- Home Care & Utilities

- Smart Animal Trap Market

Smart Animal Trap Market Size, Share, Trends, Growth, Forecasts for 2026 - 2033

Smart Animal Trap Market by Component (Hardware, Software, Services), Product (Live Traps, Kill Traps, Electric Traps), Animal Type (Rodents, Birds, Small Mammals, Others), Application and Regional Analysis 2026 - 2033

Smart Animal Trap Market Share and Trends Analysis

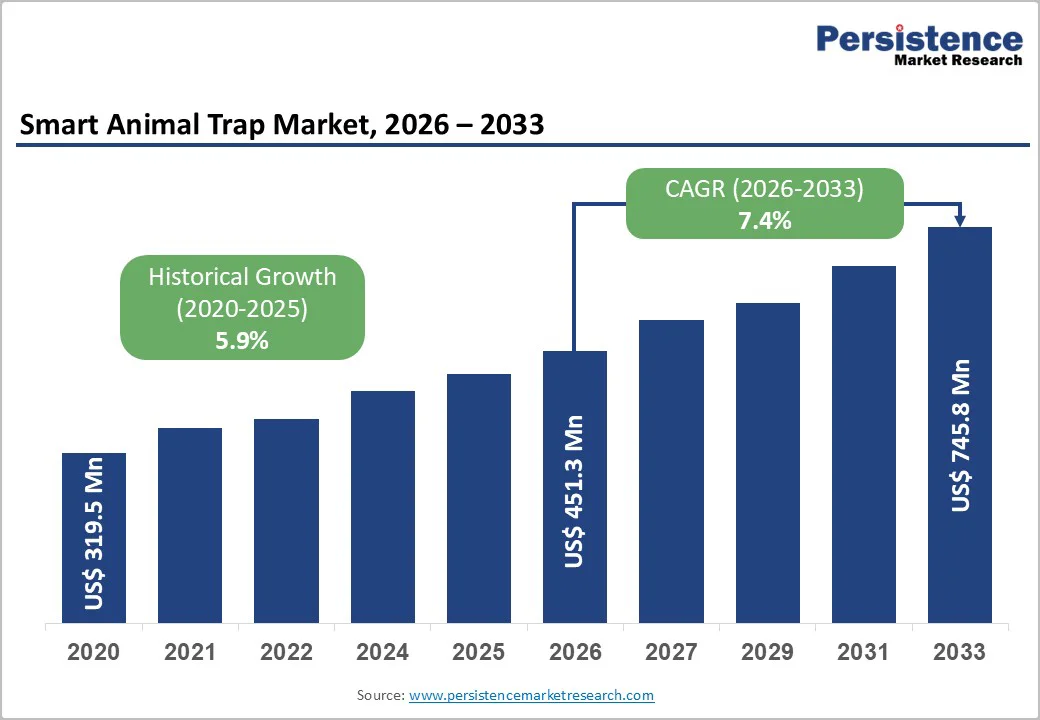

The global smart animal trap market size was valued at US$ 451.3 million in 2026 and is projected to reach US$ 754.8 million by 2033, growing at a CAGR of 7.4% between 2026 and 2033. The market expansion is fundamentally driven by the rise in wildlife-crop damage incidents, urbanization intensifying rodent infestations in metropolitan areas, and the integration of IoT-enabled monitoring systems transforming traditional trapping methods into data-driven wildlife management solutions.

Increasing regulatory emphasis on humane animal capture standards across Europe and North America, coupled with the growing adoption of smart pest control technologies by commercial establishments for food safety compliance, is accelerating market penetration. The convergence of artificial intelligence, sensor fusion technology, and cellular connectivity is enabling real-time monitoring capabilities that significantly reduce labor costs while improving capture efficiency across residential, agricultural, and conservation applications.

Key Industry Highlights:

- Hardware components lead by 49% revenue share, while software demonstrates the fastest growth driven by AI analytics and mobile monitoring platform adoption

- Live Traps dominate product categories by 35% market share, reflecting humane capture preferences; Monitoring/Smart Modules exhibit fastest growth as retrofit solutions gain traction

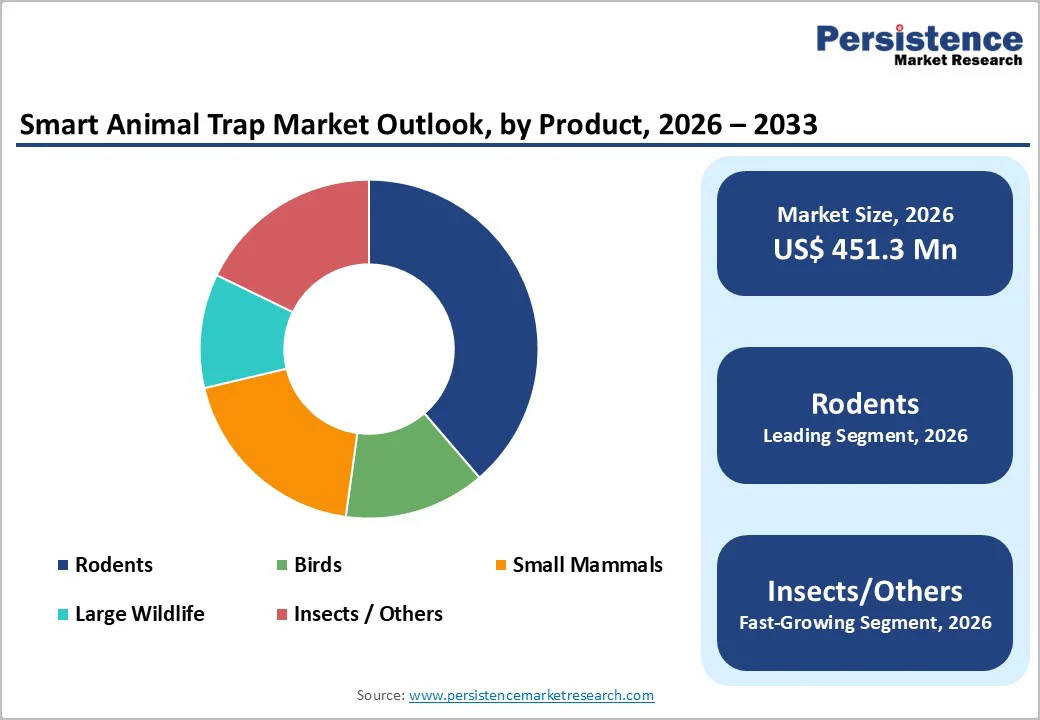

- Rodents constitute the largest animal type segment addressing urban infestation challenges; Insects/Others represent the fastest-growing with a CAGR of 9.3% in a specialized application.

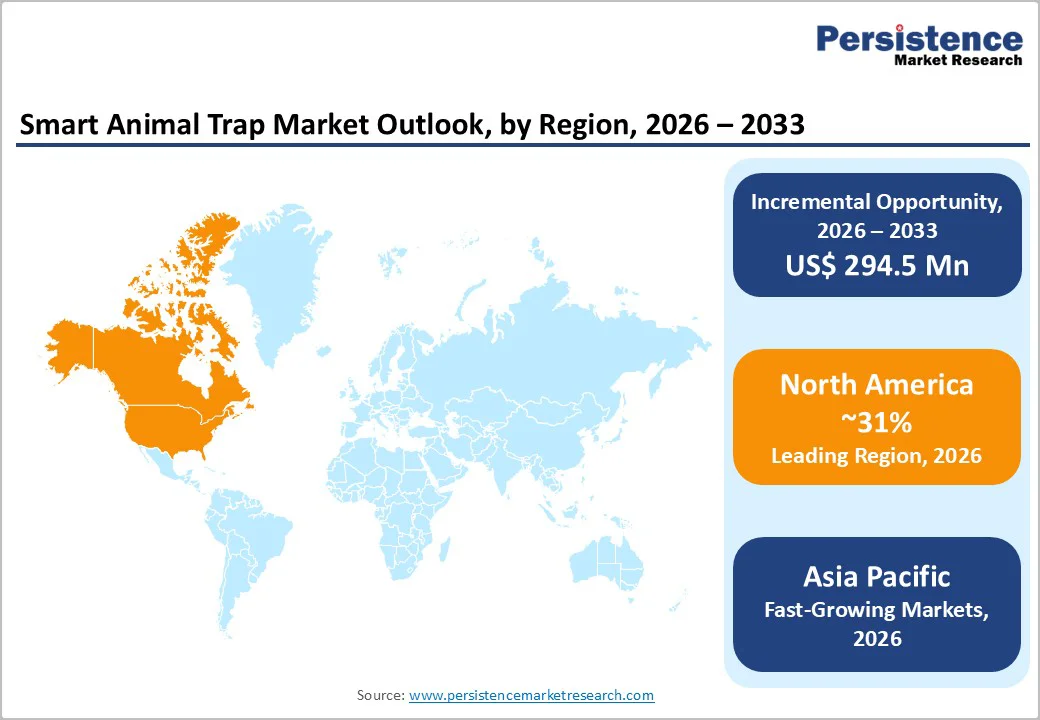

- North America leads with 31% revenue share; Asia Pacific emerges as fastest-growing region at 8.8% CAGR driven by urbanization and agricultural modernization

- Strategic developments include Goodnature's smart mouse trap U.S. launch (September 2024), Bell Laboratories' Mouse iQ introduction (March 2025), and Rentokil's AI-monitoring expansion in Asia (October 2024)

| Key Insights | Details |

|---|---|

|

Smart Animal Trap Market Size (2026E) |

US$ 451.3 million |

|

Market Value Forecast (2033F) |

US$ 745.8 million |

|

Projected Growth CAGR (2026-2033) |

7.4% |

|

Historical Market Growth (2020-2025) |

5.9% |

Market Dynamics Analysis

Drivers - Escalating Urban Rodent Infestations Driven by Climate Change and Urbanization

Urban rodent populations are experiencing significant increases globally, directly correlating with demand for smart pest monitoring solutions. Research published in Science Advances reveals that 69% of analyzed cities (11 of 16) demonstrated significant increasing trends in rat populations, with Washington D.C., San Francisco, Toronto, and New York City exhibiting the strongest positive trends. Climate warming accounts for around 40.7% of variation in rat population trend strength, with cities experiencing greater temperature increases showing larger growth in rat sightings. Global expenditure on urban rat control efforts remains substantial, and the urban pest management market reflects growing municipal and commercial investment in technology-driven pest control infrastructure. Major metropolitan areas including Los Angeles, Chicago, and New York consistently rank among the most rodent-affected cities, driving adoption of IoT-enabled smart traps that offer real-time monitoring, remote alerts, and predictive analytics capabilities for commercial and residential applications.

Integration of IoT and AI Technologies Enhancing Trap Efficacy and Operational Efficiency

The technological transformation of traditional trapping methods through Internet of Things integration represents a fundamental market catalyst. IoT-enabled pest control systems currently represent approximately 30% of pest management provider operations, enabling automated tracking, real-time data analytics, and remote management capabilities. Smart traps utilize sensors, cameras, and wireless connectivity to provide instantaneous alerts upon animal capture, eliminating repetitive manual inspection requirements. Low Power Wide Area Network (LoRaWAN) connectivity is revolutionizing scalable trap deployment, with the smart rodent trap LoRaWAN segment projected to grow at 10.7% CAGR through 2033. These systems enable operators to manage multiple trap sites from centralized interfaces, receive tamper alerts, ensure regulatory compliance, and generate predictive insights through cloud-based analytics. The convergence of edge computing, AI-powered species recognition, and solar-powered autonomous operation is significantly reducing environmental footprint while maximizing capture precision.

Restraints - High Initial Investment Costs and Infrastructure Requirements

The implementation of comprehensive smart trapping systems involves substantial capital expenditure that constrains adoption among price-sensitive consumer segments and smaller agricultural operations. Smart animal traps incorporating advanced sensors, cellular connectivity modules, rechargeable battery systems, and cloud monitoring platforms command significantly higher price points compared to conventional mechanical alternatives, with premium connected traps retailing between US$100-300 per unit.

The need for reliable cellular or LoRaWAN network coverage limits deployment in remote agricultural and conservation areas lacking adequate telecommunications infrastructure. Additionally, subscription fees for cloud monitoring platforms, data analytics services, and ongoing connectivity charges create recurring operational costs that elevate total cost of ownership. While larger commercial enterprises and institutional conservation programs can justify these investments through labor savings and efficiency gains, residential consumers and small-scale farmers frequently opt for more affordable traditional solutions despite reduced functionality.

Regulatory Complexity and Humane Trapping Standards Compliance

Divergent regulatory frameworks across jurisdictions create market access barriers and increase compliance complexity for manufacturers and operators. The Agreement on International Humane Trapping Standards (AIHTS), binding on European Union member states, Canada, and Russia, mandates specific certification requirements for traps targeting fur-bearing species, requiring devices to meet stringent humaneness testing standards.

EU Regulation 3254/91 prohibits leghold traps and restricts imports of products from countries not meeting international humane trapping standards. In the United Kingdom, implementation involves changes to Wildlife and Countryside Act schedules, with certain trap types prohibited for specific species. The U.S. Environmental Protection Agency regulates pesticidal devices, though vertebrate animal traps are generally exempt from premarket registration requirements. This regulatory fragmentation necessitates region-specific product development, certification processes, and market entry strategies, increasing compliance costs and extending time-to-market for innovative trapping technologies.

Opportunities - Expansion in Conservation and Wildlife Management Applications

Growing investment in biodiversity conservation and wildlife research presents substantial expansion opportunities for smart trapping technology providers. Camera traps and remote monitoring systems have become essential tools for ecological researchers studying elusive and endangered species, generating spatiotemporal population data with minimal disturbance. The integration of satellite connectivity enables real-time footage transmission in protected areas, with networked camera traps boosting poacher interceptions by 70% and tracking collars reducing poaching incidents by around 50-90%. Conservation organizations including the Nature Conservancy and United Nations Development Program actively deploy smart trapping solutions for invasive species management and ecosystem restoration. Climate change is intensifying human-wildlife conflicts globally, with ~25% of Climate Crowd interviews across 40+ countries reporting increased conflict incidents alongside other climate impacts. As governments and conservation agencies allocate greater resources toward ecological balance restoration and biodiversity protection, demand for non-lethal smart capture systems with species identification capabilities continues expanding.

Commercial and Industrial Sector Adoption for Regulatory Compliance

Stringent food safety regulations and hygiene compliance requirements create compelling demand drivers within commercial and industrial sectors. The Food Safety Modernization Act (FSMA) prescribes preventive pest control approaches for food producers and manufacturers, requiring integrated pest management programs with documentation of inspection, monitoring, and corrective actions. Pest presence in food shipments triggers load rejections and costly product recalls while damaging brand reputation. The commercial pest control segment commands substantial market share, with the U.S. structural pest control industry showing strong performance and achieving 7.9% year-over-year growth. Commercial clients including food processing facilities, hospitality establishments, and healthcare providers prioritize smart monitoring systems that provide continuous surveillance, automated alerts, and compliance documentation capabilities. Approximately 39.8% of global pest control market revenue derives from commercial applications. As regulatory scrutiny intensifies and digital transformation accelerates across industries, commercial adoption of connected pest management infrastructure offers sustained growth potential.

Category-wise Analysis

Component Insights

The hardware segment commands market leadership, encompassing cameras, sensors, actuators, and power units that constitute the physical infrastructure of smart trapping systems. Hardware components represented the largest revenue share, with around 49% market share. Sensors detecting motion, environmental conditions, and species presence form the technological foundation enabling intelligent trap functionality, while wireless communication modules facilitate real-time data transmission to cloud platforms.

The software segment demonstrates the fastest growth trajectory as data analytics, mobile applications, and cloud monitoring platforms become increasingly sophisticated. Software growth is estimated at 9.2% CAGR through 2033. The development of AI-powered object recognition for species identification, predictive analytics for infestation forecasting, and integrated building management system connectivity drives software value creation. Mobile applications enabling remote trap management from smartphones represent a critical software advancement, with platforms like Victor's Smart-Kill app allowing monitoring from any location.

Product Type Insights

Live traps maintain market dominance as the leading product segment with around 35% market share, reflecting growing emphasis on humane and non-lethal animal capture methods across conservation, residential, and commercial applications. Live cage traps with remote alert capabilities address ethical wildlife management requirements while meeting regulatory standards for humane treatment. The segment benefits from increasing awareness around animal welfare and expanding municipal adoption of humane pest control policies.

Monitoring/Smart Modules represent the fastest-growing product segment with a CAGR of 10.7%, as retrofit solutions enabling digital connectivity for existing trap infrastructure gain market traction. TRAPMASTER and similar systems offer cost-effective upgrades for conventional traps, providing SMS, email, and app-based notifications upon capture without requiring complete trap replacement. The monitoring modules segment benefits from lower entry costs and compatibility with diverse trap types, including cage traps, box traps, and tube traps.

Animal Type Insights

Rodents constitute the largest consumer segment with 39% market share, driven by pervasive urban infestation challenges and substantial health hazard concerns. Nearly one-third of American households have experienced rodent problems, creating persistent demand for effective control solutions. The U.S. smart animal trap market is estimated to grow at a significant pace with a CAGR of 7.6%, with rodent control representing the primary application. Municipal investments in citywide rodent management programs and commercial compliance requirements sustain segment dominance.

Insects/Others demonstrate the fastest growth trajectory with a CAGR of 9.3% as integrated pest management approaches expand beyond traditional rodent focus. Innovations including AI-powered insect recognition, pheromone-based smart traps, and IoT-enabled monitoring for agricultural applications, drive segment expansion. The development of smart traps capable of identifying specific pest species, including fruit flies and fall armyworm, reflects growing precision agriculture adoption.

Application Insights

The residential segment leads application categories by holding 36% market share, serving homeowner demand for convenient and effective pest control solutions. The residential pest control products market has expanded significantly over the past decade, reflecting strong demand growth driven by increasing household focus on sanitation, safety, and effective pest management solutions. Consumer preference for technology-integrated products enabling smartphone monitoring and hands-free disposal drives residential smart trap adoption. Over 13.25 million U.S. residential customers receive professional pest control services, with recurring revenue comprising 85.2% of residential service revenue.

The commercial & industrial segment exhibits the fastest growth rates, as food safety compliance with a CAGR of 9.1%, hygiene regulations, and operational efficiency requirements intensify across business establishments. Commercial pest control service revenue grew 9.0% in 2024, demonstrating robust demand expansion. Food processing facilities, warehouses, and hospitality establishments prioritize smart monitoring systems providing continuous surveillance and compliance documentation. The commercial segment's technology adoption curve accelerates as businesses recognize labor cost savings and enhanced operational visibility benefits.

Regional Market Insights

North America Smart Animal Trap Market Trends

North America commands market leadership with approximately 31% of global revenue share, underpinned by advanced technological infrastructure, substantial pest control investment, and robust regulatory frameworks supporting humane wildlife management practices. The U.S. structural pest control industry showed strong performance in 2024, reflecting 7.6% year-over-year growth. The U.S. smart animal trap market alone is estimated at ~US$110.5 million in 2026. Regulatory environment includes EPA device regulations exempting vertebrate traps from premarket registration while maintaining production standards. The region's innovation ecosystem benefits from significant R&D investment, with Rentokil Terminix opening its first pest control innovation center in Dallas, Texas in June 2024.

Market growth is sustained by the rise in rodent population in urban areas with Los Angeles, Chicago, and New York ranking among the most affected cities. Climate warming correlation with rat population increases drives municipal smart pest monitoring investments. The commercial segment demonstrates particular strength through food safety compliance requirements and digital transformation across hospitality, healthcare, and food processing sectors.

Europe Smart Animal Trap Market Trends

Europe holds a considerable market share of approximately 25% and demonstrates strong growth at 6.6% CAGR, driven by stringent animal welfare regulations and conservation-focused wildlife management priorities. The European smart animal trap market has been experiencing steady expansion, driven by rising adoption of intelligent pest management systems and growing emphasis on humane, technology-enabled wildlife control solutions. The Agreement on International Humane Trapping Standards (AIHTS) shapes market dynamics by mandating humaneness certification for traps targeting specified species. EU Regulation 3254/91 prohibits leghold traps and restricts imports from non-compliant countries.

Germany emerges as a key market with approximately 5.1% CAGR growth, emphasizing eco-efficient pest management solutions and advanced control technologies. TRAPMASTER, manufactured in Germany, represents regional innovation leadership in trap monitoring systems compatible with European network providers. Europe's 504 national parks and extensive Natura 2000 protected area network drive conservation technology adoption, with wildlife keepers increasingly deploying smart monitoring solutions for species protection.

Asia Pacific Smart Animal Trap Market Trends

Asia Pacific represents the fastest-growing region at approximately 8.8% CAGR, propelled by rapid urbanization, agricultural expansion, and growing awareness of advanced pest management solutions. China’s market is expected to continue its steady growth, supported by rising demand for advanced pest management solutions. The broader Asia-Pacific pest control sector is expanding rapidly, driven by urbanization, regulatory focus, and technology adoption. India’s pest control market is also strengthening, supported by increased residential, commercial, and industrial reliance on professional pest management services. Agricultural modernization initiatives across China, India, and ASEAN nations drive demand for IoT-enabled pest monitoring integrated with precision farming systems.

Regional growth benefits from expanding e-commerce agricultural input platforms capturing significant market share, with Alibaba's Taobao Rural reporting 280% growth in pesticide sales through 2024. Urban pest management demand intensifies as Asia-Pacific accommodates the world's largest population concentrations, creating substantial residential and commercial market opportunities. Climate-driven pest challenges, including fall armyworm outbreaks exceeding around US$2.5 billion in annual Chinese losses accelerate technology adoption.

Competitive Landscape

The global smart animal trap market exhibits a moderately fragmented competitive structure characterized by the presence of specialized technology providers, established pest control equipment manufacturers, and emerging IoT-focused startups. Leading players collectively account for an estimated 35-40% market share, with Trapmaster, Woodstream Corporation, CatchAlive ApS, and Encounter Solutions among prominent participants. Competitive positioning varies between companies emphasizing hardware manufacturing excellence, software platform development, and integrated service offerings. Market concentration is increasing as strategic acquisitions consolidate regional capabilities and technology platforms. Differentiation strategies center on sensor technology innovation, connectivity options, mobile application functionality, and species-specific solutions.

Strategic Developments

- In September 2024, Goodnature, with Automatic Trap Company, launched an advanced smart mouse trap in the U.S. featuring infrared no-touch sensors, self-resetting capability, smartphone connectivity, and rechargeable batteries, marking a major innovation in residential rodent control.

- In March 2025, Bell Laboratories introduced the Mouse iQ smart trap using Bell Sensing Technologies, offering Bluetooth connectivity for technicians to check traps remotely in confined spaces, improving accuracy and efficiency in professional pest management.

- In October 2024, Rentokil Initial expanded its partnership with Fujitec Pest Solutions to deploy AI-driven pest monitoring across Japan and Southeast Asia, supporting its broader plan to globally implement AI-enabled smart trapping systems over the next few years.

Companies Covered in Smart Animal Trap Market

- Trapmaster / Fallenmeder

- Woodstream Corporation (Victor)

- AlertHouse ApS (Minkpolice)

- CatchAlive ApS

- Encounter Solutions Ltd.

- Goodnature Limited

- Econode Ltd.

- PestSense Pty Ltd

- Wildlife Dominion Management (HogEye)

- TrapSmart LLP

- Skyhawk

- Boarmaster

- Contech Enterprises Inc.

- uWatch

- OcuTrap

Frequently Asked Questions

The global Smart Animal Trap Market was valued at US$319.5 million in 2020, expected to reach US$451.3 million in 2026, and is projected to surpass US$745.8 million by 2033.

Key drivers include escalating wildlife-induced agricultural losses, rising urban rodent populations, integration of IoT and AI technologies enhancing trap efficacy, and growing emphasis on humane animal capture methods.

The smart animal traps market demonstrated historical CAGR of 5.9% between 2020-2026 and is projected to accelerate at 7.44% CAGR from 2026-2033.

Primary opportunities include conservation and wildlife management technology expansion, commercial and industrial sector adoption for regulatory compliance, emerging market penetration across Asia-Pacific regions, precision agriculture integration enabling targeted pest intervention, and subscription-based monitoring service business model development.

Leading market participants include Trapmaster/Fallenmeder, Woodstream Corporation, AlertHouse ApS/Minkpolice, CatchAlive ApS, Encounter Solutions Ltd., Goodnature Limited, Econode Ltd., PestSense Pty Ltd, Wildlife Dominion Management/HogEye, and Skyhawk.