- Aerospace & Defense

- Commercial Aircraft Landing Gear Market

Commercial Aircraft Landing Gear Market Size, Share, and Growth Forecast, 2026 - 2033

Commercial Aircraft Landing Gear Market by Gear Type (Main Landing Gear and Nose Landing Gear), By Aircraft Type (Narrow-Body, Wide-Body, Regional Jet and Others), by Component Outlook (Landing Gear Steering System, Wheel & Brake System, Actuation System and Others) and Regional Analysis for 2026 - 2033

Commercial Aircraft Landing Gear Market Size and Trends Analysis

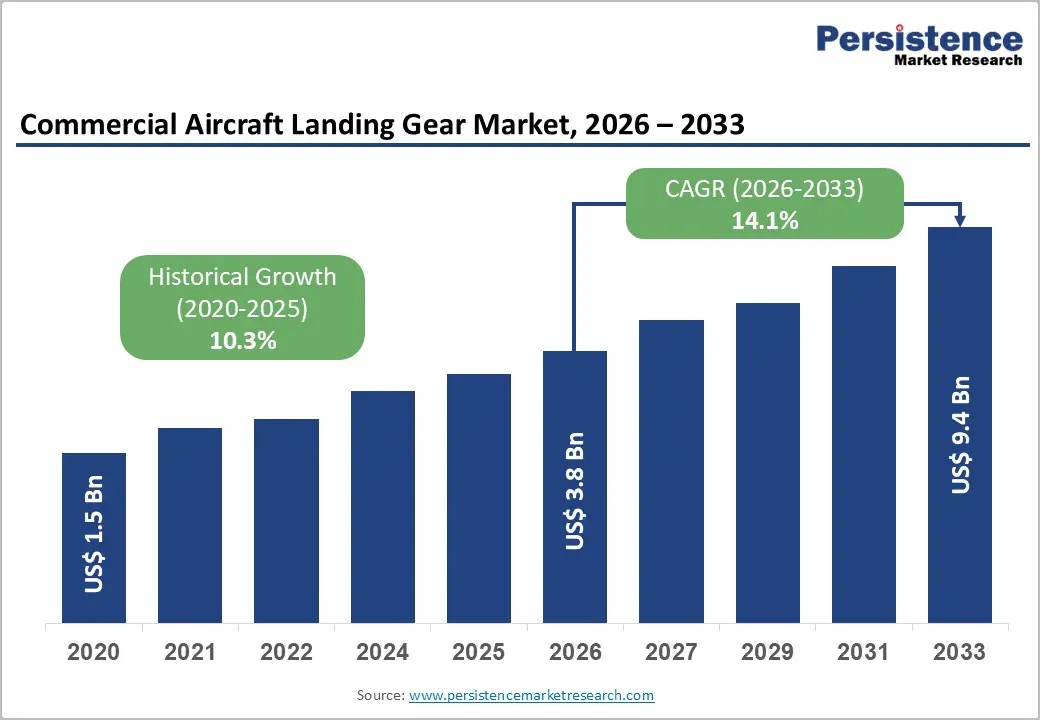

The global commercial aircraft landing gear market size was valued at US$ 3.8 billion in 2026 and is projected to reach US$ 9.4 billion by 2033, growing at a CAGR of 14.1% between 2026 and 2033.

This expansion reflects accelerating commercial aircraft production, reaching 11,000+ deliveries through 2033; systematic fleet modernization across major carriers; and advanced technology integration, including electromechanical actuation systems that reduce hydraulic dependency.

Key Industry Highlights:

- Leading Gear Type: Main landing gears dominate with 65.6% market share through structural load-bearing requirements; Nose landing gears represent fastest-growing at 16% CAGR, driven by electric steering system integration and retrofit modernization.

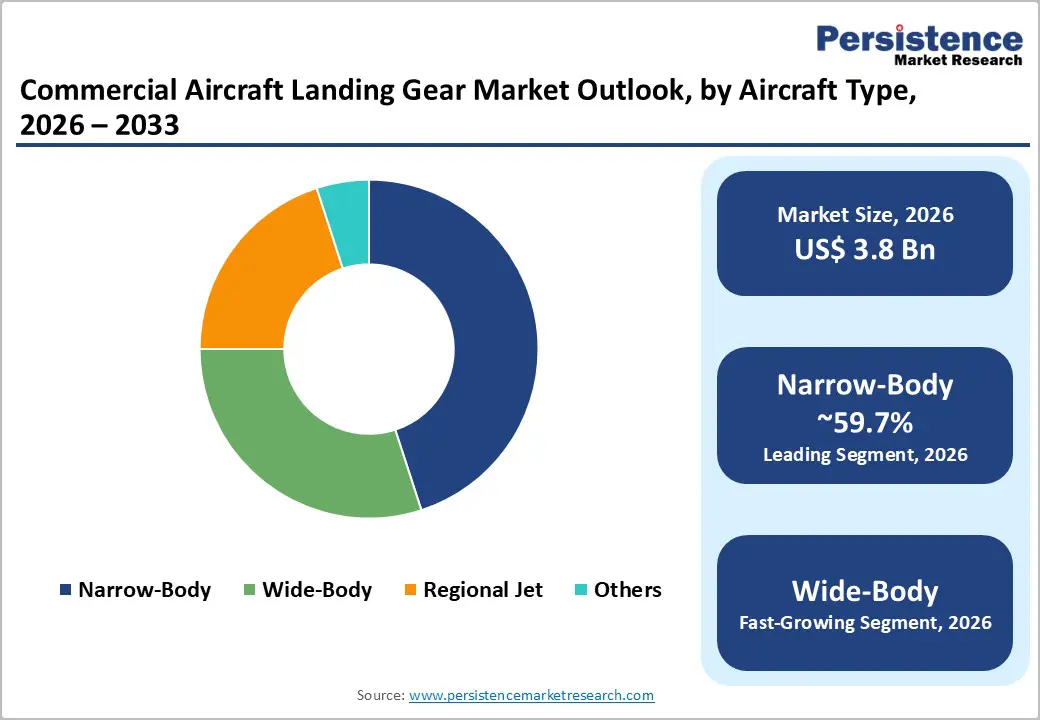

- Dominant Aircraft Type: Narrow-body aircraft maintain 59.7% market share through production volume dominance; Wide-body aircraft represent fastest-growing at 18% CAGR, driven by emerging market long-haul expansion and aircraft replacement cycles.

- Leading Component: Landing gear steering systems command 41.3% component market share through cost and technology concentration; Actuation systems represent the fastest growing at 17% CAGR, driven by electric system transition and weight reduction advantages.

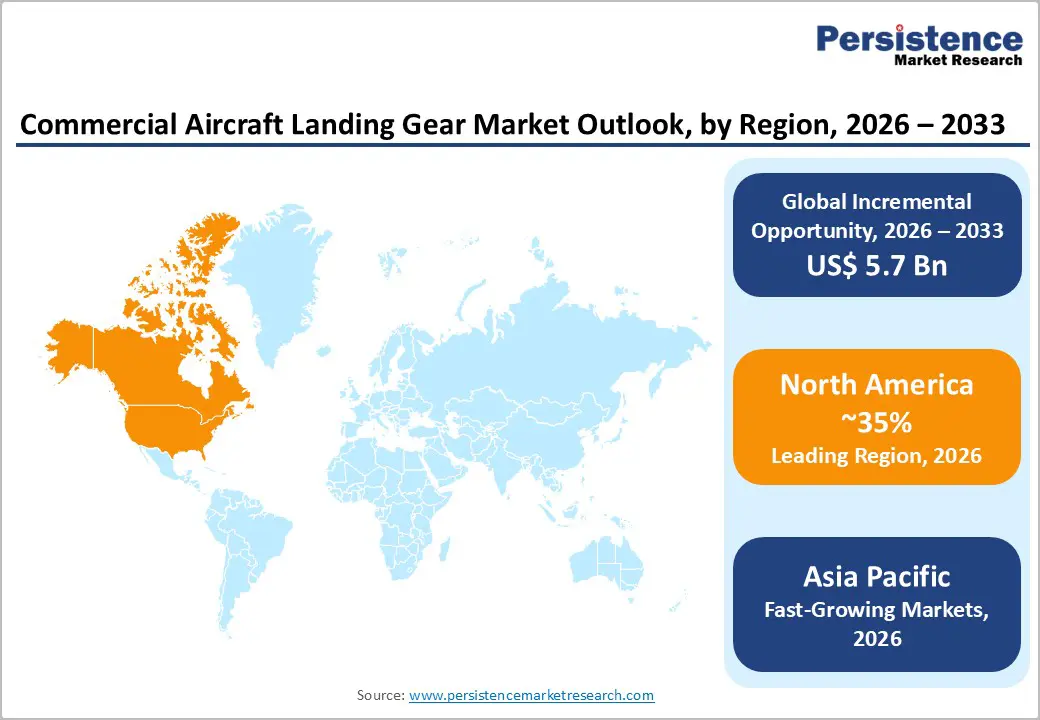

- Regional Market Dominance and Growth: North America maintains 35% global market share driven by Boeing production and major carrier concentration; Asia-Pacific demonstrates the fastest regional growth at 19% CAGR, expanding from 22% current share to 30% by 2033.

- Technology and Market Innovation Momentum: Top 10 suppliers control 70% market share (Safran, Liebherr, Eaton, Collins leading); Electric actuation system advancements achieving 25%+ weight reduction; Lightweight material integration reducing landing gear weight by 15-20%; Predictive maintenance systems extending service intervals by 20-30%.

| Global Market Attributes | Key Insights |

|---|---|

| Commercial Aircraft Landing Gear Market Size (2026E) | US$ 3.8 Bn |

| Market Value Forecast (2033F) | US$ 9.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.1% |

| Historical Market Growth (CAGR 2020 to 2024) | 10.3% |

Market Dynamics

Growth Drivers

Global Commercial Aircraft Production Expansion and Fleet Modernization

Aircraft delivery acceleration, with Boeing 737 MAX and 787 Dreamliner combined with Airbus A320neo family and A350 achieving production rates exceeding 2,000+ aircraft annually through 2033, establishing proportionate landing gear demand. Global commercial fleet expansion, with the global commercial aircraft fleet projected to surpass 46,000 aircraft by 2035, creating sustained retrofit and replacement demand, drives proportionate component requirements. Regional jet proliferation, with regional carriers operating 4,000+ aircraft and expanding routes with 70-100 seat aircraft, establishing distributed landing gear demand across aircraft classes.

Low-cost carrier dominance, with carriers operating 50%+ of the global commercial fleet and prioritizing cost-efficient narrow-body aircraft, establishes a foundation for volume production. Aircraft replacement cycles, with 20-30-year aircraft operational lifespans and 15-20% annual fleet utilization growth requiring proportionate landing gear maintenance and replacement, establish recurring demand.

Advanced Technology Integration and Electro-Mechanical System Adoption

Electro-mechanical actuation advancement, with electric landing gear actuation systems replacing hydraulic alternatives and reducing weight by 15-20% while improving reliability and reducing maintenance requirements by 10-12%, justifies technology transition. Predictive maintenance system deployment, with integrated sensors enabling real-time health monitoring and reducing unplanned downtime by 30-40% through condition-based maintenance optimization, establishes operational value. Lightweight material adoption, with titanium alloys and carbon-composite integration, reducing landing gear weight by 15% and improving aircraft fuel efficiency and operating economics, drives specification advancement.

Smart landing gear technology, with integrated diagnostics and health-monitoring systems that extend service intervals by 20-30% and reduce maintenance costs by 15%, establishes owner-operator economics. Advanced brake systems, with electric carbon-brake technology that provides superior fade resistance and eliminates hydraulic fluid dependency, improve safety and reduce environmental concerns.

Market Restraints

High Development and Certification Costs Limiting Innovation Entry

Certification expenses, with FAA and EASA landing gear certification consuming 3-5 years and US$ 50M-150M per new design, limit new manufacturer participation. Component qualification requirements, with OEM suppliers requiring extensive testing and validation increasing development costs 20-30% versus standard component manufacturing. Supply-chain concentration, with major aircraft OEMs (Boeing, Airbus) controlling supplier selection and limiting competitive dynamics, reducing pricing pressure and innovation motivation.

Manufacturing capital intensity, with landing gear production requiring specialized facilities and precision tooling representing substantial capital barriers limiting entrant participation. Technology licensing constraints, with established suppliers controlling proprietary actuation technologies and creating licensing barriers protecting incumbent market positions. Retrofit compatibility requirements, with existing aircraft fleet requiring backward-compatible solutions limiting revolutionary technology adoption.

Supply Chain Constraints and Geopolitical Dependencies

Specialty material sourcing: with titanium alloy and advanced composite material supply constraints, lead-time risks and cost volatility create production schedule risks. Manufacturing bottlenecks, with landing gear production requiring specialized capabilities concentrated in a few suppliers, creating single-source risk for aircraft OEMs. Geopolitical tensions, with semiconductor supply uncertainties affecting the availability of electromechanical actuation systems and creating sourcing risk for manufacturers.

Labor skill constraints: specialized aerospace manufacturing requires experienced technicians and faces skill shortages in developed markets, limiting production scaling. Global supply-chain complexity, with landing gear systems comprising 500+ components from distributed suppliers, creates coordination challenges and extends lead times. Quality assurance requirements, with aerospace safety standards requiring comprehensive testing and documentation extending production timelines 10-20%.

Market Opportunities

Wide-Body Aircraft Market Expansion and Long-Haul Route Growth

Long-haul aircraft demand, with emerging market airlines (China, India, Southeast Asia) expanding international route networks requiring wide-body aircraft with advanced landing gear systems, establish growth opportunity. Aircraft replacement cycles, with 15-20-year-old wide-body aircraft retirement and replacement creating demand for modern landing gear systems with advanced technology integration, establish a retrofit foundation. Cargo aircraft conversion, with passenger-to-freight aircraft conversion programs accelerating post-pandemic, is creating demand for landing gear systems supporting increased weight loads. Regional hub development, with emerging markets establishing international hub airports requiring modern landing gear infrastructure investment, drives proportionate demand.

Electric and Autonomous Aircraft Development Programs

Electric aircraft development, with aviation authorities and manufacturers investing in electric aircraft programs that require innovative landing gear designs optimized for electric propulsion, is driving emerging demand. Urban Air Mobility (UAM) expansion, with electric vertical takeoff and landing (eVTOL) aircraft development, creates specialized landing gear requirements for novel aircraft configurations and establishes a new market segment. Autonomous flight programs, with unmanned aircraft system (UAS) development for commercial applications requiring landing gear systems that support autonomous operations, are establishing an emerging segment. Hydrogen-powered aircraft development, with next-generation aircraft exploring hydrogen propulsion requiring specialized landing-gear integration with alternative-fuel systems, establishes an emerging technology opportunity.

Segmentation analysis

Gear Type Analysis

The main landing gear holds 65.6% market share, driven by its critical load-bearing role and high system complexity. It supports over 70% of aircraft weight during taxi, takeoff, and landing, necessitating robust structures, multi-wheel assemblies, advanced shock absorption, and integrated braking systems. These factors significantly increase unit cost and technology content. Main landing gear also dominates the aftermarket, accounting for the highest replacement frequency in aircraft MRO cycles. Standardization by Boeing and Airbus across aircraft families ensures consistent OEM volumes, while stringent fatigue testing exceeding 30,000 flight hours creates high entry barriers.

The nose landing gear is the fastest-growing segment (16% CAGR through 2033), driven by advanced steering systems, electrification reducing weight by 20%, taxi automation integration, and retrofit demand in narrow-body fleets, which are increasing system value and driving upgrade-driven growth.

Aircraft Type Analysis

The narrow-body aircraft segment holds 59.7% market share, driven by its dominance in global fleet composition and production volumes. Narrow-body aircraft account for over 65% of the in-service fleet and more than 80% of new deliveries, supported by strong demand for short- and medium-haul connectivity. Low-cost carriers, operating over half of the narrow-body fleets, reinforce high-volume, cost-efficient aircraft deployment. Sustained production backlogs for the Boeing 737 and Airbus A320 families exceeding 8,000 aircraft ensure long-term OEM demand, while a large installed base supports steady aftermarket requirements.

The wide-body aircraft segment is the fastest growing (15-18% CAGR through 2033), driven by emerging-market long-haul expansion, fleet replacement cycles, cargo conversion growth, and higher-value landing gear systems on next-generation wide-body platforms.

Component Analysis

Landing gear steering systems account for 41.3% of component market share, driven by high cost, system complexity, and growing technology content. Advanced steering assemblies account for 35% of total landing gear cost and integrate actuators, sensors, and control electronics. Enhanced control precision reduces ground handling incidents by 20%, justifying premium OEM specifications. Increasing adoption of electronically controlled steering enables automated taxiing and tighter integration with fly-by-wire systems, while retrofit programs for narrow-body fleets prioritize steering electrification. automtive Steering systems dominate nose landing gear value, reinforcing revenue concentration and market leadership.

Actuation systems are the fastest-growing component segment (17% CAGR through 2033), driven by the shift from hydraulic to electro-mechanical systems. Electric actuation delivers 16% weight reduction, 25% lower maintenance costs, smart diagnostics for predictive maintenance, and standardization across next-generation aircraft platforms, accelerating adoption.

Regional market insights

North America Market Analysis

North America commands approximately 35% of the global commercial aircraft landing gear market share, valued at approximately US$ 2.3 billion in 2026, with projections approaching US$ 3.5 billion by 2033. The United States represents a dominant regional market contributor, accounting for 85% of the North American market value, driven by Boeing production dominance and major carrier concentration.

Aircraft OEM concentration, with Boeing 737 MAX and 787 production lines establishing dominant landing gear requirements and specification leadership. Major carrier procurement, with American Airlines, United, Delta, and Southwest operating 3,000+ narrow-body and 1,000+ wide-body aircraft requiring proportionate maintenance and replacement demand. Military aircraft programs, with F-35 fighter jet production and KC-46 tanker development, are creating defense landing applications to complement commercial demand.

Europe Market Analysis

Europe accounts for approximately 28% of the global commercial aircraft landing gear market, valued at approximately US$ 1.6 billion in 2026. Germany, France, the United Kingdom, and Spain collectively represent 75% of the European market value, reflecting Airbus's production concentration and specialized supplier ecosystems.

Airbus production dominance, with Airbus A320 family and A350 wide-body production establishing European landing gear demand and specification standards. Supplier specialization, with German landing gear manufacturers (Liebherr-Aerospace, Eaton) and French manufacturers (Safran) maintaining technology leadership and specialized capabilities. Regulatory framework alignment with the EASA certification authority and CS-23/CS-25 standards, which establish European certification pathways. Regional aircraft integration, with European regional jet manufacturers (ATR) and emerging aircraft programs creating specialized landing gear requirements.

Asia-Pacific Market Analysis

Asia-Pacific region demonstrates robust growth dynamics, commanding approximately 25% market share with projections increasing to 30% by 2033. The region valued at approximately US$ 1.2 billion in 2026 is expected to reach US$ 2.8 billion by 2033, representing the fastest-growing regional market with an estimated CAGR of 18%.

Commercial aircraft demand acceleration, with China, India, and Southeast Asia experiencing rapid air travel growth and airline expansion driving aircraft procurement. Domestic aircraft programs, with COMAC C919 and ARJ21 production, are establishing landing gear demand and creating localization opportunities for regional suppliers. Fleet modernization acceleration, with Asian carriers upgrading aging fleets with modern fuel-efficient aircraft driving retrofit component demand.

Commercial Aircraft Landing Gear Market Competitive Landscape

The competitive landscape of the global commercial aircraft landing gear market is characterized by the presence of key players such as Safran Landing Systems, Collins Aerospace, and Liebherr-Aerospace. These companies dominate the market through advanced technologies and established relationships with leading aircraft manufacturers. Their extensive product portfolios and experience in the aerospace sector enable them to cater to diverse customer needs across different aircraft types.

Manufacturers are actively pursuing strategic collaborations, mergers, and investments in research and development to enhance market growth. For instance, companies are focusing on developing lightweight landing gear solutions and automated manufacturing processes to improve efficiency and reduce turnaround times. This strategic emphasis not only strengthens their market position but also aligns with the growing demand for fuel-efficient and reliable aircraft systems.

Key Industry Developments

- In February 2024, Liebherr Aerospace announced signed a long-term service contract with Japan Airlines (JAL) for the overhaul of aircraft landing systems. Liebherr would offer its extensive service and product portfolio for the maintenance, repair, and overhaul of landing systems for JAL’s operational fleet.

- In October 2023, Safran Landing Systems announced that the company signed a five-year contract with airline company Wizz Air, under which the company would be provided with MRO operations for 57 aircraft.

Companies Covered in Commercial Aircraft Landing Gear Market

- Safran Landing Systems

- Collins Aerospace

- Liebherr-Aerospace

- Héroux-Devtek

- Honeywell International

- Magellan Aerospace

- GKN Aerospace

- AAR Corp.

- Triumph Group

- Sumitomo Precision Products Co., Ltd.

- CIRCOR Aerospace

- Revima Group

- Others Key Players

Frequently Asked Questions

The Commercial Aircraft Landing Gear market is estimated to be valued at US$ 3.8 Bn in 2026.

The key demand driver for the Commercial Aircraft Landing Gear market is the global expansion and modernization of commercial aircraft fleets driven by rising air passenger traffic.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Commercial Aircraft Landing Gear market.

Among the Aircraft Type, Narrow-Body holds the highest preference, capturing beyond 59.7% of the market revenue share in 2026, surpassing other Application type.

The key players in Commercial Aircraft Landing Gear are Safran Landing Systems, Collins Aerospace, Liebherr-Aerospace, Héroux-Devtek and Honeywell International.