- Automotive Components & Materials

- Automotive Smart Keys Market

Automotive Smart Keys Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Smart Keys Market by Technology (Remote Keyless Entry (RKE), Passive Keyless Entry & Start (PKES), Biometric Entry Systems, Mobile/Digital Key, Others), Function (Single Function, Multi-Function), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles), Distribution Channel (OEM, Aftermarket), and Regional Analysis for 2026 - 2033

Automotive Smart Keys Market Size and Trend Analysis

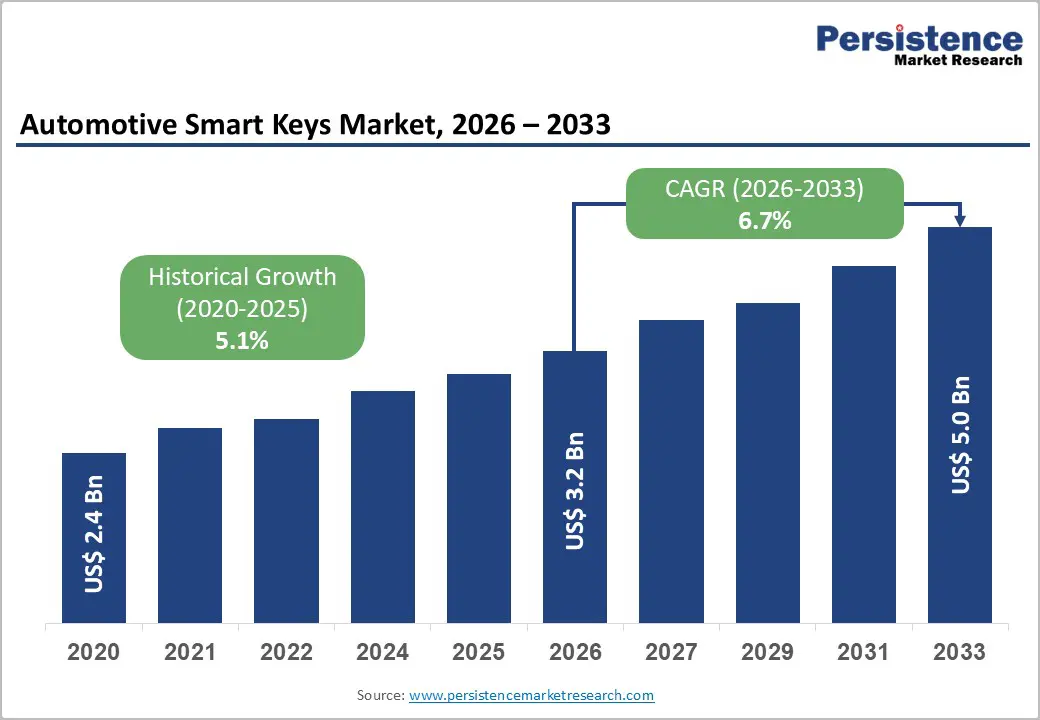

The global automotive smart keys market size is expected to be valued at approximately US$ 3.1 Bn in 2026 and is projected to reach US$ 5.0 Bn by 2033, growing at a CAGR of 6.7% between 2026 and 2033.

This robust growth is driven by the accelerating global adoption of connected and electric vehicles, rising consumer demand for keyless convenience features, and original equipment manufacturers' (OEMs') strategic emphasis on premium in-cabin technology as a differentiator. Regulatory developments mandating advanced vehicle security systems, including the United Nations Economic Commission for Europe (UNECE) Regulation No. 116 on unauthorized use of motor vehicles.

Key Industry Highlights:

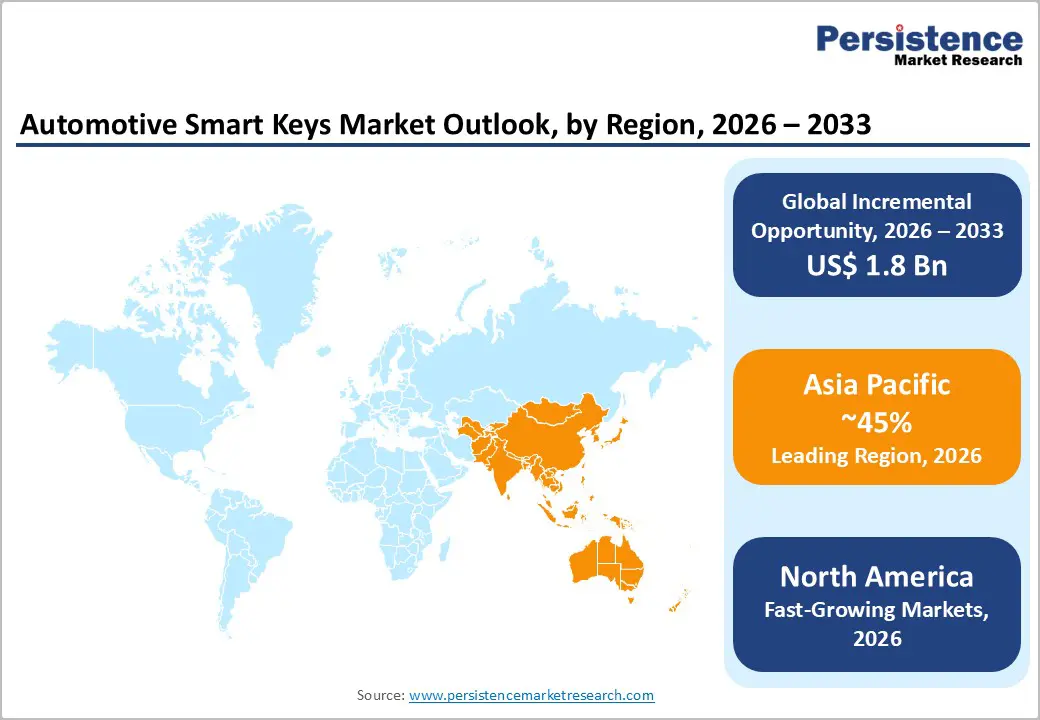

- Leading Region – Asia Pacific leads the global automotive smart keys market with approximately 45% revenue share in 2025, anchored by China's dominance as the world's largest NEV market and Japan's premium OEM technology ecosystem.

- Fastest Growing Region – India and Southeast Asia are the fastest-growing sub-regions, driven by vehicle premiumization and rising EV adoption under government incentive programs that are structurally elevating smart key fitment rates in mid-segment vehicles.

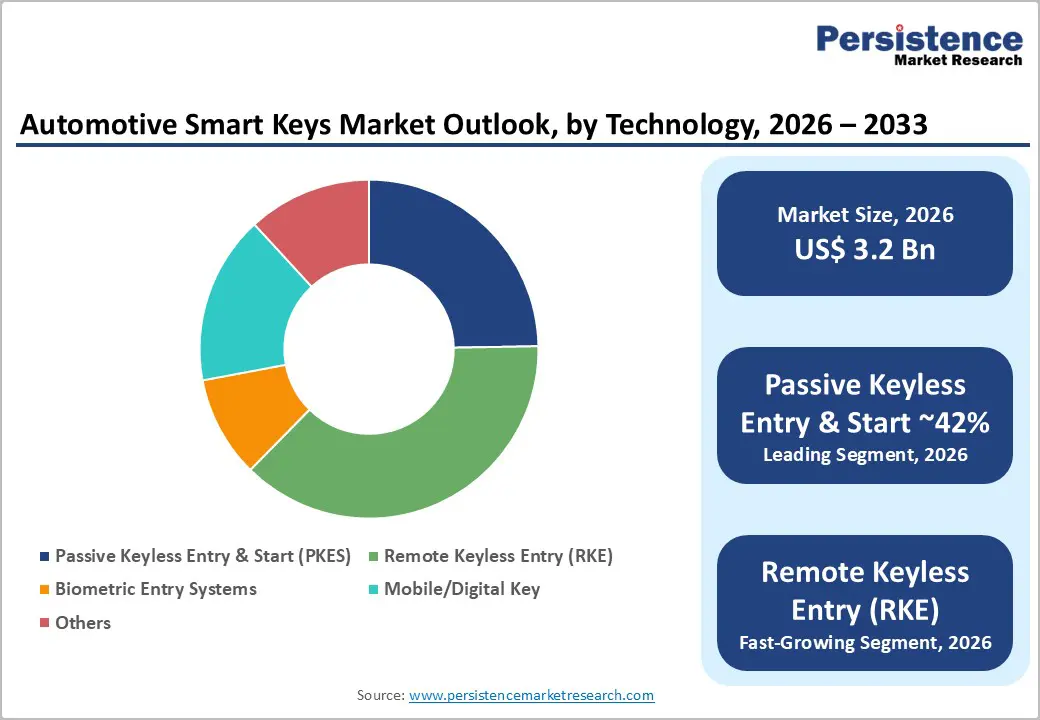

- Dominant Technology– Passive Keyless Entry & Start (PKES) holds approximately 42% technology segment share in 2025, entrenched by its status as the baseline premium entry system standard across mid-range and above vehicle programs globally.

- Fastest Growing Technology – Mobile/digital key systems are the fastest-growing technology segment, propelled by CCC Digital Key Release 3.0 adoption by leading global OEMs and the integration of UWB chipsets into mainstream smartphones by Apple and Samsung.

- Key Opportunity – The global EV sales boom, with IEA reporting 14 million EV sales in 2023 creates a structurally expanding demand base for digital key platforms, as EV architectures natively eliminate mechanical keys and default to smart entry as standard.

Market Dynamics

Drivers – Rise in Global Vehicle Electrification and Connected Vehicle Adoption Are Embedding Smart Key Technology as a Standard Feature

The global transition to electric vehicles (EVs) is a powerful structural catalyst for the automotive smart keys market, as EV platforms by design default to keyless and digital access architectures that eliminate the mechanical key entirely. According to the International Energy Agency (IEA), global EV sales surpassed 14 million units in 2023, accounting for approximately 18% of total passenger vehicle sales, with the share expected to rise substantially through the decade.

EV manufacturers, including Tesla, BYD, and Rivian, have standardized mobile/digital key systems that allow vehicle access and ignition via NFC-enabled smartphones, normalizing a user behaviour that is now influencing expectations across the broader automotive market.

Escalating Vehicle Theft Rates and Regulatory Mandates Are Accelerating the Retirement of Traditional Key Systems

Rising vehicle theft rates globally and the vulnerability of older remote keyless entry (RKE) systems to relay-attack theft methods are prompting both regulatory bodies and consumers to demand more sophisticated smart entry and anti-theft solutions. Europol's 2023 organized crime report highlighted that relay attacks on keyless vehicles accounted for a growing proportion of automobile theft in Europe, pressuring automakers to upgrade from legacy RKE to Passive Keyless Entry & Start (PKES) systems with rolling-code encryption and ultra-wideband (UWB) precision ranging.

UNECE Regulation No. 116, now adopted by over 60 countries, mandates immobilizer systems in all new light-duty vehicles, creating a regulatory floor for smart key adoption. Insurers in the UK and Germany are also offering premium discounts for vehicles equipped with certified advanced entry systems, generating a downstream consumer pull that reinforces OEM investment in smart key technology.

Restraints - High System Cost and Integration Complexity Constrain Adoption in Price-Sensitive Vehicle Segments

Advanced smart key systems, particularly PKES with UWB ranging, biometric entry, and mobile key platforms, carry a significant bill-of-materials premium over conventional mechanical or basic RKE systems, limiting their adoption in entry-level and economy vehicle segments that dominate volume sales in price-sensitive markets such as India, Southeast Asia, and Latin America.

A full PKES system can add USD 80–250 to vehicle production cost according to automotive tier-1 supplier pricing disclosures, a price increment that translates directly into reduced adoption rates among OEMs targeting sub-USD 15,000 vehicle price points. This cost barrier segments the market structurally, concentrating smart key adoption in mid-premium and luxury vehicles and constraining the addressable base in the highest-volume global vehicle segments.

Cybersecurity Vulnerabilities and Relay-Attack Exploits Are Creating Consumer Hesitancy and Liability Risk for Manufacturers

The proliferation of keyless vehicle entry systems has been accompanied by a well-documented increase in relay-based and signal-amplification theft techniques that exploit the continuous radio frequency emissions of PKES fobs. The German General Automobile Club (ADAC) tested over 400 vehicle models and found that the majority were vulnerable to relay attacks, a finding that has been widely publicized and has created measurable consumer concern around keyless entry security.

For smart key manufacturers and OEMs, this dynamic creates both reputational risk and product liability exposure, requiring ongoing investment in countermeasures, including UWB technology adoption and motion-sensing fob deactivation, that add cost and development complexity without delivering additional consumer-facing features that justify premium pricing.

Opportunities - Mobile and Digital Key Technology Represents the Fastest-Growing Segment, Unlocking New Service Revenue Models for OEMs and Suppliers

Mobile/digital key technology enabling vehicle access and start via NFC, Bluetooth Low Energy (BLE), or UWB-enabled smartphones is the fastest-growing segment within the automotive smart keys market, propelled by the convergence of smartphone ubiquity, cloud connectivity, and OEM investment in software-defined vehicle platforms. The Car Connectivity Consortium (CCC) released Digital Key Release 3.0 in 2021, establishing an industry-wide standard for UWB-based digital keys that has since been adopted by BMW, Hyundai, Mercedes-Benz, and Volkswagen, among others.

Beyond convenience, digital key platforms enable OEMs to offer subscription-based access sharing, fleet management integrations, and valet mode features that generate recurring software revenue fundamentally transforming the smart key from a one-time hardware sale into a platform for ongoing customer engagement.

Electric Vehicle Proliferation in Asia Pacific Creates a Structurally Expanding Demand Base for Integrated Smart Entry Platforms

Asia Pacific and China specifically is the world's largest and fastest-growing EV market, and since EV architectures natively favor digital and keyless entry systems, this regional growth dynamic directly translates into accelerating smart key adoption at scale. China's Ministry of Industry and Information Technology (MIIT) reported that NEV (New Energy Vehicle) sales in China reached 9.5 million units in 2023, representing approximately 32% of total vehicle sales, the highest penetration rate globally.

Chinese domestic EV brands, including BYD, NIO, Xpeng, and Li Auto, are competing aggressively on digital cockpit and entry technology features, embedding mobile key and biometric entry as standard across their lineups to differentiate in an intensely competitive market. International smart key system suppliers and Tier-1 automotive technology companies that establish localized engineering and supply chain capabilities in China and South Korea are positioned to capture a disproportionate share of this rapidly expanding demand base through the forecast period.

Category-wise Insights

Technology Analysis

Passive Keyless Entry & Start (PKES) leads the technology segment with approximately 42% market share in 2025, reflecting its dominant position as the premium standard entry system across mid-range and luxury passenger vehicles globally. PKES systems enable hands-free door unlocking and push-button ignition when the authenticated fob is within proximity, a user experience that has become an expected feature in vehicles above the entry-level price tier.

According to the European Automobile Manufacturers' Association (ACEA), the share of new vehicles in Europe equipped with at least PKES-level entry systems exceeded 55% in recent model years, demonstrating the technology's mainstream penetration in the region's significant premium automotive segment.

Function Insights

Multi-Function smart keys lead the function segment with approximately 64% market share in 2025, a position driven by consumer preference for consolidated vehicle control capabilities, including remote start, window operation, trunk release, and personalization settings within a single integrated fob or digital key interface.

The automotive industry's transition to software-defined vehicles is further accelerating the bundling of functions into smart key platforms, as OEMs leverage the key-vehicle communication channel to deliver OTA feature updates. Single-function basic remote keyless entry systems are declining in new vehicle fitment as even volume-segment OEMs shift toward multi-function PKES as a standard fitment to improve their vehicles' perceived value positioning in competitive segment comparisons.

Vehicle Type Insights

Passenger cars dominate the vehicle type segment with approximately 68% market share in 2025, anchored by the sheer volume of global passenger car production, with the International Organization of Motor Vehicle Manufacturers (OICA) reporting over 67 million passenger vehicles produced globally in 2023 and the consistently high smart key fitment rates in mid-to-premium passenger car segments.

The passenger car segment encompasses both the highest-volume OEM smart key contracts and the fastest technology upgrade cycles, as consumer-facing feature competition among automakers drives rapid adoption of new entry system generations. Electric Vehicles (EVs) are the fastest-growing vehicle type sub-segment, with essentially 100% digital/smart key fitment across virtually all EV models currently on the market, making EV volume growth a direct and reliable proxy for smart key demand growth.

Distribution Channel Analysis

The OEM channel leads the distribution segment with approximately 78% market share in 2025, reflecting the embedded nature of smart key systems as factory-installed vehicle equipment that is specified, validated, and procured by automakers through multi-year supply agreements with Tier-1 system integrators. OEM contracts for smart key systems are typically awarded two to four years ahead of vehicle production launch, aligning with automotive platform development cycles, creating highly predictable, long-duration revenue streams for qualified suppliers.

The Aftermarket segment, while smaller, is growing as consumers seek replacement smart key fobs, key programming services, and upgrade installations for older vehicles, supported by the expanding service networks of specialist automotive electronics retailers and independent workshops.

Regional Insights

North America Automotive Smart Keys Market Trends & Analysis

North America represents a mature and innovation-driven market for automotive smart keys, characterized by high base penetration of PKES across mid-range and above vehicle segments and accelerating adoption of UWB-based digital key solutions. The U.S. vehicle fleet's progressive premiumization, with SUVs and trucks accounting for over 80% of new vehicle sales according to the Alliance for Automotive Innovation, sustains high smart key fitment rates. Growing OEM investment in connected vehicle platforms and smartphone-based digital key rollouts is repositioning North America as a key battleground for next-generation entry technology.

U.S. Automotive Smart Keys Market Size

The United States commands approximately 85% of the North American smart keys market, underpinned by its dominant position in global premium vehicle consumption and the high prevalence of PKES and digital key systems across the popular light truck and SUV segments. Ford, General Motors, and Stellantis have progressively standardized PKES across their F-150, Silverado, and Ram pickup lines the top-selling U.S. vehicle nameplates creating enormous volume-level demand.

Europe Automotive Smart Keys Market Trends, Drivers & Insights

Europe is the most regulatory-advanced regional market for automotive smart keys, shaped by UNECE Regulation No. 116 mandates, strong premium OEM heritage, and active government investment in connected vehicle infrastructure. The region's concentration of premium vehicle manufacturers BMW, Mercedes-Benz, Audi, Volkswagen, and Stellantis, drives systematic adoption of the most advanced smart entry technologies. Cybersecurity regulations under UNECE WP.29 R155 are compelling OEMs to upgrade legacy keyless systems to encryption-hardened UWB platforms, adding a regulatory pull to consumer-facing demand drivers.

Germany Automotive Smart Keys Market Size

Germany holds approximately 28% of the European automotive smart keys market, directly reflecting its status as home to the world's most influential premium automotive OEMs. BMW Group, Mercedes-Benz, and Volkswagen Group collectively produce millions of vehicles annually, virtually all equipped with PKES or more advanced smart entry systems, and their global product platforms export German smart key fitment standards worldwide.

U.K. Automotive Smart Keys Market Size

The United Kingdom accounts for approximately 13% of the European market. The UK's ZEV Mandate, requiring 22% of new car sales to be zero-emission in 2024, rising to 100% by 2035, is expanding the share of EV platforms with native digital key architectures. UK consumer sensitivity to vehicle theft, following published ADAC-equivalent vulnerability studies by Thatcham Research, is also accelerating OEM adoption of UWB anti-relay-attack countermeasures in vehicles sold in the UK.

France Automotive Smart Keys Market Size

France represents approximately 11% of the European automotive smart keys market. Stellantis and Renault Group, both headquartered in France are significant drivers of smart key adoption across their European and global product ranges. France's ambitious ZFE (Zero Emission Zone) urban clean mobility zones and government-backed EV purchase subsidies are accelerating EV sales, with Renault's digital key integration across its Megane E-Tech and 5 E-Tech EV platforms contributing to rising smart entry system demand in the French market.

Asia Pacific Automotive Smart Keys Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing regional market for automotive smart keys, led by China's dominance as both the world's largest vehicle production base and its most dynamic EV market. China's MIIT reported NEV sales of 9.5 million units in 2023, approximately 32% of total new vehicle sales, and essentially all NEV models include standard smart entry systems. Beyond China, Japan's premium domestic brands and South Korea's Hyundai-Kia group are advancing UWB and digital key adoption at scale.

China Automotive Smart Keys Market Size

China is the single largest country market globally, accounting for approximately 45% of Asia Pacific's smart keys revenue in 2025. The explosive growth of domestic NEV brands BYD, NIO, Xpeng, Geely, and SAIC, which routinely offer mobile key and biometric entry as standard, has made China the world's most competitive laboratory for next-generation smart entry technology.

India Automotive Smart Keys Market Size

India holds approximately 10% of the Asia Pacific smart keys market, with demand concentrated in the rapidly growing mid-premium vehicle segment. Maruti Suzuki, Hyundai India, Tata Motors, and Mahindra are progressively standardizing PKES across their popular SUV nameplates, including the Creta, Nexon, and Scorpio-N in response to consumer demand for premium features at accessible price points.

Japan Automotive Smart Keys Market Size

Japan represents approximately 16% of the Asia Pacific automotive smart keys market, underpinned by its world-class automotive technology ecosystem and the global production footprint of Toyota, Honda, Nissan, and Denso. Japanese OEMs are actively advancing smart key miniaturization and energy efficiency, with Toyota's latest smart key systems incorporating motion-sensor sleep modes specifically engineered to counter relay-attack theft.

Competitive Landscape

The global automotive smart keys market is moderately consolidated at the system integration level, with Continental AG, Denso Corporation, Huf Group, Valeo, and Alps Alpine collectively holding an estimated 55–60% of global OEM smart key system revenue.

Market leadership in this sector rewards both scale to absorb lengthy OEM qualification and validation cycles and deep software capability, as digital key and UWB platform differentiation increasingly drives program awards. Strategic themes include investment in UWB chip integration, CCC Digital Key platform compliance, and cybersecurity hardening in response to UNECE WP.29 R155 requirements.

Key Developments:

- In February 2026, the Tata Punch EV facelift was launched in India. This is the first major update to Tata’s smallest electric SUV since its introduction, bringing with it styling tweaks inspired by the ICE Punch, and features smart keyless entry.

- In December 2025, Kia unveiled the all-new Seltos in India, featuring significant upgrades. The vehicle features Smart Key Proximity Unlock. The SUV comes in four core variants – HTE, HTK, HTX, and GTX – with the X-Line package exclusive to the GTX.

Global Automotive Smart Keys Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 2.4 Bn |

|

Current Market Value (2026) |

US$ 3.2 Bn |

|

Projected Market Value (2033) |

US$ 5.0 Bn |

|

CAGR (2026-2033) |

6.7% |

|

Leading Region |

Magnesium steering wheels, 42% share |

|

Dominant Application |

Passive Keyless Entry & Start, 42% share |

|

Top-ranking Product |

Passenger Cars, 68% |

|

Incremental Opportunity |

US$ 1.8 Bn |

Companies Covered in Automotive Smart Keys Market

- Continental AG

- Denso Corporation

- Valeo SA

- Huf Group

- Alps Alpine Co. Ltd.

- Mitsubishi Electric Corporation

- Tokai Rika Co. Ltd.

- Lear Corporation

- Dorman Products Inc.

- Fortin Electronic Systems

- Directed Electronics

- Strattec Security Corporation

- Hella GmbH & Co. KGaA

- Silca (Kaba Group)

- UFI Filters

Frequently Asked Questions

The global automotive smart keys market is estimated at approximately US$ 3.1 billion in 2026, growing from US$ 2.4 billion in 2020 at a historical CAGR of 5.1% (2020–2025). The market is projected to reach US$ 5.0 billion by 2033, expanding at a CAGR of 6.7%, driven by EV proliferation, OEM smart entry standardization, and mobile/digital key platform adoption.

The primary demand drivers are the global transition to electric vehicles with IEA reporting 14 million EV sales in 2023, nearly all with native smart entry architectures rising consumer demand for keyless convenience features, UNECE Regulation No. 116 mandates for advanced vehicle security, and OEM investment in digital cockpit and connected vehicle platforms that embed smart key systems as foundational access technology.

Passive Keyless Entry & Start (PKES) leads the technology segment with approximately 42% market share in 2025. Its dominance is anchored by widespread OEM adoption as the standard entry system across mid-range and premium vehicle segments globally, with ACEA data showing PKES fitment rates exceeding 55% in European new vehicle sales a benchmark that signals its mainstream, rather than premium-only, positioning.

Asia Pacific leads the global automotive smart keys market with approximately 45% revenue share in 2025. China is the dominant country market, accounting for approximately 45% of regional revenue, driven by its position as the world's largest NEV market with 9.5 million NEV sales recorded in 2023 per China's MIIT virtually all equipped with advanced smart entry systems as standard.