- Industrial Machinery

- Automated Feeding Systems Market

Automated Feeding Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Automated Feeding Systems Market by Component (Hardware, Software, and Services), By System (Conveyor Feeding System, Self-Propelled Feeding System, and Rail-Guided Feeding System), by Livestock (Ruminants, Poultry, Swine, and Others), and Regional Analysis for 2026 - 2033

Automated Feeding Systems Market Size and Trends Analysis

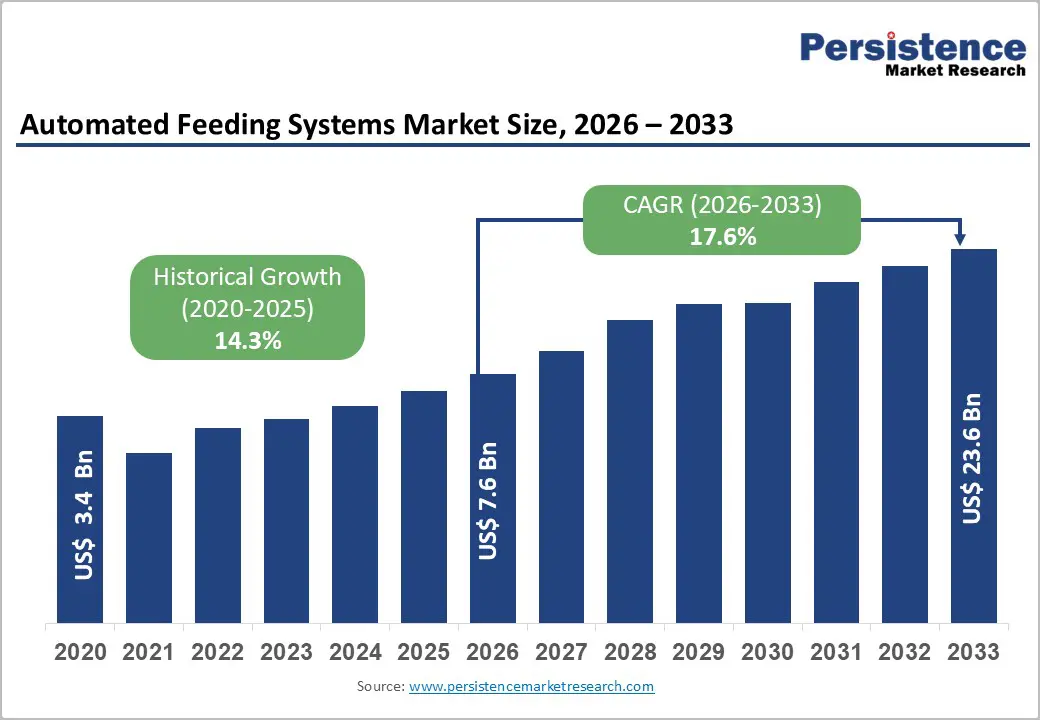

The global automated feeding systems market size is likely to be valued at US$ 3.4 billion in 2020 and reached approximately US$ 7.6 billion in 2026, with projections to reach US$ 23.6 billion by 2033, growing at a robust CAGR of 17.6% during the 2026-2033 forecast period. The market has demonstrated consistent historical growth at a 14.3% CAGR from 2020-2026, with significant acceleration in the forward projection period.

This acceleration is driven by the increasing mechanization of livestock farming operations, rising demands for feed efficiency amid elevated commodity costs, and technological adoption to address labor constraints in agriculture. The sector is transitioning from manual feeding practices toward integrated, digitalized systems that enhance operational efficiency and animal welfare outcomes across global livestock production chains.

Key Industry Highlights:

- Component Leadership & Software Acceleration: Hardware dominates with 65%+ revenue share reflecting capital-intensive system deployment, while software represents the fastest-growing component at 19% CAGR, reflecting market transition toward data-driven, AI-enabled farm operations.

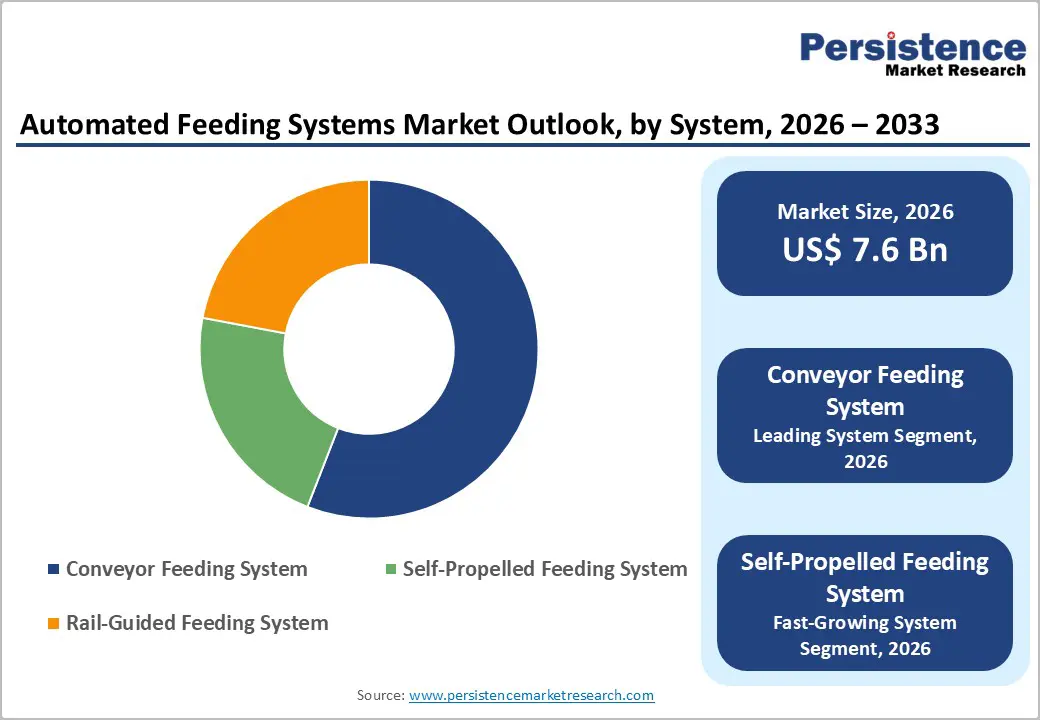

- System Growth Leaders: Conveyor systems command 45%+ market share as a dominant, established technology, while self-propelled systems exhibit the fastest growth at a 19.2% CAGR, driven by adoption in grass-fed, regenerative, and pasture-based production models that are gaining sustainability emphasis.

- Livestock Expansion: Ruminants (dairy, beef) maintain 40%+ market share, reflecting production scale, while poultry demonstrates the fastest expansion at 19.5% CAGR, driven by intense production methodologies and feed cost optimization imperatives across Asian production expansion.

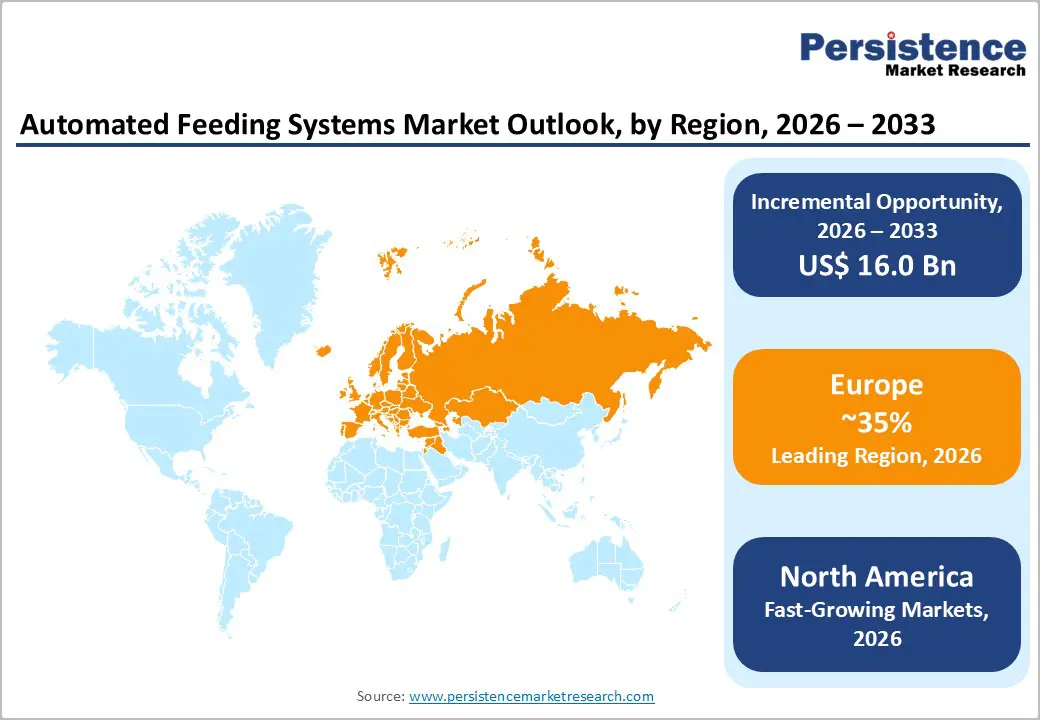

- Regional Growth Leadership: Europe leads with 35%+ global share, while North America demonstrates fastest growth at 19.8% CAGR driven by acute labor scarcity and regulatory intensity. Asia Pacific represents the fastest-growing absolute market with 18-20% CAGR reflecting production expansion and emerging market mechanization.

- Strategic Market Developments: Post-2023 consolidation reflects software value migration, with platform integration (GEA-Houle), cloud partnership development (Lely-Microsoft), and precision nutrition technology launches (Delaval) demonstrating competitive emphasis on ecosystem integration and recurring revenue models.

- Sustained global poultry production supports automation demand: Global chicken meat production is estimated at 103.3 million tons in 2024, remaining largely stable despite regional fluctuations, underscoring the need for efficient, high-throughput feeding solutions in large-scale poultry operations, according to the Food and Agriculture Organization (FAO).

- Regional production shifts emphasize efficiency-driven technologies: A downward revision in U.S. poultry production is offset by increased output in the EU and UK, while Brazil and China maintain stable volumes, highlighting the growing importance of standardized and automated feeding systems to sustain productivity across regions, as per FAO.

- Strong export volumes sustain commercial-scale farming: Global chicken meat exports are projected at 13.9 million tons in 2024, indicating continued large-scale poultry production systems where automated feeding plays a key role in feed precision, labor reduction, and cost optimization, as per FAO.

- Export demand volatility accelerates cost-control strategies: Weaker import demand from Saudi Arabia, South Korea, and Japan is pressuring exporters such as Brazil and the U.S., prompting producers to adopt automated feeding systems to protect margins by reducing feed waste and improving operational efficiency, according to the FAO.

| Key Insights | Details |

|---|---|

|

Automated Feeding Systems Market Size (2026E) |

US$ 7.6 Bn |

|

Market Value Forecast (2033F) |

US$ 23.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

17.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

14.3% |

Market Dynamics

Drivers - Rising Labor Scarcity and Operational Efficiency Demands

The global livestock farming sector faces unprecedented labor availability challenges, with agricultural workforce participation declining across developed economies at rates exceeding 3-5% annually. Automated feeding systems address this critical gap by reducing manual labor requirements by 40-60%, enabling farmers to maintain or expand production with constrained workforce resources. In North American dairy operations, labor costs represent 18-22% of total operating expenses, creating strong economic incentives for automation adoption.

European Union regulations mandate improved animal welfare standards that require precision feeding protocols, achievable only efficiently through automated systems. The efficiency gains translate to feed conversion improvements of 8-12%, directly impacting profitability in commodity-constrained markets. Integration with farm management information systems (FMIS) enables real-time monitoring and data-driven decision-making, which are essential for large-scale operations managing herds of 500 or more animals. Market data indicates that farms with automated feeding infrastructure achieve 15-18% higher productivity metrics than conventional operations, justifying capital expenditure decisions despite upfront costs ranging from $50,000 to $200,000 per installation.

Restraint - Technological Integration, Complexity,y and Skills Gap

Automated feeding systems integration within existing farm operations presents significant technical complexity, requiring skilled technicians for installation, calibration, and ongoing maintenance, a specialist workforce experiencing acute shortage across major agricultural regions. European countries report vacancy rates of 25-35% for agricultural machinery technician positions, while North American and Asian markets face comparable constraints. System interoperability challenges persist due to limited vendor-standardization, creating "lock-in" effects that increase switching costs and reduce competitive pressure on providers. Farm operators frequently lack the technical literacy required for system programming, troubleshooting, and data interpretation, necessitating external support arrangements that extend implementation timelines by 30-60% and increase total cost of ownership. Cybersecurity vulnerabilities in connected farming systems have emerged as serious risks, with documented cases of compromised systems impacting animal welfare and farm operations. These integration barriers disproportionately affect small and mid-sized operations, concentrating market adoption within larger, better-capitalized farming enterprises and effectively fragmenting the addressable market across geographies and farm scales.

Opportunity - Integration with Precision Livestock Farming (PLF) Ecosystems

The convergence of automated feeding systems with broader Precision Livestock Farming technologies, encompassing wearable sensors, biometric monitoring, behavioral analytics, and artificial intelligence, creates ecosystem opportunities valued at US$ 3.2-3.8 billion over the 2026-2033 forecast period. Integrated PLF platforms that enable real-time animal health monitoring, early disease detection, and performance optimization have demonstrated veterinary cost reductions of 15-20% and improvements in health-related mortality of 10-15%. Leading agricultural research institutions document that integrated feeding and monitoring systems improve feed conversion ratios by 12-18%, substantially exceeding single-technology implementations.

Market opportunity centers on premium production segments, including organic dairy, grass-fed beef, and specialty poultry operations, which command price premiums of 20-30%, where consumers and retailers mandate comprehensive sustainability and welfare documentation. Adopting the software-as-a-service (SaaS) business model creates recurring revenue opportunities and superior customer retention compared to traditional capital equipment sales. The estimated market opportunity for PLF integration services spans US$ 400-700 million, representing the fastest-growing segment within the broader automated feeding systems market architecture.

Category-wise Analysis

Component Insights - Hardware Dominance and Rapid Software Growth Reshape Automated Feeding Systems Market

The component structure of the automated feeding systems market is strongly influenced by the capital-intensive nature of farm automation investments. Hardware remains the leading segment, accounting for over 65% of total market revenue. This dominance is driven by the high cost and technical complexity of physical components such as conveyor mechanisms, motor assemblies, control electronics, and feed distribution networks. These systems require advanced mechanical engineering, robust materials, and precision manufacturing, which result in a significant upfront investment. In addition, hardware installations typically follow long replacement cycles of 8 to 12 years, reinforcing their substantial share of the total system value. Hardware suppliers also benefit from recurring demand, as wear-and-tear components require periodic replacement, enabling service contracts and aftermarket sales that enhance customer lifetime value.

In contrast, software represents the fastest-growing component segment, expanding at a CAGR of approximately 19%, well ahead of hardware growth. Software solutions include farm management information systems, animal performance monitoring, precision nutrition tools, and AI-enabled predictive analytics. Growth is fueled by the shift toward data-driven farming and cloud-based SaaS models, which lower adoption barriers for smaller farms. As the installed hardware base expands, demand for advanced analytics is accelerating, creating a software opportunity estimated between US$ 800 million and US$ 1.2 billion through 2033.

Systems Insights - Conveyor Systems Dominate Automated Feeding, While Self-Propelled Solutions Accelerate Rapidly Globally

The automated feeding systems market is characterized by a clear technology hierarchy shaped by adoption maturity, operational scale, and application versatility. Conveyor feeding systems represent the leading segment, accounting for over 45% of total market revenue. Their dominance is driven by proven operational reliability, ease of integration with existing farm infrastructure, and wide applicability across multiple livestock categories, including ruminants, poultry, and swine. The technological maturity of conveyor systems has enabled cost efficiencies, offering a 20–35% pricing advantage over alternative solutions, while also supporting a well-established global service and maintenance ecosystem. These systems are highly scalable and are therefore disproportionately adopted in large-scale commercial operations such as premium dairy farms, industrial poultry units, and intensive swine production facilities. In Europe and North America regions with high mechanization intensity and larger farm sizes, conveyor installations contribute approximately 58–62% of total system revenues.

In contrast, self-propelled feeding systems represent the fastest-growing segment, expanding at a CAGR of 19.2%. Their rapid growth reflects increasing suitability for extensive grazing models, rotational paddock systems, and outdoor livestock rearing practices aligned with animal welfare and sustainability goals. Key advantages include operational flexibility, minimal fixed infrastructure requirements, and efficient management of dispersed feeding locations. Demand is particularly strong in grass-fed beef, pasture-based dairy, and outdoor swine operations, with cumulative market opportunities estimated at US$ 450–650 million through 2033, led by the European Union, New Zealand, and regenerative agriculture markets.

Livestock Insights - Ruminants Lead Automated Feeding Adoption While Poultry Drives High-Growth Market Expansion

Ruminants, including cattle, buffalo, sheep, and goats, represent the leading livestock segment in the automated feeding systems market, accounting for over 40% of global revenue. This dominance reflects the sheer scale of global dairy and beef production, which collectively involves nearly one billion animals worldwide. Dairy farming remains the core focus, as the integration of automatic milking systems and lactation-stage–linked feeding protocols strongly encourages automation adoption. Ruminant nutrition is technically complex, requiring precise multi-ingredient ration formulation that supports rumen fermentation, microbial protein synthesis, and production stage–specific nutritional needs. These technical demands create a strong value proposition for precision feeding technologies. In addition, the dairy industry’s premium pricing structure and greater capital investment capacity enable adoption rates approximately 2.5 to 3.5 times higher than those of other livestock categories.

In contrast, the poultry segment is the fastest-growing, expanding at a robust CAGR of 19.5%. Growth is driven by intensive production systems that depend on accurate nutrient delivery, strict biosecurity, and optimized environmental control. Feed costs, which account for 55–65% of poultry production expenses, further strengthen the return-on-investment case for automated feeding solutions.

Regional Insights

Europe’s Regulatory-Led Leadership Driving Automated Feeding Systems Market Expansion

Europe stands as the largest global market for automated feeding systems, accounting for approximately 35–37% of the total market share. The regional market is valued at around US$ 2.0–2.2 billion in 2026 and is projected to expand to US$ 7.8–8.8 billion by 2033, registering a steady CAGR of about 15.5%. Growth is largely shaped by strong regulatory enforcement, high levels of farm consolidation, and a mature technological ecosystem.

Germany leads adoption, with automated feeding systems installed in nearly 75–80% of large commercial dairy farms and 60–65% of swine operations. France follows closely, supported by strong precision feeding integration in dairy farming. The Netherlands demonstrates the highest level of technological sophistication, with penetration rates exceeding 80%, while Denmark, Sweden, and Finland show similarly advanced adoption. In contrast, Southern Europe records moderate penetration of 35–45%, reflecting smaller farm sizes and lower mechanization budgets. Central and Eastern Europe remain at earlier stages, with 20–30% penetration, but rapid growth driven by modernization investments.

Regulatory pressure under the EU’s Common Agricultural Policy, Farm to Fork Strategy, and environmental directives is the primary growth catalyst. These frameworks, combined with acute labor shortages and rising wages, have made automated feeding systems a compliance necessity rather than a discretionary efficiency upgrade.

North America’s Automated Feeding Systems Market Driven by Scale, Labor, and Regulation

North America represents the second-largest regional market for automated feeding systems, accounting for approximately 28–30% of global share. The market is valued at around US$ 1.6–1.8 billion in 2026 and is projected to expand rapidly to US$ 5.2–5.8 billion by 2033, making it the fastest-growing major region with a CAGR of 19.8%. The United States dominates regional output, accounting for 75–80% of market value, while Canada and Mexico play important roles in integrated North American supply chains.

The U.S. dairy sector, supported by roughly 9.4 million cows and an annual output of US$ 38–42 billion, has achieved 65–70% automation penetration among large commercial farms. Broiler production records even higher adoption, while swine operations show moderate but accelerating uptake, particularly among large integrated producers. Canadian farms display similar penetration levels, supported by slightly larger average herd sizes.

Market growth is primarily driven by labor shortages, rising agricultural wages, stricter environmental and nutrient-management regulations, and greater supply chain integration with premium dairy and meat processors. Regulatory oversight related to environmental compliance, feed safety, and antimicrobial stewardship further reinforces automation adoption. Competitive intensity remains moderate, with technology differentiation centered on precision nutrition software, data analytics, and retrofit compatibility. Rising private equity and venture capital investments highlight strong long-term confidence in the region’s automated feeding ecosystem.

Competitive Landscape

The global automated feeding systems market demonstrates a moderate-to-high level of fragmentation, with the top ten manufacturers collectively accounting for approximately 55–65% of total global revenue. Despite this concentration among leading players, the market remains structurally diverse and is clearly segmented into three competitive tiers. The first tier consists of global platform leaders around five to six multinational companies that together command nearly 35–40% of the market. These players benefit from comprehensive product portfolios, advanced automation and software integration, and well-established global distribution and service networks, enabling strong customer retention and premium positioning.

The second tier includes roughly 8–12 regional or specialized competitors, contributing an estimated 20–25% market share. These companies typically focus on specific geographies, livestock categories, or niche feeding solutions, allowing them to remain competitive through tailored offerings and localized expertise. The third tier comprises more than 50 emerging and local providers, accounting for 35–45% of market share. Their growth is driven by cost-competitive solutions, customization for local farming practices, and expanding penetration in developing agricultural markets.

Overall market concentration is gradually increasing, supported by accelerating mergers and acquisitions since 2020. While manufacturing entry barriers remain relatively moderate, high technology requirements particularly in software, sensors, and control systems continue to restrict new entrants and favor established players.

Key Industry Developments

- In June 2025, Yanmar participated in a joint demonstration project for a remote automated feeding system aimed at promoting sustainable fisheries. The initiative reflects Yanmar’s strategic focus on applying automation and digital control technologies to improve operational efficiency, reduce resource waste, and support environmentally responsible practices within aquaculture and marine food production systems.

- In 2023, GEA announced the launch of the GEA DairyFeed F4500, an autonomously driving feeding robot designed to enhance sustainability and resilience in dairy farming. As a global leader in milking and feeding technologies, GEA emphasized automation and digital integration to help farms reduce operating costs and carbon emissions while improving flexibility in daily operations. The DairyFeed F4500 was initially scheduled for availability in Germany, Austria, Switzerland, France, and Sweden in the fourth quarter of the year, with a phased global rollout planned thereafter.

- In March 2023, DeLaval expanded its automated feeding portfolio by introducing OptiWagon, an autonomous feed distribution robot integrated into its total feeding solution. The development targeted one of the most cost-intensive and labor-demanding activities on dairy farms-feeding-positioning OptiWagon as a solution to improve efficiency, reduce labor dependency, and ensure consistent feed delivery within modern dairy operations.

Companies Covered in Automated Feeding Systems Market

- Lely

- GEA Group Aktiengesellschaft

- DeLaval

- Trioliet

- HETWIN - FÜTTERUNGSTECHNIK

- Schauer Agrotronic GmbH

- Rovibec Agrisolutions

- RNA Automation Limited

- Fullwood JOZ

- BouMatic

- DAIRYMASTER

- FishFarmFeeder

- Other Market Players

Frequently Asked Questions

The Automated Feeding Systems market is estimated to be valued at US$ 7.6 Bn in 2026.

The key demand driver for the Automated Feeding Systems market is the need to optimize feed costs and reduce labor dependency amid rising large-scale livestock and poultry production.

In 2026, the Europe region will dominate the market with an exceeding 35% revenue share in the global Automated Feeding Systems market.

Among systems, Conveyor Feeding System has the highest preference, capturing beyond 21% of the market revenue share in 2026, surpassing other systems.

Lely, GEA Group Aktiengesellschaft, DeLaval, Trioliet, HETWIN – FÜTTERUNGSTECHNIK, Schauer Agrotronic GmbH, and Rovibec Agri solutions. There are a few leading players in the Automated Feeding Systems market.