- Food Ingredients & Additives

- Fortified Sugars Market

Fortified Sugars Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Fortified Sugars Market by Micronutrients Type (Vitamins, Minerals, Other Fortifying Nutrients), Technology (Drying, Extrusion, Coating & Encapsulation, Others), Sales Channel (Modern Trade, Convenience Stores, Online Stores, Others), and Regional Analysis from 2025 to 2032

Fortified Sugars Market Share and Trends Analysis

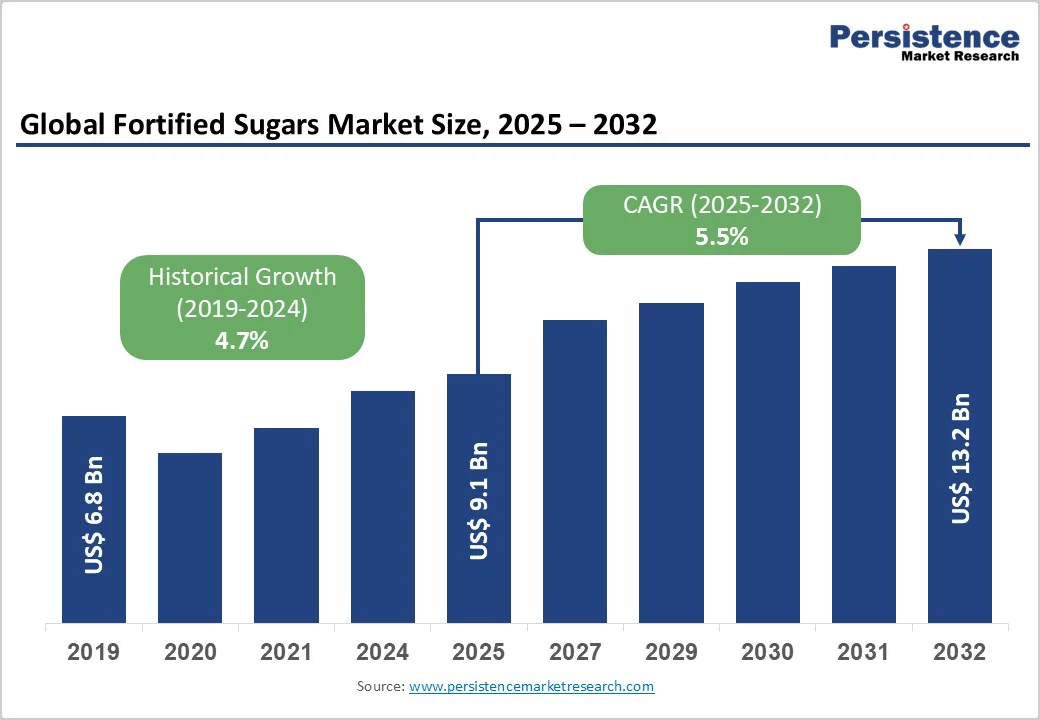

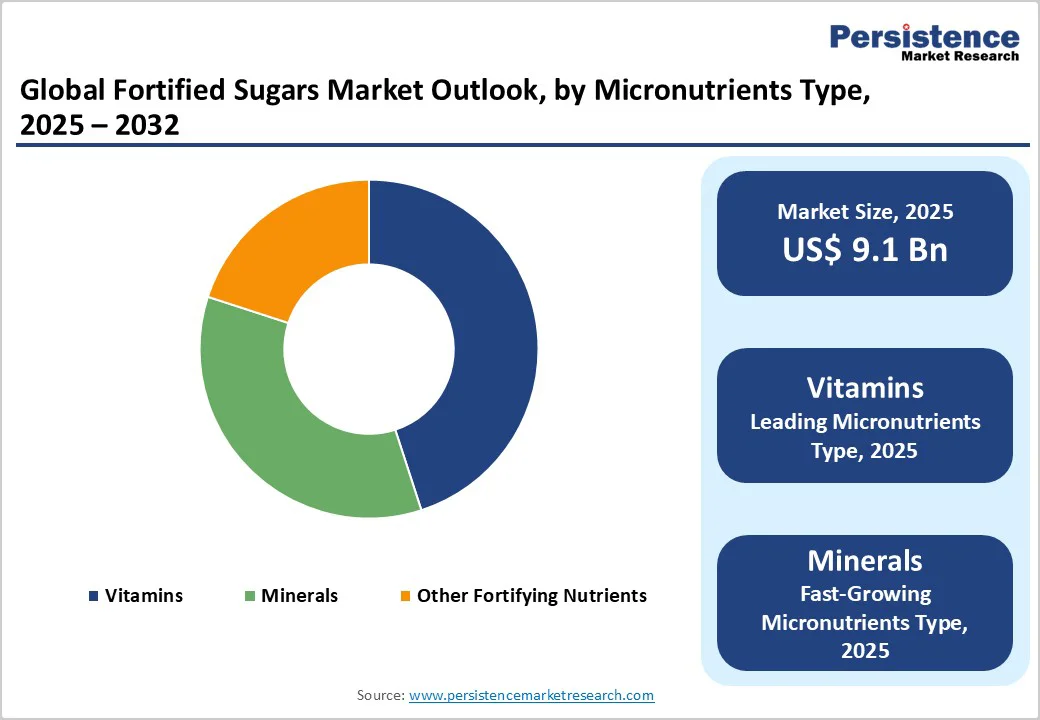

The global fortified sugars market size is likely to value US$ 9.1 billion in 2025 and is projected to reach US$ 13.2 billion, growing at a CAGR of 5.5% during the forecast period from 2025 to 2032.

Rise in health awareness, increasing demand for nutrient-enriched foods, and government-supported fortification programs. Asia Pacific leads the market due to high consumption and deficiency-prevention initiatives, while North America and Europe follow with strong adoption in processed foods, beverages, and functional nutrition products.

Key Industry Highlights:

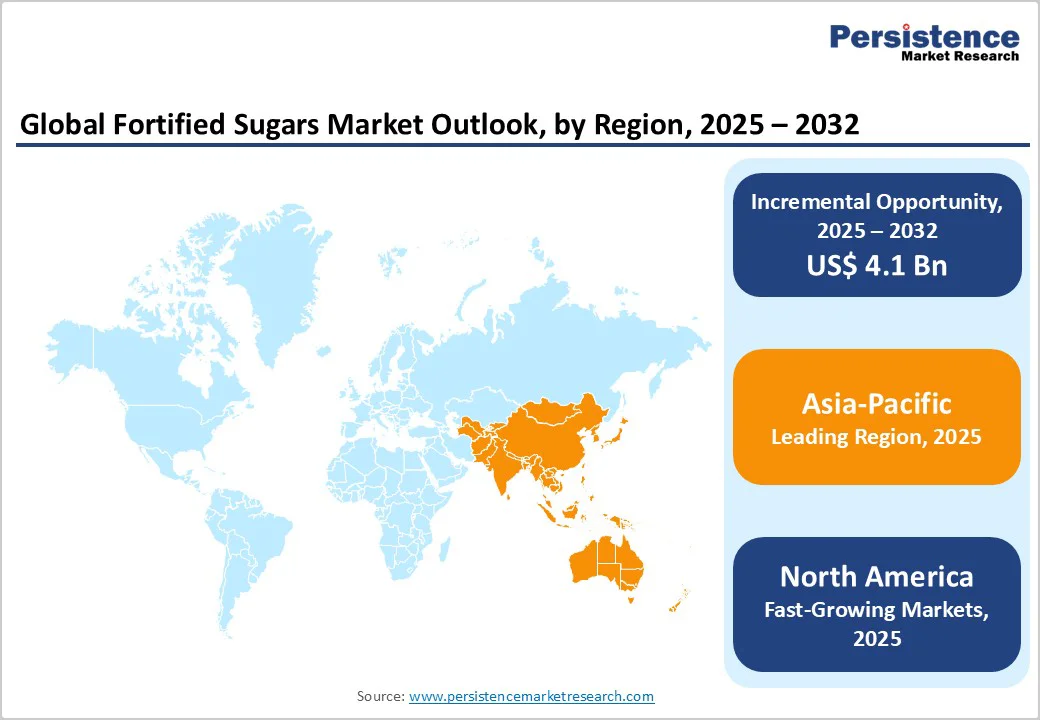

- Leading Region: Asia Pacific, holding nearly 35.3% market share in 2025, driven by government-led fortification programs, high sugar consumption, and large-scale production in countries like India, China, and Thailand.

- Fastest-growing Region: North America, fueled by increasing demand for fortified and functional foods, rising health awareness, and product innovation in nutrient-enriched sweeteners and beverages.

- Investment Plans: Europe, focusing on sustainable fortification technologies, micronutrient stability research, and compliance with EU fortification regulations to enhance product quality and nutritional impact.

- Dominant Product: Vitamin-Fortified Sugar, capturing nearly 46.3% market share, due to its effectiveness in addressing deficiencies and wide application across food, beverage, and confectionery sectors.

- Growth Indicator: Increasing prevalence of micronutrient deficiencies, rising health awareness, and government-led food fortification initiatives are driving the Fortified Sugars Market. Growing use of fortified sugar in processed foods, beverages, and household consumption further supports market expansion.

- Opportunity: Expanding adoption of vitamin- and mineral-enriched sugars, innovations in fortification technologies, and growing demand in emerging economies present significant opportunities for fortified sugar manufacturers.

| Key Insights | Details |

|---|---|

| Global Fortified Sugars Market Size (2025E) | US$ 9.1 Bn |

| Market Value Forecast (2032F) | US$ 13.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.7% |

Market Dynamics

Driver - Rising Health Awareness and Government Fortification Initiatives Fueling Growth Across Food and Beverage Applications

Rising health awareness and government-driven food fortification policies are major forces propelling the market. According to the WHO, over 2 billion people globally are deficient in essential vitamins and minerals such as vitamin A, iodine, iron, and zinc. In India, every second child under five suffers from malnutrition stunting, wasting or micronutrient deficiency, with anaemia affecting nearly half the children, according to UNICEF.

These alarming data prompt governments to mandate fortification of staples, create legislation and standards, and promote fortified products. As consumers grow more health-conscious and seek out nutrient-rich diets, fortified sugars present an accessible way to deliver micronutrients. The combination of public health need and supportive regulation thus creates a strong foundation for market growth.

Restraints - Challenges of Nutrient Stability

Nutrient stability challenges significantly constrain the market, particularly concerning the degradation of added vitamins and minerals during processing, storage, and transportation. For instance, vitamin A, a common fortificant in sugar, is highly sensitive to light, heat, and oxygen exposure. Studies have shown that losses of up to 40% can occur in fortified sugar products under suboptimal storage conditions.

Similarly, vitamin D, when added to sugar, requires precise processing and packaging to maintain its stability; improper handling can lead to significant nutrient loss. These stability issues necessitate the use of advanced technologies such as microencapsulation and specialized packaging, which increase production costs.

Furthermore, the need for overages-additional amounts of nutrients added to compensate for expected losses-can further elevate costs and complicate manufacturing processes. These factors collectively pose substantial challenges to the widespread adoption and affordability of fortified sugars, particularly in regions with limited access to advanced fortification technologies.

Opportunity - Integration with Functional Foods and Nutraceuticals

The integration of fortified sugars into functional foods and nutraceuticals presents a significant opportunity for market expansion, particularly in India. Functional foods, which include products enhanced with additional nutrients, are gaining popularity as consumers seek convenient ways to improve their health.

The Food Safety and Standards Authority of India (FSSAI) regulates these products under the Food Safety and Standards (Health Supplements, Nutraceuticals, Food for Special Dietary Use, Food for Special Medical Purpose, Functional Food and Novel Food) Regulations, 2016, ensuring safety and quality.

By fortifying sugars with essential nutrients like vitamins and minerals, manufacturers can cater to the growing demand for functional foods, thereby tapping into a lucrative market segment.

Category-wise Analysis

By Micronutrients Type, Vitamins dominate the Fortified Sugars Market

Vitamins dominate with a 46.3% share in 2025 due to their critical role in addressing widespread micronutrient deficiencies, particularly in developing countries.

For instance, iron deficiency anemia affects approximately 58.5% of children in India, with vitamin A deficiency being a leading cause of preventable blindness in children Press Information Bureau. The World Health Organization (WHO) identifies iron, vitamin A, and iodine deficiencies as the most prevalent globally, especially among children and pregnant women World Health Organization.

In response, governments have implemented large-scale fortification programs. In India, for example, the government has fortified wheat flour and rice with iron, folic acid, and vitamin B12 to combat these deficiencies. These initiatives highlight the emphasis on vitamins in fortification efforts, driving their dominance in the fortified sugars market.

By Technology, Drying is Gaining Traction Due to Efficiently Removing Moisture While Preserving Vitamin and Nutrient Stability

Drying is the dominant technology in the market due to its efficiency and compatibility with large-scale sugar production processes. This method effectively removes excess moisture from sugar crystals, preventing clumping and discoloration during storage and transport. For instance, rotary dryers, commonly used in sugar processing, employ high temperatures to achieve rapid moisture removal, ensuring a consistent and high-quality final product.

Additionally, the drying process is crucial for maintaining the stability of added nutrients. Studies have shown that drying fortified sugar at temperatures below 80°C can preserve the stability of vitamins, such as vitamin A, ensuring their efficacy in addressing nutritional deficiencies. Furthermore, drying facilitates the incorporation of fortified nutrients into sugar without compromising its quality, making it a preferred method in the industry.

Regional Insights

Asia Pacific Fortified Sugars Market Trends

Asia Pacific dominates the global market with a 35.3% share in 2025, due to high population, widespread micronutrient deficiencies, and strong government fortification programs. In India, for example, nearly 58.5% of children suffer from anemia, and vitamin A deficiency affects millions of children under five. Governments in the region mandate or encourage fortification of staples like sugar, wheat, and rice to combat deficiencies.

Large-scale production in countries like India, China, Vietnam, and Indonesia, combined with rising domestic consumption in the food and beverage industries, further drives market dominance. Public health initiatives, such as programs empowering millers to produce nutrient-enriched foods and increasing consumer awareness about health benefits of fortified products, make Asia Pacific the leading region in fortified sugar adoption globally.

Europe Fortified Sugars Market Trends

Europe is a significant market poised to account for a 22.1% share in 2025, due to its proactive approach to combating micronutrient deficiencies and its robust regulatory framework. The European Food Safety Authority (EFSA) has established Dietary Reference Values (DRVs) to guide nutrient intake, highlighting the importance of fortification in addressing nutritional gaps.

Additionally, the European Commission's initiatives emphasize food fortification strategies to improve public health outcomes. These efforts are complemented by widespread consumer awareness and demand for healthier food options, further driving the adoption of fortified products. The combination of scientific backing, regulatory support, and consumer preference positions Europe as a significant player in the fortified sugars sector.

North America Fortified Sugars Market Trends

North America is the fastest-growing region in the market based on health awareness, government nutrition initiatives, and strong consumer demand for functional foods. The U.S. and Canada have high rates of micronutrient deficiencies in certain populations; for example, nearly 10% of Americans have iron deficiency, and around 3% of adults are vitamin D deficient.

Government programs and guidelines, such as the U.S. FDA’s fortification recommendations and dietary guidelines, encourage adding essential vitamins and minerals to staple foods. Consumers are increasingly seeking nutrient-enriched products in bakery items, beverages, and confectionery, while modern retail and online channels improve accessibility. Combined, these factors make North America a rapidly expanding market for fortified sugars.

Competitive Landscape

The global fortified sugars market is expanding as manufacturers adopt advanced fortification, processing, and quality-control techniques. Leading producers focus on nutrient stability and shelf life, while emerging players target organic and specialty segments. Strategic initiatives like sustainable sourcing, traceability, and partnerships enhance competitiveness, boost adoption in food, beverages, and confectionery, and drive overall market growth.

Key Industry Developments:

- In July 2025, the Mozambican government announced a significant achievement in its National Fortification Programme, reporting the sale of over 13 million tonnes of fortified food products, including maize flour, wheat flour, sugar, cooking oil, and iodized salt, over the past six years. This initiative aims to combat nutritional deficiencies by adding essential micronutrients to staple foods.

- In November 2023, the National Sugar Institute (NSI) in Kanpur announced a significant breakthrough in sugar technology. After years of extensive research, NSI developed a technique for producing Low Glycemic Index (Low GI) sugar and fortified sugar, both with a shelf life of one year under standard storage conditions.

Companies Covered in Fortified Sugars Market

- Cargill Inc.

- Bunge Limited

- Bühler AG

- BASF SE

- General Mills, Inc

- Koninklijke D.S.M.

- Wilmar International Limited

- Tereos SA

- Nordzucker AG

- Associated British Foods Plc.

- Dangote Sugar Refinery PLC

- BUA Foods

- Amalgamated Sugar

- American Crystal Sugar Co

- Tate & Lyle PLC

- Ingredion Incorporated

- Archer Daniels Midland Company

- Louis Dreyfus Company

- Sucden Group

- Südzucker AG

- Others

Frequently Asked Questions

The global fortified sugars market is projected to be valued at US$ 9.1 Bn in 2025.

Rising micronutrient deficiencies, health awareness, government fortification programs, and growing food and beverage applications drive growth.

The global fortified sugars market is poised to witness a CAGR of 5.5% between 2025 and 2032.

Expanding functional foods, emerging economies, advanced fortification technologies, and government nutrition programs create significant market opportunities.

Major players in the global are Cargill Inc., Bunge Limited, Bühler AG, BASF SE, General Mills, Inc, Koninklijke D.S.M., and Others.