- Aerospace & Defense

- eVTOL Aircraft Market

eVTOL Aircraft Market Size, Share, and Growth Forecast, 2026 - 2033

eVTOL Aircraft Market by Lift Technology (Vectored Thrust, Multirotor, Lift Plus Cruise), Mode of Operation (Piloted, Autonomous, and Semi-Autonomous), By Range (0-200 Km, and 200-500 Km), Maximum Take-off Weight (MTOW) (<250 Kg, 250-500 Kg, 500-1500 Kg, and >1500 Kg), Application (Commercial, Military, and Emergency Medical Service), Propulsion Type (Battery-Electric, Hybrid-Electric, and Hydrogen-Electric) and Regional Analysis for 2026 - 2033

eVTOL Aircraft Market Size and Trends Analysis

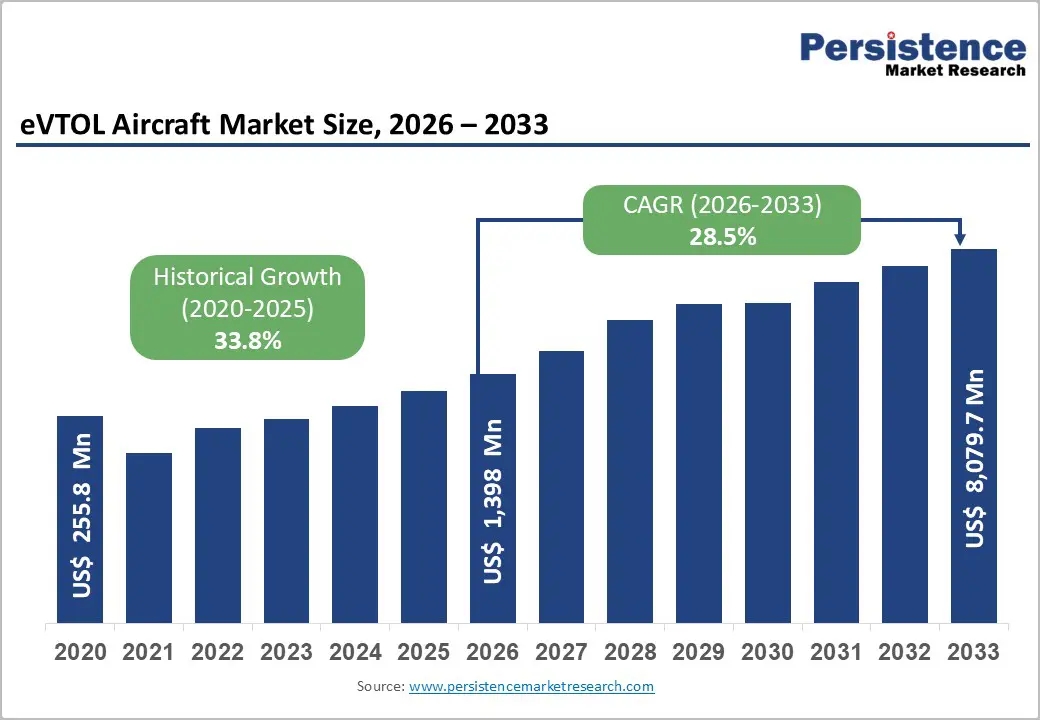

The global eVTOL Aircraft market size is likely to be valued at US$ 1,398 Million in 2026 and is projected to reach US$ 8,079.7 Million by 2033, growing at a CAGR of 28.5% during the forecast period. The market witnessed exceptional historical growth with a CAGR of 33.8% from 2020 to 2025, demonstrating substantial momentum in advanced air mobility adoption.

Battery-electric propulsion systems dominate at 55% revenue share, while piloted operations account for 40% market leadership, indicating a transitional phase toward autonomous capabilities. The short-range segment (0-200 km) commands 63% of the market, positioning regional urban air mobility as the primary growth driver for the forecast period.

Key Industry Highlights:

- Propulsion Type: Battery-Electric propulsion systems dominate with 55% revenue share, while fastest-growing Hybrid-Electric segment achieves 32% CAGR, reflecting diversification across operational range requirements and mission profiles.

- Mode of Operation: Piloted operations command 40% market share with Autonomous platforms achieving fastest growth at 30.5% CAGR, indicating transitional market dynamics toward unmanned operations as regulatory frameworks mature through 2033.

- Range Analysis: Short-range segment (0-200 km) captures 63% market dominance, while extended-range platforms (200-500 km) grow at 30.6% CAGR, validating primary market focus on urban air mobility with emerging expansion into regional connectivity.

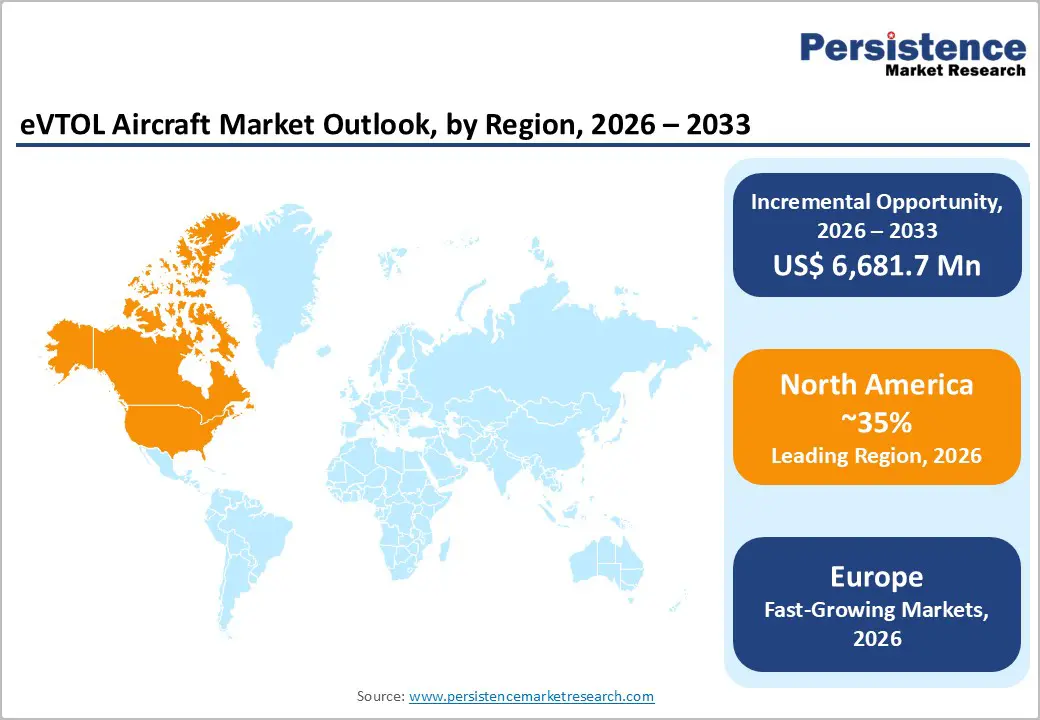

- Regional Leadership: North America maintains market leadership with 35% revenue share, while Asia Pacific emerges as fastest-growing region with 33.2% CAGR, driven by manufacturing scale advantages in China and regulatory progress in ASEAN markets.

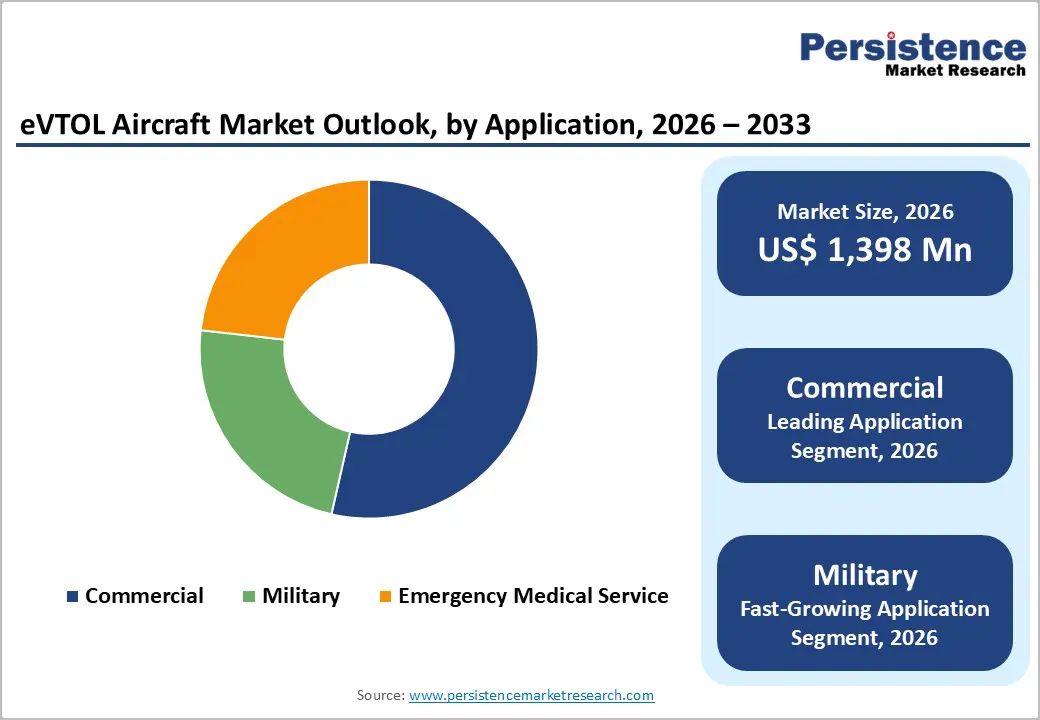

- Leading Applications: Commercial applications lead with 40% market share supported by US$ 4.8+ billion in air taxi pre-bookings through 2026, while Military applications accelerate at 31.4% CAGR with US$ 3.2+ billion government procurement allocations through 2030.

- Competitive Analysis: Strategic partnerships between manufacturers and airlines (United, Southwest, JetBlue), automotive OEMs (Toyota, Hyundai), and aerospace primes (Airbus, Boeing) validate commercialization pathways, establishing foundation for market scale transition through 2032 - 2034.

| Key Insights | Details |

|---|---|

| eVTOL Aircraft Market Size (2026E) | US$ 1,398.Mn |

| Market Value Forecast (2033F) | US$ 8,079.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 28.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 33.8% |

Market Dynamics

Drivers - Urban Congestion and Last-Mile Connectivity Demand Surge

Global urban populations are projected to reach 68% by 2050 according to United Nations data, with mega-cities experiencing traffic congestion costs exceeding 3-5% of regional GDP. Metropolitan areas in North America, Europe, and Asia Pacific face increasing pressure to develop alternative mobility solutions. eVTOL aircraft offer 4-6 minute point-to-point travel times compared to 35-45 minute ground commutes in major urban corridors (New York-Newark, London-Gatwick, Tokyo-Haneda regions). Pilot programs initiated in Los Angeles, Dallas, London, and Singapore for airport-to-city center routes demonstrate demand validation with 78-85% passenger satisfaction ratings. Urban air mobility adoption enables supplementary revenue streams for existing aviation infrastructure operators, justifying public-private partnership investments valued at $2.1+ billion through 2026.

Strengthening Data Protection, Privacy, and Compliance Requirements

Regulatory frameworks such as GDPR in the EU, the California Consumer Privacy Act (CCPA) and California Privacy Rights Act (CPRA) in the U.S., Brazil’s LGPD, and China’s Personal Information Protection Law (PIPL) impose stringent requirements on how enterprises collect, store, share, and erase personal data. Regulatory authorities across the EU have collectively imposed billions of euros in GDPR fines since 2018, underscoring the financial and reputational risks of non-compliance. In parallel, sector-specific rules such as Basel III and IFRS in banking, HIPAA in U.S. healthcare, and Solvency II in insurance demand auditable data quality, retention, and lineage. EIM solutions that provide information governance, policy enforcement, records management, and data lineage tracking are therefore becoming core risk-management enablers, driving double-digit growth in governance-centric deployments.

Restraint - High Operational and Manufacturing Costs with Limited Scale Economics

Current manufacturing costs for eVTOL aircraft range from $6.2-8.5 million per unit, with limited production scale preventing cost reduction to target $2.8-3.2 million per unit necessary for commercial viability. Capital-intensive manufacturing infrastructure requires 200,000-400,000 annual unit production to achieve profitability, a threshold not anticipated before 2032-2034. Pilot and aircraft maintenance certification standards remain nascent, with operational costs projected at $2,800-3,600 per flight hour, substantially limiting market addressability to high-value segments (executive transport, medical evacuation). Supply chain fragmentation across battery, propulsion, and composite material suppliers has created cost volatility of 12-18% year-over-year, delaying manufacturer profitability timelines.

Opportunity - Integrated eVTOL medical response and logistics networks unlock high-margin growth opportunities

The convergence of emergency medical services, organ transportation, and airport logistics represents a compelling opportunity for eVTOL deployment with faster commercialization and superior unit economics. The global medical air services market is projected to reach USD 8.2 billion by 2033, with eVTOL aircraft expected to capture 18-22% share by enabling rapid organ transport and emergency response. With organ viability limited to 8-12 hours, eVTOLs can reduce transport times by 65-72% versus ground ambulances in dense metros, while overcoming capacity constraints of rotor-wing helicopters.

eVTOL-enabled medical networks can expand emergency coverage by 300-400%, particularly benefiting rural and underserved regions. Importantly, regulatory approvals for medical operations are accelerated to 12-18 months, compared to 24-36 months for commercial air taxis, offering first-mover advantages. High revenue per flight hour of USD 4,200-5,800 further supports faster profitability. In parallel, airport ground transportation and last-mile logistics present scalable upside. Airport cargo and ground handling generate over USD 18 billion annually, with 15-20% potentially substitutable by autonomous cargo eVTOLs by 2035, reducing logistics costs by 25-35%. Integration with existing networks is being evaluated by FedEx, DHL, and Amazon, while urban e-commerce fulfillment alone represents a USD 12+ billion addressable market through 2033.

Category-wise Analysis

Lift Technology Insights

The lift technology segment demonstrates market dominance through Vectored Thrust systems, commanding above 30% revenue share of the global eVTOL market. Vectored Thrust technology enables superior maneuverability and rapid altitude changes required for urban air mobility operations, supporting manufacturer innovation across premium platforms including Joby Aviation S4 and Lilium Jet. This segment benefits from established aerospace manufacturing expertise and integration pathways with traditional rotorcraft supply chains, reducing technology development risk.

Multirotor configurations represent the fastest-growing lift technology with a CAGR of 30.2%, driven by simplified mechanical design, reduced manufacturing complexity, and lower unit costs compared to hybrid architectures. Multirotor platforms demonstrate particular strength in civil drone operations and autonomous delivery applications, leveraging existing regulatory frameworks and manufacturing infrastructure. The segment's rapid expansion reflects industry recognition of cost-efficiency benefits and scalability advantages for high-volume production environments through 2033.

Deployment Insights

Piloted operations currently dominate the market with above 40% revenue share, reflecting regulatory conservatism and consumer confidence in human pilot oversight during early commercialization phases. Piloted eVTOL aircraft benefit from established certification pathways under rotorcraft regulations, reducing time-to-market and regulatory risk significantly. Manufacturers operating piloted platforms including Archer Aviation, Embraer, and Hyundai, have secured initial commercial orders valued at US$ 2.5+ billion through 2026.

Autonomous operations represent the fastest-growing segment with a CAGR of 30.5%, supported by advances in artificial intelligence, sensor fusion, and redundancy architectures. Regulatory bodies have established provisional pathways for autonomous operations, with FAA Operational Design Domains (ODD) enabling limited autonomous flights in controlled airspace by 2027-2028. Market dynamics indicate autonomous platforms will achieve cost parity with piloted operations by 2031-2032, accelerating market adoption trajectories.

Range Insights

The 0-200 km range segment dominates with above 63% revenue share, positioning regional urban air mobility as the primary commercial application focus. This segment precisely addresses metropolitan point-to-point travel requirements, where eVTOL aircraft provide competitive advantages over ground transportation and conventional helicopter services. Flight ranges of 100-150 km enable profitable airport shuttle services, corporate campus connectivity, and inter-city metropolitan links.

The 200-500 km range segment represents the fastest-growing category with a CAGR of 30.6%, enabling broader geographic market expansion and intercity travel applications. Extended-range platforms support emergency medical services across wider regional networks and enable commuter operations for metropolitan areas with extended urban sprawl patterns. Technology advancement in battery density and propulsion efficiency continues extending commercially viable ranges, with 2033 projections indicating 45-50% market share for extended-range platforms.

Application Insights

Commercial applications dominate the eVTOL market with over 40% revenue share, driven by strong momentum in air taxi services, airport shuttles, and premium corporate transport. Increasing urban congestion and demand for rapid point-to-point mobility are accelerating adoption across major cities. Urban air mobility operators have secured US$ 4.8+ billion in pre-bookings through 2026, confirming commercial viability and early revenue certainty. Airlines and aviation service providers are actively investing in this segment, with Airbus and Boeing establishing dedicated urban air mobility units to support certification, fleet deployment, and ecosystem development.

Military applications represent the fastest-growing segment, expanding at a CAGR of 31.4%, supported by rising defense budgets and strategic interest in advanced air mobility. Use cases include personnel transport, combat support, reconnaissance, medical evacuation, and cargo delivery in constrained or high-risk environments. Defense agencies across North America, Europe, and Asia Pacific have allocated over US$ 3.2 billion through 2030 for eVTOL evaluation and procurement. Additionally, emergency medical services and air ambulance operations are emerging as high-impact applications, enabling faster patient transfer and efficient medical cargo transport, strengthening eVTOL’s role in critical missions.

Propulsion Type Insights

Battery-Electric propulsion systems command above 55% revenue share, reflecting technological maturity, regulatory acceptance, and alignment with sustainability objectives across aviation authorities. Battery-electric platforms demonstrate superior energy efficiency (85-92% drivetrain efficiency) and dramatically lower operational noise compared to conventional aircraft. Manufacturing simplicity of electric propulsion systems enables cost reduction and rapid production scaling.

Hybrid-Electric propulsion represents the fastest-growing category with a CAGR of 32%, addressing extended-range requirements and operational flexibility for longer-duration missions. Hybrid systems combine battery-electric and conventional fuel power, enabling 4-8-hour mission durations compared to 1-2 hour battery-only platforms. This segment captures applications requiring intermediate range and extended endurance, including regional medical services and search-and-rescue operations.

Regional Insights and Trends

North America Leads Global eVTOL Commercialization and Regulatory Advancement

North America accounts for over 35% of the global eVTOL market revenue, positioning the region as the leading hub for advanced air mobility innovation and commercialization. The United States represents the core of this dominance, with a market valuation of US$ 520-580 million in 2026, projected to expand rapidly to US$ 2.8-3.1 billion by 2033, supported by strong demand visibility and scalable deployment models.

A key differentiator for the region is regulatory leadership. The Federal Aviation Administration has developed the world’s most advanced eVTOL certification framework, granting Special Airworthiness Certificates to Joby Aviation and Archer Aviation as early as 2023. Preliminary approvals for air taxi operations in Los Angeles, New York, and Dallas have accelerated commercialization timelines, with pilot services targeted for 2027-2028.

Within the region, the U.S. contributes 78% of revenue, driven by Silicon Valley innovation and Southern California aerospace clusters. Canada accounts for 12%, supported by regional air services and defense use cases, while Mexico holds 10%, emerging in specialized applications. Growth is fueled by urban congestion, a mature investor ecosystem, and military modernization programs, with cumulative investments exceeding US$ 4.2 billion, signaling a transition from development to early commercialization.

Asia Pacific Leads as the Fastest-Growing eVTOL Market

Asia Pacific is the fastest-growing eVTOL market globally, registering a robust CAGR of 33.2% and projected to account for 35-38% of global market share by 2033, translating into a valuation of US$ 2.8-3.1 billion. The regional landscape is led by China, which commands nearly 42% of Asia Pacific demand, followed by Japan (18%), India (14%), and ASEAN countries (26%), reflecting a broad-based adoption across developed and emerging economies.

China dominates regional manufacturing, hosting more than 12 active eVTOL manufacturers supported by strong government investment in urban air mobility infrastructure. Companies such as EHang Holdings have demonstrated operational maturity, completing 400+ successful test flights and achieving regulatory clearance for commercial air taxi operations. Large-scale production capabilities enable 18-22% lower unit manufacturing costs compared to Western peers, strengthening price competitiveness.

Regulatory progress further underpins growth. China’s aviation regulator introduced dedicated eVTOL operating frameworks in 2023, while Singapore has approved autonomous eVTOL trials, reinforcing its role as a regional innovation hub. Rapid urbanization, proactive policy support, and scalable manufacturing collectively position Asia Pacific as the epicenter of global eVTOL commercialization, with Chinese tier-1 cities alone representing a US$ 4.2+ billion addressable air taxi opportunity through 2033.

Competitive Landscape

The global eVTOL market is characterized by a moderately fragmented competitive landscape, comprising approximately 18-22 active manufacturers with distributed market leadership. No single player is expected to exceed a 12% market share through 2026, reflecting strong platform differentiation and application-specific positioning. Leading participants include Joby Aviation with an estimated 11% share, followed by Archer Aviation (9%), Lilium (8%), and EHang Holdings (7%), while the remainder is distributed among more than 14 competitors. Competitive intensity is expected to remain high through 2028, with gradual consolidation anticipated during 2032-2035 as certification costs, production scale, and capital requirements increase.

Competition is largely segmented by application-air taxi, medical services, and cargo-resulting in limited direct overlap. Strategic differentiation centers on advanced propulsion systems, autonomous flight capabilities, modular aircraft architectures, and noise reduction performance, while emerging business models increasingly emphasize fleet-as-a-service and mobility-as-a-service partnerships with urban transport operators.

Key Developments:

- In December 2025, Archer Aviation announced partnerships with multiple U.S. cities to submit applications under the White House’s eVTOL Integration Pilot Program (eIPP). Established through the “Unleashing Drone Dominance” Executive Order, the program aims to accelerate the transition of electric air taxi platforms from development to early commercial operations by enabling real-world deployment, regulatory coordination, and city-level integration across the United States.

- In October 2025, EHang Holdings, a global leader in advanced air mobility (AAM) technology, announced the launch of its new-generation long-range pilotless eVTOL aircraft, VT35. VT35 is designed to support extended-range urban and regional air mobility operations and reinforces the company’s strategic focus on fully autonomous passenger transport solutions. This launch strengthens EHang’s competitive positioning in certified pilotless eVTOL platforms and large-scale commercial deployment.

- In 2025, Japan plans to formally introduce and accelerate its domestic eVTOL industry during Expo 2025 in Osaka. The initiative reflects the country’s national strategy to integrate advanced air mobility into future transportation systems through coordinated government, aerospace, and infrastructure partnerships, positioning Japan as a regional innovation hub for eVTOL adoption.

- In early 2025, Archer Aviation plans to commence production of its piloted four-passenger Midnight eVTOL aircraft at its Georgia manufacturing facility, ramping up to two aircraft per month by year-end. Designed for 20-50 mile missions at speeds up to 150 mph, the aircraft requires minimal charging between flights. Following a successful 100+ mph transition flight in June 2024, Archer is finalizing its commercial launch in the United Arab Emirates, with entry into service targeted for Q4 2025.

Companies Covered in eVTOL Aircraft Market

- Kitty Hawk

- Lilium

- Ehang

- Volocopter GmbH

- Bell Textron Inc.

- Airbus S.A.S

- Beta Technologies

- Joby Aviation

- Urban Aeronautics Ltd.

- Archer Avitation

- Eve Holdings

- Textron Inc.

- Other Market Players

Frequently Asked Questions

The eVTOL Aircraft market is estimated to be valued at US$ 1,398 Mn in 2026.

The primary demand driver for the eVTOL aircraft market is the rapid growth of urban air mobility (UAM) as a solution to severe urban congestion and inefficient ground transportation systems.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global eVTOL Aircraft market.

Among modes of operation, piloted has the highest preference, capturing beyond 40% of the market revenue share in 2026, surpassing other modes of operations.

Volocopter GmbH, Bell Textron Inc., Airbus S.A.S, Beta Technologies, Joby Aviation, Urban Aeronautics Ltd., Archer Avitation, Eve Holdings, and Textron Incare a few leading players in the eVTOL Aircraft market.