- Aerospace & Defense

- Aircraft Engines Market

Aircraft Engines Market Size, Trends, Share, and Forecasts for 2025 - 2032

Aircraft Engines Market by Engine (Turboprop, Turbofan, Turboshaft, and Piston Engine Driven), Aircraft (Commercial Aircraft, Military Aircraft, Business and General Aviation Aircraft), Component (Compressor, Turbine, Gearbox, Exhaust System, Fuel System, and Others), and Regional Analysis 2025 - 2032

Aircraft Engines Market Share and Trends Analysis

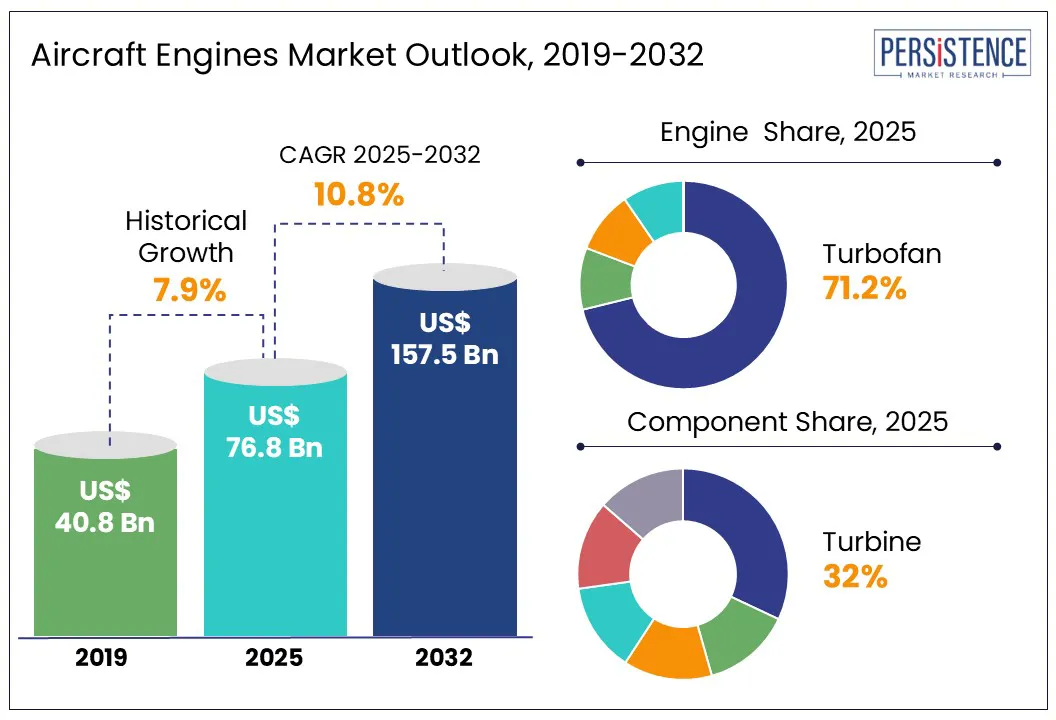

The global aircraft engines market size is likely to be valued at US$ 76.8 Bn in 2025 to US$ 157.5 Bn by 2032, growing at a CAGR of 10.8% for the forecast period from 2025 to 2032.

The aircraft engine market is experiencing a huge demand for fuel-efficient and environmentally friendly engines, driven by airlines’ efforts to reduce operational costs and comply with strict emissions regulations. This has led to a growing preference for engines that offer improved fuel efficiency and lower carbon emissions per flight hour. Technological advancements, including efficient turbine designs and the use of lightweight materials, are accelerating innovation.

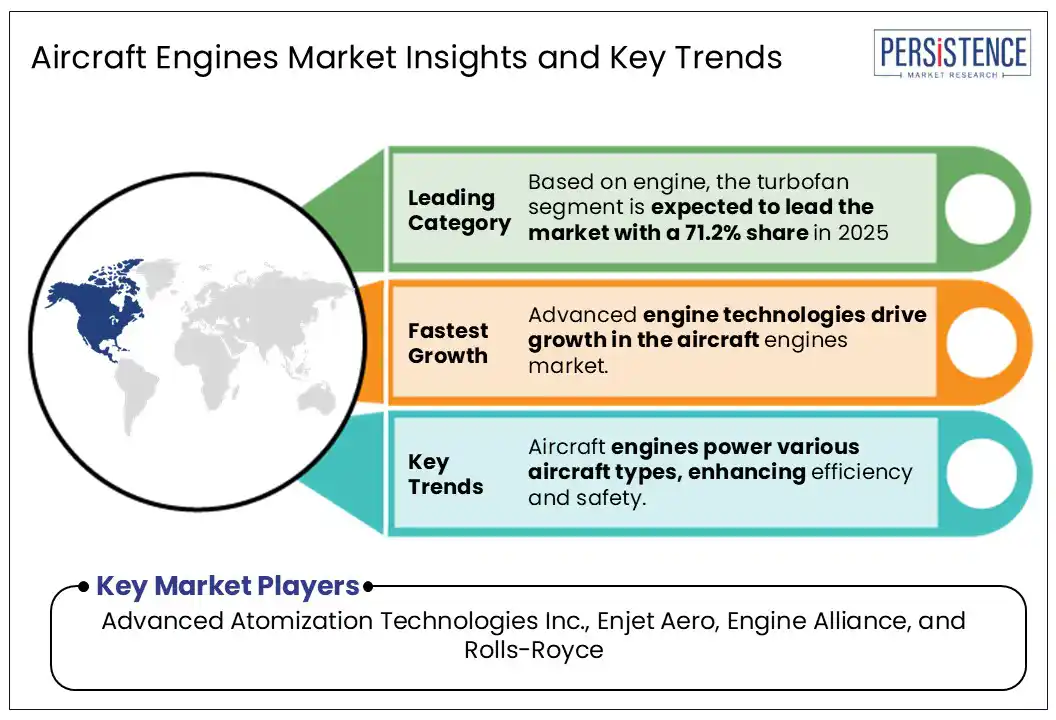

Aircraft engines are essential across various types of aircraft, enhancing operational efficiency, safety, and reliability. They are widely used in narrow-body and wide-body aircraft, private jets, transport planes, fighter jets, helicopters (both commercial and military), and unmanned aerial vehicles (UAVs). The growing number of commercial flight operations globally is expected to be a major driver of the aircraft engine market growth in the coming years.

Key Industry Highlights:

- The development of more efficient, environment-friendly engine technologies and the adoption of advanced engine technologies fuel aircraft engines market growth.

- North America market is projected to account for 35.1% of the market share by 2025.

- The industry demand is fueled due to increased air travel demand, fleet expansion, and demand for fuel-efficient engines.

- Technological advancements such as lightweight materials and advanced engine designs, are driving market growth.

- Based on engine, the turbofan segment is expected to lead the market with a 71.2% share in 2025

- Regulatory changes in emission reductions and noise abatement are driving manufacturers to invest in engine efficiency innovation.

- The commercial aircraft segment is predicted to achieve the largest revenue share in 2025.

|

Global Market Attribute |

Key Insights |

|

Aircraft Engines Market Size (2025E) |

US$ 76.8 Bn |

|

Market Value Forecast (2032F) |

US$ 157.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

10.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.9% |

Market Dynamics

Driver - Surge in adoption of cost-effective and fuel-efficient aircraft is accelerating market growth

The surge in adoption of cost-effective and fuel-efficient aircraft is significantly accelerating market growth in the aviation sector. Airlines and manufacturers are prioritizing fuel efficiency to reduce operational costs amid rising fuel prices and stringent environmental regulations. Advances in lightweight engine technology, such as GE Aviation’s 3D printed components and CFM International’s LEAP engines, reduce aircraft weight and fuel consumption by 15%, lowering emissions and costs.

Additionally, the shift to electric aircraft, replacing traditional systems with electric ones, further enhances fuel efficiency and sustainability, supported by strong investments and regulatory pressure globally. This trend drives fleet modernization, especially in high-growth regions such as Asia Pacific and the Middle East, fostering innovation and expanding demand for next-generation, eco-friendly aircraft.

GE Aerospace has announced an investment of USD 11 million to upgrade its aircraft engine repair facility in Singapore into a state-of-the-art “smart factory.” This transformation aims to revolutionize engine repair processes and enhance workforce skill development, ensuring the facility is equipped to support emerging technologies and future demands in the aerospace sector.

Restraint - Environmental regulations and high development and production costs

Stricter environmental regulations targeting reductions in carbon emissions and noise pollution are compelling aircraft engine manufacturers to develop cleaner, more efficient engines. Meeting these standards often requires substantial investment in research and development, which can strain financial resources and cause delays in production schedules. The complexity of aircraft engine design, coupled with rigorous safety requirements and the use of advanced materials, makes development and manufacturing costly.

These high expenses create barriers for new companies attempting to enter the market and pressure established firms to enhance operational efficiency without compromising quality or safety. Consequently, manufacturers must balance innovation with cost control to remain competitive while adhering to evolving environmental and regulatory demands.

Opportunity - Growth of Unmanned Aerial Vehicles (UAVs)

The aircraft engines market is experiencing significant growth driven by the increasing adoption of unmanned aerial vehicles (UAVs) across various sectors. UAVs are being utilized for applications such as cargo delivery, surveillance, and agricultural monitoring, necessitating the development of lightweight and efficient engines tailored for these platforms. This trend has opened new avenues in commercial and military domains.

Honeywell International is advancing UAV capabilities by developing hydrogen fuel cells that significantly extend the range of drones, tripling that of traditional battery-powered systems. Rolls-Royce has successfully tested the Taranis unmanned aerial vehicle, powered by the Adour Mk951 engine, marking a significant step in UAV propulsion technology.

The surge in UAV utilization is propelling the demand for specialized aircraft engines that are efficient, lightweight, and reliable. Engine manufacturers are responding by innovating and investing in technologies that cater to the unique requirements of UAVs, thereby expanding their market presence and contributing to the evolution of the aircraft engines industry. Turkish drone maker Baykar is devoting resources to bring more component production in-house amid industry supply chain pressures, and will invest $300 million to develop jet engines.

Category-wise Analysis

Engine Segments Insights

The turbofan engine segment is expected to register the highest CAGR in the aircraft engine market during the forecast period. Also known as fanjet or bypass engines, turbofan engines generate thrust using both the jet core efflux and bypass air accelerated by a ducted fan driven by the engine core. The bypass ratio, which is the mass of air bypassing the core versus that passing through it, defines the engine type low bypass engines rely more on jet core thrust, while high bypass engines derive most thrust from the fan.

Turbofan engines are widely favored due to their superior performance at higher altitudes, lower noise levels, and lighter weight compared to other engine types. These features make them ideal for long-range commercial aircraft, contributing significantly to their rising demand. Their efficiency and environmental benefits further support their dominance in future aircraft engine developments.

Component Insights

The turbine segment is projected to experience the highest compound annual growth rate (CAGR) in the aircraft engine market during the forecast period. Turbines are rotary engines that extract energy from high-velocity combustion gases, converting it into rotational motion to power aircraft propulsion systems. Comprising a series of blades, turbines harness the kinetic energy of exhaust gases, producing thrust as the gases pass through and exit with reduced energy.

The U.S. Department of Defense has promoted market growth through contracts for next-generation propulsion systems, increasing the need for high-performance turbine engines.

NASA has awarded GE Aerospace a contract for Phase 2 of the Hybrid Thermally Efficient Core (HyTEC) program, supporting continued technology development for the next generation of commercial aircraft engines to significantly improve fuel efficiency and reducing emissions compared to current engines.

Regional Insights

Asia Pacific Aircraft Engines Market Trends

Asia Pacific aircraft engine market accounted for a significant revenue share in 2025, fueled by rapid growth in commercial aviation and increasing air travel demand. Countries such as China and India are at the forefront, with substantial investments in new aircraft acquisitions to expand airline fleets. Technological improvements in engine performance and the growing presence of Maintenance, Repair, and Overhaul (MRO) facilities across the region are supporting this surge.

In addition, rising geopolitical tensions have prompted regional powers to modernize their aerial capabilities. For instance, in September 2024, Hindustan Aeronautics Limited (HAL) signed a USD 3.1 billion deal with India's Ministry of Defence to deliver 240 AL-31FP engines for the Su-30MKI fleet. Similarly, China’s government has launched initiatives through 2027 aimed at developing advanced aircraft engines and enhancing domestic aviation capabilities. These factors collectively strengthen the region’s position as a key growth driver in the global aircraft engine market.

North America Aircraft Engines Market Trends

North America is projected to maintain its position as the largest regional market for aircraft engines during the forecast period, driven by robust advancements in aerospace manufacturing and defense aviation.

Key industry players such as General Electric Company, Honeywell International Inc., Collins Aerospace, and Textron Inc. are headquartered in North America, contributing significantly to market growth through continuous research and development initiatives. For instance, GE Aerospace has announced plans to increase jet engine deliveries by 15–20% in 2025, addressing previous supply chain challenges.

The U.S. Department of Defense awarded GE Aerospace and NAVAIR a contract worth USD 683.7 million for T408 engines to power the Sikorsky CH-53K King Stallion helicopters, with deliveries anticipated between 2024 and 2027.

Europe Aircraft Engines Market Trends

The aircraft engine market in Europe is projected to grow at a CAGR of nearly 9% from 2025 to 2032, supported by a well-established aerospace infrastructure and a strong focus on innovation. Leading nations such as Germany, the UK, and France are at the forefront of developing advanced engine technologies aimed at enhancing fuel efficiency, lowering emissions, and minimizing noise to comply with strict EU environmental standards.

Germany’s aircraft engine market is also expected to expand steadily through 2030, supported by a robust aerospace sector and a commitment to sustainability. Cross-border partnerships within the EU continue to boost R&D capabilities, fostering the development of next-generation engines for both commercial and defense aviation.

France held a significant revenue share in 2023, driven by industry leaders investing in eco-friendly propulsion technologies and advancements in materials science. The country's strategic role in European aerospace collaboration further strengthens its global competitiveness.

Competitive Landscape

The global aircraft engines market is highly consolidated, with a few major players controlling a significant share of global output. GE Aviation, a subsidiary of General Electric Company, stands out as a market leader due to its technological excellence and broad product portfolio across turboprop and jet engines. Other prominent players include Rolls-Royce Holdings Plc, Safran SA, and CFM International SA, all of whom focus on introducing and modernizing advanced engine technologies to enhance their offerings.

Key Industry Developments

- In April 2024, Rolls-Royce has launched a flight test campaign for its advanced aero engine, the Pearl 10X, marking a significant milestone in the company's business aviation venture. The engine, chosen by Dassault exclusively for its Falcon 10X, is designed to operate seamlessly with 100% Sustainable Aviation Fuel (SAF), reducing carbon emissions.

- In January 2024, Homegrown low-cost airline Akasa Airlines signed an agreement with CFM International to purchase more than 300 Leap-1B engines to power 150 aircraft. The contract also included a spare engine and service contract. The agreement was signed during French President Emmanuel Macron's state visit to India.

Companies Covered in Aircraft Engines Market

- Advanced Atomization Technologies Inc.

- Enjet Aero

- Engine Alliance

- Safran Group

- Pratt & Whitney

- Rolls-Royce

- MTU Aero Engines AG

- CFM International

- General Electric Company

- ITP Aero

- New Hampshire Ball Bearing (MinebeaMitsumi Aerospace)

Frequently Asked Questions

The market is set to reach US$ 76.8 Bn in 2025.

Rising air travel demand and fleet expansion & modernization are the major growth drivers.

The industry is estimated to rise at a CAGR of 10.8% through 2032.

Rising Demand for Energy-Efficient Cooling Solutions, and Integration with Renewable Energy Sources are the key market opportunities.

Advanced Atomization Technologies Inc., Enjet Aero, Engine Alliance, and Rolls-Royce are a few leading players.