- Food Ingredients & Additives

- Beet Sugar Market

Beet Sugar Market Size, Share, and Growth Forecast, 2026 – 2033

Beet Sugar Market by Product Type (White Beet Sugar, Brown Beet Sugar, Liquid Beet Sugar), Application (Beverages, Confectionery, Bakery Goods, Dairy Products) and Regional Analysis for 2026 – 2033

Beet Sugar Market Size and Trends Analysis

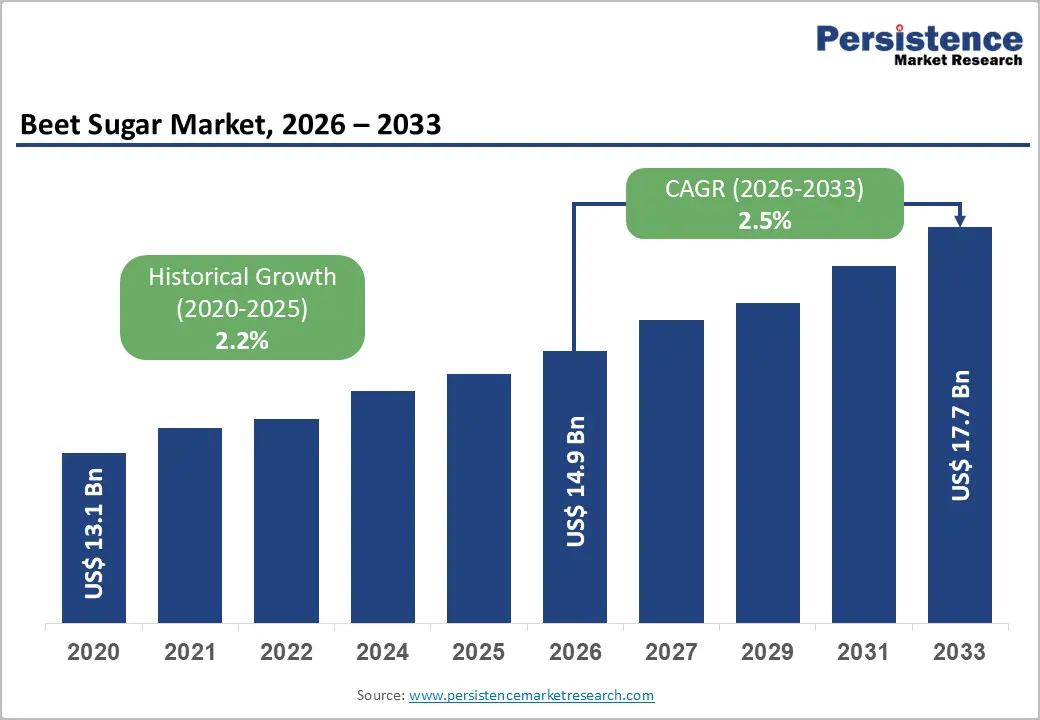

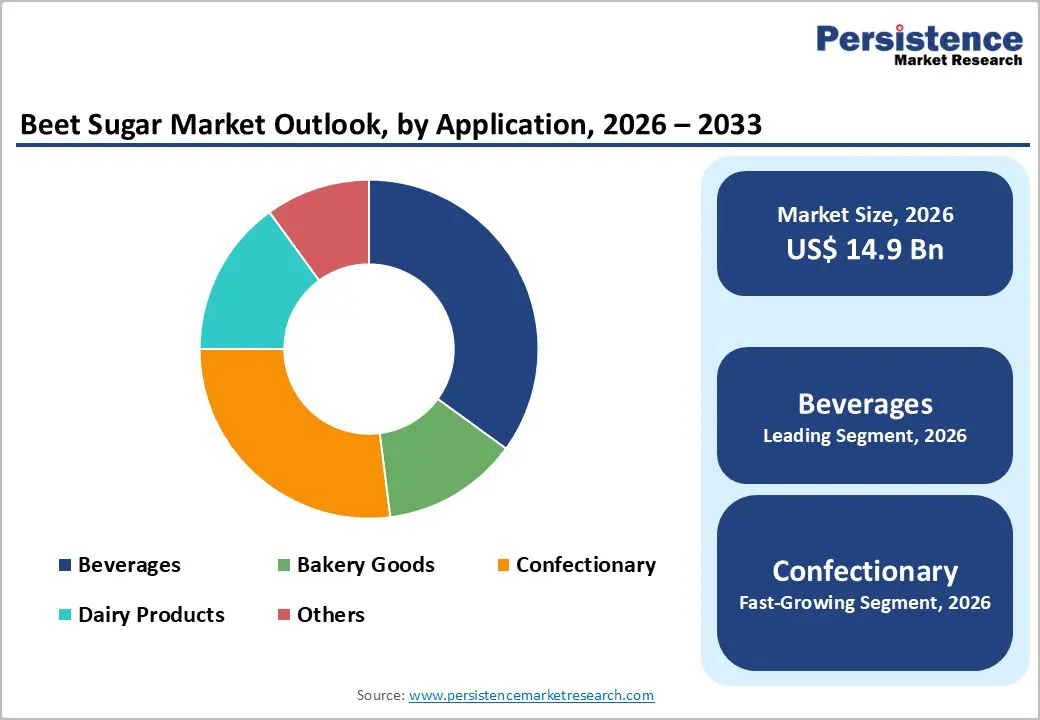

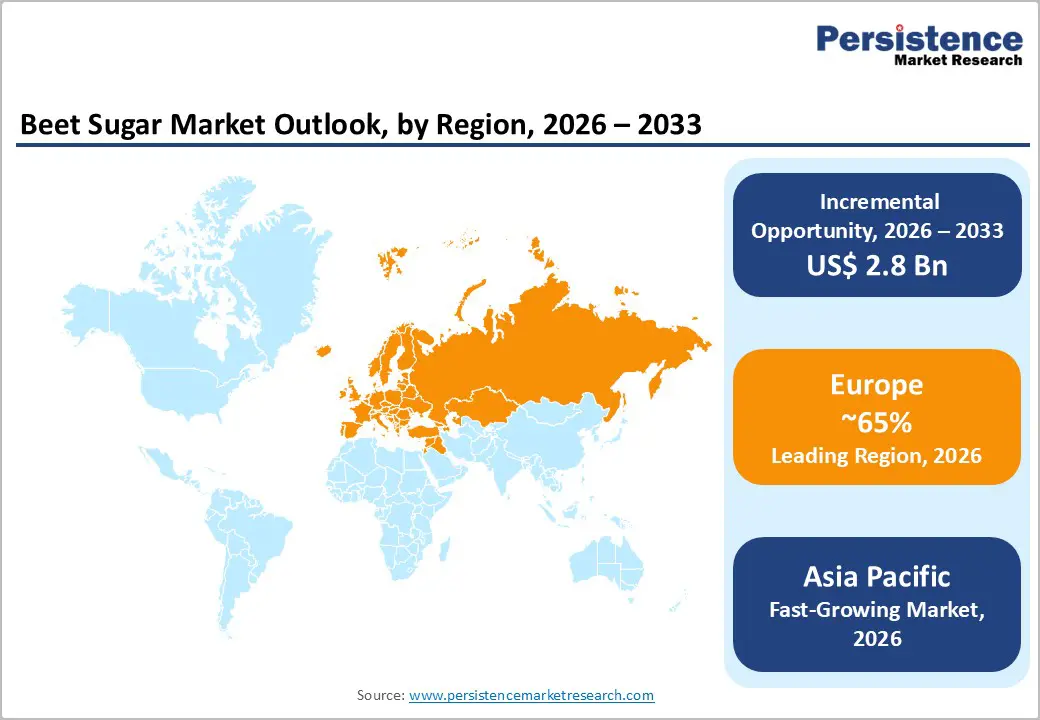

The global beet sugar market size is likely to be valued at US$14.9 billion in 2026 and is expected to reach US$17.7 billion by 2033, growing at a CAGR of 2.5% during the forecast period from 2026 to 2033, driven by steady demand from food and beverage processing industries, including beverages, confectionery, bakery, and dairy products, supported by rising preference for non GMO, traceable, and regionally sourced sweeteners, particularly in Europe and North America.

However, expansion remains moderated by intense competition from cane sugar, fluctuating agricultural yields, and health-driven shifts toward reduced sugar consumption. Despite these challenges, emerging opportunities lie in clean-label formulations, organic beet sugar, and sustainable production practices, as manufacturers focus on efficiency improvements and by-product utilization.

Key Industry Highlights:

- Leading Region: Europe is anticipated to be the leading region, accounting for a market share of 65% in 2026, driven by strong production in Germany, France, the U.K., and Spain, robust food manufacturing, and established players such as Südzucker and Tereos.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the beet sugar industry in 2026, supported by the rapid expansion of processed food industries, government policy support, and increasing local production in China, India, Japan, and ASEAN countries.

- Leading Product Type: White beet sugar is projected to represent the leading product type in 2026, accounting for 70% of the revenue share, driven by its high purity, neutral taste, and wide application across food processing industries.

- Leading Application: Beverages are anticipated to be the leading application type, accounting for over 40% of the revenue share in 2026, supported by consistent demand in soft drinks, functional beverages, and the role of sugar in taste and preservation.

| Report Attribute | Details |

|---|---|

|

Beet Sugar Market Size (2026E) |

US$14.9 Bn |

|

Market Value Forecast (2033F) |

US$17.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

2.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Natural and Non-GMO Sweeteners

Health-conscious buyers are shifting away from artificial sweeteners and high-fructose corn syrup, favoring products with clear, sustainable sourcing. Beet sugar, particularly white and liquid forms, provides a natural alternative with consistent quality, neutral taste, and high purity.

Food and beverage manufacturers are responding by incorporating beet sugar in processed foods, beverages, confectionery, and dairy products to meet clean-label requirements. This trend is strongest in Europe and North America, where regulatory standards and consumer awareness around non-GMO labeling are highly enforced.

Non-GMO and natural sweeteners create opportunities for product differentiation and premium pricing in competitive markets. Organic and sustainably produced beet sugar variants are increasingly preferred by niche consumers and specialty food brands. Companies such as Südzucker, Tereos, and Nordzucker are investing in traceable production and certification programs to ensure transparency from farm to processing.

This strengthens brand trust and aligns with the rising trend of environmentally conscious consumption. The market’s expansion is closely tied to clean-label adoption, sustainable practices, and the continuous demand for naturally sourced sweeteners.

Expansion in the Food and Beverage Processing Sectors

Growing urbanization, rising disposable incomes, and changing consumer lifestyles are driving increased consumption of processed foods, soft drinks, bakery items, and dairy products. Beet sugar is widely used in these industries due to its neutral taste, high solubility, and consistent quality, making it ideal for mass production and formulation stability.

Regions such as Europe and Asia Pacific are witnessing accelerated growth in industrial-scale food manufacturing, which directly increases the demand for beet sugar as a key ingredient across multiple product categories.

The beverage and confectionery segments are major contributors to this demand surge. Soft drinks, functional beverages, candies, and chocolates require precise sugar content for taste, texture, and preservation. Food manufacturers are increasingly adopting liquid beet sugar for its ease of integration in large-scale operations, reducing processing time and enhancing efficiency. The sector’s expansion is complemented by automation, modern processing equipment, and supply chain improvements, which increase the beet sugar utilization.

Barrier Analysis - Health Concerns and Sugar Reduction Initiatives

Rising awareness of obesity, diabetes, and other lifestyle-related diseases has led governments and health organizations to promote reduced sugar consumption through policies such as sugar taxes and labeling regulations. This is driving demand for low-calorie sweeteners, such as stevia and monk fruit, especially in developed regions such as North America and Europe.

Food manufacturers are reformulating products to comply with health guidelines, creating challenges for traditional beet sugar producers. While industrial demand remains steady, the health-conscious shift is limiting growth in beet sugar consumption.

Competition from Cane Sugar and Substitutes

Cane sugar benefits from lower production costs, higher yields, and established supply chains in tropical regions, making it a cost-effective option for manufacturers. Beet sugar faces competition from alternative sweeteners, including high-fructose corn syrup, stevia, and other low-calorie options, driven by health concerns and sugar reduction trends.

This competition limits beet sugar's pricing power and market growth, especially in price-sensitive regions such as Asia Pacific and Latin America. To stay competitive, beet sugar producers must invest in technological improvements, processing efficiency, and value-added products. Despite its purity and non-GMO advantages, beet sugar's growth is constrained by market preference for cost-effective, locally available sweeteners, requiring innovation and strategic marketing to maintain market share.

Opportunity Analysis - Growing Clean-Label and Organic Product Demand

Consumers are seeking products made with natural, minimally processed ingredients that are free from additives, artificial sweeteners, and genetically modified organisms (GMOs). Beet sugar, particularly organic and white variants, aligns well with these preferences due to its traceable sourcing, high purity, and neutral taste, making it a preferred ingredient in beverages, bakery items, confectionery, and dairy products.

This trend is strongest in Europe and North America, where consumers are highly conscious of ingredient transparency, quality, and sustainability, driving consistent demand for clean-label beet sugar products.

The growth of organic and premium food segments presents a significant market opportunity. Manufacturers are increasingly leveraging beet sugar in organic-certified products and functional foods to meet regulatory standards and consumer expectations.

Companies such as Südzucker, Tereos, and Nordzucker are investing in organic production, certification, and sustainable practices to capture this niche but expanding market. The focus on clean-label formulations not only differentiates products but also enhances brand credibility and loyalty. The clean-label and organic trend continues to expand beet sugar producers are well-positioned to capitalize on these high-value opportunities.

Technological Convergence in Processing

Modern processing technologies enable higher extraction rates, consistent sucrose purity, and reduced energy consumption, making beet sugar more competitive against cane sugar and alternative sweeteners. Innovations in liquid beet sugar production and automated crystallization processes streamline operations for beverages, confectionery, and bakery products.

These advancements allow manufacturers to meet growing industrial demand while reducing production costs and waste, positioning beet sugar as a more sustainable and efficient ingredient in the food and beverage sector.

The adoption of data-driven production and quality monitoring systems enhances operational control, ensuring uniform product characteristics across batches. Integration of smart sensors, real-time analytics, and automated feeding systems reduces labor dependency and processing errors, while optimizing energy and water usage.

These advancements allow beet sugar producers to increase extraction efficiency and minimize raw material losses, lowering overall production costs. Automation in packaging and handling ensures consistent product delivery for beverages, bakery, and confectionery industries.

Category-wise Analysis

Product Type Insights

White beet sugar is expected to lead the beet sugar market, accounting for approximately 70% of revenue in 2026, driven by its high purity, neutral taste, and versatility across various industrial applications. Its dominance is evident in beverage manufacturing, where white beet sugar is extensively used to maintain consistent sweetness and taste stability.

The high solubility and quality standards of white beet sugar make it ideal for confectionery, bakery, and dairy products, ensuring uniform performance in large-scale operations. For example, Südzucker AG utilizes white beet sugar extensively in soft drinks and processed food production, demonstrating its wide acceptance in industrial applications. Its non-GMO and traceable sourcing appeals to clean-label and organic product lines, supporting adoption.

Liquid beet sugar is expected to be the fastest-growing segment in 2026, supported by its convenience and ease of use in industrial applications. Its fully dissolved form allows food and beverage manufacturers to reduce processing steps, improve mixing efficiency, and save production time, particularly in dairy products such as flavored milk and yogurts.

For example, Tereos Group has invested in liquid beet sugar production to meet growing demand from beverage and dairy manufacturers seeking ready-to-use sugar solutions. The product’s compatibility with automated filling and blending systems enhances operational efficiency, reducing labor costs and minimizing processing errors. Liquid beet sugar provides consistent sweetness and precise dosing, which is critical for high-volume manufacturing.

Application Insights

Beverages areprojected to lead the market, capturing around 40% of the revenue share in 2026, supported by high demand in soft drinks, functional beverages, and flavored water. Sugar’s role in taste, preservation, and mouthfeel makes it indispensable for beverage manufacturers, particularly in large-scale production where consistent quality is critical.

For example, Coca-Cola and other beverage companies rely on beet sugar as a primary sweetener in certain regional markets, ensuring product consistency and adherence to regulatory and labeling standards. The segment benefits from the growing consumption of ready-to-drink beverages, energy drinks, and functional beverages across Europe and North America.

Confectionery is likely to be the fastest-growing application in 2026, driven by increasing consumption of candies, chocolates, and snack-based sweets worldwide. Sugar plays a key role in providing texture, flavor stability, and structure in confectionery products, making beet sugar a preferred ingredient for consistent quality outcomes.

For example, Mars Inc. relies on beet sugar in chocolate and candy production to maintain uniform sweetness, color, and consistency across batches. Growth in this segment is fueled by rising snack culture, urbanization, and higher disposable income in emerging markets such as Asia Pacific. Liquid and white beet sugar variants allow manufacturers to integrate automation and improve production efficiency, reducing labor requirements and production time.

Regional Insights

North America Beet Sugar Market Trends

North America is likely to be a significant market for beet sugar in 2026, driven by strong food and beverage processing demand and increasing consumer preference for natural, non-GMO, and sustainable sweeteners.

The U.S. and Canada have well-established beet sugar industries with mechanized farming practices and advanced processing technologies that boost yield and production efficiency. North America accounts for a significant portion of beet sugar production and continues to expand its role in clean-label products, bakery goods, and beverage formulations, aligning with broader health and sustainability trends in the region’s packaged food market.

Precision agriculture and biotechnology advancements have also improved disease resistance and reduced chemical inputs in sugar beet farming, making production more resilient and economically viable for producers across the region.

For example, Michigan Sugar Company is expanding its cooperative networks and production facilities to increase capacity and respond to growing demand from bakery and beverage applications. The trend toward clean-label and plant-based products reinforces beet sugar positioning as a preferred ingredient, supporting sustained market growth and innovation.

Europe Beet Sugar Market Trends

Europe is likely to be a significant market for beet sugar in 2026, due to its strong production base and established food processing industries. The region’s temperate climate and advanced agricultural practices enable high-quality beet cultivation, while consumer demand for locally sourced, non-GMO sweeteners strengthens beet sugar’s position in beverages, bakery goods, and confectionery applications.

Environmental policies and sustainability initiatives, such as low-carbon farming standards under the EU Green Deal, promote eco-friendly beet sugar production. Innovation in premium and organic beet sugar lines continues, meeting rising clean-label demand, particularly in Germany and northern European countries.

European refiners are investing in advanced processing technologies and quality optimization to ensure a consistent supply and differentiate their products in industrial applications. For instance, Nordzucker AG, one of Europe’s largest sugar producers based in Germany, offers a wide variety of beet sugar products, including refined sugars, liquid sugars, and specialty varieties for the food and beverage industries.

Through partnerships with major food manufacturers and its expansion into value-added sweeteners, Nordzucker is adapting to market trends of diversification and innovation, aiming to navigate competitive pressures from alternative sweeteners and regulatory changes.

Asia Pacific Beet Sugar Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the beet sugar market in 2026, driven by rising processed food demand and investments in modern sugar beet production. Cultivation areas increase, and industrial demand strengthens across the bakery, confectionery, and processed beverage sectors.

Rising health awareness and clean label trends are encouraging manufacturers to consider beet sugar as an alternative to conventional cane sugar, especially in urban markets with growing processed food consumption. Production and consumption remain relatively flat overall, reflecting the need for investments in processing infrastructure and supply chain development to fully realize growth potential.

This growth is supported by regional investments in processing facilities and strategic partnerships to meet rising industrial and consumer demand. For example, is COFCO Tunhe, part of COFCO International, which is actively investing in localized beet sugar processing facilities and strategic partnerships across China to support regional demand and reduce reliance on imported substitutes.

This reflects a broader trend of companies in the Asia Pacific leveraging domestic production capacity to supply industrial users, including beverage and dairy manufacturers, with high-quality beet sugar. Such efforts are bolstered by government policies promoting agricultural diversification and technology adoption in temperate growing zones, enhancing competitiveness against cane sugar alternatives.

Competitive Landscape

The global beet sugar market exhibits a moderately fragmented structure, driven by the presence of large multinational sugar producers, regional cooperatives, and agricultural processing firms competing across cultivation, refining, and distribution networks. Market leadership is shaped by factors such as production capacity, geographic reach, product quality, sustainability credentials, and integration with food and beverage supply chains.

With key leaders including Südzucker AG, Nordzucker AG, British Sugar, Tereos Group, Cosun Beet Company, and American Crystal Sugar Company, the competitive landscape reflects a mix of European heavyweights and North American cooperatives with strong market influence and diversified portfolios. These players compete through product differentiation, technological investments, sustainability commitments, and value-added solutions such as organic and liquid beet sugar variants to meet clean-label and industrial use demands.

Key Industry Developments:

- In September 2025, Cosun Beet Company launched its sugar beet campaign across multiple locations, expecting higher yields despite reduced acreage. Thanks to early sowing, the projected sugar yield is 15 tonnes per hectare, above the five-year average. Dutch factories plan to process 7.55 million tonnes of beet, with a 16.85% sugar content and a 90.5% processing yield.

- In August 2025, NFU Sugar and British Sugar agreed on a flexible 2026/27 sugar beet contract, offering growers options such as a fixed price of US$40.2/t for up to 65% of the crop, a market-linked bonus, and an index-linked contract. Additional provisions include yield protection, transport allowances, and interest-free cash advances.

Companies Covered in Beet Sugar Market

- Südzucker AG

- Nordzucker AG

- British Sugar (Associated British Foods plc)

- Tereos Group

- Cosun Beet Company

- American Crystal Sugar Company

- Michigan Sugar Company

- Amalgamated Sugar Company

- Western Sugar Cooperative

- Southern Minnesota Beet Sugar Cooperative

- COFCO International

- Mitr Phol Group

- Dalmia Bharat Sugar and Industries Limited

- E.I.D. - Parry

- Rusagro Group

- Thai Roong Ruang Sugar Group

Frequently Asked Questions

The global beet sugar market is projected to reach US$14.9 billion in 2026.

Steady demand from food and beverage processing industries, growing preference for natural and non-GMO sweeteners, and advancements in sustainable sugar beet cultivation and processing.

The beet sugar market is expected to grow at a CAGR of 2.5% from 2026 to 2033.

Key market opportunities in the beet sugar market include rising demand for clean-label and organic products, technological advancements in processing, and expanding food and beverage manufacturing in emerging regions.

Südzucker AG, Nordzucker AG, British Sugar (Associated British Foods plc), Tereos Group, Cosun Beet Company, and American Crystal Sugar Company are the leading players.