- Automotive Components & Materials

- Smart Glass in Automotive Market

Smart Glass in Automotive Market Size, Share, and Growth Forecast, 2025 - 2032

Smart Glass in Automotive Market by Technology Type (Electrochromic, Polymer Dispersed Liquid Device (PDLC), Suspended Particle Device (SPD)), Vehicle Type (Passenger Cars, Commercial Vehicles), Application (Rear and Side Windows, Sunroof Glass, Front and Rear Windshield), and Regional Analysis for 2025 - 2032

Smart Glass in Automotive Market Size and Trend Analysis

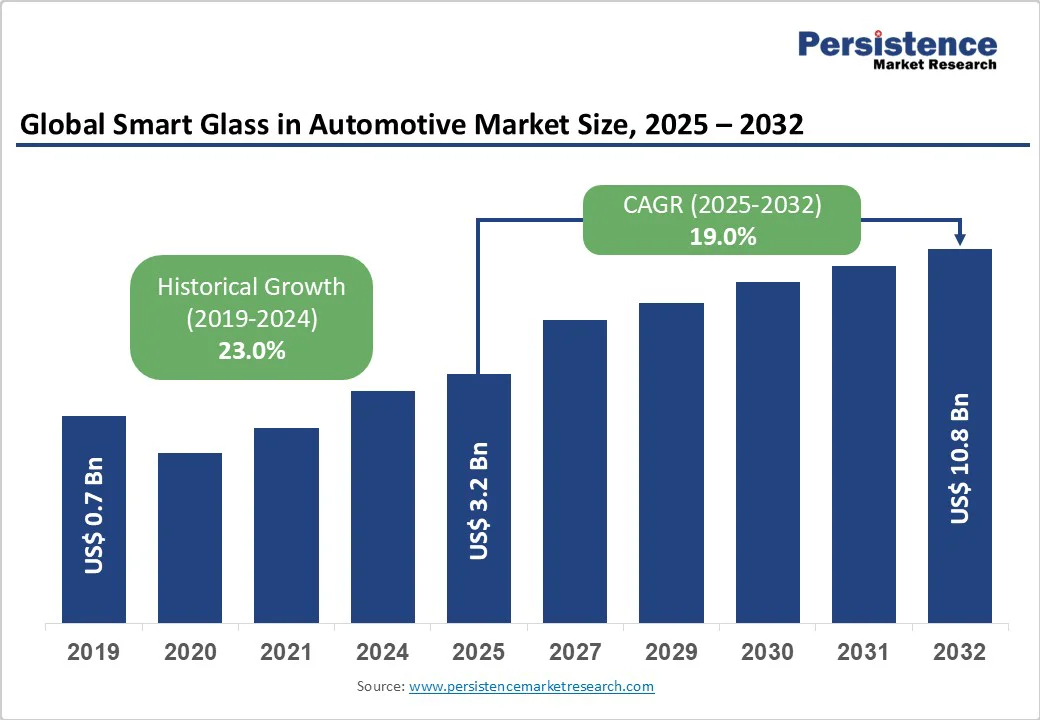

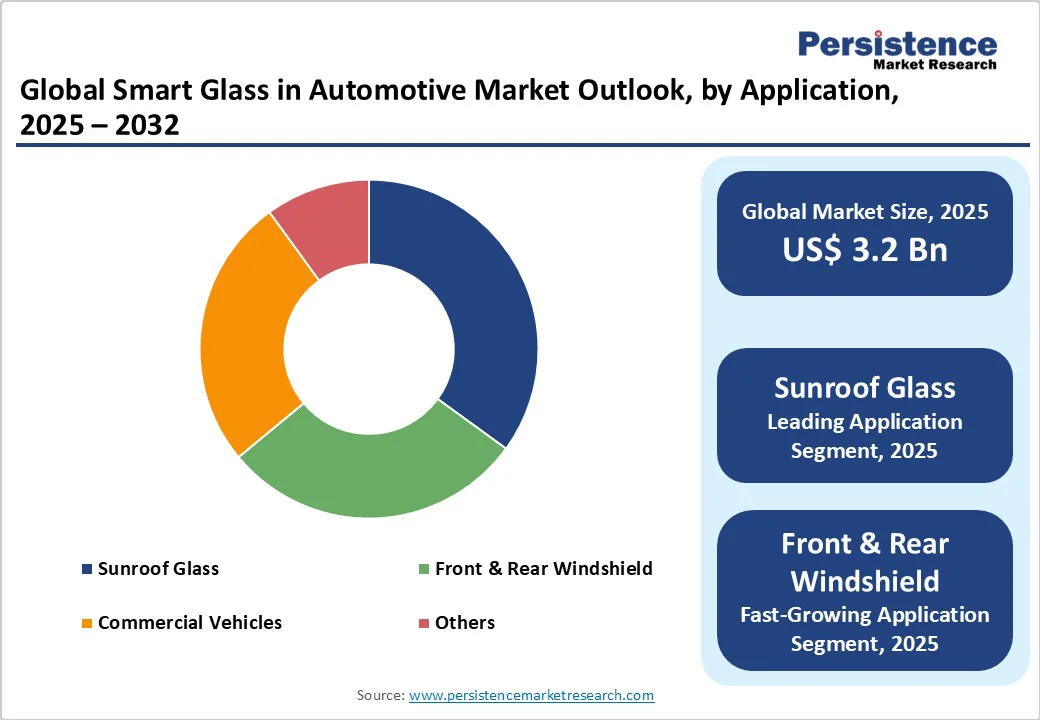

The global smart glass in automotive market size is likely to be valued at US$3.2 bn in 2025 and is expected to reach US$10.8 bn by 2032, growing at a CAGR of 19.0% during the forecast period from 2025 to 2032.

The increasing adoption of electric vehicles and advanced automotive features is a key growth driver. Rising consumer demand for energy-efficient, comfortable, and high-tech vehicle interiors encourages integration of smart glass technologies.

Key Industry Highlights:

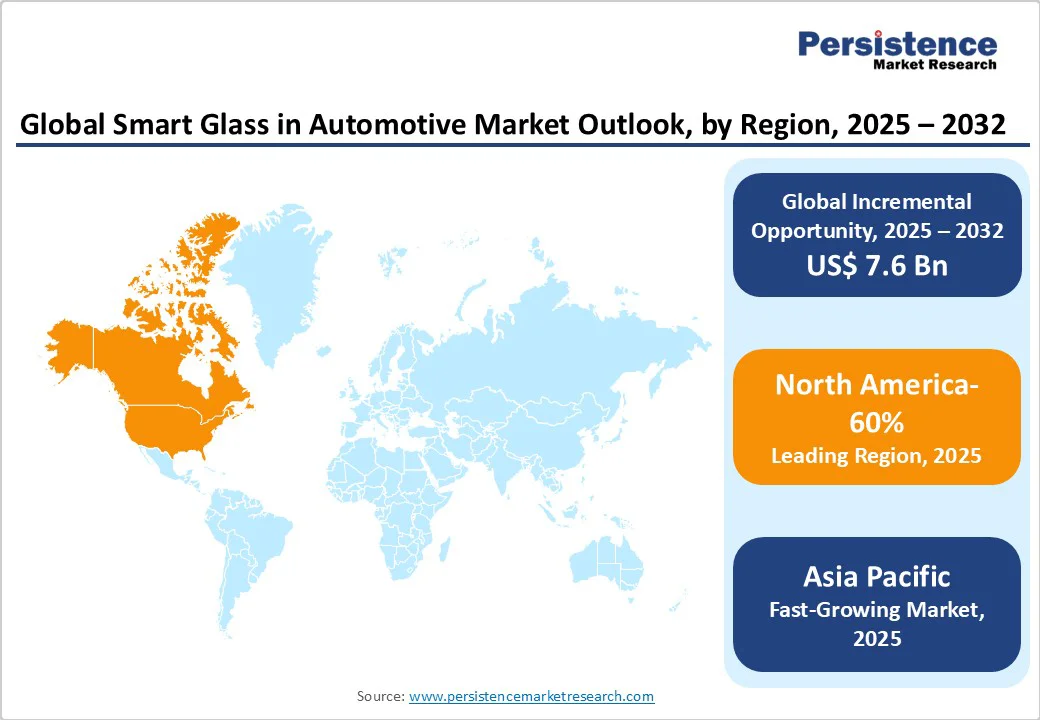

- Leading Region: North America holds a 60% global smart glass in automotive market share in 2025, supported by strong EV adoption in the U.S. and growing demand for luxury vehicle smart glass features.

- Fastest-growing Region: Asia Pacific is expanding rapidly, driven by China’s automotive production, India’s infrastructure growth, and increasing adoption of energy-efficient and comfort-enhancing smart glass technologies.

- Dominant Technology Type: Electrochromic glass leads with a 45% share, offering superior energy efficiency, customizable tint control, and integration in passenger vehicle sunroofs and windshields.

- Dominant Vehicle Type: Passenger cars dominate with a 60% share, reflecting high consumer demand for comfort, advanced glazing, and premium features in mid-range and luxury models.

- Dominant Application: Sunroof glass holds a 35% share, propelled by its popularity in luxury vehicles, enhancing interior comfort, aesthetics, and cabin temperature control.

- Key Developments: In 2024, Ford’s F-150 Lightning sales surged, while Gauzy Ltd. launched a prefabricated electrochromic smart glass stack for electric vehicle applications.

| Key Insights | Details |

|---|---|

| Smart Glass in Automotive Market Size (2025E) | US$3.2 Bn |

| Market Value Forecast (2032F) | US$10.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 19.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 23.0% |

Market Dynamics

Driver: Increasing Adoption of Electric Vehicles and Smart Automotive Features

The rising adoption of electric vehicles (EVs) is a major catalyst for the growth of smart glass in the automotive market. EVs emphasize aerodynamics, lightweight structures, and energy efficiency, which has increased the use of panoramic roofs and large windshields. Smart glass technologies, such as electrochromic and suspended particle device (SPD) glass, allow dynamic control of light and heat inside the vehicle.

This reduces glare, improves passenger comfort, and lowers the load on air conditioning systems-helping extend battery range. As EV customers often expect advanced, futuristic features, smart glass provides both functional and premium value.

Government support is also driving this trend. For instance, India’s NITI Aayog projected that nearly 90% of new cars will feature advanced driver-assistance and smart technologies by 2030, compared to about 42% in 2020. Additionally, government schemes such as the Production Linked Incentive (PLI) and FAME II for EVs encourage manufacturers to adopt innovative technologies, further boosting smart glass integration.

Restraint: High Costs and Manufacturing Complexity

The high cost of smart glass and its complex manufacturing process act as significant restraints in the automotive market. Smart glass technologies, such as electrochromic and SPD systems, involve advanced materials, multilayer coatings, and precise integration with electronic controls.

This raises production expenses compared to conventional automotive glass, making it challenging for automakers to balance affordability with innovation. The higher pricing often limits adoption to premium and luxury vehicles, restricting widespread use in mass-market models.

In addition, the manufacturing complexity creates challenges for scalability. Specialized equipment, longer production cycles, and stringent quality standards increase operational costs for suppliers. These factors slow down large-scale commercialization and create barriers for automakers aiming to integrate smart glass across broader vehicle portfolios.

Opportunity: Advancements in Affordable Technologies and Emerging Markets

Advancements in affordable smart glass technologies are creating strong growth opportunities in the automotive market. Continuous innovation in materials, coating techniques, and electronic integration is reducing the cost of production. As economies of scale improve and manufacturers adopt streamlined processes, smart glass is becoming more accessible beyond luxury segments. This enables mid-range and even entry-level vehicles to incorporate advanced glazing features, broadening the customer base and increasing adoption rates across markets.

Emerging economies further enhance this opportunity. Rapid urbanization, rising disposable incomes, and increasing vehicle ownership in regions such as the Asia Pacific and Latin America are fueling demand for smart automotive solutions. Automakers entering these markets can leverage cost-effective smart glass to meet growing consumer preferences for modern, safe, and energy-efficient vehicles.

Category-wise Insights

Technology Type Insights

Electrochromic smart glass is projected to dominate the automotive market in 2025, accounting for around 45% of the total share. Its popularity stems from advantages such as energy efficiency, smooth light transmission control, and seamless integration with vehicle electronics.

Electrochromic glass is widely used in sunroofs, side windows, and windshields, particularly in premium cars, due to its ability to reduce glare, improve cabin comfort, and enhance aesthetics. The growing emphasis on energy savings in electric vehicles further reinforces its dominance.

On the other hand, Suspended Particle Device (SPD) glass is emerging as the fastest-growing technology segment. Its instant switching speed, superior heat management, and excellent shading capabilities make it highly attractive for luxury and high-performance vehicles. Increasing adoption in panoramic roofs and advanced concept cars highlights its strong growth potential in the coming years.

Application Insights

Sunroof glass is expected to dominate the automotive smart glass market in 2025, accounting for nearly 35% market share. The rising consumer preference for panoramic and larger sunroofs, particularly in mid-range and luxury vehicles, is driving this trend. Smart glass in sunroofs offers dynamic control of light and heat, enhances cabin aesthetics, and improves passenger comfort, making it a preferred choice among automakers. Its ability to reduce UV exposure and minimize air conditioning load also supports energy efficiency, especially in electric vehicles.

In contrast, the front and rear windshield segment is projected to be the fastest-growing. With advancements in heads-up displays, ADAS integration, and glare-reducing technologies, smart windshields are becoming crucial for safety and driver assistance. Automakers are increasingly adopting smart glass windshields to support connected and autonomous driving features, accelerating growth in this category.

End-use Insights

Passenger cars are projected to dominate the automotive smart glass market in 2025, holding nearly 60% of the share. The rising adoption of premium features such as panoramic sunroofs, advanced windshields, and smart windows in sedans and SUVs is driving this dominance.

Increasing consumer demand for comfort, safety, and luxury, along with the rapid growth of electric and hybrid passenger cars, further accelerates the integration of smart glass technologies in this segment. Automakers are leveraging smart glass to differentiate models and meet evolving customer expectations.

Commercial vehicles are emerging as the fastest-growing segment. Growing investments in connected fleets, smart logistics, and passenger comfort in buses and coaches are encouraging adoption of smart glass solutions. Features such as glare reduction, heat control, and enhanced visibility improve driver safety and passenger experience, making smart glass increasingly attractive for commercial applications.

Regional Insights

North America Smart Glass in Automotive Market Trends

North America is projected to dominate the automotive smart glass market in 2025 with a 60% share, driven by strong demand for premium and electric vehicles. The presence of leading automakers and technology providers, coupled with high consumer preference for advanced comfort and safety features, fuels adoption.

Regulatory emphasis on energy efficiency and safety standards further supports integration of smart glazing in vehicles. Additionally, the rapid penetration of EVs in the U.S. and Canada, supported by government incentives and infrastructure investments, accelerates the use of electrochromic and SPD glass in sunroofs, windshields, and windows, reinforcing the region’s leadership.

Europe Smart Glass in Automotive Market Trends

Europe holds a significant share of the automotive smart glass market, supported by the strong presence of luxury and premium car manufacturers such as BMW, Mercedes-Benz, and Audi. The region’s emphasis on sustainability, energy efficiency, and advanced automotive technologies drives wider adoption of smart glazing solutions in passenger vehicles.

Strict EU regulations on vehicle emissions and safety further encourage automakers to integrate energy-saving features such as electrochromic and SPD glass. In addition, the growing penetration of electric and hybrid vehicles, combined with rising consumer demand for comfort and high-tech driving experiences, reinforces Europe’s position as a key market for smart glass.

Asia Pacific Smart Glass in Automotive Market Trends

Asia Pacific is emerging as the fastest-growing market for automotive smart glass, driven by rapid urbanization, rising disposable incomes, and increasing vehicle ownership. Countries such as China, India, and Japan are witnessing strong demand for electric and premium vehicles equipped with advanced features such as smart sunroofs and windshields.

Government initiatives promoting electric mobility and stringent safety regulations further accelerate adoption. Additionally, growing consumer awareness about energy efficiency, cabin comfort, and glare reduction is driving interest in electrochromic and SPD glass technologies. The combination of expanding automotive production, technological advancements, and supportive policies positions Asia Pacific as a high-growth region in the smart glass market.

Competitive Landscape

The global smart glass in automotive market is competitive, with companies focusing on innovation and improving product functionality. Key efforts include enhancing light and heat control, boosting energy efficiency, and increasing passenger comfort.

Manufacturers are also pursuing collaborations, partnerships, and production expansions to strengthen their presence. While advanced smart glass solutions are widely adopted in premium vehicles, there is a growing focus on developing cost-effective options for mid-range models, enabling broader accessibility and supporting steady market growth.

Key Developments

- September 2024: Ford’s F-150 Lightning, a fully electric pickup, recorded a 104.5% sales increase compared to the same period in 2023. This surge highlights growing consumer demand for advanced features in electric vehicles, including smart glass technologies that enhance comfort and energy efficiency.

- July 2025: Gauzy Ltd. launched a prefabricated smart glass stack combining dimmable films, conductive layers, and adhesive interlayers into a single unit. The innovation aims to simplify manufacturing and accelerate adoption of dynamic smart glazing solutions in electric and connected vehicles.

- April 2025: Research Frontiers Inc. showcased SPD-SmartGlass technology in the Mercedes-Benz Vision V concept car, integrating smart glass across most of the glazing. This enhances passenger comfort, energy efficiency, and premium vehicle appeal.

Companies Covered in Smart Glass in Automotive Market

- Corning Inc.

- Guardian Industries

- Saint-Gobain SA

- AGP Glass

- Hitachi Chemical Co. Ltd

- Research Frontiers Inc.

- Nippon Sheet Glass Co. Ltd

- AGC Inc.

- Gentex Corporation

- Gauzy Ltd.

- Others

Frequently Asked Questions

The smart glass in automotive market is projected to reach US$3.2 bn in 2025, driven by EV adoption and smart vehicle features.

Rising EV production, consumer demand for comfort, and regulatory focus on energy efficiency fuel market growth.

The smart glass in automotive market will grow from US$3.2 bn in 2025 to US$10.8 bn by 2032, with a CAGR of 19.0%.

Advancements in affordable technologies and emerging market expansion drive opportunities in EVs and luxury vehicles.

Leading players include Corning Inc., Guardian Industries, Saint-Gobain SA, AGP Glass, Hitachi Chemical Co. Ltd, Research Frontiers Inc., Nippon Sheet Glass Co. Ltd, AGC Inc., Gentex Corporation, and Gauzy Ltd..