- Pharmaceuticals

- Therapeutic Hypothermia Systems Market

Therapeutic Hypothermia Systems Market Size, Share, and Growth Forecast 2026 – 2033

Therapeutic Hypothermia Systems Market by Product Type (Cooling Devices, Cooling Catheters, Cooling Packs, Others), Application (Neurology, Cardiology, Neonatal Care, Others), End-user (Hospitals, Specialty Clinics, ASCs, Others), and Regional Analysis, 2026–2033

Therapeutic Hypothermia Systems Market Share and Trends Analysis

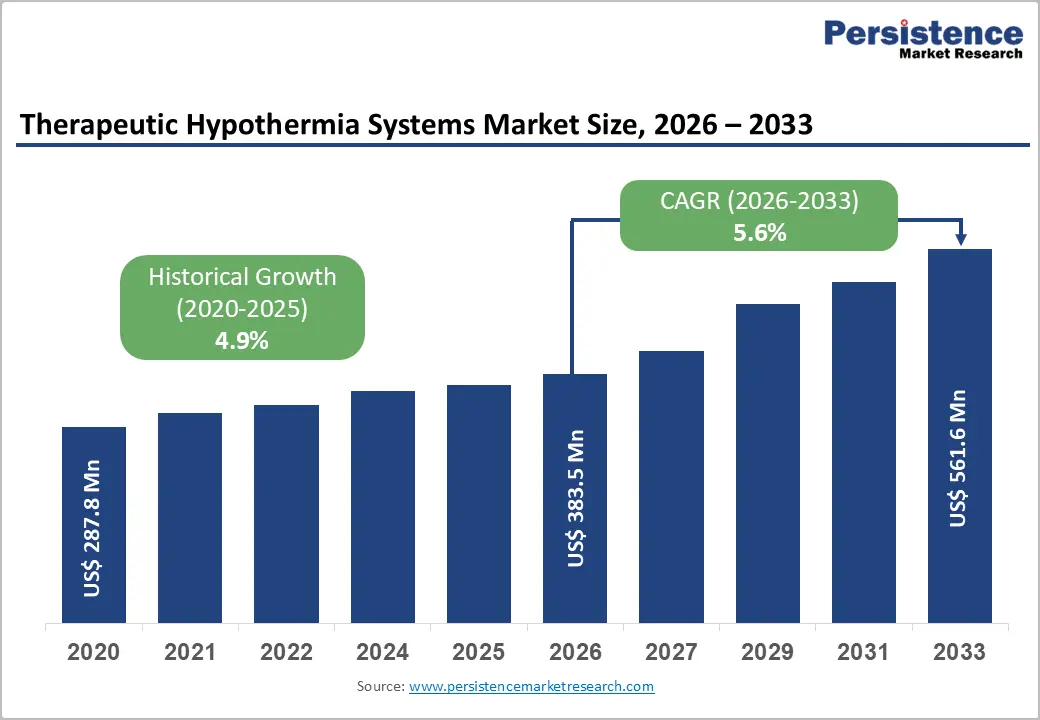

The global therapeutic hypothermia systems market size is expected to be valued at US$ 383.5 million in 2026 and projected to reach US$ 561.6 million by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The market is advancing steadily, driven by expanding clinical guidelines mandating targeted temperature management (TTM) following cardiac arrest, growing neonatal care adoption of hypothermia protocols for hypoxic-ischemic encephalopathy (HIE), and increasing investment in critical care infrastructure across Asia Pacific and Latin America. The American Heart Association (AHA) and European Resuscitation Council (ERC) both incorporate therapeutic hypothermia into their resuscitation guidelines, providing a regulatory and clinical foundation that sustains device procurement across intensive care units and cardiac centers globally.

Key Industry Highlights:

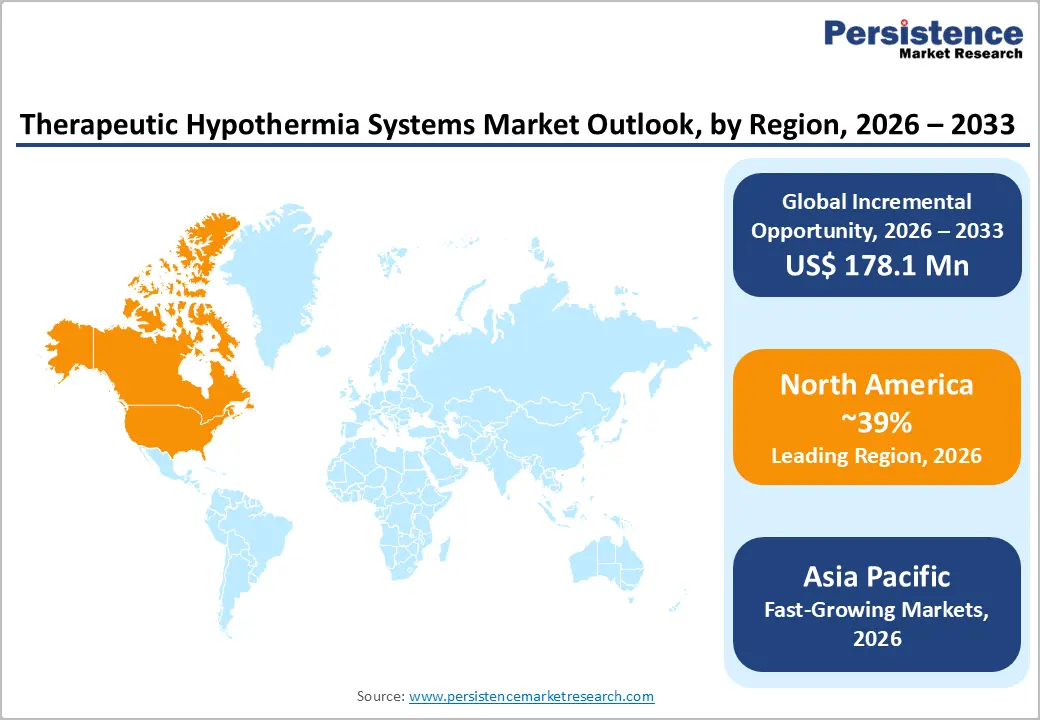

- Leading Region – North America commanded approximately 39% of the global therapeutic hypothermia systems share in 2026, driven by AHA-mandated TTM guidelines, CMS reimbursement, 350,000+ annual U.S. cardiac arrests, and ZOLL Medical's Arctic Sun® platform dominance in ICU settings.

- Fast-Growing Market– Asia Pacific is the fastest-growing market, driven by India's 25 million annual births creating massive neonatal HIE demand, China's Healthy China 2030 cardiac ICU expansion, and Phoenix Medical Systems' Tecotherm Neo® targeting emerging NICU markets.

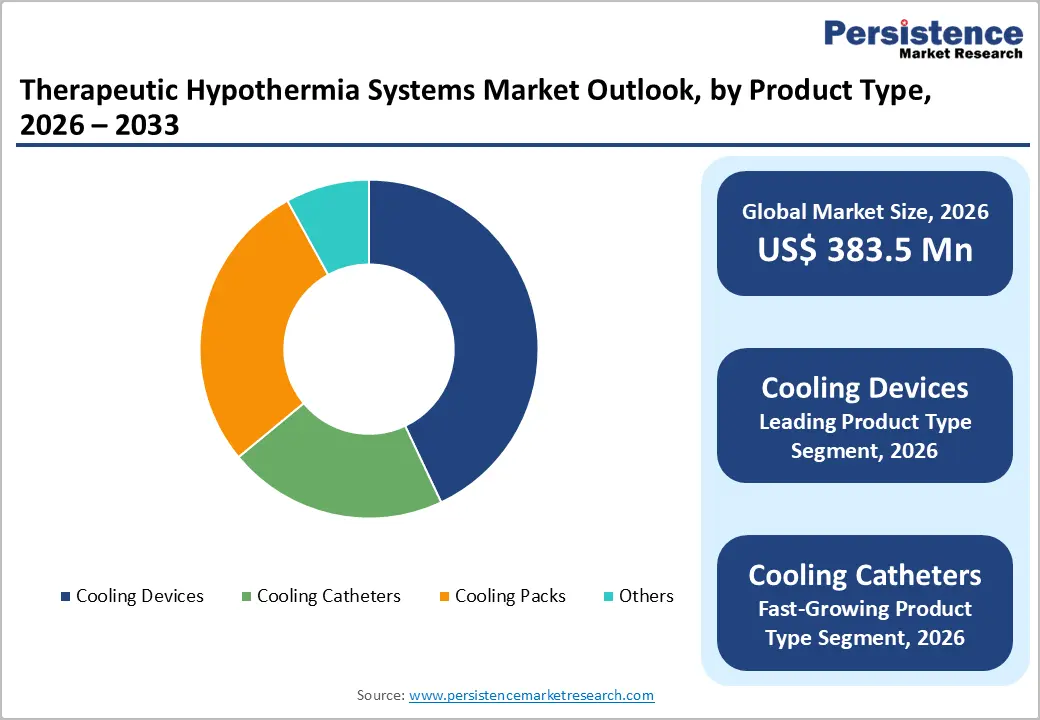

- Dominant Product – Cooling devices held approximately 43% market share in 2025, preferred for their non-invasive application across neurology, cardiology, and neonatal indications, with ZOLL's Arctic Sun® and Stryker's IntelliCool® leading installed base volumes.

- Fast-Growing Product Segment – Cooling catheters are the fastest-growing product type, achieving target temperatures 60–90 minutes faster than surface methods per SCCM documentation, with ZOLL's Thermogard XP® and Becton Dickinson's Cool Line® expanding adoption in cardiac ICUs globally.

- Key Opportunity – Asia Pacific Neonatal Hypothermia: India's INNF guidelines endorsing neonatal cooling, 25 million annual births, PM-JAY expanding tertiary care access, and China's NHC NICU buildout collectively represent a US$ 178.1 million incremental demand opportunity through 2033.

Market Dynamics

Drivers - AHA and ERC Clinical Guidelines Mandating Targeted Temperature Management in Post-Cardiac Arrest Care

The systematic incorporation of therapeutic hypothermia or targeted temperature management (TTM) into evidence-based resuscitation guidelines by leading cardiac societies is the most authoritative and structurally impactful demand driver for the market. The American Heart Association (AHA) 2020 Guidelines for CPR and Emergency Cardiovascular Care and the European Resuscitation Council (ERC) 2021 Guidelines both recommend TTM at 32–36°C for comatose adult survivors of cardiac arrest, establishing therapeutic hypothermia as a standard of care in ICU management.

The American College of Cardiology (ACC) further supports post-resuscitation TTM protocols in its clinical performance measures. With cardiac arrest affecting approximately 350,000 individuals annually in the U.S. alone,s per AHA, and similar incidences in Europe, guideline-driven TTM adoption generates a large, growing, and clinically mandated addressable market for therapeutic hypothermia cooling devices and catheters.

Rising Global Incidence of Hypoxic-Ischemic Encephalopathy in Neonates Expanding Cooling Device Demand

Therapeutic hypothermia is now the globally accepted standard of care for neonatal hypoxic-ischemic encephalopathy (HIE), a leading cause of neonatal death and disability. The World Health Organization (WHO) estimates that approximately 1 million neonates annually suffer from HIE, with birth asphyxia accounting for 23% of neonatal deaths globally. Cooling to 33–34°C for 72 hours has been demonstrated in landmark clinical trials published in The Lancet and the New England Journal of Medicine to significantly reduce neonatal brain injury and improve neurodevelopmental outcomes.

The WHO Newborn Action Plan and national neonatal cooling programs in India, China, and Brazil are expanding institutional cooling device adoption, with companies including Phoenix Medical Systems Pvt. Ltd. and Gentherm Incorporated specifically targeting neonatal hypothermia as a high-growth application segment.

Restraint - Evolving Evidence-Based and TTM Protocol Uncertainty Following TTM2 Trial Outcomes

The TTM2 trial, published in the New England Journal of Medicine in 2021 found no significant survival benefit for hypothermia at 33°C versus normothermia at 37.5°C after out-of-hospital cardiac arrest, creating uncertainty about optimal temperature targets and protocol standardization. This evolving evidence has led some institutions to revise or de-emphasize aggressive cooling protocols, potentially constraining new cooling device procurement in markets where clinical administrators await further evidence consensus from AHA and ERC guideline updates, introducing near-term demand headwinds for certain cooling device categories.

Opportunities - Cooling Catheters: Fastest-Growing Product Segment Driven by Precision Temperature Control Demand

Cooling catheters represent the fastest-growing product segment within the therapeutic hypothermia systems market, offering clinicians superior precision in core body temperature management compared to surface cooling devices. Intravascular cooling catheter systems, including ZOLL Medical's Thermogard XP® and Becton Dickinson's Cool Line® catheter, achieve target temperatures 60–90 minutes faster than surface cooling methods and provide automated closed-loop temperature control, reducing nursing workload in intensive care settings. The Society of Critical Care Medicine (SCCM) has documented clinician preference for catheter-based cooling in complex post-cardiac arrest cases requiring precise, prolonged temperature management. As adoption of evidence-based TTM protocols expands into South Asian and Latin American tertiary hospitals, intravascular catheter platforms are increasingly being specified in new cardiac ICU (CICU) buildouts, positioning the cooling catheter segment for sustained high-growth through 2033.

Asia Pacific Neonatal Care Infrastructure Expansion Creating High-Growth Hypothermia Device Market

Asia Pacific represents the most significant geographic growth opportunity for therapeutic hypothermia system manufacturers, driven by large neonatal populations, high birth asphyxia incidence, and rapidly expanding neonatal intensive care unit (NICU) infrastructure. India, with approximately 25 million annual births per Ministry of Health and Family Welfare (MoHFW) data, has one of the world's highest absolute neonatal HIE burdens.

The Indian National Neonatal Forum (INNF) has published guidelines endorsing therapeutic hypothermia for eligible neonates, driving institutional adoption across tertiary care hospitals. Phoenix Medical Systems Pvt. Ltd. has developed the Tecotherm Neo® neonatal cooling system specifically targeting Indian and emerging market NICU adoption. China's National Health Commission (NHC) hospital expansion program and Japan's Ministry of Health, Labour and Welfare (MHLW)'s reimbursement framework for neonatal cooling collectively underpin a robust and growing regional demand pipeline for therapeutic hypothermia devices through the forecast period.

Category-wise Analysis

Product Type Insights

Cooling devices dominated the therapeutic hypothermia systems market, commanding approximately 43% of total product-type share in 2026. Surface cooling devices encompassing water-circulating blankets, vest-based systems, and gel pad platforms remain the most widely deployed therapeutic hypothermia products due to their non-invasive nature, broad clinical applicability across neurology, cardiology, and neonatal indications, and significantly lower per-use cost compared to intravascular catheter systems.

Leading products include ZOLL Medical's Arctic Sun® 5000 and Stryker Corporation's IntelliCool®, which integrate automated temperature feedback control with patient-friendly gel pad interfaces. The accessibility of surface cooling systems for hospitals with varying levels of critical care infrastructure, including district hospitals and regional medical centers in Asia Pacific and Latin America, sustains their dominant market position across a broad geographic and institutional spectrum.

Application Analysis

Neurology constituted the leading application segment of the therapeutic hypothermia systems market, accounting for approximately 42% demand share in 2026. Neurological applications encompassing post-cardiac arrest cerebral protection, traumatic brain injury (TBI) management, and acute ischemic stroke neuroprotection represent the broadest and most evidence-supported clinical domain for therapeutic hypothermia.

The AHA and Neurocritical Care Society (NCS) both endorse TTM in post-arrest neurological recovery protocols, and over 350,000 annual out-of-hospital cardiac arrest events in the U.S. create a large and consistent patient population requiring neurological temperature management. The European Stroke Organisation (ESO) is actively investigating hypothermia as an adjunct to thrombolysis in ischemic stroke, representing a potential future expansion of neurology application volumes beyond the established post-arrest indication.

End-user Insights

Hospitals dominated the end-user segment of the therapeutic hypothermia systems market, likely to account for approximately 78% of total demand in 2026. The procedural and physiological complexity of therapeutic hypothermia, requiring continuous core temperature monitoring, hemodynamic management, and intensive nursing oversight throughout 12–72 hour cooling protocols, makes hospital-based intensive care units (ICUs), cardiac care units (CCUs), and neonatal intensive care units (NICUs) the overwhelmingly appropriate clinical settings for these devices.

Large academic medical centers and comprehensive stroke centers, such as those certified by the Joint Commission's Comprehensive Stroke Center program, are required to have TTM capability as part of their certification standards. Hospital procurement cycles, CMS reimbursement for TTM procedures in the U.S., and expanding critical care hospital networks in China and India collectively sustain hospital segment market dominance.

Regional Insights

North America Therapeutic Hypothermia Systems Market Trends and Insights

North America is a dominant region for therapeutic hypothermia systems, with approximately 39% share in 2026, driven by AHA-mandated TTM protocols in post-cardiac arrest care, CMS reimbursement coverage for therapeutic hypothermia procedures, established critical care infrastructure, and ZOLL Medical Corporation and Gentherm Incorporated, headquartered within the region.

The region also benefits from high ICU bed availability, strong physician awareness, and increasing adoption of advanced surface and intravascular cooling technologies. Ongoing investments in emergency response systems and neurocritical care programs continue to support sustained market growth. Additionally, growing emphasis on reducing neurological damage following cardiac arrest and increasing utilization of evidence-based temperature management practices across hospitals are supporting long-term demand for therapeutic hypothermia systems.

U.S. Therapeutic Hypothermia Systems Market Size

The U.S. accounts for approximately 88% of North American market revenues, anchored by 350,000+ annual cardiac arrest events per AHA, Joint Commission-certified comprehensive stroke centers requiring TTM capability, and strong commercial positions of ZOLL Medical's Arctic Sun® and Stryker's IntelliCool® in hospital ICU installations nationwide. The country's advanced healthcare expenditure, extensive hospital network, and continuous clinical research evaluating targeted temperature management strategies further reinforce market leadership and technology adoption.

Europe Therapeutic Hypothermia Systems Market Trends and Insights

Europe is the second-largest regional market, shaped by European Resuscitation Council (ERC) 2021 Guidelines endorsing TTM, universal healthcare coverage providing consistent procedure reimbursement, and home-market innovation from BrainCool AB (Sweden), Getinge AB, and Koninklijke Philips N.V. Germany and Scandinavia demonstrate the highest per-capita therapeutic hypothermia device adoption rates in the region. Increasing focus on improving post-resuscitation survival rates and growing investments in neonatal intensive care services are further contributing to market expansion across major European countries.

Germany Therapeutic Hypothermia Systems Market Size

Germany leads European therapeutic hypothermia device adoption, supported by approximately 75,000 annual cardiac arrests per German Resuscitation Council (GRC) data and GKV statutory insurance coverage for post-resuscitation TTM. Germany's dense network of cardiac catheterization laboratories and certified stroke centers drives consistent cooling device procurement, with Getinge AB and ZOLL Medical maintaining strong commercial presences.

UK Therapeutic Hypothermia Systems Market Size

UK therapeutic hypothermia market benefits from NHS England commissioning standards mandating TTM capability in cardiac arrest centers and NICU services. Approximately 30,000 out-of-hospital cardiac arrests are treated annually per British Heart Foundation (BHF) data, generating consistent cooling device demand. BrainCool AB's RhinoChill® and Stryker products are widely deployed in NHS critical care networks. Rising attention toward standardized post-cardiac arrest pathways and ongoing modernization of intensive care facilities are expected to support future adoption of advanced hypothermia management technologies.

France Therapeutic Hypothermia Systems Market Size

France's therapeutic hypothermia market is sustained by Sécurité Sociale reimbursement for post-arrest TTM and robust critical care ICU networks managing approximately 40,000 annual cardiac arrests per French Institute of Public Health Surveillance estimates. Koninklijke Philips N.V. and Getinge AB maintain strong French hospital commercial presences through established medical device distributor networks. The growing adoption of evidence-based neurological protection protocols and increasing investments in emergency medicine infrastructure are further strengthening demand for therapeutic hypothermia solutions.

Asia Pacific Therapeutic Hypothermia Systems Market Trends and Insights

Asia Pacific is the fastest-growing regional market for therapeutic hypothermia systems, driven by India's 25 million annual births creating high neonatal HIE device demand, expanding Chinese NICU and cardiac ICU infrastructure under Healthy China 2030, and growing clinical awareness of TTM protocols. China's NHC is actively adding tertiary hospital capacity that includes cardiac arrest management protocols incorporating therapeutic hypothermia capability. Rapid healthcare infrastructure development, increasing healthcare expenditure, and rising adoption of advanced critical care technologies across emerging economies are accelerating regional market growth.

Japan Therapeutic Hypothermia Systems Market Size

Japan represents a premium therapeutic hypothermia market, with MHLW national health insurance reimbursement for post-arrest TTM and neonatal hypothermia established. Terumo Corporation and Asahi Kasei Corporation serve domestic cooling device demand. Japan's 120+ certified cardiac arrest centers per Japan Resuscitation Council (JRC) standards maintain consistent high-specification cooling device procurement. Strong emphasis on clinical quality standards, an aging population vulnerable to cardiovascular events, and rapid adoption of technologically advanced medical devices continue to support market expansion.

Southeast Asia Therapeutic Hypothermia Systems Market Size

Southeast Asia is an emerging therapeutic hypothermia market, with Thailand, Singapore, and Vietnam investing in critical care and NICU infrastructure. Singapore's advanced cardiac care network and Thailand's medical tourism infrastructure are driving premium cooling device adoption. Shenzhen Comen Medical Instruments Co., Ltd. serves cost-sensitive Southeast Asian markets with competitive hypothermia products. Rising healthcare investments, increasing awareness of neonatal hypoxic-ischemic encephalopathy management, and gradual expansion of tertiary care facilities are expected to create significant opportunities for market participants across the region.

Competitive Landscape

The global therapeutic hypothermia systems market is highly competitive, driven by continuous innovation in patient temperature management technologies used in critical care settings. Market participants focus on developing advanced, precise, and non-invasive cooling solutions that improve patient outcomes in cardiac arrest, neurological injury, and neonatal care. Competition is shaped by product differentiation, ease of use, safety performance, and integration with ICU monitoring systems. Companies are increasingly investing in portable and automated systems to enhance clinical efficiency and reduce response time.

Key Developments:

- In July 2025, Medline launched the ComfortTemp® Patient Warming System, a new forced-air warming solution designed to help maintain and regulate patient body temperature during pre-, intra-, and post-operative care.

- In May 2025, TEQCool AB announced its patented non-invasive intranasal brain cooling system, extending its application beyond the conventional therapeutic hypothermia market and targeting the global market for brain metabolism reduction.

- In January 2024, SourceMark announced a partnership with Gentherm Medical to become the master supplier of certain Gentherm product lines in the U.S., including the Gelli-Roll, a reusable warming and cooling gel pad.

Companies Covered in Therapeutic Hypothermia Systems Market

- ZOLL Medical Corporation

- Becton, Dickinson and Company

- Stryker Corporation

- Gentherm Incorporated

- BrainCool AB

- Belmont Medical Technologies

- Asahi Kasei Corporation

- Terumo Corporation

- Getinge AB

- Koninklijke Philips N.V.

- Phoenix Medical Systems Pvt. Ltd.

- Shenzhen Comen Medical Instruments Co., Ltd.

Frequently Asked Questions

The global therapeutic hypothermia systems market is expected to be valued at US$ 383.5 million in 2026.

Key drivers include AHA 2020 and ERC 2021 guidelines mandating TTM at 32–36°C for post-cardiac arrest patients, 350,000+ annual U.S. cardiac arrests per AHA, WHO-estimated 1 million annual neonatal HIE cases, and Lancet/NEJM clinical evidence supporting neonatal cooling for improved neurodevelopmental outcomes.

North America leads with approximately 39% global market share in 2025, driven by AHA-mandated TTM protocols, CMS procedure reimbursement, Joint Commission-certified stroke center TTM requirements, and ZOLL Medical's Arctic Sun® and Gentherm's Blanketrol® commercial dominance in U.S. hospital ICU installations.

The most significant opportunities include cooling catheters achieving 60–90-minute faster target temperature onset per SCCM data and Asia Pacific neonatal hypothermia expansion through India's INNF guidelines, 25 million annual births, and Phoenix Medical Systems' emerging market-targeted Tecotherm Neo® neonatal cooling platform.

Leading companies include ZOLL Medical Corporation (Arctic Sun®), Stryker Corporation, Gentherm Incorporated (Blanketrol®), Getinge AB, Becton, Dickinson and Company, BrainCool AB, Terumo Corporation, and Phoenix Medical Systems Pvt. Ltd