- Medical Devices

- Therapeutic Medical Guidewire Market

Therapeutic Medical Guidewire Market Size, Share, and Growth Forecast, 2026 - 2033

Therapeutic Medical Guidewire Market by Product Type (Solid Guidewire, Wrapped Guidewire), Shape (J-Shape, Straight, Angled), Application (Peripheral Artery Disease, Others), End-user (Hospitals, Others), and Regional Analysis for 2026 – 2033

Therapeutic Medical Guidewire Market Size and Trends Analysis

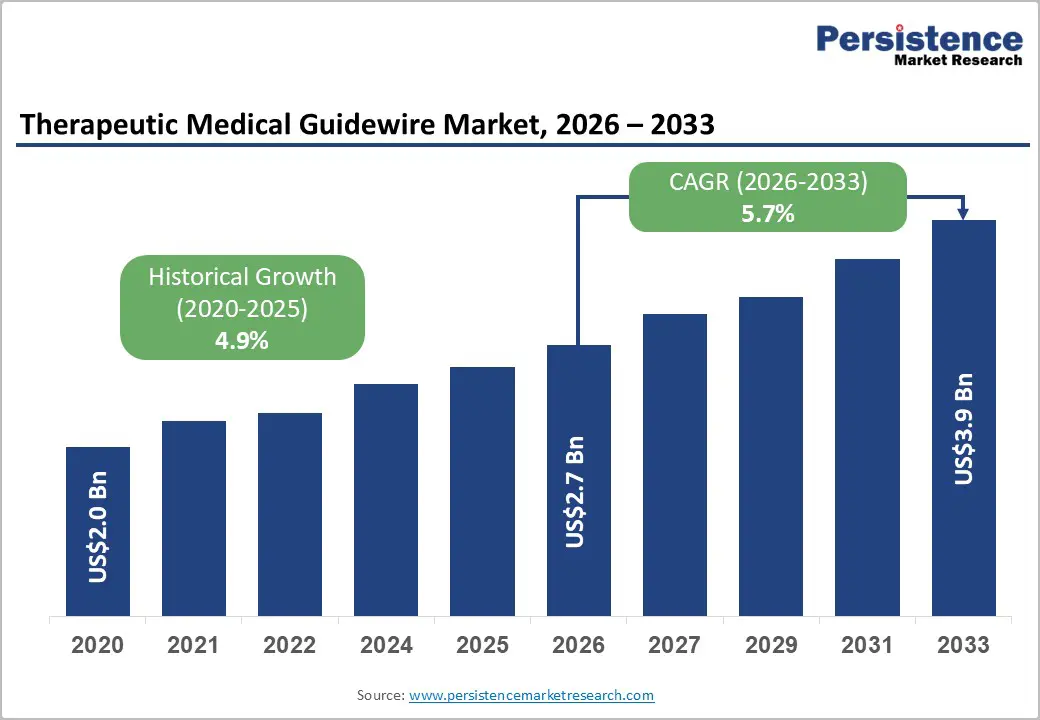

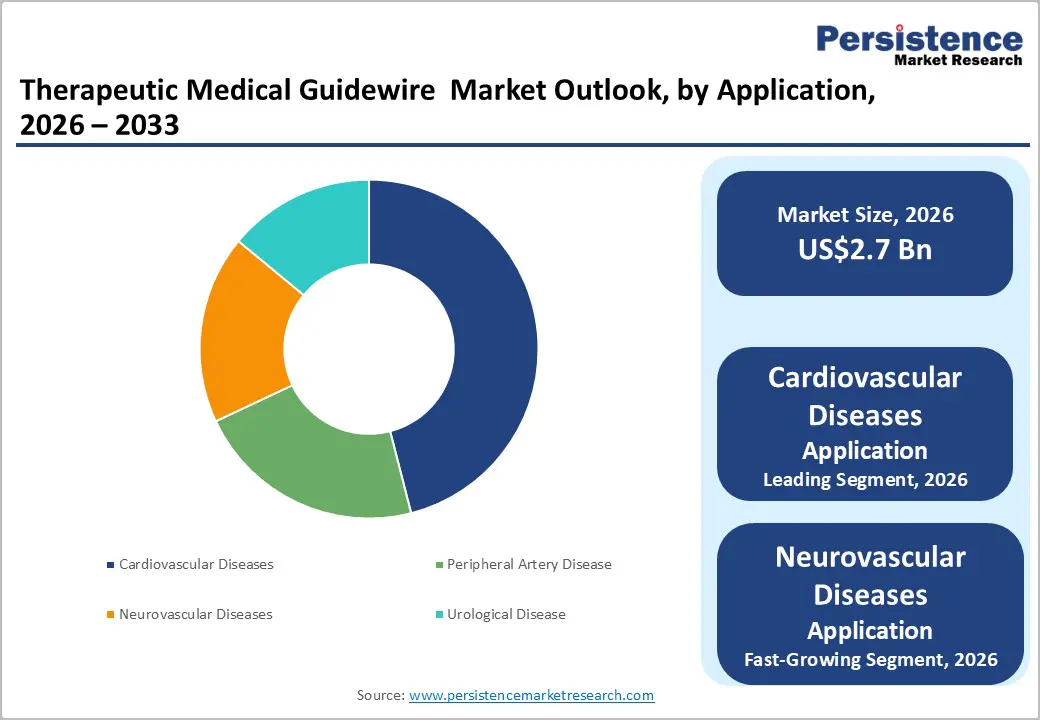

The global therapeutic medical guidewire market size is likely to be valued at US$2.7 billion in 2026, and is expected to reach US$3.9 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033, driven by the increasing prevalence of cardiovascular and peripheral artery diseases requiring interventional procedures, rising adoption of minimally invasive catheter-based therapies, growing procedural volumes in neurovascular and urological interventions, and expanding demand for specialized guidewires with enhanced trackability and torque control.

Growing demand for solid guidewires in cardiovascular diseases across hospitals is accelerating adoption among interventional cardiologists and radiologists.

Key Industry Highlights:

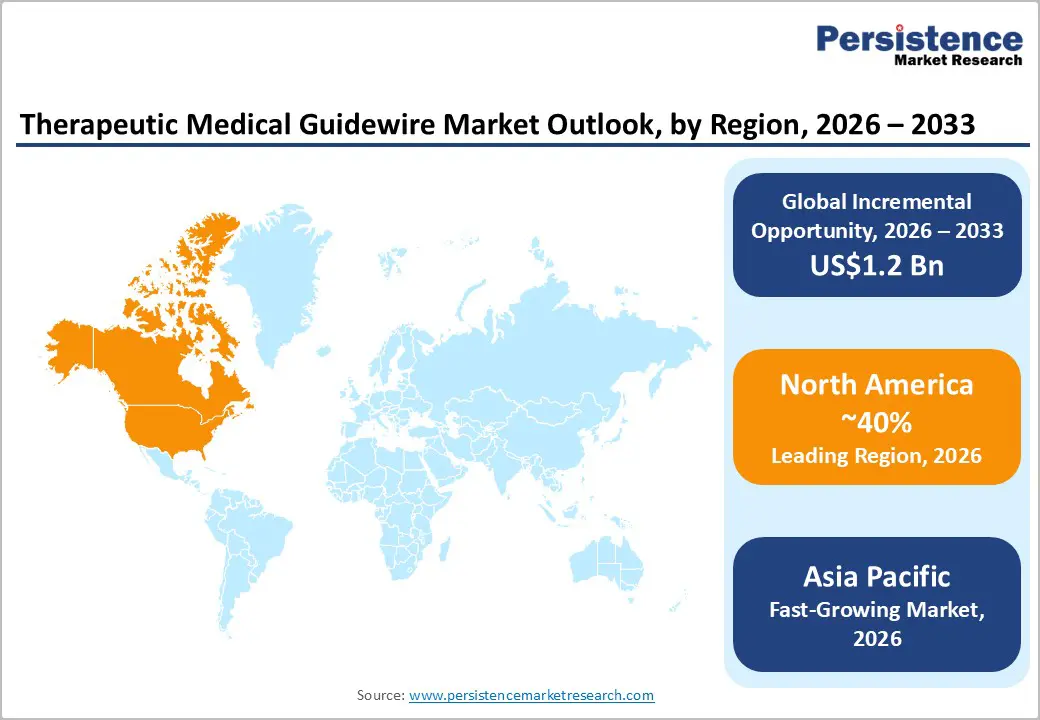

- Leading Region: North America, anticipated to account for a 40% market share in 2026, driven by high procedural volumes, advanced interventional infrastructure, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising cardiovascular burden, increasing cath-lab installations, and growing medical tourism in India and China.

- Dominant Product Type: Solid guidewire, to hold approximately 62% of the market share, as it remains the standard for most therapeutic indications.

- Leading Shape: The straight segment is expected to dominate the market with nearly 58% share in 2026, driven by its versatility, easy insertion, and reliable navigation in routine procedures.

| Key Insights | Details |

|---|---|

| Therapeutic Medical Guidewire Market Size (2026E) | US$2.7 Bn |

| Market Value Forecast (2033F) | US$3.9 Bn |

| Projected Growth CAGR (2026-2033) | 5.7% |

| Historical Market Growth (2020-2025) | 4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Cardiovascular & Peripheral Interventions

The increasing prevalence of cardiovascular diseases, including coronary artery disease, peripheral artery disease, and stroke, is driving the demand for interventional procedures worldwide. Aging populations, sedentary lifestyles, unhealthy diets, and rising incidences of diabetes and hypertension are contributing to a growing patient pool requiring minimally invasive treatments. Healthcare systems are witnessing a surge in procedures such as angioplasty, stenting, atherectomy, and catheter-based therapies.

Technological advancements have significantly improved the safety, precision, and outcomes of these interventions. Innovations in imaging guidance, drug-eluting stents, and advanced catheter designs have enhanced procedural success rates while reducing recovery times and complications. This has encouraged both physicians and patients to prefer minimally invasive options over traditional open surgeries. Expanding healthcare infrastructure, especially in emerging economies, is improving access to advanced interventional treatments. Increased awareness, better diagnostic capabilities, and supportive reimbursement policies in developed regions are further accelerating procedure volumes.

Neurovascular & Urological Procedure Growth

The growing incidence of neurological disorders such as stroke, aneurysms, and arteriovenous malformations is significantly increasing the demand for neurovascular procedures. Rapid advancements in minimally invasive techniques, including endovascular coiling, thrombectomy, and embolization, have improved clinical outcomes and reduced mortality rates. Faster intervention times, especially in acute stroke management, are encouraging hospitals to expand neurointerventional capabilities and invest in specialized infrastructure.

The rising prevalence of urological conditions, including kidney stones, benign prostatic hyperplasia, and urinary tract disorders, is driving procedural volumes in urology. Lifestyle factors, aging populations, and increasing awareness are leading to earlier diagnosis and treatment. Minimally invasive approaches such as ureteroscopy, laser lithotripsy, and catheter-based drainage procedures are gaining preference due to shorter hospital stays, reduced pain, and quicker recovery. Technological innovations, including advanced imaging systems, robotic-assisted platforms, and improved catheter designs, are enhancing procedural accuracy and efficiency in both segments. In addition, growing healthcare investments and expanding access to specialized care in developing regions are supporting higher adoption rates.

Barrier Analysis – High Device Cost and Reimbursement Challenges

Elevated prices of advanced medical devices create a significant barrier to widespread adoption, particularly in cost-sensitive healthcare systems. Hospitals and clinics often face budget constraints, making it difficult to procure high-end equipment such as specialized catheters, stents, and imaging-guided systems. This challenge is more pronounced in developing regions, where healthcare spending and infrastructure investments remain limited.

Inconsistent or limited reimbursement policies further restrict patient access to these technologies. Many procedures involving advanced devices are either partially covered or excluded from insurance plans, increasing out-of-pocket expenses for patients. This can lead to delayed treatments or a preference for less effective alternatives.

Regulatory and Clinical Trial Requirements

Strict approval processes for medical devices and procedures create significant hurdles for manufacturers seeking market entry. Regulatory authorities require extensive documentation on safety, quality, and performance, often involving multiple phases of evaluation. These processes can be time-consuming and costly, delaying product launches and increasing overall development expenses.

Clinical trials play a crucial role in demonstrating effectiveness and minimizing risks, but they demand substantial investment, skilled resources, and long timelines. Recruiting suitable patient populations, maintaining compliance with protocols, and ensuring accurate data collection add further complexity. Any delays or unfavorable outcomes can significantly impact commercialization plans.

Opportunity Analysis – Innovation in Hydrophilic-Coated and Neurovascular Guidewires

Continuous advancements in material science and device engineering are significantly enhancing the performance of modern guidewires, particularly those used in complex vascular and neurovascular procedures. Hydrophilic-coated guidewires now incorporate advanced polymer coatings that create a thin fluid layer when activated, enabling smooth and low-friction navigation through tortuous vessels while minimizing trauma to vessel walls. These coatings are being engineered for improved durability and lubricity retention, ensuring consistent performance throughout lengthy procedures.

Innovations in core materials such as nitinol and hybrid alloys have improved flexibility, kink resistance, and torque control, allowing physicians to achieve precise navigation even in highly complex anatomies. Enhanced tip designs, including soft, shapeable, and atraumatic tips, further support controlled manoeuvrability and reduce procedural risks. Neurovascular guidewires are evolving to address the challenges of delicate cerebral vasculature. Manufacturers are developing microcatheter-compatible and smaller-diameter wires that can access distal and narrow vessels with greater accuracy. Integration with advanced imaging technologies is also improving real-time visualization and procedural precision.

Expansion in Cath-Lab Markets

Rapid growth in interventional procedures is driving the expansion of catheterization laboratories (cath-labs) across both developed and emerging healthcare systems. Hospitals are increasingly investing in advanced cath-lab infrastructure to manage rising cases of cardiovascular, neurovascular, and peripheral vascular diseases. The shift toward minimally invasive treatments has made cath-labs a critical component of modern healthcare delivery, enabling faster diagnosis and treatment with reduced patient recovery times.

Technological advancements are playing a key role in this expansion. Modern cath-labs are equipped with high-resolution imaging systems, real-time data integration, and enhanced navigation tools that improve procedural accuracy and efficiency. The integration of digital platforms and automation is also streamlining workflows, reducing procedure time, and improving patient outcomes. Improving healthcare infrastructure, growing private sector investments, and increasing patient awareness are accelerating the establishment of new cath-labs.

Category-wise Analysis

Product Type Insights

Solid guidewires are expected to lead the market, accounting for approximately 62% of the total share in 2026. Their dominance is attributed to superior strength, durability, and reliable performance across a broad range of interventional procedures. The solid core design ensures excellent torque control, allowing physicians to navigate complex vascular pathways with greater precision. These guidewires are widely preferred in procedures that require high pushability and stability, especially in challenging anatomical conditions.

In addition, their cost-effectiveness and consistent performance compared to more specialized variants support their widespread adoption in both routine and advanced interventions. A representative example is the OmniWire pressure guidewire by Philips, which features a solid proximal core design that enhances torque control, pushability, and kink resistance, key attributes that make solid guidewires highly effective in complex procedures.

Wrapped guidewires represent the fastest-growing product type, due to their enhanced flexibility and superior tactile feedback during procedures. Their design, which incorporates an outer wire wrap around the core, improves torque transmission while maintaining softness at the tip for safer navigation through delicate and tortuous vessels. This balance between control and flexibility makes them highly suitable for complex cardiovascular and neurovascular interventions.

Advancements in coating technologies further enhance their trackability and reduce friction. Flagship™ Coronary Guidewire by Integer Holdings Corporation. This device features a spring coil (wrapped) design, which enhances flexibility while maintaining adequate support for device delivery during coronary interventions.

Shape Insights

The straight segment is expected to dominate the market, contributing nearly 58% of revenue in 2026, fueled by its versatility and widespread use across a broad range of interventional procedures. Their simple design allows for easier insertion, better pushability, and reliable navigation in relatively less complex vascular pathways. Physicians often prefer straight guidewires for routine diagnostic and therapeutic procedures where high precision and direct access are required. These guidewires are commonly used as primary access tools before switching to more specialized variants if needed.

Intuition™ Coronary Guidewire by Medtronic. This widely used workhorse guidewire is available with a straight tip configuration, designed to provide strong torque control, smooth navigation, and reliable crossability in coronary interventions.

The angled segment represents the fastest-growing shape, propelled by its superior ability to navigate complex and tortuous anatomies. The angled tip allows physicians to access side branches, bifurcations, and sharply curved vessels with greater precision compared to straight designs. This enhances procedural efficiency, especially in challenging cardiovascular, neurovascular, and peripheral interventions. Their improved steerability reduces the need for repeated repositioning, saving time and minimizing vessel trauma.

Zebra™ Urological Guidewire by Boston Scientific. This device features a 3 cm angled flexible tip, specifically designed to improve navigation through tortuous or obstructed anatomical pathways.

Regional Insights

North America Therapeutic Medical Guidewire Market Trends

North America is projected to dominate, accounting for nearly 40% of the revenue in 2026, with advanced healthcare systems, high procedural volumes, and early adoption of minimally invasive techniques. The growing prevalence of cardiovascular, neurovascular, and peripheral vascular diseases continues to increase the demand for interventional procedures such as angioplasty, stenting, and catheter-based therapies. An aging population and lifestyle-related risk factors further contribute to consistent procedure growth.

The rapid adoption of technologically-advanced guidewires with enhanced torque control, flexibility, and hydrophilic coatings. Hospitals and ambulatory surgical centers are increasingly prioritizing devices that improve procedural efficiency and patient outcomes. Strong reimbursement frameworks and the presence of skilled healthcare professionals support the widespread use of advanced interventional tools. For example, Abbott Laboratories offers the HI-TORQUE BALANCE MIDDLEWEIGHT™ (BMW™) Universal II guidewire, which uses a nitinol core and advanced coating to provide excellent control and trackability in coronary procedures.

Europe Therapeutic Medical Guidewire Market Trends

Europe represents a well-established market for therapeutic medical guidewires, driven by advanced healthcare systems and a high volume of interventional procedures. Countries such as Germany, France, and the U.K. play a major role due to their strong hospital networks and widespread availability of catheterization laboratories. The rising prevalence of cardiovascular and neurovascular diseases, along with an aging population, continues to increase the demand for minimally invasive treatments such as angioplasty and endovascular interventions.

The growing preference for precision-driven and low-risk procedures is leading to increased adoption of advanced guidewires with improved flexibility, torque control, and hydrophilic coatings. The expansion of outpatient care and day-surgery centers is supporting the use of efficient and easy-to-handle devices. Strict regulatory standards in Europe also ensure high product quality and safety, encouraging manufacturers to focus on innovation and compliance. For example, B. Braun SE offers a range of high-performance guidewires designed for vascular access and interventional procedures, known for their precision and reliability. These factors collectively support steady growth across the region.

Asia Pacific Therapeutic Medical Guidewire Market Trends

Asia Pacific is likely to be the fastest-growing market for therapeutic medical guidewires in 2026, expanding healthcare infrastructure and rising demand for minimally invasive procedures. Countries such as China, India, and Japan are witnessing a significant increase in cardiovascular, neurovascular, and urological disorders due to aging populations, urbanization, and lifestyle changes. This growing disease burden is leading to higher volumes of interventional procedures, including angioplasty and catheter-based treatments.

The rapid development of hospitals and catheterization laboratories, particularly in urban and semi-urban areas. Governments and private healthcare providers are investing heavily to improve access to advanced medical technologies. Increasing awareness and early diagnosis are encouraging patients to opt for timely treatment. Cost sensitivity remains an important factor, driving demand for affordable yet high-quality guidewires. This has encouraged both global and regional manufacturers to expand their presence and offer competitively priced products.

For example, Terumo Corporation provides advanced hydrophilic guidewires widely used across Asia for their smooth navigation and reliability in complex procedures.

Competitive Landscape

The global therapeutic medical guidewire market is shaped by the presence of both global medtech leaders and specialized device manufacturers. In developed regions like North America and Europe, companies such as Boston Scientific Corporation, Abbott Laboratories, and Medtronic maintain strong positions through extensive product portfolios, established clinical credibility, and long-standing relationships with hospitals and healthcare providers. Their focus on advanced technologies, including solid and hydrophilic-coated guidewires, enhances procedural precision and outcomes.

In Asia Pacific region is witnessing the rise of regional manufacturers offering cost-effective solutions, improving accessibility in price-sensitive markets. Solid guidewires remain widely adopted due to their reliability, improved pushability, and ability to support complex procedures across cath labs. To sustain growth, companies are increasingly investing in research and development, forming strategic clinical collaborations, and expanding their product portfolios. These strategies help strengthen technological capabilities and broaden application areas across cardiovascular, neurovascular, and peripheral interventions.

Key Industry Developments:

- In January 2026, Kaneka Medical America LLC announced the U.S. launch of Enlight Medical Ltd.’s WaveSelect 1014 guidewire under an exclusive distribution agreement, strengthening its neurovascular portfolio while reinforcing its focus on embolization coil technologies for neurovascular therapies.

- In October 2025, Medtronic announced the launch of the Stedi™ Extra Support guidewire to enhance the performance of its Evolut™ transcatheter aortic valve replacement (TAVR) platform. The guidewire was designed to improve procedural stability and ensure compatibility with all commercially available TAVR systems for treating patients with severe aortic stenosis. The announcement was made during the Transcatheter Cardiovascular Therapeutics (TCT) 2025 conference held in San Francisco.

Companies Covered in Therapeutic Medical Guidewire Market

- Abbott

- Boston Scientific Corporation

- Medtronic

- Terumo Corporation

- Cardinal Health

- B. Braun SE

- Cook Medical

- Olympus Corporation

- Merit Medical Systems

- Teleflex Incorporated

- Asahi Intecc Co., Ltd.

- Nipro Corporation

- Smiths Medical

- Integer Holdings Corporation

- Biotronik SE & Co. KG

Frequently Asked Questions

The global therapeutic medical guidewire market is projected to reach US$2.7 billion in 2026.

The increasing volume of cardiovascular and peripheral interventions is a key factor driving market growth.

The therapeutic medical guidewire market is poised to witness a CAGR of 5.7% from 2026 to 2033.

Hydrophilic-coated and neurovascular guidewires and expansion in Asia Pacific and emerging cath-lab markets are the key opportunities.

Boston Scientific Corporation, Abbott, Medtronic, Terumo Corporation, and Cook Medical are the key players.