- Clothing, Footwear, & Accessories

- Smartphone Screen Protector Market

Smartphone Screen Protector Market Size, Share, Trends, Regional Forecasts 2026 - 2033

Smartphone Screen Protector Market Product Type (Clear Screen Protectors, Privacy Screen Protectors, Anti-glare / Matte Screen Protectors, Miscellaneous), Material Type (Tempered Glass, Polyethylene Terephthalate, Thermoplastic Polyurethane), Price Range (Economy, Mid-Range, Premium), and Regional Analysis from 2026 - 2033

Smartphone Screen Protector Market Share and Trends Analysis

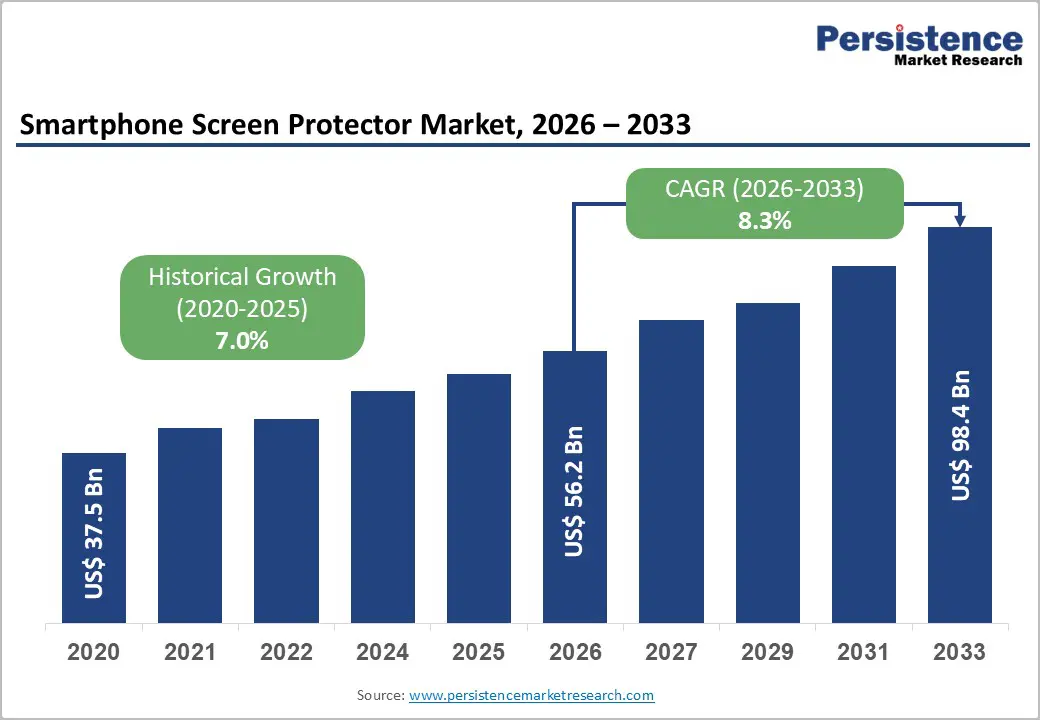

The global smartphone screen protector market size is anticipated at US$56.2 Billion in 2026 and is projected to reach US$98.4 Billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033. Market expansion is fundamentally driven by the proliferation of premium smartphones with high-end displays, rising consumer awareness of device protection, and technological advances in protective materials.

E-commerce channel expansion has democratized access to diverse protection solutions across geographies, while post-pandemic emphasis on hygiene and privacy concerns has created demand for specialized protectors with antimicrobial and privacy-filtering capabilities. The market's resilience reflects the essential nature of screen protection as consumers increasingly view it as a non-negotiable investment to preserve device longevity and aesthetic appeal.

Key Industry Highlights:

- Tempered Glass Dominance: Tempered glass maintains a 61% material market share, driven by superior durability and optical clarity; however, TPU is growing at a 9.2% CAGR, driven by foldable device compatibility and self-healing properties.

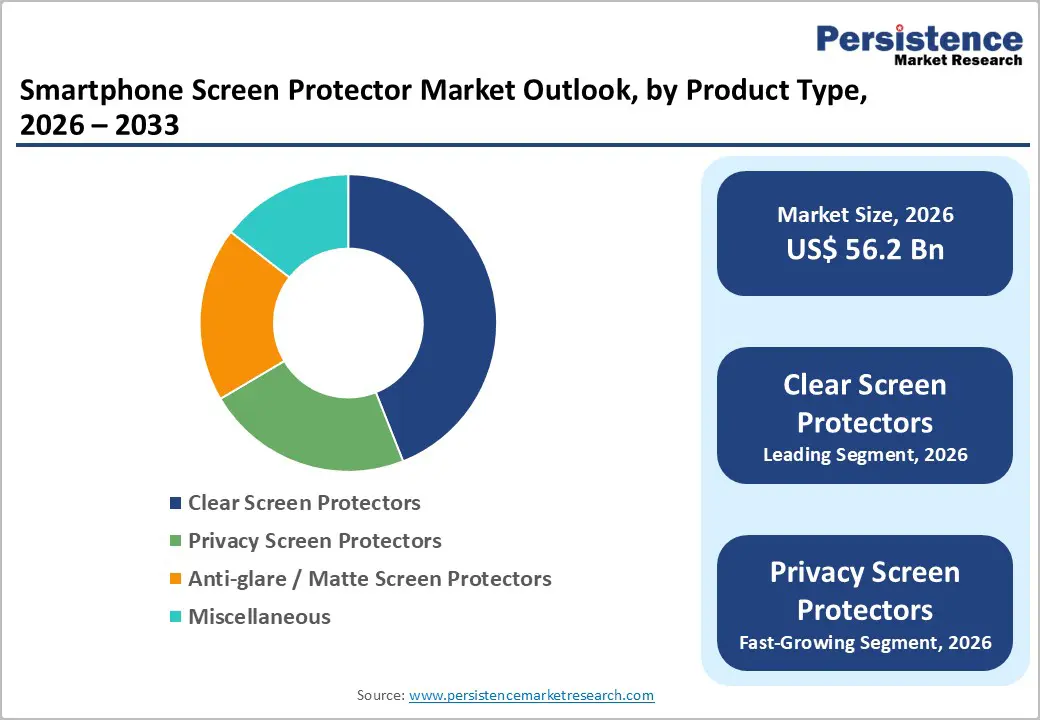

- Clear Screen Protectors Market Leadership: Clear protectors command 44% product segment share and the highest volume penetration; privacy screen protectors are accelerating at a 9.4% CAGR, driving market diversification toward specialized functional protection.

- Premium Segment Acceleration: Premium-priced protectors expand fastest at 9.9% CAGR as consumers increasingly treat protection as an essential investment for flagship devices; Western brands maintain a distribution advantage in developed markets.

- Strategic Manufacturing Shift: BIS-certified domestic production launch in India (2025) signals a structural shift toward geographic manufacturing diversification, establishing potential supply chain alternatives to the China-dominant historical structure.

| Key Insights | Details |

|---|---|

|

Smartphone Screen Protector Market Size (2026E) |

US$ 56.2 billion |

|

Market Value Forecast (2033F) |

US$ 98.4 billion |

|

Projected Growth CAGR (2026-2033) |

8.3% |

|

Historical Market Growth (2020-2025) |

7.0% |

Market Dynamics Analysis

Drivers - Rising Smartphone Penetration and Device Replacement Economics

Smartphone ownership has evolved from a luxury category to a necessity across developed and emerging markets. Global smartphone penetration continues expanding, particularly in the Asia Pacific regions where India and China collectively represent over 2 billion active users. This installed-base growth directly translates into accelerating demand for protective accessories. More critically, manufacturers' strategic pricing of premium flagship devices with display replacement costs often exceeding US$200-400 has fundamentally altered consumer economics. Rather than risk expensive screen repairs, consumers increasingly opt for screen protectors as a preventive measure, thereby creating a secondary accessory market directly tied to device sales velocity. The market has shifted from a discretionary to an essential accessory status, with penetration rates in developed markets exceeding 60% among premium device users. This structural economic advantage ensures steady demand independent of broader economic cycles.

Technological Advancement in Protective Materials and Coatings

Material science innovation has transformed product capability over the past five years. Tempered glass technology now delivers improved impact absorption through enhanced annealing processes, while thermoplastic polyurethane (TPU) formulations provide edge-to-edge coverage for curved displays without optical distortion. Manufacturers have successfully integrated multifunctional properties, such as blue-light filtering, anti-glare capabilities, antimicrobial coatings, and oleophobic surfaces, into single protective layers. These innovations address specific consumer pain points: eye strain from extended use, post-pandemic hygiene concerns, and privacy protection in public environments. Corning's Gorilla Glass technology and similar advanced formulations have established performance benchmarks that validate consumer investment in quality protection, supporting premium pricing and margin expansion for market leaders.

Restraints - Intense Competition and Margin Compression

The smartphone screen protector market exhibits structural characteristics of commodity industries with low barriers to entry. Established players such as ZAGG, Belkin, and Spigen compete with numerous emerging manufacturers, particularly from China and Southeast Asia. This competitive intensity has relentlessly compressed wholesale and retail margins, creating a bifurcated market: premium players defending positions through brand equity and innovation, while cost-competitive manufacturers capture volume in economy segments. Price-sensitive consumers increasingly default to the lowest-cost options, undermining profitability for mid-tier competitors. Promotional intensity has escalated, with online marketplaces featuring aggressive discounting that erodes the perceived value of higher-quality protectors. This dynamic particularly pressures regional manufacturers lacking distribution scale or R&D resources to differentiate their offerings effectively.

Counterfeit Products and Supply Chain Vulnerabilities

The prevalence of counterfeit screen protectors represents a systemic market constraint affecting both consumers and legitimate manufacturers. Low-cost imitation products flooding e-commerce platforms damage brand equity and consumer trust, as counterfeits often exhibit inferior optical clarity, poor adhesion, and inadequate protective properties. The tempered glass segment, valued at approximately 61% of the market, is particularly vulnerable to counterfeiting due to the technical sophistication perceived by consumers, despite relatively simple manufacturing requirements. Supply chain disruptions stemming from raw material sourcing constraints and geopolitical trade tensions have led to inventory volatility. Post-pandemic logistics normalization remains incomplete in certain regions, creating fulfillment challenges for specialized products like foldable device protectors that require precise manufacturing tolerances.

Opportunities - India's Emerging Domestic Manufacturing Ecosystem

India represents perhaps the highest-potential growth opportunity in the near-term market landscape. The country consumes approximately 400 million tempered glass screen protectors annually, valued at approximately 20,000 crores (US$2.4 billion), yet over 90% are currently imported with inconsistent quality. The 2025 launch of BIS-certified, domestically manufactured screen protectors through partnerships like Optiemus Infracom and Corning has catalyzed a structural shift toward localized production. This development addresses both government manufacturing incentives (aligned with Atmanirbhar Bharat objectives) and market quality standardization. The opportunity extends beyond domestic consumption. Indian manufacturers have the potential to supply export markets across Africa and Southeast Asia, leveraging cost advantages and proximity to supply chains. Conservative estimates suggest the domestic opportunity could capture US$500 million-1 billion in incremental market value over 2025-2030 as import substitution accelerates.

Privacy and Specialized Coating Segments

Privacy screen protectors represent the fastest-growing specialized category, expanding at 9.4-11.94% CAGR as regulatory environments emphasize data protection (GDPR, CCPA) and professional users seek visual privacy in public spaces. This segment supports premium pricing justified by added technological complexity and addresses growing corporate spend on employee cybersecurity. Blue-light filtering protectors similarly address documented consumer concerns about eye strain and sleep disruption from extended device use, with adoption rates increasing by 12% annually. The market opportunity arises from education campaigns that link health benefits to purchase decisions, particularly among younger consumers and corporate purchasing departments. Bundling privacy and blue-light filtering into enterprise device protection programs creates recurring revenue opportunities and customer lock-in absent from consumer markets.

Category-wise Analysis

Product Type Insights

Clear screen protectors remain the foundational product category, commanding 44% of the global market by volume and value. This leadership reflects consumer preference for optical transparency, thereby preserving original display aesthetics and color accuracy, which are critical for premium device owners and photography enthusiasts. Clear protectors act as accessible entry products, establishing brand relationships that enable upselling into specialized variants. Tempered glass dominates due to its superior clarity relative to plastics, while retail ubiquity and competitive pricing sustain volumes despite global margin pressure.

Privacy screen protectors represent the fastest-growing segment, expanding at 9.4% CAGR, driven by workplace security mandates and rising consumer privacy awareness. Using microlouvre technology, they restrict off-angle visibility, protecting data in public settings. Corporate cybersecurity policies mandate adoption, enabling procurement channels and positioning protectors to reach a considerable share by 2033.

Material Type Insights

Tempered glass accounts for 61% of the market, establishing itself as the premium protection standard across consumer segments. Superior hardness, typically rated 9H on the Mohs scale, provides strong scratch resistance, while annealing processes enhance impact absorption and reduce the risk of shattering. Ongoing material innovation by leading manufacturers has created clear quality differentiation, thereby justifying premium pricing relative to polymers. Tempered glass also preserves optical clarity for high-pixel-density displays, supported by mature supply chains and scalable manufacturing economics globally across multiple price tiers.

TPU is the fastest-growing material, expanding at 9.2% CAGR, driven by curved, bezel-less, and foldable display designs. Its flexibility enables edge coverage, self-healing mitigates scratches, and compatibility with new form factors supports adoption. Improved clarity and touch response narrow gaps with glass, positioning TPU to approach a considerable share by 2033.

Price Range Insights

The economy price range commands 47% of the global market, reflecting cost sensitivity in emerging markets and replacement-driven demand. Economy protectors function as gateway products, introducing consumers to device protection and establishing brand relationships for future upgrades. Asian manufacturers, especially Chinese and Vietnamese producers, dominate through vertical integration and labor advantages. Retail pricing of approximately US$2–5 supports high volumes but requires scale and efficient supply chains. Competition is intense, yet the segment remains structurally vital owing to constraints on purchasing power.

Premium screen protectors are the fastest-growing price segment, with a 9.9% CAGR, driven by rising adoption of flagship devices. Advanced materials, functional coatings, and edge-to-edge designs justify prices of US$15–35, enabling R&D and branding. Demand remains resilient across cycles, with premium protection increasingly viewed as a lifestyle investment.

Regional Insights

North America Smartphone Screen Protector Market Trends

North America is a mature, high-value market in which established consumer preferences and robust distribution infrastructure sustain demand. The region accounts for roughly 18% of global value, reflecting a premium product mix and price realization that exceed those of developing markets. A projected 7.8% CAGR is supported by flagship replacement cycles, foldable adoption among affluent users, and rising use of privacy and specialty protectors among professionals. The U.S. leads through sophisticated retail channels, strong brands such as ZAGG and OtterBox, and a willingness to pay for quality. Regulatory focus on consumer protection sets global benchmarks, while advanced e-commerce platforms concentrate purchasing power, accelerate the uptake of innovation, and support sustainability-driven premium positioning across the broader smartphone accessories ecosystem over the medium to long term, regionally.

Europe Smartphone Screen Protector Market Trends

Europe accounts for approximately 21% of the global smartphone screen protector market value, reflecting a mature, highly regulated landscape with elevated quality expectations and strong brand loyalty. Smartphone penetration exceeds 85% across developed countries, with premium device ownership concentrated in Northern and Western Europe. Consumers favor established brands such as PanzerGlass, Tech21, and Belkin, supporting premium pricing and margin stability. Germany, the United Kingdom, France, and Spain account for nearly 65% of regional value, while Northern Europe shows the highest per capita accessory spending. EU regulations emphasize sustainability and the reduction of electronic waste, favoring the use of recycled materials. GDPR heightens privacy awareness, driving a 10–12% CAGR in privacy protection. Advanced retail networks and strict supply chain governance create entry barriers and elevate manufacturing standards regionwide globally.

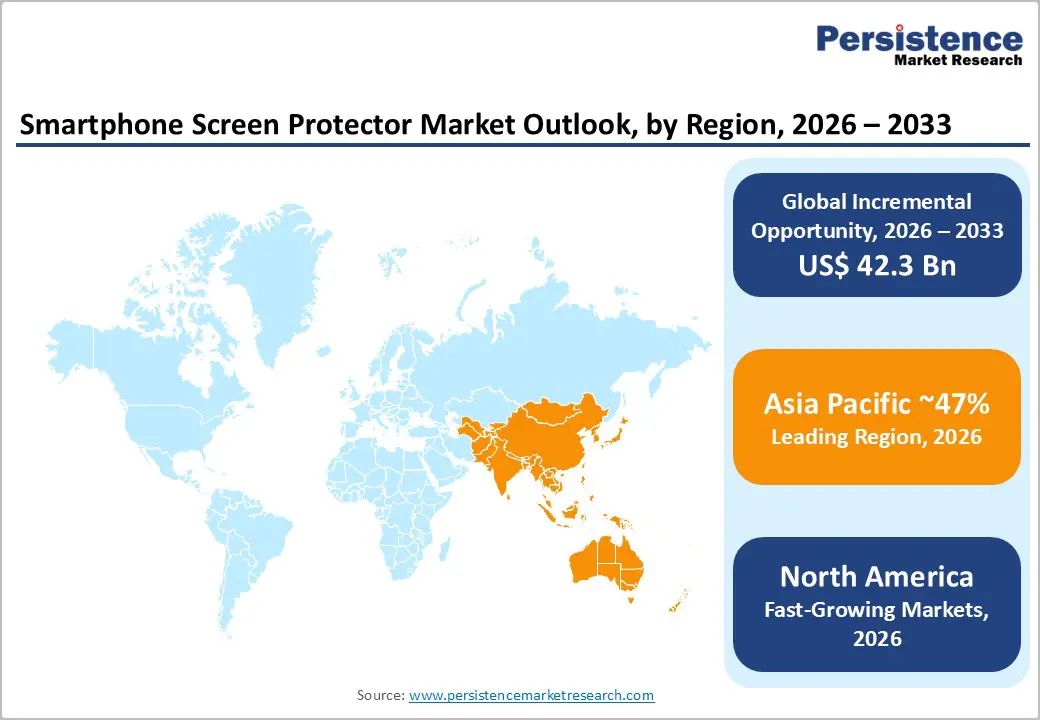

Asia Pacific Smartphone Screen Protector Market Trends

Asia-Pacific accounts for an overwhelming share, commanding approximately 47% of global volume and expanding rapidly. China alone accounts for approximately 18–22% of global value, supported by the world’s largest smartphone installed base and a growing middle class that prioritizes protection. India shows exceptional momentum, with a 9.1% CAGR projected through 2032 as penetration rises from ~35% in 2020 to 75%, thereby increasing accessory demand. Japan and South Korea retain premium positioning, with consumers favoring advanced technologies and higher prices. The region accounts for 75–80% of global manufacturing capacity, thereby providing cost and logistics advantages. Chinese vertical integration accelerates innovation cycles, while India’s emerging domestic production and incentives gradually diversify a historically China-centric supply base, thereby supporting long-term investment, employment creation, and the growth of resilient regional ecosystems.

Competitive Landscape

Market leaders employ differentiated strategic approaches: premium Western brands emphasize innovation, brand heritage, and distribution control; cost-competitive Asian manufacturers leverage volume scale and e-commerce channel presence. Dominant themes include product specialization (privacy, blue-light, antimicrobial variants), technological partnership (Corning partnerships establishing material standards), and vertical integration (manufacturing control reducing supply chain risk). Emerging business model trends include direct-to-consumer digital channels reducing retail intermediary dependency, subscription models for enterprise privacy solutions, and device OEM partnerships embedding protection solutions into launch ecosystems.

Strategic Developments:

- In August 2025, Optiemus Infracom, partnering with Corning, launched BIS-certified RhinoTech screen protectors—the world’s first such certification—reducing India’s 90% import dependence while aligning with government manufacturing initiatives and enabling domestic and export market expansion.

- In March 2024, Apple strengthened its control of the accessory ecosystem by formalizing a collaboration with Belkin for the iPhone 15 lineup, reinforcing premium brand positioning, expanding curated retail distribution, and limiting competitors' access to Apple’s high-value sales channels.

Companies Covered in Smartphone Screen Protector Market

- ZAGG Inc.

- Belkin International

- OtterBox (Otter Products, LLC)

- Spigen Inc.

- 3M

- Anker Innovations

- RhinoShield

- Tech21

- Case-Mate

- Mophie

- PanzerGlass

- Nillkin

- Baseus

- BodyGuardz

- Whitestone Dome

Frequently Asked Questions

The global Smartphone Screen Protector Market size was valued at US$37.5 Billion in 2020 and reached US$56.1Billion in 2026, with projections to attain US$98.4 Billion by 2033.

Market growth is fueled by rapid smartphone penetration, high screen replacement costs, advances in tempered glass and TPU technologies, e-commerce expansion, stricter data privacy regulations, and rising demand for hygiene-, privacy-, and eye-protection features.

The Smartphone Screen Protector Market is projected to grow at a CAGR of 8.3% between 2026 and 2033.

Major opportunities include India’s domestic manufacturing potential, foldable device protection solutions, rapid growth of privacy protectors, sustainable material adoption, and enterprise-focused privacy offerings.

Leading players include ZAGG, Belkin, OtterBox, Spigen, 3M, Anker, RhinoShield, Tech21, Case-Mate, Mophie, Nillkin, Baseus, and emerging Indian manufacturer RhinoTech.