- Home Appliances

- Automated Blinds and Shades Market

Automated Blinds and Shades Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Automated Blinds and Shades Market by Product Type (Fully-automatic, Semi-automatic), End Use (Residential, Commercial), Installation (New Installations, Retrofit), Sales Channel (Hypermarkets/Supermarkets, Specialty Stores, Independent Retailers, Online Sales, Others), and Regional Analysis from 2026 to 2033

Automated Blinds and Shades Market Share and Trends Analysis

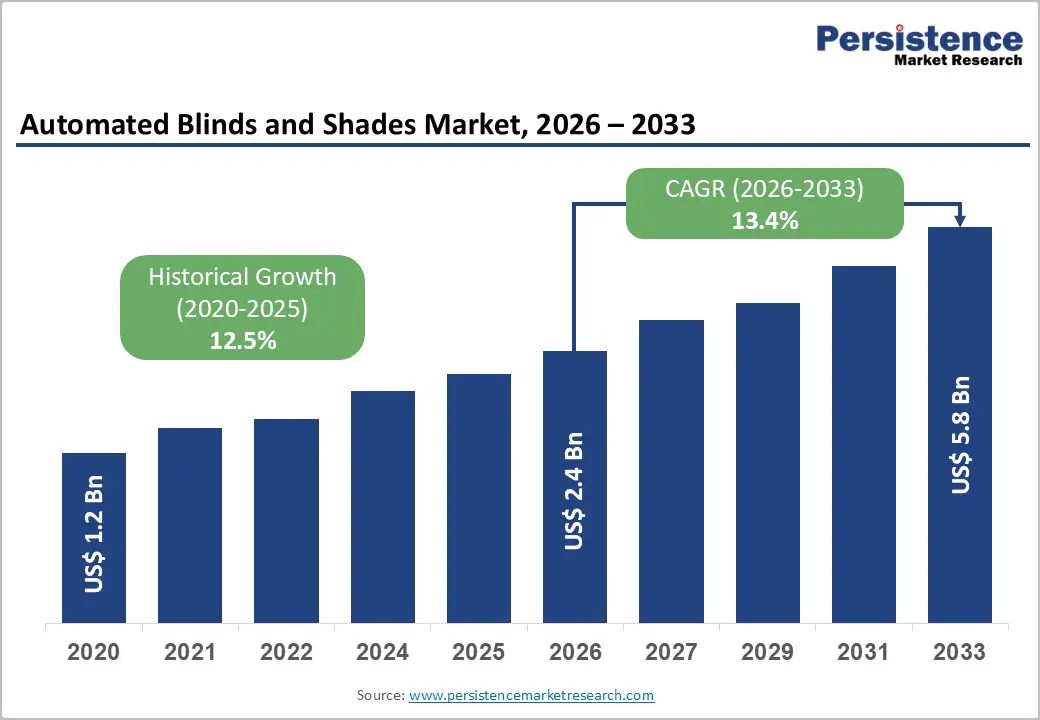

The global automated blinds and shades market size is anticipated at US$ 2.4 billion in 2026 and is projected to reach US$ 5.8 billion by 2033, growing at a CAGR of 13.4% between 2026 and 2033. Accelerating smart home ecosystem adoption, expanding energy efficiency regulations mandating dynamic solar control, and rising consumer demand for voice- and app-controlled home automation are primary growth enablers.

Commercial real estate's transition toward intelligent building management systems is generating large-scale retrofit demand. Asia Pacific's rapid urbanization and rising middle-class disposable income are unlocking high-volume emerging market demand across the forecast period.

Key Industry Highlights:

- The market surged from US$ 1.19 Bn (2020) at a 12.5% historical CAGR, fueled by rapid smart-home penetration and tightening energy-efficiency building regulations.

- Semi-automatic dominates with 71% share, while fully-automatic races ahead at 15.7% CAGR, powered by sensor intelligence, IoT control, and luxury building integration.

- Residential leads with 61% share, while commercial grows fastest at 14.5% CAGR; new installations command 66%, but retrofit outpaces all at 14.9% CAGR.

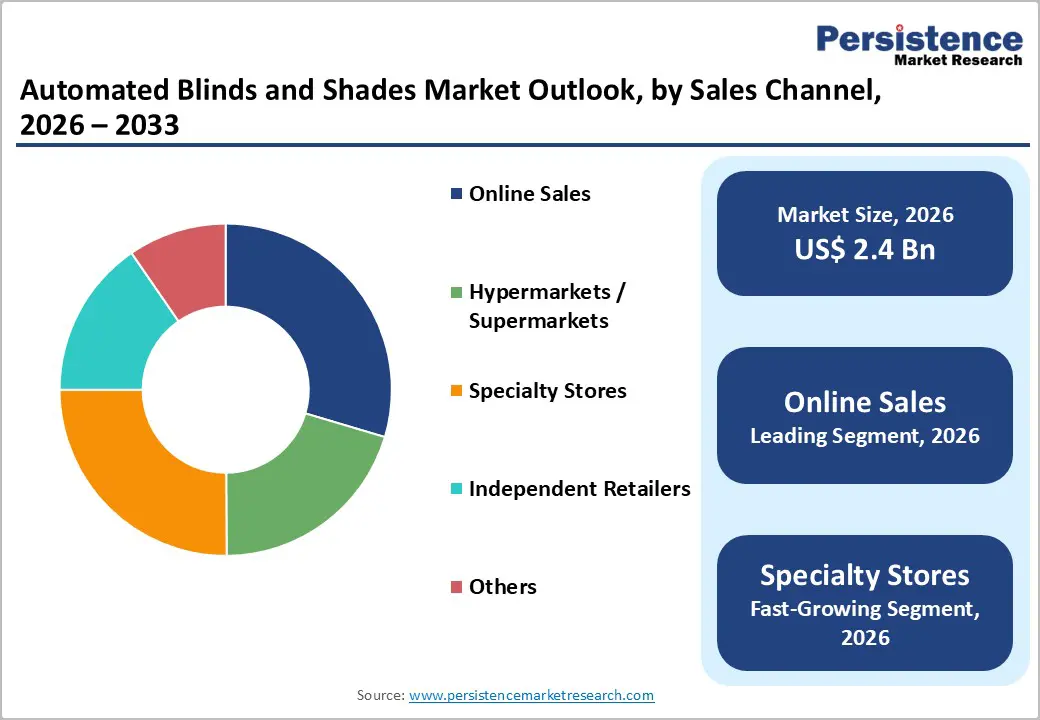

- Online channels capture 30% share, while specialty stores post the fastest growth at 12.1% CAGR, driven by consultative, premium-focused selling models.

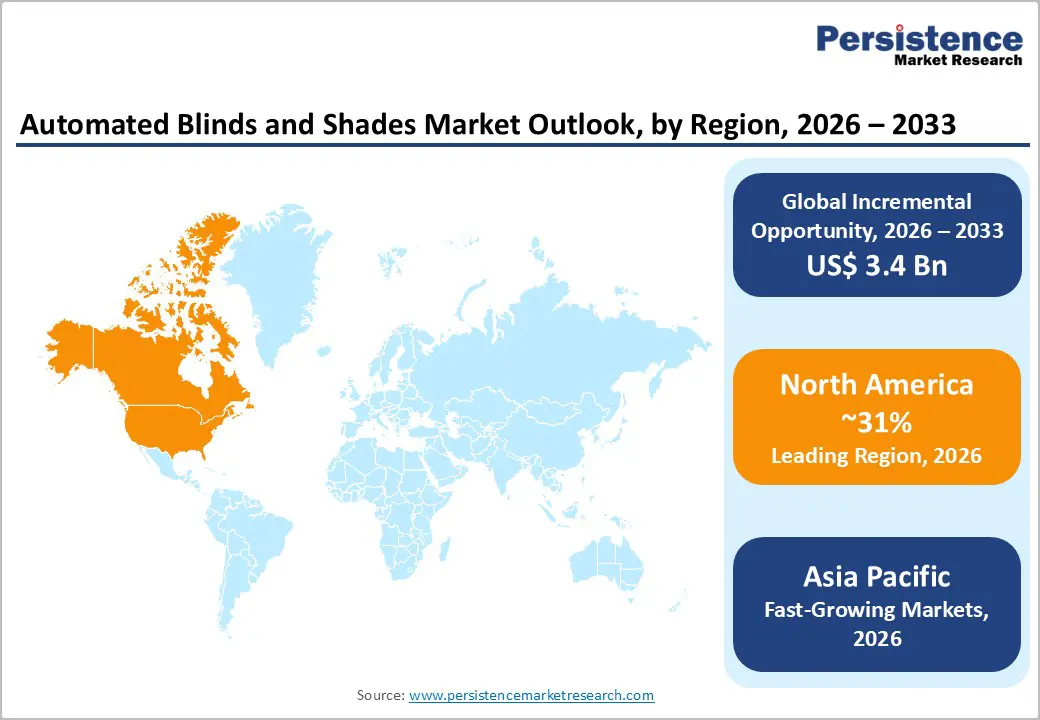

- North America holds ~31% share, Asia Pacific leads at 15.1% CAGR, and Europe advances at 11.8% CAGR under EPBD and Renovation Wave mandates.

- Post-2023 strategies center on Matter protocol integration, luxury system launches, Asia Pacific expansions, and developer-channel supply agreements, redefining market leadership.

| Key Insights | Details |

|---|---|

| Automated Blinds and Shades Market Size (2026E) | US$ 2.4 Billion |

| Market Value Forecast (2033F) | US$ 5.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 13.4% |

| Historical Market Growth (2020 - 2025) | 12.5% |

Market Dynamics Analysis

Drivers - Smart Home Ecosystem Proliferation and IoT Integration

Global smart home solutions market revenues reached US$ 113.4 billion in 2025, with compound annual growth projected at over 10.7% through 2032. Automated window treatments are among the top five fastest-adopted smart home product categories, driven by seamless integration with Amazon Alexa, Google Home, and Apple HomeKit ecosystems. The International Data Corporation (IDC) estimates that 1.5 billion connected smart home devices were shipped globally in 2023 alone, expanding the compatible platform base for motorized blind and shade installations. Consumer preference for unified app-based home control, growing voice-command adoption, and declining wireless communication module costs are lowering adoption barriers, directly accelerating both new installations and retrofit demand across residential and light commercial segments globally.

Building Energy Efficiency Regulations and Green Building Standards

Stringent energy efficiency mandates are structurally embedding automated solar shading into new construction and renovation projects globally. The EU's Energy Performance of Buildings Directive (EPBD) recast requires all new buildings to achieve net-zero energy performance by 2030, with automated solar control recognized as a compliance pathway. In the U.S., ASHRAE Standard 90.1 and California's Title 24 building code require dynamic fenestration control in commercial projects exceeding 5,000 sq ft. The U.S. Department of Energy estimates automated shading systems can reduce cooling loads by up to 30% and heating loads by 20%. LEED and BREEAM green building certification frameworks award credits for dynamic shading integration, incentivizing architects and developers to specify automated blinds and shade systems as standard building envelope components in premium construction projects.

Restraints - High Product and Installation Costs Limiting Mass-Market Penetration

Fully-automatic motorized blind and shade systems for a typical residential installation range between US$ 800-3,500 per window, including hardware, motor, hub, and professional installation labor. This price point primarily restricts adoption to premium and luxury residential segments, excluding the mid-market and affordable housing categories, which represent the largest volume of new construction globally. Consumer payback period calculations based solely on energy savings range from 8 to 15 years in moderate climates, weakening the economic argument outside premium positioning. Cost barriers are compounded in multi-window commercial projects, where system integration and commissioning costs add significant project overhead.

Interoperability, Complexit,y and Consumer Technical Adoption Barriers

The automated shading market remains fragmented across competing wireless communication protocols, Z-Wave, Zigbee, Wi-Fi, and proprietary RF systems, creating interoperability complexity for end-users and installers. A 2023 Parks Associates consumer survey found that 38% of smart home device owners reported frustration with multi-brand device integration. Retrofit installations in older buildings often require extensive rewiring or hub additions, increasing total installation cost. The lack of standardized control interfaces and the technical complexity of integrating automated shades with existing building management systems (BMS) in commercial applications slow adoption among non-specialist property operators and cost-conscious facility managers.

Opportunity - Commercial Building Retrofit and Smart Building Upgrades

The global commercial building stock exceeds 5.9 million buildings in the U.S. alone (U.S. EIA), and the majority lack automated solar shading systems. The EU's Renovation Wave aims to upgrade 35 million buildings by 2030, with automated window treatments eligible for energy renovation subsidies across member states. Commercial retrofit demand is projected to generate over US$ 900 million in annual automated shading revenue by 2030 across North America and Europe. Office, hospitality, and healthcare building upgrades represent the highest-value commercial retrofit sub-segments, driven by occupant comfort standards, energy certification requirements, and corporate ESG commitment frameworks actively shaping procurement decisions.

Specialty Retail and Interior Design Channel Expansion

Specialty window treatment stores are the fastest-growing sales channel at 12.1% CAGR, driven by high-value consultative selling, sample visualization, and professional installation services that online channels cannot replicate for complex automated systems. Interior designers and architects are a highly influential specifier channel. The American Society of Interior Designers (ASID) reports that over 65% of designers actively specify automated shading in residential projects above US$ 500,000. Manufacturer investment in designer showrooms, specification tools, and certified installer networks is creating a defensible premium channel with high conversion rates and strong revenue per project, differentiating against commoditized online price competition.

Category-wise Analysis

Product Type Insights

Semi-automatic automated blinds and shades lead the product type segment with a commanding 71% market share in 2026. Semi-automatic systems requiring a single manual command via remote, app, or voice trigger to initiate motorized operation represent the more accessible and widely adopted product tier. Their lower hardware costs relative to sensor-driven, fully automatic systems, simplified installation requirements, and compatibility with standard smart home platforms have driven mass adoption across both residential and entry-level commercial applications. The semi-automatic category serves the broadest addressable market across North America, Europe, and the Asia Pacific's mid-to-premium residential segments.

Fully-automatic systems are the fastest-growing segment, expanding at a CAGR of 15.7% through 2033. Sensor-integrated, schedule-driven automation that responds autonomously to light, temperature, and occupancy data is gaining traction in premium residential smart homes and energy-certified commercial buildings, where hands-free operation and building management integration are prioritized procurement requirements.

End-user Insights

Residential end use comprising apartment buildings and individual residences, including villas, row houses, and bungalows, leads with a 61% market share in 2026. Residential demand is anchored by the premium and luxury housing segments, where smart home automation packages are standard specifications. Rising homeowner spending on home improvement and smart technology, growing awareness of energy savings, and the expanding availability of consumer-friendly DIY installation options for semi-automatic systems are sustaining residential dominance. Apartment building developers increasingly incorporate motorized window coverings as a value-add amenity in premium multi-family residential developments across North America and the Asia Pacific.

Commercial end use spanning retail, hospitality, offices, healthcare, and educational institutions is the fastest-growing segment, with a 14.5% CAGR through 2033. Hospitality and high-end office developments are leading commercial adoption, driven by building energy codes, occupant experience standards, and ESG-linked building certification requirements mandating dynamic solar control integration.

Installation Insights

New Installations dominate the installation segment with a 66% market share in 2026, reflecting construction-cycle-driven demand in residential and commercial property development across all geographies. Developer-level specifications in premium residential and commercial building projects are embedding automated shading as standard, generating high-volume new installation revenue. New construction projects in the Asia Pacific, particularly China and India, represent the most significant volume driver, with smart home and intelligent building system packages routinely including automated window treatment systems as integrated building technology components for premium project tiers.

Retrofit is the fastest growing installation segment at 14.9% CAGR through 2033, nearly matching market-level growth driven by EU building renovation programs, North American smart home upgrade cycles, and the expanding availability of wireless retrofit-compatible motorized shading solutions that eliminate the need for disruptive hard-wiring during installation.

Sales Channel Insights

Online Sales leads all sales channels with a 30% market share in 2026, reflecting the shift of consumer purchasing behavior toward e-commerce platforms for home improvement and smart home products. Amazon, Wayfair, and brand-direct D2C platforms are the primary online revenue channels, offering product comparison, customer reviews, and bundled subscription installation services. The online channel serves price-conscious residential buyers and entry-level commercial purchasers, prioritizing convenience and breadth of selection. Digital marketing, video product demonstrations, and AI-driven room visualization tools are enhancing online conversion rates for automated shading products.

Specialty stores are the fastest-growing channel at 12.1% CAGR through 2033. Expert consultation, physical product demonstration, and professional installation referral services are driving specialty retail growth for complex automated shading systems that require tailored sizing, motor selection, and smart home integration guidance unavailable through generalist retail or online purchasing channels.

Regional Market Insights

North America Automated Blinds and Shades Market Trends

North America holds the largest regional share at approximately 31% of the global Automated Blinds and Shades Market in 2026. The United States drives regional demand, supported by high adoption rates of smart home devices in U.S. households, strong luxury housing construction, and energy efficiency mandates for commercial buildings, including ASHRAE and California Title. The U.S. Department of Energy's Building Technologies Office actively funds dynamic shading research and incentivizes commercial adoption. Canada's National Energy Code for Buildings supports the adoption of automated solar shading in new commercial construction. North America's mature installer network and strong specialty retail channel sustain premium market value positioning.

Brand investment in certified designer and installer networks, integration partnerships with leading smart home platforms, and growing commercial retrofit demand driven by corporate ESG building certifications collectively reinforce North America's position as the global revenue anchor market for automated blinds and shades.

Europe Automated Blinds and Shades Market Trends

Europe is expanding at a CAGR of 11.8% through 2033, driven by the EU's binding energy efficiency legislative agenda. Germany, France, the U.K., and Spain lead regional market development. The EU's Energy Performance of Buildings Directive recast and Renovation Wave initiative are creating structural policy-driven demand across both new construction and retrofit segments. Germany's Gebäudeenergiegesetz (GEG) building energy law and France's RE2020 construction standard explicitly recognize dynamic solar control as a compliance mechanism. Somfy and Nice SpA, Europe-headquartered market leaders, benefit from strong regional brand recognition and established installer distribution networks across Western European markets.

Spain's Balearic and Mediterranean building stock renovation programs and the U.K.'s Future Homes Standard regulatory framework are generating steady near-term retrofit project pipeline. European markets demonstrate the highest automated shading specification rates globally in new commercial construction, led by BREEAM and HQE green building certification requirements.

Asia Pacific Automated Blinds and Shades Market Trends

Asia Pacific is the fastest-growing region at 15.1% CAGR through 2033, poised to emerge as the second-largest regional market by 2030. China's annual premium residential and commercial construction output, India's smart city and luxury housing development boom, and Japan's precision interior design culture collectively drive regional momentum. ASEAN luxury property markets in Singapore, Malaysia, and Vietnam are rapidly adopting automated window treatments as standard smart home specifications. Regional manufacturing advantages particularly in China's Zhejiang and Guangdong provinces, are reducing product cost structures, enabling competitive pricing at mid-tier residential market segments inaccessible to premium European brands.

Government smart city infrastructure programs in India and China, expanding middle-class home improvement spending, and growing international hotel brand investments in ASEAN hospitality real estate are creating a multi-vector demand expansion environment across the Asia Pacific region through the forecast horizon.

Competitive Landscape

Market leaders are converging on smart ecosystem integration as the dominant strategic theme prioritizing Matter protocol compatibility, voice-platform partnerships, and API-driven BMS integration to embed automated shading within broader smart home and building automation architectures. Premium channel investment via designer showrooms, certified installer networks, and architect specification programs, alongside Asia Pacific geographic expansion, define the competitive differentiation strategies of leading market players.

Strategic Developments

- In February 2025, Amazon.com, Inc. unveiled Alexa+, its upgraded AI-powered virtual assistant. Alexa+ integrates generative AI capabilities, powered by Amazon Bedrock models like Nova and Anthropic’s Claude AI, enabling more natural conversations, improved contextual understanding, and multi-command handling.

- In September 2024, Schneider Electric SE launched an AI-powered energy management feature in its Wiser Home app to optimize energy consumption for water heaters and EV chargers. This feature, developed in-house, uses AI to learn from user habits, weather forecasts, and tariff data to automatically manage energy loads and reduce bills.

Companies Covered in Automated Blinds and Shades Market

- Somfy Group

- Hunter Douglas N.V.

- Lutron Electronics Co., Inc.

- Springs Window Fashions

- Legrand SA

- Nice SpA

- IKEA Group

- Budget Blinds (Home Franchise)

- Mechoshade Systems LLC

- Rollease Acmeda

- Graber (Springs Industries)

- Elero GmbH

- Bali Blinds & Shades

- AutomationDirect (Hikvision)

Frequently Asked Questions

The global automated blinds and shades market is projected at US$ 2.4 Billion in 2026, expanding to US$ 5.8 Billion by 2033.

Smart home ecosystem proliferation, binding building energy efficiency regulations, and rising premium residential and commercial construction specifying integrated automation packages are the primary market growth drivers.

The automated blinds and shades market is projected to grow at a 13.4% CAGR between 2026 and 2033.

Commercial building retrofit programs, Asia Pacific emerging market residential demand, and specialty retail channel expansion represent the highest-value near-term growth opportunities for market participants.

Leading players include Somfy Group, Hunter Douglas, Lutron Electronics, Springs Window Fashions, Legrand, Nice SpA, Mechoshade Systems, Rollease Acmeda, and IKEA, among others.