- Aerospace & Defense

- Trainer Aircraft Market

Trainer Aircraft Market Size, Share, and Growth Forecast, 2026 - 2033

Trainer Aircraft Market by Wing Type (Fixed, Rotary, Unmanned), Application (Military Training, Commercial Training, Private Training Providers, Original Equipment Manufacturers (OEMs)), Technology (Conventional, Advanced, Intermediate), and Regional Analysis for 2026-2033

Trainer Aircraft Market Share and Trends Analysis

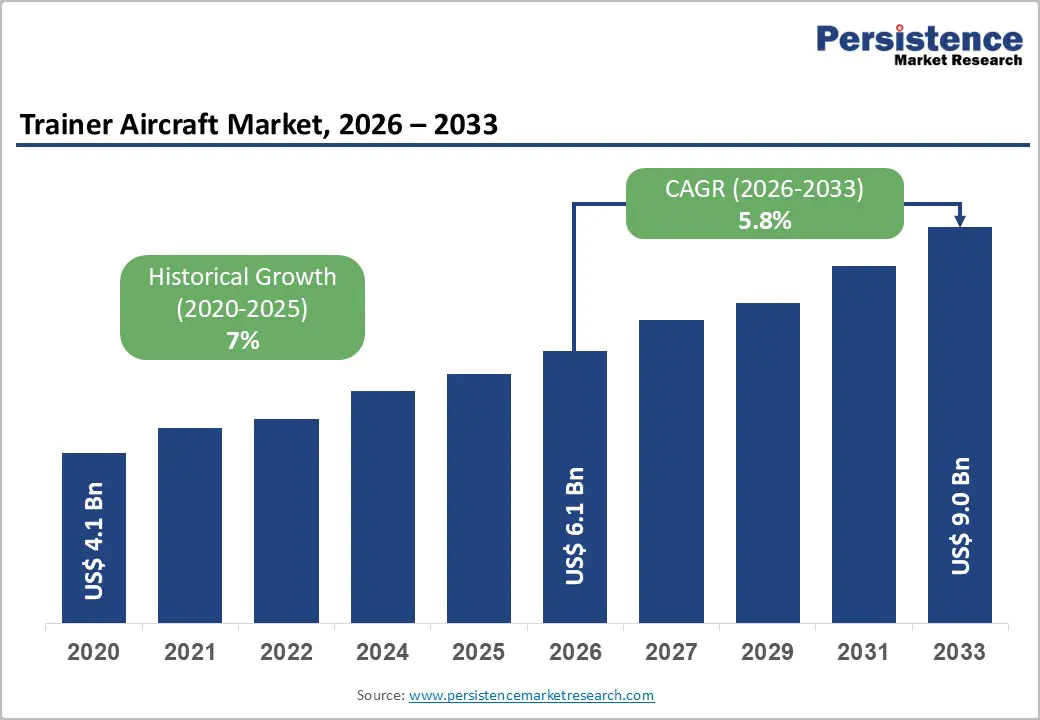

The global trainer aircraft market size is likely to be valued at US$ 6.1 billion in 2026, and is projected to reach US$ 9.0 billion by 2033, growing at a CAGR of 5.8% during the forecast period 2026−2033. This growth trajectory is primarily driven by escalating defense modernization programs across emerging economies, increasing pilot training requirements for commercial aviation expansion, and technological advancements in simulation-integrated training platforms. The market demonstrates robust momentum as air forces worldwide replace aging training fleets while commercial aviation sectors address pilot shortage challenges through enhanced training infrastructure investments.

Key Industry Highlights

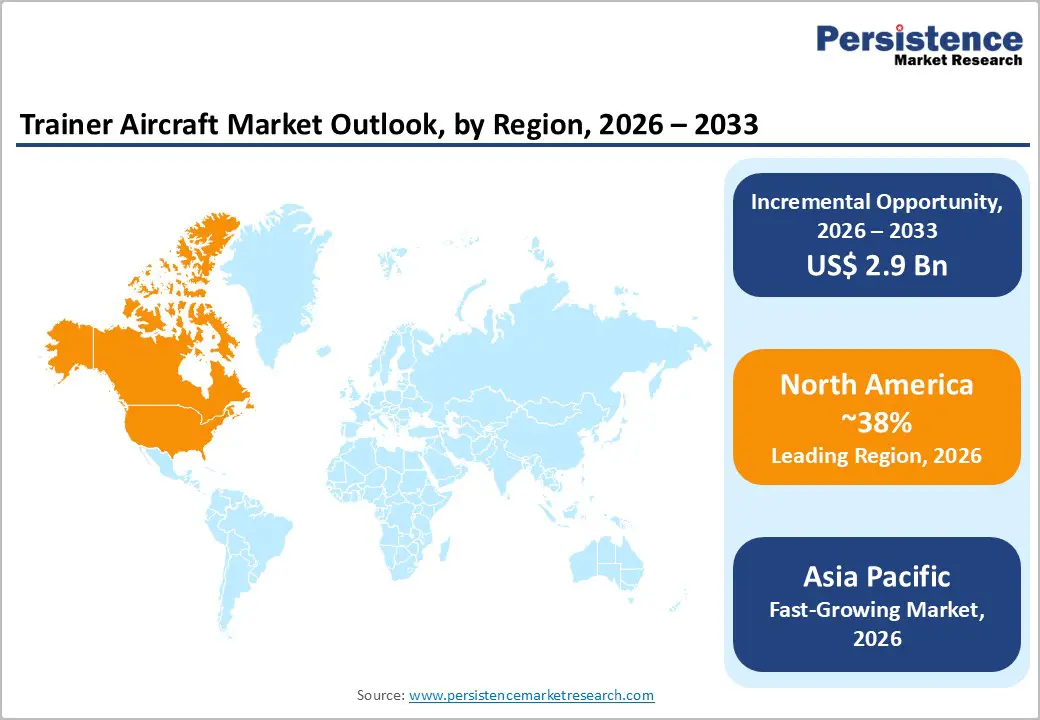

- Dominant Region: North America is expected to command about 38% of the market share in 2026, supported by the scale and sophistication of the United States military and commercial training ecosystems.

- Fastest-growing Market: The Asia Pacific market is set to be the fastest-growing due to rapid defense modernization, expanding commercial aviation, and deliberate industrial policy support.

- Leading & Fastest-growing Wing Types: Fixed wings are slated to dominate with an estimated share of 70% in 2026, while rotary-wing aircraft are likely to be the fastest-growing during the 2026-2033 forecast period.

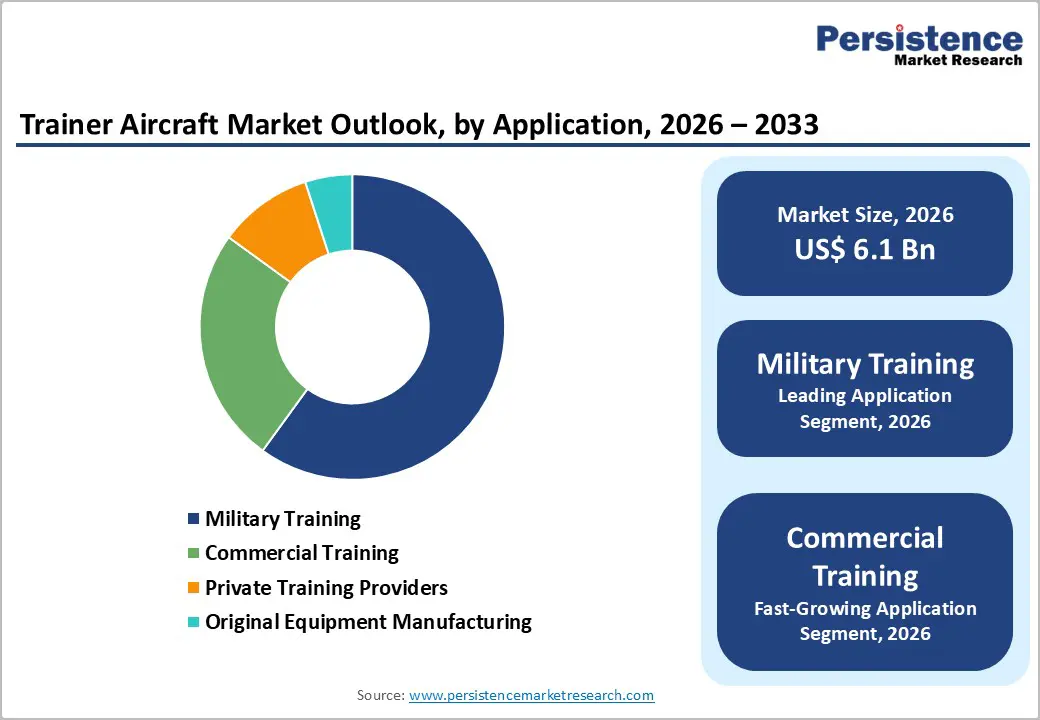

- Leading & Fastest-growing Application: Military training is expected to command about 60% revenue share in 2026, with commercial training registering the highest CAGR over the 2026-2033 forecast period.

- December 2025: Coimbatore-based Sakthi Group entered the aviation sector, partnering with Austria’s Diamond Aircraft, to set up India’s first private trainer aircraft manufacturing facility in Tirupur with an investment of INR 750 crore.

| Key Insights | Details |

|---|---|

| Trainer Aircraft Market Size (2026E) | US$ 6.1 Bn |

| Market Value Forecast (2033F) | US$ 9.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Defense Expenditure and Military Modernization Programs

Military spending across countries has continued to rise as governments reassess security priorities and invest in modern force structures across land, air, and maritime domains. For example, according to findings of the Stockholm International Peace Research Institute (SIPRI), global military expenditure hit a record US$ 2,718 billion in 2024, up 9.4% from 2023, with the military burden at 2.5% of world GDP and 7.1% of government spending. Defense ministries in Asia Pacific and beyond increasingly view pilot training as a strategic capability rather than a support function, aligning training aircraft renewal with broader combat aircraft procurement cycles. Air forces now favour advanced trainer platforms that replicate frontline cockpits and mission systems, because this alignment shortens conversion timelines and reduces the risk of skill gaps as new fighters enter service. In this context, training fleets have become central to long-term readiness planning, sustainment strategies, and doctrine development for complex, multi-domain operations.

Trainer aircraft programs provide both capability enhancement and cost-management opportunities. Modern training ecosystems, which combine aircraft with sophisticated simulators and data-driven performance assessment tools, enable air forces to shift a greater share of instruction into synthetic environments while preserving essential live-flying experience. This approach can help defense stakeholders optimize budgets, extend the service life of high-value combat platforms, and build more resilient training pipelines that adapt to evolving mission profiles. Governments and industry partners that align trainer procurement with integrated training system investments are better positioned to scale pilot output, maintain operational standards, and support future technology transitions in areas such as unmanned teaming and advanced electronic warfare.

Regulatory Certification Complexity and Compliance Requirements

The trainer aircraft market growth faces increasingly stringent certification and airworthiness requirements across major jurisdictions, which lengthen development cycles and add complexity to program management. Military authorities such as the United States Air Force Materiel Command and comparable organizations in Europe and Asia apply rigorous testing, evaluation, and documentation standards before approving aircraft for training operations. Civil regulators such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) also require comprehensive evidence that new trainer types meet safety, performance, and operational suitability criteria for their intended roles. These layered approval processes often run in parallel but follow different procedures, creating coordination challenges for program teams and slowing time to market.

The most significant impact arises from the combined burden of testing, validation, and configuration management requirements across multiple target markets. Divergent certification expectations in areas such as avionics architecture, flight control laws, and mission systems integration can drive the need for platform-specific variants, which reduces standardization and weakens economies of scale in both production and through-life support. This environment tends to favour established incumbents with dedicated certification engineering teams, while new entrants must commit substantial upfront investment before they can secure meaningful contracts. From a strategic standpoint, manufacturers that deliberately design certificate-ready architectures and engage early with both military and civil regulators are better positioned to mitigate risk, shorten approval timelines, and bring innovative training solutions to market more efficiently.

Emerging Markets and Regional Training Hub Development

Developing economies across Asia Pacific, the Middle East, and Latin America are emerging as important growth corridors for the trainer aircraft market, as governments build indigenous aerospace capabilities and invest in purpose-built training ecosystems. Many of these countries are shifting from reliance on foreign training pipelines to establishing national or regional academies that train pilots, instructors, and maintenance personnel closer to their operational environments. This shift strengthens control over training doctrine, improves alignment with local mission profiles, and reduces long-term dependence on external service providers. At the same time, the creation of dedicated training centers enables defense ministries and civil aviation authorities to structure capability development in stages, starting with basic training and then progressing to advanced and multi-role training as experience and resources increase.

These trends create opportunities for partnership-based market entry models rather than relying solely on straightforward platform sales. International cooperation can take forms such as structured technology transfer, offset programs tied to industrial and workforce development, and local final assembly or subsystem production aligned with national priorities. Manufacturers that approach these markets with flexible architectures, modular training solutions, and a clear commitment to co-investing in local capabilities are better positioned to secure durable roles in national training plans. Governments can, in turn, use these collaborations to growth of sustainable aerospace clusters, strengthen sovereign control over critical training infrastructure, and progressively integrate domestic firms into global supply chains for both trainer and frontline aircraft programs.

Category-wise Analysis

Wing Type Insights

Fixed wings are slated to maintain a dominant position in the market, with an estimated 2026 share hovering around 70% due to intensifying military and commercial pilot training programs, where these aircraft are used extensively. These platforms range from basic propeller-driven trainers such as the Beechcraft T-6 Texan II to advanced jet trainers such as the BAE Systems Hawk and the Leonardo M-346, supporting progressive skill development from initial flight training through advanced tactical instruction. Fixed-wing trainers also benefit from mature training curricula, broad global operational use, and strong compatibility with existing infrastructure and maintenance ecosystems. Many major air forces maintain sizeable fleets of fixed-wing trainers, which underscores the persistent reliance on these aircraft to meet core training requirements.

The rotary-wing segment is likely to be the fastest-growing during the 2026-2033 forecast period, driven by expanding helicopter operations in military aviation, emergency medical services, and various commercial missions. The increasing complexity of modern helicopter systems and the rising demand for rotary-wing pilots, particularly in Asia-Pacific markets, are encouraging air operators and defense organizations to invest in dedicated helicopter training fleets. Platforms such as the Leonardo TH-119 and the Airbus H125, when configured for training, provide sophisticated solutions that address the specific handling, systems management, and operational skills required for rotary-wing aviation.

Application Insights

Military training is anticipated to hold an estimated 60% of the trainer aircraft market revenue share in 2026, reinforced by continuous defense force pilot training requirements, tactical mission preparation, and aircrew currency maintenance programs. Military trainers serve diverse roles from basic flight screening through advanced mission training, with air forces typically operating multiple trainer types to support progressive training pipelines. The U.S., China, Russia, and India collectively operate over 3,000 military training aircraft, representing substantial procurement and replacement demand. Military applications demand platforms capable of simulating operational aircraft characteristics while providing robust performance, reliability, and maintainability in demanding training environments.

Commercial training is expected to be the fastest-growing segment over the 2026-2033 forecast period, propelled by unprecedented pilot demand from expanding airline networks, particularly in Asia-Pacific and Middle Eastern markets. Commercial pilot training increasingly prioritizes cost-efficiency, safety, and compliance with international certification standards, which drives demand for aircraft optimized for intensive, high-frequency training operations. Training organizations seek platforms that offer reliable performance, predictable operating costs, and robust support ecosystems to sustain high utilization without compromising safety outcomes.

Technology Insights

The conventional segment is poised to lead with an approximate 55% market share in 2026, aided by platforms with mechanical flight controls, analog or basic digital avionics, and established training methodologies. These aircraft remain widely used in basic and primary training roles, where the development of fundamental airmanship skills takes precedence over exposure to advanced onboard systems. Their key advantages include lower acquisition cost, simpler maintenance requirements, and high levels of instructor familiarity, all of which support predictable and efficient training delivery. Many air forces and training organizations continue to employ conventional trainers for initial screening and early flight training phases, where their cost-effectiveness and reliability offer a strong value proposition for building core piloting competencies.

Advanced technology is anticipated to be the fastest-growing segment between 2026 and 2033. These platforms closely mirror the cockpit layouts and human–machine interfaces of contemporary operational aircraft, which supports more effective transition training and allows instructors to integrate data recording, performance analytics, and adaptive training techniques into daily syllabi. Advanced trainers such as the T-7A Red Hawk and the KAI T-50 Golden Eagle typically incorporate mission computers, tactical data links, and weapon system simulation capabilities that help prepare pilots for the demands of fourth- and fifth-generation fighter operations.

Regional Insights

North America Trainer Aircraft Market Trends

North America is set to command a significant portion of the trainer aircraft market share at approximately 38% in 2026, underpinned by the scale and sophistication of the United States military and commercial training ecosystems. The United States shapes regional demand through major programs such as the T-7A Red Hawk and a dense network of military and civil training organizations, while Canada reinforces this role through initiatives such as the Future Aircrew Training program and other multinational training arrangements. Together, these efforts sustain ongoing investment in airframes, simulators, and integrated training systems, and they help define global expectations for safety, interoperability, and training doctrine.

North America serves both as a reference market and as a proving ground for advanced trainer concepts, with procurement choices in the region frequently influencing adoption decisions in allied air forces. Ongoing commercial pilot demand supports a broad ecosystem of flight schools and university aviation programs that favour reliable, cost-efficient trainers connected to modern simulation architectures. North American manufacturers and service providers benefit from this environment through sustained demand for integrated solutions that combine aircraft, simulators, and data-driven training services into a single offering. The strategic implication is clear: success in this region depends on demonstrating lifecycle value, meeting regulatory expectations, and achieving seamless integration across live and synthetic training environments, rather than focusing on airframe performance alone.

Europe Trainer Aircraft Market Trends

Europe plays a pivotal role in the market for trainer aircraft, supported by a high concentration of advanced air forces and a strong indigenous aerospace industrial base. Germany, the United Kingdom, France, and Spain shape much of the regional demand through combinations of national training fleets, multinational cooperation frameworks, and long-standing commitments to North Atlantic Treaty Organization (NATO) missions. The United Kingdom’s Military Flying Training System illustrates a comprehensive approach to outsourcing and modernizing flight training across multiple aircraft types, while the German Air Force uses bilateral and multilateral arrangements to optimize training capacity across borders.

The regulatory and policy environment in Europe reinforces this ecosystem by combining common civil certification rules with nationally led defense procurement decisions. The EASA provides harmonized certification frameworks that support cross-border use of aircraft and simulators, which simplifies multinational training arrangements and joint procurement initiatives. At the same time, defense ministries retain distinct acquisition processes, creating space for collaborative projects supported by instruments such as the European Defense Fund, particularly for future trainer platforms and advanced training technologies.

Asia Pacific Trainer Aircraft Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing trainer aircraft market through 2033, underpinned by rapid defense modernization, expanding commercial aviation, and deliberate industrial policy support. China, Japan, India, and member states of the ASEAN increasingly treat pilot training as a core enabler of airpower, building training fleets and infrastructure that span the full spectrum from basic propeller aircraft to advanced jet trainers. China’s People’s Liberation Army Air Force prioritizes indigenous programs such as the Hongdu JL-10, while Japan’s Air Self-Defense Force places strong emphasis on advanced jet instruction supported by tightly structured training syllabi.

India’s requirements extend across basic, intermediate, and advanced training categories, with domestic programs such as the Hindustan Aeronautics Limited (HAL) HTT-40 complemented by prospective foreign procurements to address long-standing capability gaps. Defense customers in the region typically seek solutions that replace ageing fleets, align cockpit and systems design with modern combat aircraft, and scale to support high pilot throughput, while civil operators focus on cost-efficient aircraft that integrate smoothly with simulator networks and competency-based training frameworks. As a result, the competitive landscape combines established global manufacturers operating through joint ventures and licensing arrangements with emerging regional players that compete for both domestic and export opportunities.

Competitive Landscape

The global trainer aircraft market structure is remaining moderately concentrated, with a small group of established aerospace manufacturers continuing to hold a significant share of total demand. Leading companies such as The Boeing Company, Lockheed Martin Corporation, Textron Aviation Inc., Leonardo S.p.A., and BAE Systems plc are collectively accounting for an estimated 55-60% of market revenue. Their positions are being reinforced through long-standing defense relationships, proven delivery track records, and integrated training ecosystems that combine aircraft platforms with simulators, logistics, and long-term support. Market competition is therefore evolving around differentiated value propositions rather than pure unit sales, particularly as defense customers are prioritizing training effectiveness and operational readiness.

Competitive dynamics are continuing to diverge across trainer categories based on mission complexity and customer requirements. Advanced trainer platforms that are supporting tactical and lead-in fighter training are competing on performance attributes, avionics sophistication, and the ability to replicate frontline combat environments. At the other end of the spectrum, basic and primary trainer programs are emphasizing lifecycle affordability, operational simplicity, and ease of maintenance to address budget constraints and high flight-hour utilization. From a consultative perspective, manufacturers that are aligning product offerings with end-user training doctrines, total cost of ownership expectations, and long-term fleet scalability are positioning themselves to secure repeat contracts and program extensions over the forecast period.

Key Industry Developments

- In January 2026, the U.S. Air Force inducted its first T-7A Red Hawk advanced jet trainer at Joint Base San Antonio–Randolph, beginning the replacement of the aging T-38 Talon and marking a shift to digital-first pilot training tailored to modern, data-intensive air combat.

- In November 2025, India unveiled the indigenous Hansa-3 NG, its first all-composite two-seat pilot trainer aircraft at CSIR-NAL Bengaluru. The aircraft has been designed to meet demand for 30,000 pilots over two decades, with Pioneer Clean Amps building a INR 150-crore facility in Andhra Pradesh for 100 units annually.

- In July 2025, Spain allocated €1.37 billion (about US$ 1.6 billion) for a new-generation advanced trainer aircraft program centered on acquiring Turkish Aerospace Industries’ Hurjet. The plan foresees the first delivery of six aircraft by 2028 and a total of 18 in service by 2029, with funding sized to ultimately support 28–30 aircraft and incorporating Spanish-specific modifications to the design.

Companies Covered in Trainer Aircraft Market

- The Boeing Company

- Lockheed Martin Corporation

- Textron Aviation Inc.

- Leonardo S.p.A.

- BAE Systems plc

- Saab AB

- Korea Aerospace Industries Ltd.

- Pilatus Aircraft Ltd.

- Hindustan Aeronautics Limited

- Embraer S.A.

- CAE Inc.

- Diamond Aircraft Industries

- Dassault Aviation

- Turkish Aerospace Industries

- Hongdu Aviation Industry Group

Frequently Asked Questions

The global trainer aircraft market is projected to reach US$ 6.1 billion in 2026.

Rising demand for pilot training, expanding defense budgets, and replacement of ageing trainers, supported by advances in avionics and simulation technology, are driving the market.

The market is poised to witness a CAGR of 5.8% from 2026 to 2033.

Key opportunities lie in multi-role/armed trainers, VR/AR-integrated and simulator-centric training solutions, and new demand from emerging markets upgrading their air forces and civil aviation fleets.

The Boeing Company, Lockheed Martin Corporation, Textron Aviation Inc., Leonardo S.p.A., and BAE Systems plc are some of the key players in the market.