- Medical Devices

- Endoscopy Devices Market

Endoscopy Devices Market Size, Share, and Growth Forecast 2026 – 2033

Endoscopy Devices Market by Product Type (Endoscopes, Visualization systems, Operative devices, Accessories), Application (Gastroenterology, Pulmonology, Urology, Gynecology, Orthopedics, Otolaryngology, Others), by End User (Hospitals, Ambulatory surgery centers, Specialty clinics, Diagnostic centers), by Regional Analysis, 2026-2033

Endoscopy Devices Market Size and Trend Analysis

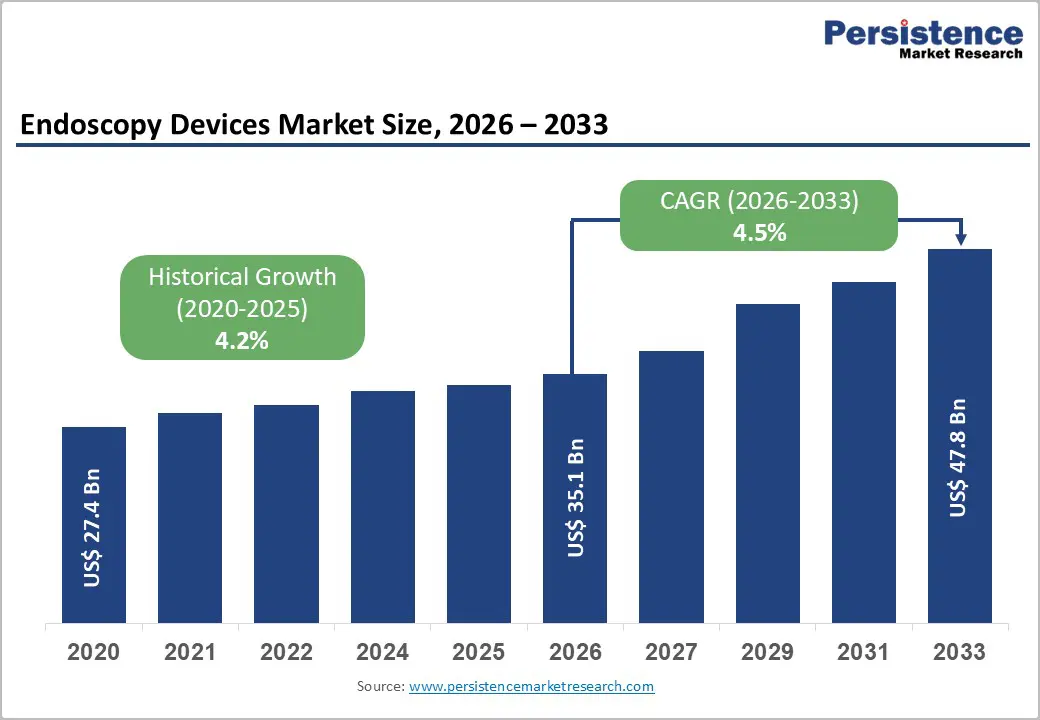

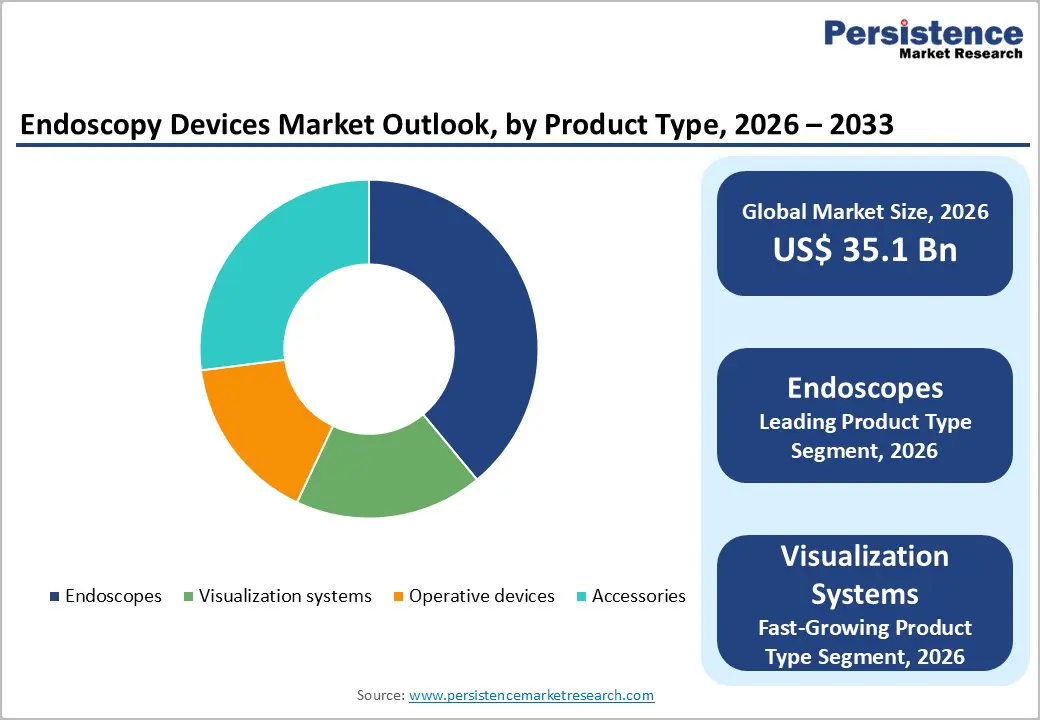

The global endoscopy devices market size is expected to be valued at US$ 35.1 billion in 2026 and projected to reach US$ 47.8 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033. The market expansion is primarily driven by rising volumes of endoscopic procedures and growing preference for minimally invasive surgeries that reduce hospital stay and recovery time.

The increasing prevalence of gastrointestinal, colorectal, pulmonary, and urologic disorders in aging populations is pushing healthcare systems to invest in advanced endoscopy platforms and accessories. In parallel, continuous innovation in flexible, capsule, and video endoscopy, including AI-enabled polyp detection and single-use scopes for improved infection control, is accelerating replacement cycles and premium device adoption.

Key Industry Highlights:

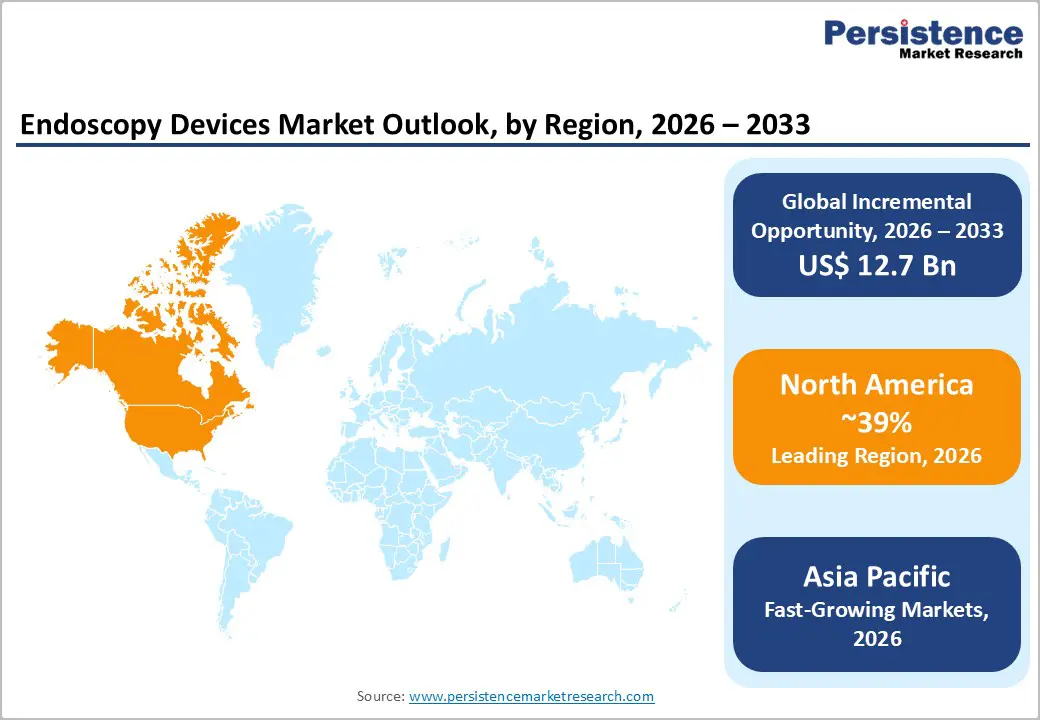

- North America remains the leading regional market for endoscopy devices, supported by high procedure volumes, strong reimbursement for screening colonoscopy, and rapid adoption of AI-assisted and single-use endoscopy technologies in hospitals and ambulatory surgery centers.

- Asia-Pacific is the fastest-growing market, driven by expanding healthcare infrastructure, rising gastrointestinal disease burden, rise in middle-income group access to care, and increasing device manufacturing capabilities in China, Japan, and South Korea.

- Within product types, endoscopes form the dominant segment, representing around 39% of market value in 2025, backed by heavy use of flexible, rigid, and capsule endoscopes across gastroenterology, pulmonology, urology, and ENT practices worldwide.

- Visualization systems, including cameras, light sources, and video processors, are among the fastest-growing segments, as providers upgrade to 4K, narrow-band imaging, and AI-capable platforms that enhance lesion detection and procedural efficiency across specialties.

- A key opportunity lies in single-use and hybrid endoscopy solutions combined with AI-enabled imaging, which address infection-control concerns, reduce reprocessing burdens, and create premium, high-growth niches across North America, Europe, and advanced Asia-Pacific markets.

| Key Insights | Details |

|---|---|

|

Endoscopy Devices Market Size (2026E) |

US$ 35.1 billion |

|

Market Value Forecast (2033F) |

US$ 47.8 billion |

|

Projected Growth CAGR (2026-2033) |

4.5% |

|

Historical Market Growth (2020-2025) |

4.2% |

Market Dynamics

Drivers - Rising endoscopy procedure volumes and chronic disease burden

A key growth driver is the surge in endoscopic procedure volumes driven by the global rise in gastrointestinal cancers, colorectal cancer, obesity, and inflammatory bowel disease. Aging populations in North America, Europe, and Asia are undergoing more diagnostic and therapeutic endoscopies for early detection and minimally invasive management of these conditions, as recommended in multiple clinical guidelines. The global endoscopy procedures market was valued at approximately US$ 361 billion in 2024, growing at a CAGR of approximately 5.5% through 2034, indicating robust, procedure-linked demand for devices and consumables. As hospitals and ambulatory surgery centers expand capacity for colonoscopy, bronchoscopy, cystoscopy, and laparoscopy, demand strengthens for endoscopes, visualization systems, and operative devices that support faster, safer procedures and higher throughput.

Shift toward minimally invasive and outpatient care models

The strong global shift from open surgeries to minimally invasive and endoscopic procedures is another powerful demand driver for endoscopy devices. Clinical evidence indicates that endoscopic interventions typically reduce postoperative pain, shorten hospital stays, lower complication rates, and enable faster return to daily activities, supporting their adoption by payers and providers. In the U.S. and Europe, favorable reimbursement for screening colonoscopy and therapeutic endoscopy, coupled with the growth of ambulatory surgery centers (ASCs), is pushing hospitals and independent centers to upgrade to high-definition and 4K endoscopy towers. In emerging markets across Asia, growing middle-class populations, rising health insurance coverage, and the expansion of day-care surgery infrastructure further reinforce demand for flexible endoscopes, video processors, and disposable accessories, thereby benefiting the overall endoscopy device ecosystem.

Restraint - High capital costs and budget constraints in developing markets

Despite strong clinical benefits, the high acquisition and maintenance costs of sophisticated endoscopy systems remain a barrier to adoption, especially in low and middle-income countries. Full endoscopy suites comprising towers, light sources, video processors, and reusable endoscopes often require six-figure capital investments per room, straining budgets for public hospitals and smaller private facilities. As a result, more than 40% of small healthcare centers in developing regions continue to rely on refurbished equipment, which accounts for nearly 22% of total endoscope sales globally, slowing the penetration of next-generation technologies. These cost pressures can delay replacement cycles and limit the adoption of premium features such as 4K imaging, narrow-band imaging, and robotic-assisted platforms.

Infection control concerns and reprocessing challenges

Another key restraint is the persistent concern about infection transmission associated with inadequate reprocessing of reusable endoscopes, particularly duodenoscopes and bronchoscopes. Healthcare authorities and professional societies have reported outbreaks associated with complex endoscope designs that are difficult to clean and disinfect thoroughly, leading to stringent guidelines and scrutiny of reprocessing workflows. Compliance with evolving standards requires significant investments in automated reprocessors, sterilization infrastructure, staff training, and documentation systems, thereby increasing operational complexity for hospitals and clinics. In some settings, these challenges drive reluctance to expand procedure volumes or adopt certain reusable devices, while also making providers cautious about transitioning to new models without robust infection-control validation.

Opportunity - Expansion of single-use and hybrid endoscopy solutions

A major opportunity lies in the rapid expansion of single-use and hybrid endoscopy platforms, which directly address infection-control, workflow, and logistics challenges associated with reusable scopes. Single-use flexible endoscopes already account for around one-quarter of purchases in some U.S. hospitals, reflecting strong interest in devices that eliminate cross-contamination risk and reduce reliance on central reprocessing. Manufacturers are developing cost-optimized single-use bronchoscopes, ureteroscopes, and ENT scopes that combine high-definition imaging with ergonomic designs, alongside hybrid models where reusable endoscopy towers interface with disposable insertion tubes. As payers and regulators increasingly prioritize patient safety and traceability, and as ambulatory centers seek simplified operations, vendors that expand portfolios in single-use and hybrid systems are positioned to capture a high-growth revenue stream within the overall endoscopy devices market.

AI-enabled visualization and robotics-assisted endoscopy

Another high-potential opportunity is the integration of artificial intelligence (AI), advanced optics, and robotic technologies into visualization systems and endoscope platforms. AI-assisted colonoscopy solutions have demonstrated improved adenoma detection rates and reduced miss rates for colorectal polyps, leading to strategic collaborations between technology companies and gastrointestinal societies to expand access to AI-powered screening, particularly in underserved communities. Robotic-assisted endoscopy and steerable capsule endoscopy are being developed to navigate complex anatomy, enhance precision, and enable remote or teleoperated procedures, as highlighted in recent clinical research on capsule endoscopy technologies. Vendors that invest in AI-driven video processors, cloud-connected image management, and robotic platforms can unlock differentiated clinical value and access premium pricing segments, particularly in North America, Europe, and advanced Asian markets.

Category-wise Analysis

Product Type Insights

The endoscopes segment represents the leading product type, accounting for about 39% of the endoscopy devices market in 2025, supported by high utilization of flexible, rigid, and capsule endoscopes across major clinical specialties. Flexible endoscopes alone account for a dominant share of procedure volumes in gastroenterology, pulmonology, and urology, with hospitals representing approximately 61% of global flexible endoscope utilization and more than 5,500 hospitals integrating digital flexible suites in 2024.

Clinical guidelines emphasizing early detection of colorectal and upper GI cancers, together with growing adoption of capsule endoscopy for small-bowel evaluation, further reinforce demand. In addition, ongoing upgrades to high-definition and ultra-slim designs, as well as the shift toward single-use variants in infection-sensitive settings, underpin the leadership of endoscopes within the broader endoscopy devices portfolio.

Application Insights

Within applications, gastroenterology is the leading segment, accounting for an estimated 40% share of global endoscopy device demand in 2025, driven by high volumes of upper GI endoscopy and colonoscopy for screening, diagnosis, and therapy. The burden of colorectal cancer, peptic ulcer disease, inflammatory bowel disease, and functional GI disorders continues to rise, prompting national screening programs and guideline-based interventions across the U.S., Europe, and several Asia-Pacific countries.

The global endoscopy procedures market indicates that gastrointestinal procedures account for the largest share of total endoscopic interventions, with strong growth expected through 2034, which naturally translates into sustained demand for GI endoscopes, visualization systems, and therapeutic accessories such as forceps, snares, and graspers. Technological advances in capsule endoscopy and AI-assisted polyp detection are further consolidating gastroenterology’s position as the anchor application for endoscopy devices.

End-user Insights

Among end users, hospitals constitute the leading segment, accounting for roughly 60%–65% of global demand for endoscopy devices due to their comprehensive service mix and high procedure throughput. Hospitals typically host full-featured endoscopy suites that span gastroenterology, pulmonology, urology, gynecology, and orthopedics and thus require a broad inventory of endoscopes, visualization towers, and operative instruments.

Evidence from the flexible endoscopes market shows that hospitals represent about 61% of utilization, with rapid integration of digital suites, AI-capable processors, and hybrid reusable/single-use workflows to support rising procedure volumes. In tertiary and academic centers, hospitals also serve as innovation hubs, running clinical trials, training programs, and advanced minimally invasive surgery units, which further drive the procurement of high-end endoscopy platforms and accessories relative to ambulatory surgery centers and specialty clinics.

Regional Insights

North America Endoscopy Devices Market Trends

North America remains the leading region in the endoscopy devices market driven by a combination of advanced healthcare infrastructure, high procedure volumes, and rapid adoption of cutting-edge technologies. The region consistently accounts for the largest share of global revenue, often around 38–41% of the market, led by the United States with strong participation from Canada and Mexico. Key factors supporting this dominance include widespread use of minimally invasive procedures across specialties such as gastroenterology, pulmonology, urology and more, an aging population with increasing chronic disease burden, and well-established reimbursement frameworks that facilitate frequent endoscopic screening and treatment.

In addition, North American healthcare systems are early adopters of high-definition imaging, AI-enabled visualization, robotic-assisted endoscopy, and single-use technologies, which enhance diagnostic accuracy and procedural outcomes. High healthcare expenditure and continuous R&D investments by major device manufacturers further reinforce the region’s leadership, establishing it as both a demand center and innovation hub for endoscopy devices globally.

Asia Pacific Endoscopy Devices Market Trends

Asia-Pacific is emerging as one of the fastest-growing regions in the global Endoscopy Devices market, driven by rising healthcare investments, expanding access to diagnostic procedures, and rapidly improving infrastructure. Countries like China, India, Japan, and South Korea are investing heavily in modern healthcare systems to meet growing demand for early disease detection and minimally invasive treatments, which boost endoscopic procedures such as gastrointestinal and bronchoscopic examinations.

The region’s aging population and increasing prevalence of chronic diseases are driving higher procedure volumes and fueling the adoption of advanced endoscopy technologies. Governments are also supporting healthcare expansion through infrastructure upgrades and screening programs, particularly in tier-2 and tier-3 cities, enhancing access in previously underserved areas. Innovations such as high-definition imaging, AI-integrated systems, and portable endoscopy platforms are gaining traction, improving diagnostic accuracy and patient outcomes.

Additionally, medical tourism growth and awareness of preventive care are further accelerating market uptake, positioning Asia Pacific as a key growth hub for global endoscopy device manufacturers.

Competitive Landscape

The endoscopy devices market competitive landscape is characterized by intense competition, rapid technological innovation, and continuous product differentiation. Market participants compete on imaging quality, procedural efficiency, safety, and cost-effectiveness, with strong emphasis on high-definition visualization, minimally invasive solutions, and infection-control features. Continuous investments in R&D, AI-enabled diagnostics, and single-use technologies are reshaping competitive positioning and raising entry barriers. Strategic focus areas include expanding product portfolios, improving clinical outcomes, and strengthening regional presence through partnerships and distribution networks.

Key Developments:

- In July 2025, FUJIFILM (Thailand) Ltd. continued to advance healthcare diagnostics and patient treatment through its comprehensive health innovations, unveiling the ELUXEO® 8000 Endoscopy System and the 800 Series ELUXEO® Endoscopes for the first time in Thailand.

Companies Covered in Endoscopy Devices Market

- Olympus Corporation

- Karl Storz SE & Co. KG

- Boston Scientific Corporation

- Stryker Corporation

- Medtronic plc

- Johnson & Johnson (Ethicon Endo-Surgery)

- Fujifilm Holdings Corporation

- Hoya Corporation (Pentax Medical)

- CONMED Corporation

- Smith & Nephew plc

- Ambu A/S

- Richard Wolf GmbH

Frequently Asked Questions

The global endoscopy devices market size is projected to reach US$ 35.1 billion in 2026, reflecting steady growth from US$ 27.4 billion in 2020 on the back of rising procedure volumes and minimally invasive surgery adoption.

Key demand drivers include increasing incidence of gastrointestinal and colorectal diseases, growing preference for minimally invasive procedures, and expanding endoscopy procedure volumes across hospitals and ambulatory surgery centers worldwide.

North America is the leading region, contributing roughly 40%–43% of global revenues, supported by advanced healthcare infrastructure, strong reimbursement frameworks, and rapid adoption of AI‑enabled and single‑use endoscopy technologies.

A major opportunity lies in developing single‑use and hybrid endoscopy platforms integrated with AI‑enhanced visualization, which address infection‑control challenges, streamline workflows, and command premium pricing in high‑value markets.

Prominent players include Olympus Corporation, Karl Storz SE & Co. KG, Boston Scientific Corporation, Stryker Corporation, Medtronic plc, Johnson & Johnson (Ethicon Endo Surgery), Fujifilm Holdings Corporation, Hoya Corporation (Pentax Medical), CONMED Corporation, Smith & Nephew plc, Ambu A/S, and Richard Wolf GmbH, among others.