- Food Ingredients & Additives

- Invert Sugar Syrups Market

Invert Sugar Syrups Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Invert Sugar Syrups Market by Product Type (Fully Inverted Sugar, Partially Inverted Sugar), by Nature (Organic, Conventional), by End Use (Bakery & Confectionery, Beverages, Dairy & Frozen Desserts, Pharmaceutical, Processed Foods, Others), by Regional Analysis, 2026-2033

Invert Sugar Syrups Market Share and Trends Analysis

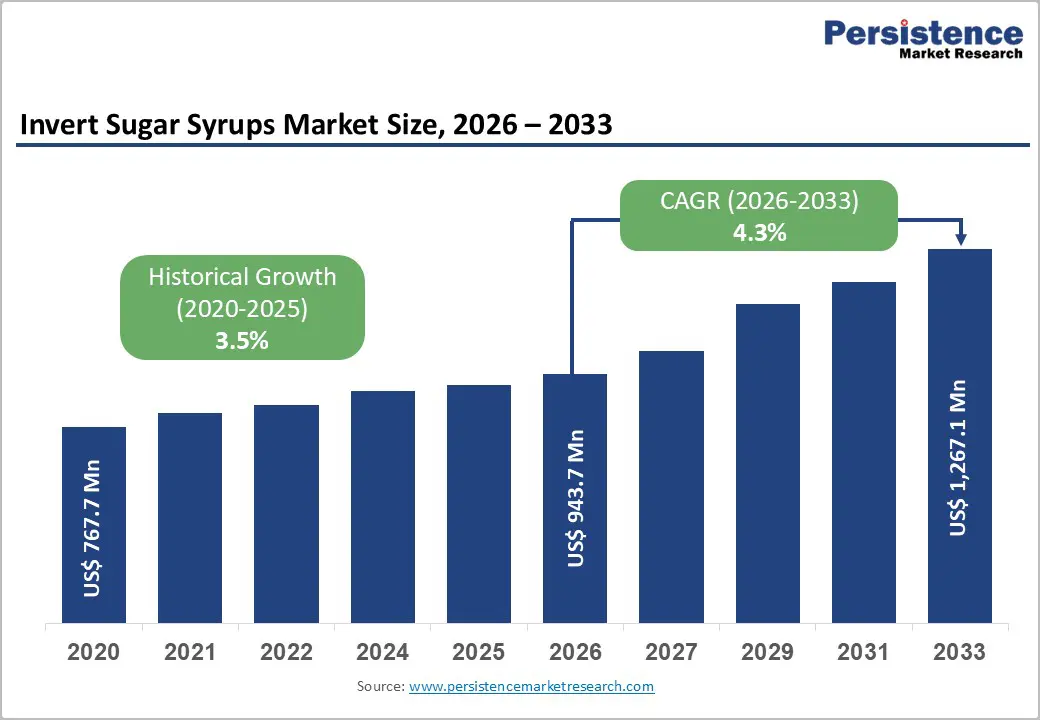

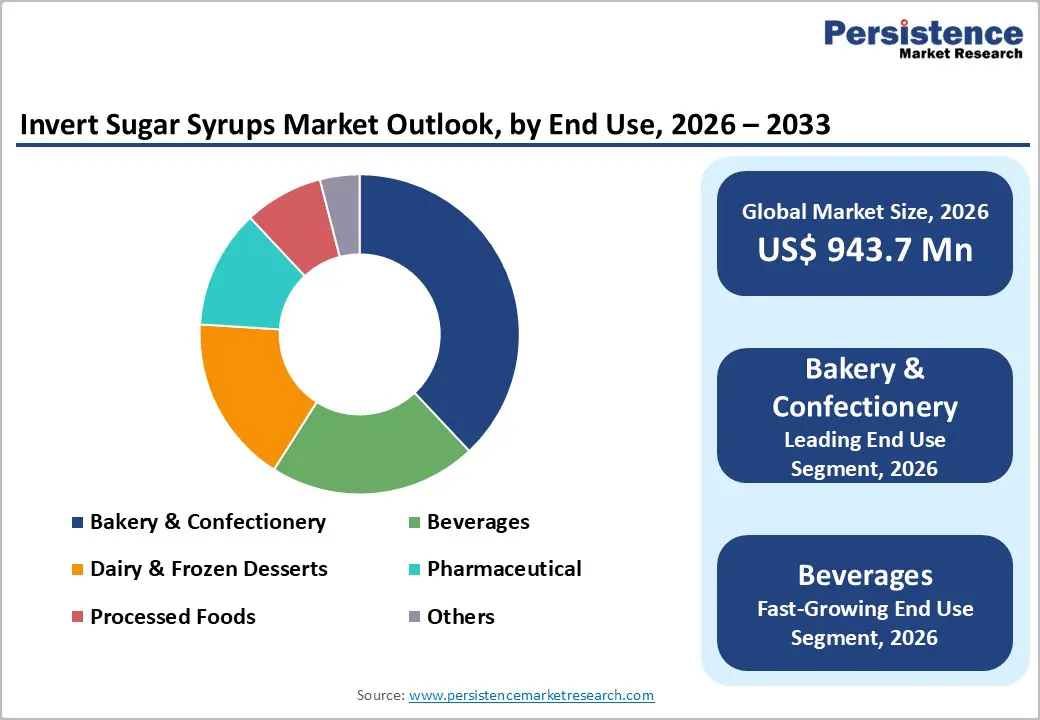

The global invert sugar syrups market size is expected to be valued at US$ 943.7 million in 2026 and projected to reach US$ 1,267.1 million by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

Invert sugar syrups sit quietly behind some of the world’s fastest-moving beverage and food production lines, enabling efficiency, consistency, and fermentation control. As formulation science and clean-label priorities advance, these liquid sweeteners are evolving from commodity inputs into strategic processing ingredients.

Key Industry Highlights

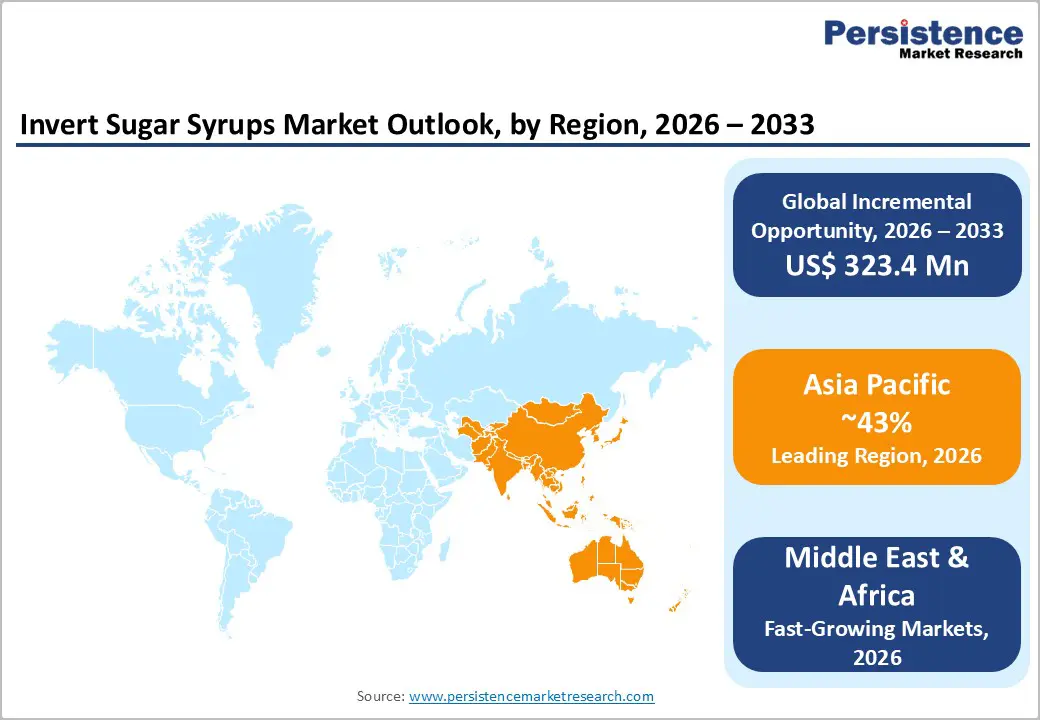

- Leading Region: Asia Pacific, holding approximately 43% market share, driven by large-scale beverage manufacturing, fermentation-led applications, and rapid modernization of food processing infrastructure across India, China, Japan, and South Korea.

- Fastest-Growing Region: Middle East & Africa, supported by expanding food processing capacity, rising beverage production in GCC countries, and strong demand for heat-stable, low-crystallization sweeteners in warm climates.

- Dominant Product Type Segment: Fully inverted sugar syrup, favored for its balanced glucose-fructose profile, superior solubility, rapid fermentability, and consistent performance across beverages, confectionery, and industrial fermentation.

- Market Drivers: Rising adoption in beverage and fermentation industries where readily fermentable sugars improve yeast efficiency, reduce processing variability, and support high-throughput production.

- Opportunities: Premium positioning through organic and non-GMO invert sugar syrups, enabling higher margins, differentiated export offerings, and alignment with clean-label and transparent sourcing expectations.

- Key Developments: In September 2025, Nordzucker initiated sugar beet processing for the 2025/2026 campaign, strengthening raw material availability across its European production network.

| Key Insights | Details |

|---|---|

| Global Invert sugar syrups Market Size (2026E) | US$ 943.7 Mn |

| Market Value Forecast (2033F) | US$ 1,267.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Dynamics

Driver - Growth in beverage and fermentation industries increases demand for readily fermentable sugars

Fermentation tanks are becoming quiet engines of growth for invert sugar syrups as beverage producers chase efficiency and flavor consistency. Inverted sugars offer immediate yeast accessibility, accelerating fermentation while reducing process variability in alcoholic drinks, kombucha, kefir, and functional beverages. Faster sugar uptake improves throughput, helping producers scale volumes without extending production cycles. Beverage formulators also value invert syrup’s uniform sweetness and solubility, which support stable taste profiles across batches.

Beyond alcohol, fermentation-driven demand is expanding in non-alcoholic segments where sugar breakdown matters are controlled. Craft beverage makers and bio-ingredient producers increasingly prefer fermentable sugars to reduce residual sweetness and improve product clarity. Invert sugar syrup simplifies formulation, lower processing risk, and aligns with clean fermentation practices. As fermentation-driven innovation spreads across beverage categories, demand for highly fermentable sugar solutions strengthens structurally.

Restraints - Availability of alternative sweeteners increases formulation competition

Sweetening strategies are evolving rapidly, intensifying competition for invert sugar syrups. Food and beverage developers now evaluate high-intensity sweeteners, polyols, fruit concentrates, and starch-derived syrups alongside traditional sugar systems. These alternatives offer varying benefits such as sweetness amplification, calorie reduction, or functional claims, challenging invert sugar’s positioning in cost-sensitive or reformulation-driven applications.

This expanding toolbox complicates ingredient selection decisions for manufacturers. Formulators often blend multiple sweeteners to optimize taste, cost, and labeling outcomes, reducing reliance on single sugar inputs. Alternative sweeteners also attract innovation budgets as brands respond to sugar reduction narratives. While invert sugar syrups retain functional strengths, rising substitution options pressure volumes and pricing, especially in applications where fermentation performance or browning control is not critical.

Opportunity - Organic and non-GMO invert sugar syrups open premium positioning

Ingredient stories are becoming as important as functionality, creating premium space for organic and non-GMO invert sugar syrups. Food brands increasingly seek sweeteners that support clean sourcing narratives while delivering reliable performance. Certified organic invert syrups align with transparency-focused product lines, particularly in beverages, bakeries, and specialty foods targeting wellness-driven consumers.

For key players and new startups, this segment enables value creation beyond commodity pricing. Organic positioning supports higher margins, limited-batch launches, and differentiated export offerings. Non-GMO credentials resonate strongly in regions where ingredient scrutiny influences purchasing decisions. Smaller producers can enter through niche certifications and localized sourcing, while larger players leverage scale to serve premium B2B customers. As clean-label expectations intensify, organic and non-GMO invert sugar syrups become strategic growth levers.

Category-wise Analysis

By Product Type, fully inverted sugar syrup dominates the global market

Fully inverted sugar syrup holds approx. 62% market share as of 2025, reflecting its broad functional reliability across food and beverage applications. Complete inversion delivers balanced glucose and fructose composition, ensuring rapid fermentability, stable sweetness, and reduced crystallization risk. These attributes make it the preferred option for beverages, confectionery, and fermentation-led processes.

Manufacturers favor fully inverted formats due to predictable behavior during heating, storage, and formulation. Its superior solubility supports consistent quality in high-volume production environments. From a processing perspective, full inversion simplifies downstream adjustments and minimizes formulation errors. This versatility, combined with established production infrastructure, reinforces dominance. As industries prioritize efficiency and consistency, fully inverted sugar syrup remains the benchmark product type globally.

By End-user, beverages are anticipated to register strong growth during the forecast period

Beverages is projected to grow at a CAGR of 6.8% during the forecast period as liquid formulations increasingly demand functional sweeteners. Invert sugar syrups integrate seamlessly into carbonated drinks, energy beverages, fermented drinks, and flavored waters. Their rapid solubility and uniform sweetness support high-speed bottling operations and consistent sensory outcomes.

Beverage brands also rely on invert sugar to manage mouthfeel and flavor release without excessive sweetness spikes. Fermentation-based beverages benefit from improved yeast performance and controlled sugar conversion. As product innovation accelerates across functional and indulgent drinks, invert sugar syrups offer formulation flexibility without complex processing adjustments. Expanding beverage diversity directly strengthens this end-use segment’s growth momentum.

Regional Insights

Asia Pacific Invert Sugar Syrups Market Trends

Asia Pacific holds approximately 43% market share in the global Invert sugar syrups Market, driven by expanding beverage manufacturing and food processing capacity. India shows rising use in traditional sweets, bakery, and fermentation-linked beverages. China accelerates demand through large-scale beverage production and industrial fermentation applications.

Japan emphasizes precision formulation, favoring invert syrups for controlled sweetness and processing stability. South Korea integrates invert sugar into functional drinks and confectionery innovations. Regional manufacturers invest in local production to reduce import dependency and improve supply responsiveness. Growth is supported by urban consumption patterns and modernization of food infrastructure. As Asia Pacific balances scale with innovation, invert sugar syrups remain central to efficient, high-volume sweetening strategies.

Middle East & Africa Invert Sugar Syrups Market Trends

Middle East & Africa Invert sugar syrups Market is expected to grow at a CAGR of 7.8% as food processing expands across developing economies. Egypt shows rising adoption in confectionery and bakery production, supporting domestic consumption. GCC countries drive demand through beverage manufacturing and foodservice growth.

Across African markets, invert sugar syrups gain traction due to stability advantages in warm climates. Reduced crystallization risk and liquid handling suitability support adoption in beverages and sauces. Regional investments in sugar refining and food manufacturing improve local availability. As processed food penetration rises, invert sugar syrups offer a practical sweetening solution aligned with infrastructure and climate realities.

Competitive Landscape

The global Invert sugar syrups Market is moderately consolidated, with established producers competing alongside regional specialists. Leading companies pursue backward integration into sugar processing to secure supply and manage cost volatility. Long-term B2B partnerships with beverage, bakery, and fermentation players strengthen demand stability.

Competition increasingly centers on certifications, sustainability practices, and application-specific innovation. Producers invest in energy-efficient processing and cleaner inversion methods to support export opportunities in developing countries. Regulatory compliance shapes formulation and labeling strategies across regions. As governments tighten food standards, operational discipline and supply-chain control define competitive advantages.

Key Developments:

- In September 2025, Nordzucker announced the start of sugar beet processing for the 2025/2026 campaign, with operations commencing in early September across its European manufacturing facilities.

Companies Covered in Invert Sugar Syrups Market

- ASR Group

- ADM

- Südzucker AG

- Cosun Beet Company

- Malt Products Corporation

- Nordzucker

- Belgosuc

- Golden Barrel

- Invert Sugar India Ltd.

- Agrana Beteiligungs AG

- Tereos

- Others

Frequently Asked Questions

The global invert sugar syrups market is projected to be valued at US$ 943.7 Mn in 2026.

The global invert sugar syrups market is driven by expanding beverage and fermentation industries that increasingly require readily fermentable sugars for efficient processing, consistent fermentation performance, and improved product quality.

The global invert sugar syrups market is poised to witness a CAGR of 4.3% between 2026 and 2033.

Organic and non-GMO invert sugar syrups open premium positioning is key opportunity.

Major players in the global Invert sugar syrups market include ASR Group, ADM, Südzucker AG, Nordzucker, Belgosuc, Agrana Beteiligungs AG, Tereos, Others, and others.