- Food Ingredients & Additives

- Specialty Sugars Market

Specialty Sugars Market Size, Share, and Growth Forecast 2026 - 2033

Specialty Sugars Market by Product Type (Caster Sugar, Icing Sugar, Muscovado Sugar, Demerara Sugar, Others), by Nature (Organic, Conventional), Application (Bakery & Confectionery, Beverages, Dairy & Desserts, Pharmaceuticals & Nutraceuticals, Personal Care & Cosmetics, Others), by Regional Analysis, 2026 - 2033

Specialty Sugars Market Share and Trends Analysis

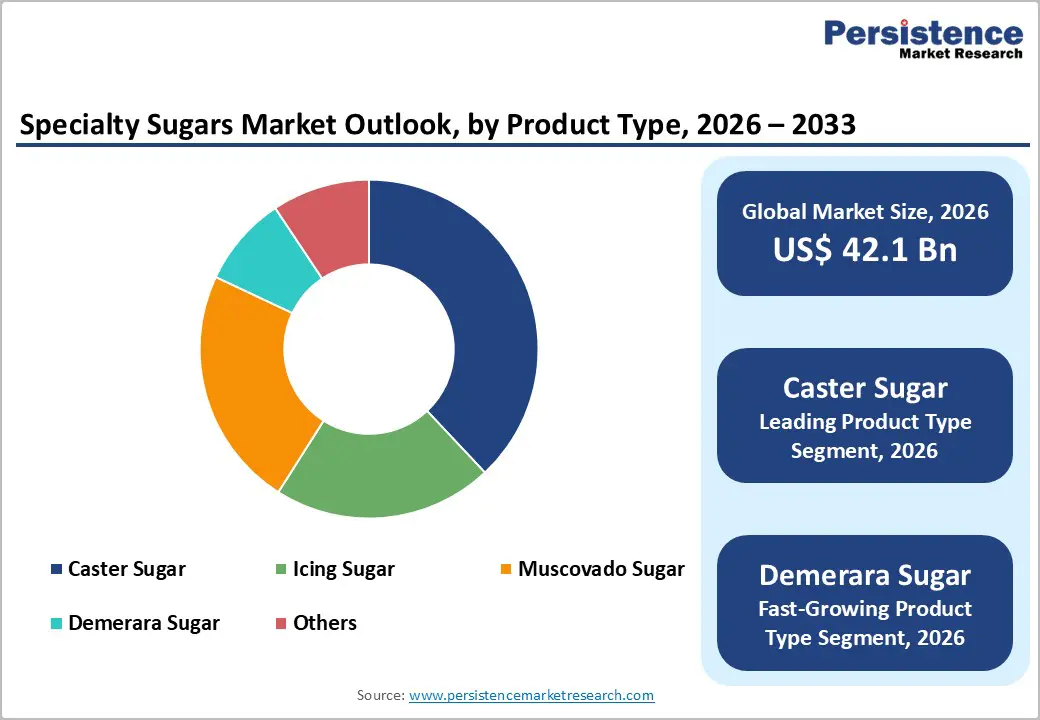

The global specialty sugars market size is expected to be valued at US$ 42.1 billion in 2026 and projected to reach US$ 60.6 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

Rising demand for premium and artisanal food products drives this growth, supported by health-conscious consumer preferences and expansion in bakery and confectionery sectors. The bakery industry consumes approximately 30% of specialty sugars globally due to their unique textures and flavors essential for high-quality baked goods. Additionally, increasing use in beverages and functional foods, fueled by clean-label trends, bolsters market expansion as manufacturers seek natural alternatives to refined sugars.

Key Industry Highlights:

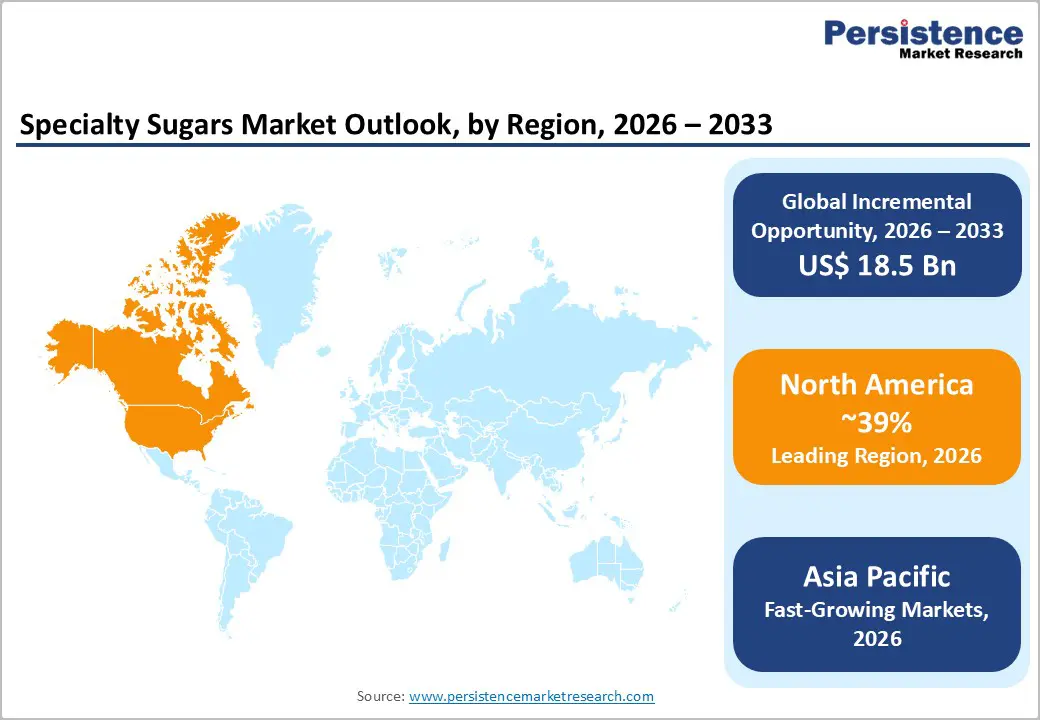

- North America dominates specialty sugars with 39% share in 2025, led by U.S. innovation and regulatory support for premium bakery applications.

- Asia Pacific grows fastest, propelled by urbanization in China and India demanding organic and Demerara variants.

- Caster Sugar leads product types at 38% share, essential for bakery texture and aeration globally.

- Demerara Sugar emerges fastest-growing, riding natural sweetener trends in beverages.

- Pharmaceuticals expansion offers key opportunity via functional sugars enhancing bioavailability.

| Key Insights | Details |

|---|---|

| Specialty Sugars Size (2026E) | US$ 42.1 billion |

| Market Value Forecast (2033F) | US$ 60.6 billion |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.7% |

Market Dynamics

Drivers - Rising Demand in Bakery and Confectionery

The bakery and confectionery sector's robust expansion significantly propels the specialty sugars market, accounting for around 30% of global consumption. High demand stems from specialty sugars like caster and icing varieties, which provide superior texture, aeration, and crystallization crucial for premium products such as artisan breads, cakes, and chocolates. According to industry analyses, the global bakery market's growth at over 5% CAGR reflects busy lifestyles and increased snacking, driving consistent uptake. This trend is evident in Europe and North America, where artisan baking has surged, with USDA data showing rising imports of specialty sweeteners for food manufacturing. Consequently, manufacturers benefit from stable volumes as food processors prioritize flavor enhancement and visual appeal, ensuring positive revenue impacts.

Health and Wellness Trends Favoring Natural Sweeteners

Consumer shift toward natural, less-processed sweeteners boosts specialty sugars, particularly organic and minimally refined types like Demerara and Muscovado. With global health awareness rising, FAO reports indicate a 15% annual increase in demand for organic sugars in food applications since 2020, driven by preferences for clean-label products. This is supported by dietary pattern changes, including higher beverage and dairy consumption, where specialty sugars offer distinct flavors without artificial additives. In regions like Asia Pacific, urbanization has amplified this, with middle-class expansion leading to 6-7% growth in premium ingredient use. These dynamics create sustained demand, enabling market participants to capitalize on premium pricing and loyalty from health-focused buyers.

Restraints - Fluctuations in Raw Material Costs

The specialty sugars market is highly sensitive to the volatility of raw material prices, particularly sugarcane and sugar beets, which form the backbone of production. Sudden increases in procurement costs directly affect manufacturing margins, especially for premium or labor-intensive variants such as Demerara and Muscovado sugar. According to Trading Economics, sugar prices surged by 5.13% in early 2026 due to supply chain disruptions, unpredictable weather, and crop yield inconsistencies, intensifying pressure on specialty sugar producers. These fluctuations make cost forecasting challenging, discouraging investment in niche processing facilities and limiting production scalability in price-sensitive regions. For manufacturers relying on consistent raw inputs to maintain uniform quality and texture, the unpredictability of raw material availability can lead to delayed deliveries, higher operational costs, and diminished competitiveness in both domestic and international markets, restraining overall market growth.

Competition from Sugar Substitutes

The specialty sugars market faces growing pressure from alternative sweeteners, including stevia, monk fruit, and high-fructose corn syrup (HFCS). These substitutes have gained popularity due to rising health awareness and the increasing prevalence of metabolic disorders; the CDC reports that 11.6% of the U.S. population lives with diabetes, driving demand for low-calorie, glycemic-friendly sweeteners. Specialty sugars, often higher in calories and priced at a premium, struggle to compete in beverages, functional foods, and processed snacks where consumers seek healthier or sugar-reduced options. The affordability, wide availability, and aggressive marketing of these substitutes have eroded the market share of traditional specialty sugars. This competitive landscape compels manufacturers to innovate or diversify product portfolios, increasing operational complexity, while also creating barriers to entry for smaller producers, thereby restraining overall market expansion.

Opportunities - Expansion in Pharmaceuticals and Nutraceuticals

The pharmaceuticals and nutraceuticals sector offers a significant growth avenue for specialty sugars, as they improve drug solubility, mask bitterness, and enhance bioavailability, particularly in pediatric and geriatric formulations. Additionally, nutraceutical expansion allows companies to develop customized blends, fortified powders, and functional beverages, creating high-margin revenue pockets. Targeting this end-use segment positions specialty sugar producers to capture both premium pricing and long-term partnerships with pharmaceutical and nutraceutical brands.

Growth in Organic and Sustainable Variants

Organic and sustainably sourced specialty sugars present a lucrative opportunity amid rising clean-label and ethical consumption trends. In the Asia Pacific, organic sugars hold a 42% market share, driven by urbanization, rising health consciousness, and increasing disposable incomes. EU regulations promoting sustainable sourcing and traceability further encourage adoption, allowing companies to command premium pricing of 20-30% over conventional variants. Demerara and other minimally processed sugars are the fastest-growing segments, supported by e-commerce channels and the artisan food market. Consumers increasingly prefer natural, ethically produced sweeteners for bakery, beverages, and functional foods, creating demand for volume expansion. Producers innovating in organic, fair-trade, and ethically sourced specialty sugars can capture emerging market niches, strengthen brand differentiation, and achieve long-term revenue growth in both domestic and international markets.

Category-wise Analysis

Product Type Insights

Caster sugar is the leading specialty sugar, capturing a 38% market share in 2025, primarily due to its ultra-fine granulation and versatility in baking and confectionery applications. Its fine texture allows for rapid dissolution and incorporation of air, making it ideal for delicate recipes like cakes, meringues, and mousses where consistency and lightness are critical. Persistence Market Research reports that demand has grown steadily from artisan and premium bakers who prioritize product quality, texture, and aesthetics. Beyond traditional baking, caster sugar is increasingly used in functional foods, beverages, and high-end desserts, reinforcing its dominance. Global bakery market expansion, particularly in Asia, Europe, and North America, drives sustained demand, as manufacturers and home bakers alike prefer caster sugar over standard granulated sugar for uniform results. Its versatility, combined with premium product positioning, cements its leadership and ensures continued adoption in both industrial and specialty culinary segments.

Application Insights

The Bakery & Confectionery segment dominates specialty sugar consumption, accounting for 46% share in 2025, as these sugars are essential for achieving desired texture, flavor, and appearance in baked goods. According to FAO-aligned data, nearly 30% of specialty sugar usage is concentrated in this segment, reflecting the critical role of caster and icing sugars in aeration, sweetness balance, and structural integrity of pastries, cakes, cookies, and confections. Rising consumer preference for premium and artisanal baked products, particularly in emerging markets like Asia Pacific, drives growth, as manufacturers increasingly incorporate specialty sugars to differentiate products. The segment benefits from urbanization, rising disposable incomes, and an expanding café and patisserie culture, which favor visually appealing and high-quality baked goods. Additionally, specialty sugars contribute to product innovation, enabling unique textures, flavors, and decorative finishes, thereby reinforcing the bakery and confectionery sector as the most significant and stable end-use market for specialty sugars globally.

Regional Insights

North America Specialty Sugars Market Trends and Insights

North America leads the global specialty sugars market, driven by a mature food and beverage industry, high consumer spending, and a strong preference for premium and artisanal products. The U.S. dominates, with bakeries, confectioneries, and specialty beverage manufacturers driving consistent demand for caster, icing, and liquid sugars. Health-conscious trends have also fueled growth in low-glycemic, organic, and natural sugar variants, as consumers seek cleaner labels and reduced processing. E-commerce adoption and gourmet retail chains further enhance accessibility to specialty sugar types, expanding market reach. Technological innovations in refining and sustainable sourcing enable manufacturers to maintain quality and differentiate products, while partnerships with bakery chains and nutraceutical companies create additional revenue streams. Additionally, regulatory approvals like FDA GRAS status support product integration across functional foods, nutraceuticals, and beverages. Combined, these factors make North America a high-value, growth-oriented region, setting benchmarks for innovation, premium pricing, and consumer adoption in the global specialty sugars landscape.

Asia Pacific Specialty Sugars Market Trends and Insights

Asia Pacific is emerging as the fastest-growing region in the specialty sugars market, fueled by rising urbanization, increasing disposable incomes, and shifting consumer preferences toward premium and health-oriented products. Countries such as China, India, Japan, and South Korea are witnessing robust demand for organic, Demerara, and muscovado sugars, driven by the expanding bakery, confectionery, and specialty beverage industries. The growing middle-class population favors artisanal, clean-label, and minimally processed sugar variants, reflecting awareness of wellness, taste, and sustainability. E-commerce platforms and modern retail chains have further boosted accessibility, enabling niche sugar types to reach urban consumers quickly. Government policies supporting organic farming, coupled with supply chain investments, encourage adoption of sustainably sourced specialty sugars. Additionally, regional foodservice growth, including cafes, bakeries, and gourmet outlets, is driving consistent consumption. These factors position Asia Pacific as a high-potential market, offering opportunities for innovation, premium pricing, and long-term volume growth in specialty sugars.

Competitive Landscape

The specialty sugars market is moderately consolidated, with competition driven by product innovation, sustainability, and premium positioning. Key players focus on developing organic, low-glycemic, and clean-label variants to meet rising consumer demand for healthier and ethically sourced sweeteners. Manufacturers invest in advanced refining technologies, artisan processing techniques, and functional blends to differentiate offerings in bakery, confectionery, beverages, and nutraceutical applications. Market rivalry also extends to distribution, with e-commerce and modern retail channels gaining prominence.

Key Developments:

- In November 2025, Signature Brands expanded its dessert portfolio by launching a new line of flavored sugars under the Betty Crocker brand. The product range included six distinct flavors Lemon Twist, Salted Caramel, Pumpkin Spice, Cinnamon Roll, Vanilla Bean, and Peppermint each produced in the United States and packaged in easy-to-use shaker bottles.

- In August 2025, Coffee mate® and Warner Bros. Discovery Global Consumer Products partnered to launch a Harry Potter® x Coffee mate® Honeydukes Café pop-up event in Chicago. celebrating two limited-edition creamers inspired by iconic Honeydukes sweets. Fans were invited to enjoy specialty beverages crafted with the Toffee Cauldron Cake and Zero Sugar White Chocolate Peppermint Toad flavored creamers at the themed café at 444 N Michigan Avenue, which featured whimsical touches designed to evoke the magical world of Harry Potter®.

Companies Covered in Specialty Sugars Market

- Cargill Incorporated

- Tate & Lyle PLC

- Ingredion Incorporated

- Archer Daniels Midland Company

- Südzucker AG

- Tereos S.A.

- Nordzucker AG

- Wilmar International Limited

- Associated British Foods plc

- Louis Dreyfus Company

- Domino Foods Inc.

- Imperial Sugar Company

- ASR Group

- Billington's

- Dhampure Speciality Sugars

Frequently Asked Questions

The global Specialty Sugars market is expected to reach US$ 42.1 billion in 2026.

Rising bakery and confectionery demand, accounting for 30% consumption, drives growth via premium texture needs.

North America leads with 39% share in 2025, supported by U.S. innovation.

Pharmaceuticals and nutraceuticals expansion, with 7% CAGR from functional applications.

Leading players include Cargill, Tate & Lyle, ADM, and Südzucker AG.