- Food Ingredients & Additives

- Fruit Sugar Market

Fruit Sugar Market Size, Share, and Growth Forecast, 2026 - 2033

Fruit Sugar Market by Product Type (Berry Sugar, Citrus Fruits Sugar, Apple Sugar, Mango Sugar, Banana Sugar), Application (Household, Food & Beverage Manufacturers, Bakery & Confectionery Producers, Others), and Regional Analysis for 2026 - 2033

Market Introduction:

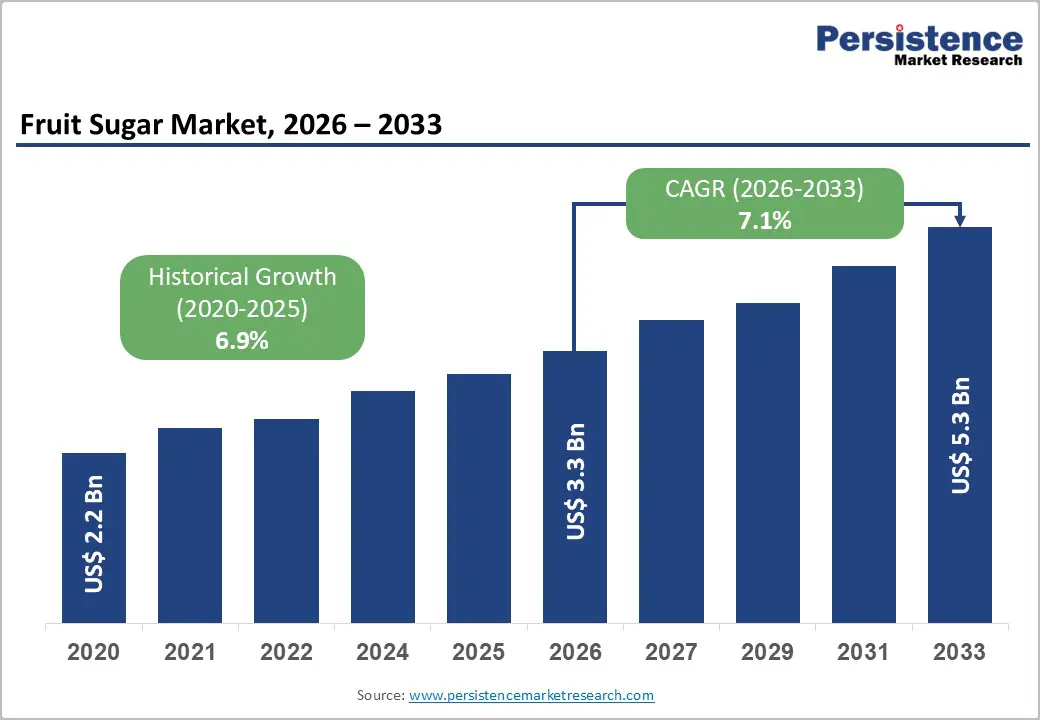

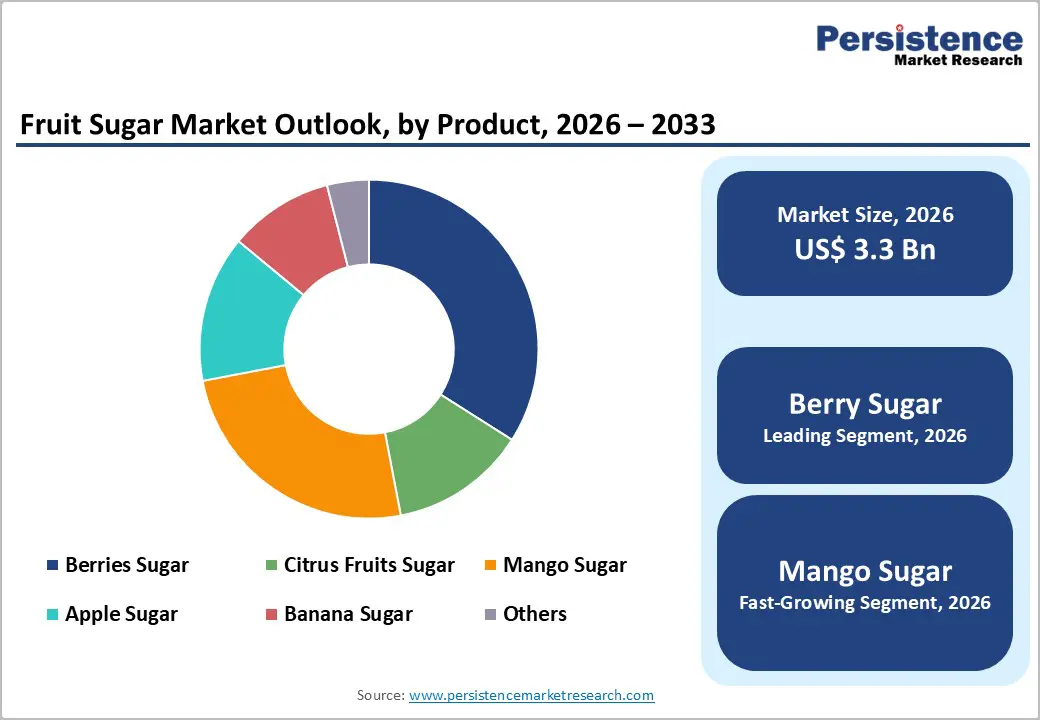

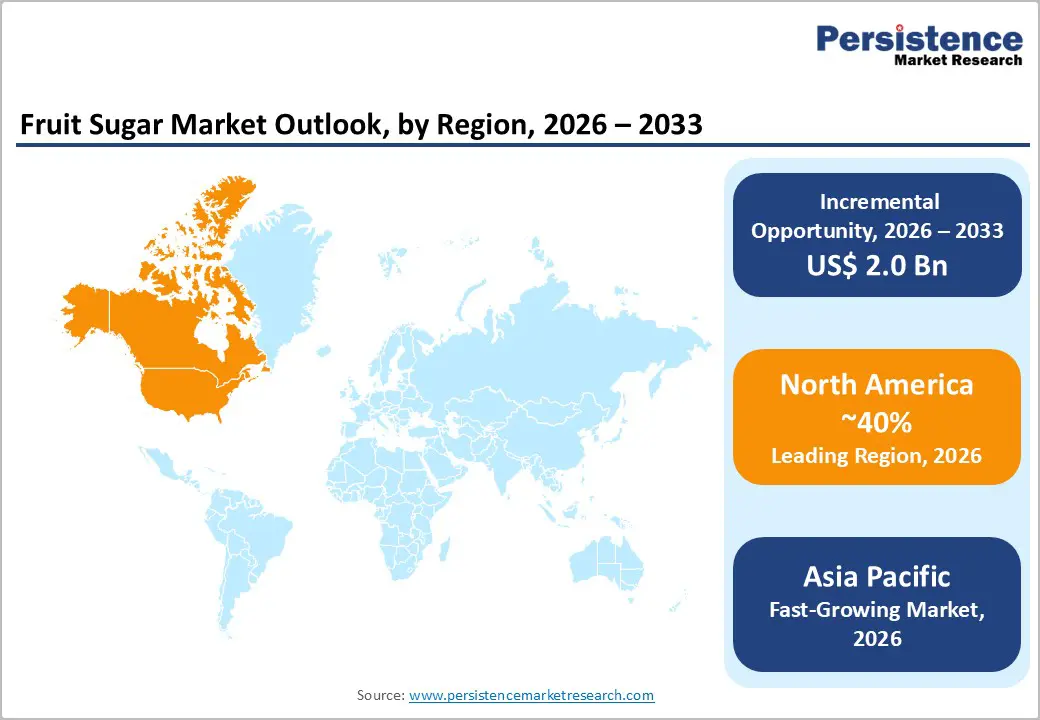

The global fruit sugar market size is likely to be valued at US$3.3 billion in 2026 and is expected to reach US$5.3 billion by 2033, growing at a CAGR of 7.1% during the forecast period from 2026 to 2033, driven by the extraction or concentration of sugars from fruits such as berries, citrus fruits, apples, mangoes, and bananas.

These fruit-based sugars are increasingly utilized as alternatives or complements to refined sugars, offering advantages such as natural origin, clean-label appeal, mild sweetness profiles, and the retention of trace nutrients and flavor compounds inherent to their source fruits. The market is primarily driven by shifting consumer preferences toward healthier and minimally processed food ingredients, supported by growing awareness regarding the adverse effects of excessive refined sugar consumption, including obesity, diabetes, and metabolic disorders. This has encouraged food and beverage manufacturers to reformulate products using fruit-derived sweeteners to align with evolving dietary trends and regulatory expectations for transparency and labeling. Advancements in fruit processing, enzymatic conversion, and concentration technologies have improved the efficiency, scalability, and cost-effectiveness of producing fruit sugars.

Key Industry Highlights:

- Leading Region: North America is expected to be the leading region, accounting for a 40% market share in 2026, driven by strong health consciousness, clean-label demand, and advanced food innovation.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rising urbanization, expanding middle-class demand, and abundant fruit resources.

- Leading Product Type: Sugar from berries is projected to be the leading product type in 2026, accounting for 34% of revenue share, driven by strong consumer preference for antioxidant-rich and premium natural sweeteners.

- Leading Application: The food & beverage segment is anticipated to be the leading application, accounting for over 45% of revenue in 2026, driven by high-volume demand for natural sweeteners in processed foods and beverages.

| Key Insights | Details |

|---|---|

|

Fruit Sugar Market Size (2026E) |

US$3.3 Bn |

|

Market Value Forecast (2033F) |

US$5.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.9% |

DRO Analysis

Driver - Rising Health Consciousness and Demand for Natural Sweeteners

Growing awareness of lifestyle-related conditions such as obesity, diabetes, and metabolic disorders is significantly influencing consumer preferences toward healthier dietary choices. Consumers are actively reducing intake of refined sugars and seeking alternatives perceived as more natural and less processed. Their association with natural nutrition and mild sweetness profiles makes them increasingly desirable across packaged foods, beverages, and home consumption, particularly among urban and health-conscious populations.

Regulatory bodies and public health campaigns promoting sugar reduction are encouraging manufacturers to reformulate products using natural sweetening solutions. Fruit sugars offer a dual advantage by delivering sweetness and subtle flavor enhancements, making them suitable for a wide range of applications. The growing popularity of organic and minimally processed food products strengthens demand.

Growth in Food Processing and Functional Applications

The expansion of the food processing industry is driving demand for fruit sugars, particularly as manufacturers seek versatile ingredients that offer both functionality and natural appeal. Fruit sugars are widely used in beverages, dairy products, bakery items, and confectionery due to their ability to enhance taste, improve texture, and support browning properties. Their compatibility with clean-label formulations makes them an attractive option for companies developing premium and health-oriented products, especially in functional and fortified food segments.

Increasing innovation in functional foods and beverages is driving the incorporation of fruit sugars into value-added formulations. These sugars provide sweetness while enhancing flavor and differentiating products. Advances in processing technologies have improved extraction efficiency and consistency, enabling large-scale production. As demand for ready-to-eat and convenience foods rises, fruit sugars are gaining traction as a reliable ingredient that supports both industrial scalability and evolving consumer expectations.

Restraint - Perception and Taste Profile Limitations

Despite their natural appeal, fruit sugars face limitations in taste perception and consistency, which can affect their broader adoption. Compared to refined sugar, some fruit-derived sugars exhibit varying sweetness intensities or distinct flavor notes that are not always suitable for all product categories. This can pose formulation challenges for manufacturers aiming to maintain uniform taste profiles across large-scale production. Consumers accustomed to the neutral sweetness of traditional sugar may require time to adapt to these subtle differences.

Variability in raw materials, influenced by seasonal and regional factors, can affect the consistency of fruit sugar products. This creates challenges in standardization and quality control, especially for multinational food companies operating across diverse markets. While technological advancements are addressing some of these concerns, perceptions of taste and performance remain a barrier. Overcoming these limitations requires continued innovation in processing techniques and increased consumer education to enhance acceptance and trust in fruit-based sweeteners.

Competition from Established Sweetener Alternatives

The fruit sugar market operates in a highly competitive environment, facing strong competition from well-established natural and artificial sweeteners. Alternatives such as stevia, monk fruit, and other low-calorie sweeteners have gained significant traction due to their high sweetness intensity and lower caloric content. These products are often preferred in diet and zero-sugar formulations, creating challenges for fruit sugars that may not offer the same level of sweetness efficiency or calorie reduction.

Large-scale availability and cost advantages of conventional sweeteners, such as high-fructose corn syrup and refined sugar, continue to dominate industrial use. Many food manufacturers rely on these established options due to their consistent performance and lower production costs. Fruit sugars must compete based on functionality, pricing, and scalability. Strengthening their market position requires differentiation through natural positioning, improved processing, and targeted applications where flavor and clean-label attributes are prioritized.

Opportunity - Technological Convergence with Clean-Label and Reduced-Sugar Trends

Advancements in food processing and ingredient technologies are creating new opportunities for fruit sugars to align with clean-label and reduced-sugar trends. Innovations in enzymatic processing, concentration methods, and blending techniques enable manufacturers to enhance the sweetness profile while maintaining the natural integrity of the product. These developments support the creation of products with lower added sugar content without compromising taste or texture, making fruit sugars increasingly relevant in reformulation strategies.

The integration of fruit sugars with other natural ingredients allows for customized solutions tailored to specific product applications. This technological convergence is particularly valuable in premium and functional food segments, where consumers demand both health benefits and sensory appeal. As food companies invest in research and development, fruit sugars are being positioned as key components in next-generation formulations, offering a balance between natural origin, functionality, and improved nutritional profiles.

Unmet Needs in Specialty Applications and Sustainability

The fruit sugar market presents significant opportunities in specialty applications where traditional sweeteners may fall short. Niche segments such as organic foods, infant nutrition, sports nutrition, and medical diets require ingredients that combine safety, natural origin, and functional benefits. Fruit sugars can address these needs by providing mild sweetness, trace nutrients and flavor enhancements. Their adaptability across diverse formulations positions them well for expansion into high-value, specialized product categories.

Sustainability is another critical area offering growth potential, as consumers and manufacturers increasingly prioritize environmentally responsible sourcing and production practices. Utilizing surplus or imperfect fruits for sugar extraction can reduce food waste and support circular economy initiatives. Improvements in sustainable farming and processing methods can enhance the environmental profile of fruit sugars. As sustainability becomes a key purchasing factor, companies that invest in eco-friendly solutions and transparent supply chains are likely to gain a competitive advantage in this evolving market.

Category-wise Analysis

Product Type Insights

Berry sugar is expected to lead the fruit sugar market, accounting for approximately 34% of revenue in 2026, driven by its strong positioning as a premium and health-oriented natural sweetener. Its association with antioxidant-rich fruits such as strawberries, blueberries, and raspberries enhances its appeal in clean-label and functional food formulations. For example, Berry sugar is widely used in premium fruit-flavored yogurts, where it provides sweetness and enhances natural flavor, aligning with consumer expectations for minimally processed, naturally sourced ingredients.

Mango sugar is likely to represent the fastest-growing segment, supported by abundant raw material availability in regions such as the Asia Pacific and Latin America, along with the increasing popularity of tropical flavors in food trends. Mango sugar offers a rich taste profile and versatility, making it suitable for beverages, desserts, and functional foods. For example, mango sugar is increasingly utilized in ready-to-drink beverages and flavored juices, where it enhances sweetness while delivering a natural fruit identity, supporting both flavor innovation and clean-label positioning in competitive markets.

Application Insights

The food & beverage segment is projected to lead the market, capturing around 45% of revenue in 2026, supported by the widespread use of fruit sugars in processed foods and beverages. This segment benefits from the need for consistent, natural sweetening solutions in products such as soft drinks, sauces, dairy items, and packaged snacks. Manufacturers prefer fruit sugars for their ability to enhance flavor while supporting clean-label claims and sugar reduction strategies. For example, fruit sugars are widely used in flavored yogurt drinks, where they provide balanced sweetness and natural taste, helping brands cater to health-conscious consumers while maintaining product consistency and quality across large production volumes.

Bakery & confectionery producers are likely to be the fastest-growing application, driven by increasing innovation in reduced-sugar and premium baked goods. This segment benefits from the functional properties of fruit sugars, including moisture retention, browning, and texture enhancement, which are essential in bakery applications. For example, fruit sugars are increasingly used in low-sugar fruit-filled pastries and natural confectionery products, where they enhance both taste and visual appeal while supporting claims of natural ingredients and reduced processing.

Regional Insights

North America Fruit Sugar Market Trends

North America is anticipated to be the leading region, accounting for 40% market share in 2026, driven by increasing consumer awareness of health and wellness and rising demand for clean-label and natural ingredients. Manufacturers are focusing on reformulating beverages, dairy, bakery, and confectionery products to reduce refined sugar content while maintaining taste and texture. Fruit sugars, such as those from berries and apples, are increasingly used in premium and functional food products, offering both sweetness and added nutritional appeal.

Companies are actively investing in product development and partnerships to meet these trends. For example, Cargill Incorporated has expanded its portfolio of berry and apple-derived sweeteners for beverage and yogurt manufacturers, aligning with the clean-label and health-focused shift. North America benefits from a mature food innovation ecosystem, technological advancements in extraction and processing, and high per-capita spending on wellness products, making it a leading market. This region continues to prioritize functional, minimally processed sweeteners in line with evolving consumer expectations.

Europe Fruit Sugar Market Trends

Europe is likely to be a significant market for fruit sugar, driven by strong health consciousness, government-led sugar-reduction programs, and demand for organic and minimally processed products. Consumers are increasingly opting for natural sweeteners in beverages, bakery, dairy, and confectionery, reflecting a shift toward wellness-oriented lifestyles. Fruit sugars from berries, apples, and citrus are particularly popular due to their clean-label appeal and versatility in functional and fortified food formulations.

Companies are leveraging these trends by innovating in product applications and supply chain practices. For instance, Ingredion Incorporated has partnered with European food and beverage manufacturers to provide fruit-based sweeteners tailored for bakery and beverage applications, combining functional performance with natural branding. Europe also benefits from mature distribution networks, established consumer trust in natural ingredients, and ongoing innovation in specialty and functional food products.

Asia Pacific Fruit Sugar Market Trends

The Asia Pacific region is likely to be the fastest-growing, driven by urbanization, rising disposable incomes, and abundant domestic fruit supplies, including mangoes, bananas, and citrus. Manufacturers are leveraging local agricultural resources to produce high-quality fruit-derived sweeteners at competitive costs, supporting both domestic consumption and exports. Demand is rising across beverages, dairy products, bakery, and confectionery, particularly for tropical and functional flavor profiles.

Regional manufacturers are also improving consistency and scalability through investments in processing and blending technologies that enhance product performance in industrial applications. For example, PureCircle Limited, an established producer of plant-based natural sweeteners including stevia sourced and processed in Asia, collaborates with food and beverage companies to integrate cleaner natural sweetening solutions into a range of products, reflecting broader shifts toward plant-derived ingredient use in the region.

Competitive Landscape

The global fruit sugar market exhibits a moderately fragmented structure, driven by a mix of large multinational ingredient suppliers and numerous regional players competing to meet the growing demand for natural and clean-label sweeteners. Companies are investing in research and development to enhance extraction technologies, improve flavor profiles, and expand applications across beverages, bakery, dairy, and confectionery sectors, as manufacturers and consumers alike prioritize healthier alternatives to refined sugar.

With key leaders including Cargill, Incorporated, Tate & Lyle PLC, Ingredion Incorporated, and Archer Daniels Midland Company, the competitive landscape features established companies with extensive distribution networks and strong development pipelines. These players compete through continuous product innovation and strategic collaborations with food and beverage manufacturers.

Key Industry Developments:

- In March 2026, Cargill highlighted strategic reformulation guidance for European jam manufacturers ahead of the revised EU Breakfast Directive, which raises minimum fruit content requirements and reduces added sugars in fruit-based products such as jams and fruit juices.

- In August 2025, MONIN launched its new PURE range in India, featuring a line of no-added sugar fruit and plant-based flavor concentrates designed for beverages and culinary uses. The range includes natural fruit flavors such as Mint, Red Fruits, Green Apple, and Peach Apricot, and is positioned to meet rising consumer demand in India for low and no-sugar drink options without artificial sweeteners or added sugars.

- In February 2025, Israeli food-tech company BlueTree Technologies and juice producer Priniv launched the world’s first commercially available reduced-sugar orange juice with no additives in supermarkets across Israel. The product uses BlueTree’s patented sugar-reduction technology to selectively remove naturally occurring sugars such as sucrose while preserving flavor and nutrients, resulting in a healthier juice option with significantly less sugar but without artificial sweeteners or additives.

Companies Covered in Fruit Sugar Market

- Cargill Incorporated

- Mitsui & Co. Ltd.

- Archer Daniels Midland Company

- Louis Dreyfus Company B.V.

- DuPont de Nemours Inc.

- Associated British Foods plc

- Ajinomoto Co. Inc.

- Wilmar International Limited

- Ingredion Incorporated

- Cosan S.A.

- Kerry Group plc

- Tereos Group

- COFCO Corporation

- Mitr Phol Group

Frequently Asked Questions

The global fruit sugar market is projected to reach US$3.3 billion in 2026.

The fruit sugar market is driven by rising consumer demand for natural, clean-label sweeteners and healthier alternatives to refined sugar.

The fruit sugar market is expected to grow at a CAGR of 7.1% from 2026 to 2033.

Key market opportunities lie in expanding applications in beverages, bakery, dairy, and functional foods, alongside growing demand for clean-label and reduced-sugar products.

Cargill Incorporated, Mitsui & Co. Ltd., Archer Daniels Midland Company, Louis Dreyfus Company B.V, and DuPont de Nemours Inc are the leading players.