. Strategic M&A and technology partnership activity is intensifying as incumbents seek to extend platform value propositions and defend against software-native disruptors entering the port automation space.

Key Developments:

- January, 2025: Konecranes Plc announced a major automated stacking crane supply agreement for a large-scale brownfield terminal expansion project in Northern Europe, incorporating advanced predictive maintenance and fleet management systems integration, reinforcing the company's position as a preferred automation partner for European port authorities pursuing productivity-driven upgrades.

- September, 2024: Cargotec Corporation (Kalmar) launched an enhanced generation of its automated straddle carrier platform, incorporating AI-powered optimisation algorithms and expanded digital twin technology compatibility, targeting semi-automated terminal operators seeking a cost-efficient step toward full yard automation without full infrastructure replacement.

- March, 2024: Navis LLC expanded its N4 Terminal Operating System with an integrated real-time data analytics and IoT-enabled logistics module, enabling port operators to unify yard management systems, gate automation, and vessel planning on a single platform, a development that meaningfully strengthens the competitive moat of software-led automation vendors competing for TOS contract renewals.

Automated Container Terminal Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 10.46 Billion |

| Current Market Value (2026) | US$ 14.50 Billion |

| Projected Market Value (2033) | US$ 22.09 Billion |

| CAGR (2026 - 2033) | 6.2% |

| Leading Region | Asia Pacific (39%) |

| Dominant Degree | Semi-Automated Terminals (55.0%) |

| Top-ranking Offering | Equipment (47.0%) |

| Top-ranking Project Type | Brownfield Projects (68.0%) |

| Top-ranking End-user | Port Authorities / Government Terminals (49.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 7.59 Billion |

Companies Covered in Automated Container Terminal Market

- ABB Ltd.

- Cargotec Corporation

- Konecranes Plc

- Liebherr Group

- Shanghai Zhenhua Heavy Industries Co., Ltd.

- Siemens AG

- CyberLogitec Co., Ltd.

- Künz GmbH

- TMEIC

- Navis LLC

- Tideworks Technology Inc.

- Camco Technologies

- Identec Solutions AG

- Orbcomm Inc.

- Inform GmbH

- PSA International Pte Ltd.

- DP World Limited

- APM Terminals

- Daifuku Co., Ltd.

- Gottwald Port Technology GmbH

- Wärtsilä Corporation

- Hexagon AB

Frequently Asked Questions

The global Automated Container Terminal Market is valued at US$ 14.50 billion in 2026 and projected to reach US$ 22.09 billion by 2033, growing at a CAGR of 6.2%.

Growth is driven by increasing container volumes, high labour costs, mega-vessel capacity pressures, and government-backed smart port initiatives promoting automation, efficiency, and digital transformation across global port infrastructure.

Semi-automated terminals dominate with 55% share in 2026, as they balance efficiency and cost, offering throughput improvements without the high capital investment and operational risks of fully automated terminals.

Asia Pacific leads with 39% market share in 2026, driven by major ports, strong trade volumes, and government-led automation programmes, making it both the largest and fastest-growing regional market.

Major opportunities lie in deploying AI, digital twins, and predictive maintenance on semi-automated terminals, enabling software-led value creation without full hardware upgrades, especially for early-moving technology vendors.

The market is moderately consolidated in equipment but fragmented in software, with key players like ABB, Konecranes, and ZPMC competing on lifecycle value, technology integration, and long-term service capabilities.