- Sensors & Controls

- U.S. Emergency Management Services Market

U.S. Emergency Management Services Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Emergency Management Services Market by Component (Services, Systems, and Solutions), Deployment Mode (On-premises and Cloud-based), Industry Vertical (Government and Defense, Energy and Utilities, Healthcare, IT and Telecom, Transportation and Logistics, Manufacturing, and Others), and Regional Analysis, 2026 - 2033

U.S. Emergency Management Services Market Size and Share Analysis

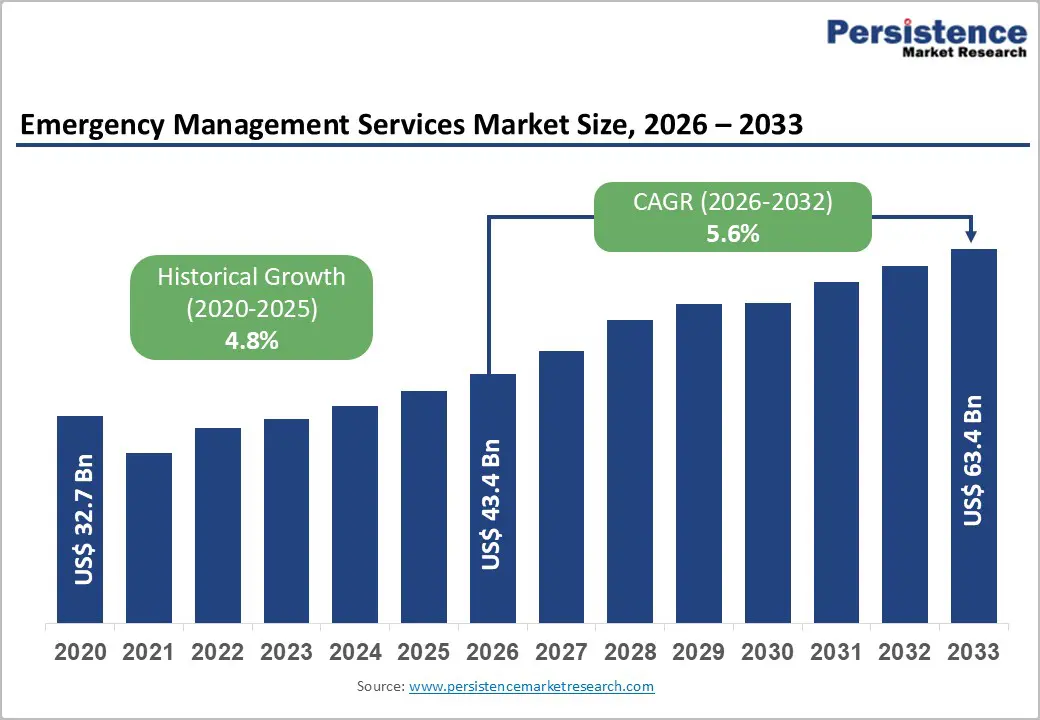

The U.S. Emergency Management Services market size was valued at US$ 43.3 billion in 2026 and is projected to reach US$ 63.4 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. The market expansion is primarily driven by the escalating frequency of climate-related natural disasters, heightened government investment in emergency preparedness infrastructure, and rapid adoption of advanced technologies, including artificial intelligence and cloud-based solutions.

Key Market Highlights

- Leading Region: The Northeast represents a mature and regulation-driven EMS market, supported by high population density, advanced hospital networks, and strong state-level emergency preparedness frameworks. States such as New York, Massachusetts, and Pennsylvania emphasize rapid response times, advanced life support (ALS) services, and integration with trauma centers.

- Fastest Growing Region: The Southwest represents a fast-evolving EMS market, influenced by rapid urbanization, cross-border mobility, and extreme climate conditions. States like Arizona, Nevada, and New Mexico face rising emergency demand due to heat-related illnesses, highway accidents, and population inflows into metropolitan areas such as Phoenix and Las Vegas.

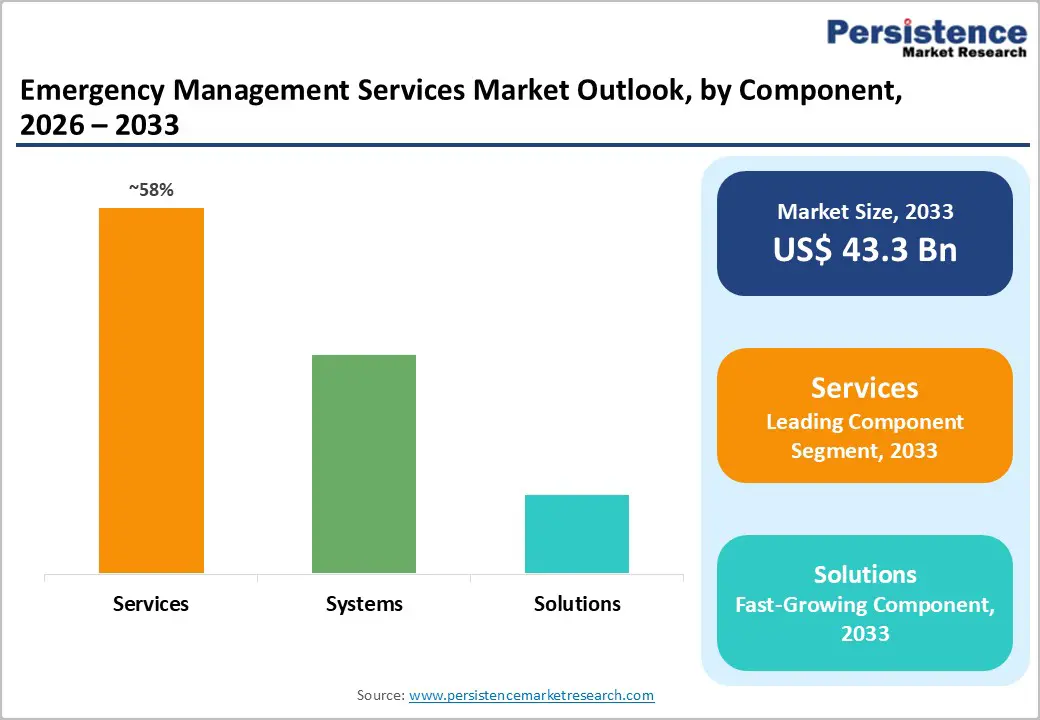

- Dominant Component: Services segment commands approximately 55% market share, encompassing consulting, emergency operations support, training and simulation, and maintenance services, reflecting the professional services intensity required for effective emergency management system implementation and operation across organizations.

- Growing Deployment Mode: Cloud-based deployment is the fastest-growing segment, with a 12% CAGR, driven by superior scalability, reduced capital expenditure, enhanced disaster recovery capabilities, and accelerated deployment timelines, and momentum in healthcare and government modernization initiatives.

- Key Market Opportunity: AI-based decision support systems integration presents a substantial growth opportunity, with the healthcare sector projected at 8.4% CAGR through 2033, driven by predictive disaster modeling, optimized resource allocation, real-time threat detection, and advanced analytics enabling proactive emergency management and improved response outcomes.

| Key Insights | Details |

|---|---|

|

U.S. Emergency Management Services Market Size (2026E) |

US$ 43.3 Bn |

|

Market Value Forecast (2033F) |

US$ 63.4 Bn |

|

Projected Growth CAGR(2026-2033) |

5.6% |

|

Historical Market Growth (2020-2025) |

4.8% |

Market Dynamics

Market Growth Drivers

Escalating Natural Disasters and Climate-Related Emergencies

The frequency and intensity of natural disasters in the United States have increased substantially, creating an urgent demand for comprehensive emergency management services. Analysis from the National Center for Environmental Information reveals that between 2015 and 2025, the nation experienced an average of 18 billion-dollar disaster events annually, compared with just 3 per year in 1980. The economic burden has escalated dramatically, with disaster recovery costs reaching $153 billion in the last five years alone. This represents a fourfold increase from the $89.2 billion spent during 2010-2019.

The rising costs and frequency of these events have compelled federal, state, and local governments to prioritize investment in advanced emergency operations centers, early warning systems, and coordination platforms. Additionally, the concentration of population in coastal and urban areas, with over 200 million Americans living in metropolitan zones and 87 million along U.S. coastlines, amplifies the potential impact of disasters, necessitating sophisticated emergency management infrastructure to protect lives and critical infrastructure.

Government Funding and Regulatory Mandates

Federal and state governments have substantially increased funding for emergency preparedness and response capabilities. The FEMA Disaster Relief Fund received historically elevated appropriations, with $57.9 billion allocated for fiscal year 2025. Beyond disaster relief, FEMA released nearly $3.5 billion in preparedness grants to states, local governments, tribes, and territories to strengthen emergency management infrastructure. These investments support workforce development, technology procurement, and system upgrades across agencies.

The Emergency Preparedness Rule, implemented by CMS, requires all healthcare providers and suppliers to maintain comprehensive emergency preparedness plans, driving adoption of emergency management systems across the healthcare sector. Similarly, the National Response Framework and National Incident Management System (NIMS) established standardized protocols and requirements that necessitate technological solutions for multi-agency coordination, resource tracking, and real-time information sharing, thereby expanding the addressable market for emergency management services and solutions.

Market Restraints

Budget Constraints and Funding Uncertainty

Despite increased federal allocations, many states and local jurisdictions face persistent budget constraints that limit their ability to invest in advanced emergency management systems. A significant proportion of state emergency management agencies depend heavily on federal funding, with Wyoming reporting over 90% dependence on federal grants, Texas approximately 75%, and North Carolina approximately 82%. The uncertainty surrounding federal funding availability creates operational challenges for emergency managers who struggle to maintain staff, conduct training programs, and sustain preparedness activities.

Furthermore, budget reductions in certain grant programs, such as the State Homeland Security Grant Program, have already impacted state allocations, with North Carolina experiencing a reduction from $10.6 million to $8.5 million between fiscal years. This funding volatility discourages long-term capital investments in technology infrastructure and creates barriers to market expansion, particularly in smaller municipalities and rural areas with limited independent budgets.

Integration Complexity and Legacy System Constraints

The proliferation of legacy emergency management systems and disparate communication platforms creates significant technical and operational barriers to deploying modern solutions. Many emergency response organizations operate with outdated software, communication networks, and hardware that lack interoperability with contemporary cloud-based and AI-driven platforms. Integration of new emergency management systems with existing databases, radio systems, and surveillance infrastructure requires substantial technical expertise and extended implementation timelines, increasing the total cost of ownership. Research indicates that approximately 50% of organizations cite legacy systems and software incompatibility as major obstacles to adopting cloud-based solutions.

The complexity of integrating multiple vendors' systems while ensuring compliance with federal standards such as NIMS and FedRAMP security requirements creates deployment hurdles that slow market adoption. Additionally, concerns about data security, cybersecurity vulnerabilities, and regulatory compliance with frameworks such as HIPAA and CMMC further constrain organizations' willingness to migrate critical emergency management functions to cloud-based platforms.

Market Opportunities

Accelerated Cloud-Based Emergency Management Adoption

Cloud-based emergency management solutions represent a significant growth opportunity as organizations recognize the advantages of scalability, cost efficiency, and accessibility. The cloud-based disaster recovery market in the United States was valued at $7.6 billion in 2025 and is projected to advance at a remarkable CAGR of 15.01% through 2033, reaching $17.59 billion. Cloud-based emergency management software specifically is experiencing robust growth at 12% CAGR, driven by the preference for scalable infrastructure, reduced capital expenditure, and rapid deployment capabilities. Organizations are increasingly leveraging cloud platforms to centralize command centers, improve inter-agency coordination, and enable real-time situational awareness without the burden of maintaining on-premises infrastructure.

Leading solutions providers such as Everbridge, WebEOC, and Veoci have demonstrated significant traction in deploying cloud-based emergency operations centers that integrate GIS capabilities, plan development tools, and customizable workflows. The adoption trajectory indicates that 51% of IT professionals expect their organizations to be "mostly in the cloud" within five years, presenting substantial market expansion opportunities for vendors offering compliant, user-friendly cloud-based emergency management platforms.

Integration of Artificial Intelligence and Advanced Analytics

The integration of artificial intelligence, machine learning, and advanced analytics into emergency management operations presents a transformative growth opportunity. Research institutions and government agencies are increasingly developing AI-based decision-support systems to enhance prediction, coordination of responses, and resource allocation during emergencies. AI technologies enable predictive modeling of natural disasters, analysis of real-time sensor data from IoT devices, and optimization of emergency vehicle routing to minimize response times. The healthcare sector is anticipated to experience the fastest growth, registering a CAGR of 8.44% through 2032, driven by hospitals and medical facilities adopting

AI-enhanced emergency preparedness platforms. Tools such as HealthMap utilize AI to scan social media and health data sources for early warnings of disease outbreaks, while natural language processing algorithms analyze emergency calls and incident reports to detect emerging threats. Federal agencies are investing in the development of specialized AI tools, such as Hazard Helper, to help emergency managers efficiently create and update hazard mitigation plans. This technological shift creates substantial opportunities for vendors to develop next-generation AI-driven decision support systems, predictive analytics platforms, and automated dispatch optimization solutions that enhance both preparedness and response capabilities.

Category-wise Insights

Component Services Analysis

The Services segment represents the dominant component within the market, commanding approximately 55% of total market share. This segment encompasses consulting services, emergency operations support, training and simulation services, and support and maintenance services. The dominance of services reflects the critical need for specialized expertise in designing emergency management frameworks tailored to organizational risk profiles, implementing complex systems integration, and providing ongoing operational support. Organizations increasingly recognize that technology deployment must be accompanied by comprehensive training programs to ensure personnel competency, regular system optimization, and continuous improvement of emergency response procedures.

Emergency management agencies contract with specialized service providers for expertise in implementing the incident command system, conducting tabletop exercises, and conducting full-scale drill simulations to validate response procedures. The Systems segment, including web-based emergency management systems, emergency and mass notification systems, surveillance systems, traffic management systems, and mobile emergency communication systems, comprises approximately 45% of the market. Within systems, web-based emergency management platforms such as WebEOC and Veoci have gained significant adoption due to their integrated capabilities for real-time situational awareness, multi-agency coordination, and customizable workflows. The services-dominant market structure reflects the professional services intensity of emergency management implementation and the ongoing requirement for expert support to maintain system effectiveness.

Deployment Mode Analysis

The Cloud-based deployment mode represents the fastest-growing segment, currently accounting for approximately 40% of the market and expanding at a 12% CAGR. Cloud deployment offers significant advantages, including scalability to accommodate varying organizational needs, reduced capital expenditure compared to on-premises infrastructure, faster time-to-value through reduced implementation cycles, and built-in disaster recovery capabilities. The Federal government's cloud-first strategy and initiatives, such as FedRAMP authorization, have accelerated cloud adoption across emergency management agencies seeking compliant, secure cloud environments. Healthcare organizations and transportation agencies are particularly driving cloud adoption due to the need for rapid scalability during surge events and the desire to reduce IT operational burden.

The On-premises deployment mode maintains approximately 60% market share, particularly among government agencies requiring stringent data control, offline operational capability, and integration with legacy communication systems. Federal, state, and local government agencies continue to prefer on-premises solutions for mission-critical emergency operations centers where data sovereignty and offline reliability are paramount. The market exhibits a bifurcated structure with mature organizations increasingly transitioning toward hybrid approaches combining on-premises core systems with cloud-based analytics and collaboration capabilities, creating growth opportunities across both deployment modes.

Industry Vertical Analysis

The Government and Defense vertical dominates, with approximately 45% market share, driven by substantial investments by federal, state, and local government agencies in emergency preparedness infrastructure. FEMA, the Department of Homeland Security, state emergency management agencies, and law enforcement organizations are the primary end-users in this vertical. Government agencies require integrated solutions combining emergency operations centers, GIS mapping capabilities, surveillance systems, and multi-agency coordination platforms. The Healthcare vertical represents the fastest-growing segment with a projected CAGR of 8.44% through 2032, driven by regulatory mandates and the critical importance of healthcare facility resilience. Hospitals and healthcare systems require emergency management solutions addressing pandemic preparedness, mass casualty incident response, supply chain management, and facility continuity planning.

The COVID-19 pandemic accelerated investment in the healthcare sector in emergency preparedness technologies, and institutions such as Johns Hopkins Medicine, Cleveland Clinic, and Children's Hospital of Philadelphia have deployed cloud-based disaster recovery systems to ensure uninterrupted patient care. The Energy and Utilities vertical represents approximately 20% of the market, requiring specialized solutions for managing critical infrastructure protection, rapid response to service disruptions, and coordination with emergency services. Transportation and logistics organizations, IT and telecommunications companies, and manufacturing facilities represent additional vertical markets with distinct emergency management requirements driving diversified solution demand.

Competitive Landscape for the Emergency Management Services Market

The U.S. Emergency Management Services market exhibits moderate consolidation with a mix of large-scale technology vendors, specialized emergency management solution providers, and consulting firms competing across segments. The competitive landscape reflects differentiation based on technology sophistication, regulatory compliance capabilities, implementation expertise, and industry vertical specialization. IBM, Honeywell International, and Hexagon AB leverage their technology portfolios and global reach to offer comprehensive solutions spanning software platforms, communication systems, and professional services. Everbridge has emerged as a specialized leader in crisis management and mass notification solutions with significant market penetration across government and healthcare sectors.

The market demonstrates consolidation trends with strategic acquisitions enhancing vendor capabilities for example, Motorola Solutions' acquisition of 3tc Software to enhance cloud-based control room capabilities. Emerging competitive strategies emphasize technology integration, combining AI, cloud computing, and IoT capabilities to deliver comprehensive situational awareness and automated response coordination. Vendors increasingly differentiate through vertical-specific solutions and implementation expertise, recognizing that government, healthcare, and energy sectors have distinct emergency management requirements. Regional vendors maintain competitive positions in specific geographies through localized expertise, regulatory knowledge, and established customer relationships, creating a fragmented competitive structure despite the presence of global technology leaders.

Key Market Developments

- In September 2025, IBM Secures Major Emergency Services Network Contract - IBM Corporation was confirmed as the lead supplier for the United Kingdom's Emergency Services Network in a £1.6 billion contract involving system design, construction, cloud infrastructure provision, and user services for approximately 300,000 emergency responders across police, fire, and ambulance services, demonstrating international market expansion for U.S. emergency management technology vendors.

- In November 2024, Motorola Solutions completed the acquisition of 3tc Software to enhance its cloud-based emergency room capabilities, improving real-time response coordination and situational awareness for emergency services, reflecting the market's emphasis on cloud-based infrastructure modernization.

- In October 2024, Hexagon Secures Patents for Emergency Response Innovation - Hexagon obtained two U.S. patents for advanced emergency response technologies including video streaming and secure data sharing capabilities, demonstrating continued innovation in real-time coordination and information management for public safety applications.

Companies Covered in U.S. Emergency Management Services Market

- IBM Corporation

- Atos SE

- West Central Environmental Consultants

- Dewberry

- Dynamiq Pty Ltd.

- Hss Inc.

- Hexagon Ab

- Honeywell International Inc.

- Willdan Group, Inc.

- Hagerty Consulting

- Witt O’ Brien (Seacor Holdings Inc.)

- Obsidian Analytics (Cadmus Group)

- Tetra Tech, Inc.

- ICF International, Inc.

- Battelle National Biodefense Institute

Frequently Asked Questions

The U.S. Emergency Management Services market is projected to reach US$ 63.4 billion by 2033, growing from US$ 43.3 billion in 2026 at a CAGR of 5.6%, driven by escalating natural disaster frequency, government investment, and technology adoption.

Primary demand drivers include the escalating frequency and cost of natural disasters (exceeding $153 billion in recovery costs in recent years), substantial government funding allocations including $57.9 billion in FEMA disaster relief funding for FY2025, regulatory mandates such as the Emergency Preparedness Rule for healthcare, and rapid adoption of advanced technologies including AI and cloud-based solutions with approximately 80% of police departments deploying AI-powered systems.

The cloud-based deployment mode represents the fastest-growing segment, expanding at 12% CAGR, driven by superior scalability, reduced capital expenditure, enhanced disaster recovery capabilities, and accelerated deployment timelines that appeal to government agencies and healthcare organizations modernizing their emergency management infrastructure.

Integration of AI-based decision support systems represents the principal market opportunity, with the healthcare vertical projected at 8.44% CAGR through 2032, driven by adoption of predictive disaster modeling, optimized resource allocation, real-time threat detection, and advanced analytics enabling proactive emergency management and improved response coordination.

Leading market players include IBM Corporation, which secured the £1.6 billion Emergency Services Network contract; Honeywell International Inc. offering integrated security solutions; Everbridge, Inc. specializing in crisis management platforms; Motorola Solutions providing communication systems; Hexagon AB delivering GIS and surveillance solutions; and Atos SE, along with specialized consulting firms including Tetra Tech Inc. and ICF International Inc.